U.S. Debt and Bankruptcy

Economics / US Debt Apr 23, 2010 - 11:29 AM GMTBy: Andy_Sutton

There has never been as much attention paid to the situation of a looming American bankruptcy since the National Debt Clock made its debut many moons ago. It is hard these days to pick up a newspaper or look at a TV program without hearing someone mention our massive debt. And they’d be correct in saying we’re in big trouble. Numerous articles have asked the question ‘Is America Bankrupt?’ While bankruptcy on a family or individual scale is a fairly simple construct to grasp, such is not the case when it comes to a nation or group of nations, as is the case in Europe. This week’s essay is dedicated to making a rather complex question a little easier to understand, and more importantly – to arrive at a more definitive answer.

There has never been as much attention paid to the situation of a looming American bankruptcy since the National Debt Clock made its debut many moons ago. It is hard these days to pick up a newspaper or look at a TV program without hearing someone mention our massive debt. And they’d be correct in saying we’re in big trouble. Numerous articles have asked the question ‘Is America Bankrupt?’ While bankruptcy on a family or individual scale is a fairly simple construct to grasp, such is not the case when it comes to a nation or group of nations, as is the case in Europe. This week’s essay is dedicated to making a rather complex question a little easier to understand, and more importantly – to arrive at a more definitive answer.

Probably the most misleading of conclusions is to simply point at the national debt and declare America to be bankrupt. While there is no denying that America is in big trouble with its national debt that will not be what causes bankruptcy. Think of it on a micro scale - a family. Family X has $120,000 per year in revenues and $150,000 in expenses. Let’s say for the sake of simplicity that the family replicates these figures for 4 years. At the end of the 4 years, Family X’s debt (not counting interest payments) will be 100% of its revenues. Is Family X bankrupt? Absolutely not. Truth told, this family could continue to run these annual deficits as long as someone is willing to give them $30,000 in loans each year, dismissing debt service payments for simplicity.

For some reason when it comes to looking at Sovereign debt and debt ratios, the number always used as a benchmark is GDP. I am uncomfortable using GDP in creating a quantitative measurement of solvency since GDP is not some cash account from which public debt may be paid off. GDP is a rather convoluted measure of output, not an expense account. Since the Federal government has assumed this debt on behalf of you and I (a whole OTHER issue), they (we) are responsible for paying it back. Therefore, since the government is on the hook, we need to be looking at the government’s revenues, not GDP when making judgments on the veracity of the government’s financial position.

In fiscal year 2009, the US Government had revenues of $2.198 Trillion. This was a decrease of $463 Billion from FY 2008 according to the Treasury’s Financial Report of the US Government report. The outstanding debt as of this writing is $12.87 Trillion making the debt/revenue ration 5.85. This is a whole lot worse (and much more accurate) than saying that debt is 90% of GDP. As bad as it is having an outstanding debt that is roughly 600% of revenue, it doesn’t even begin to address the issue of bankruptcy.

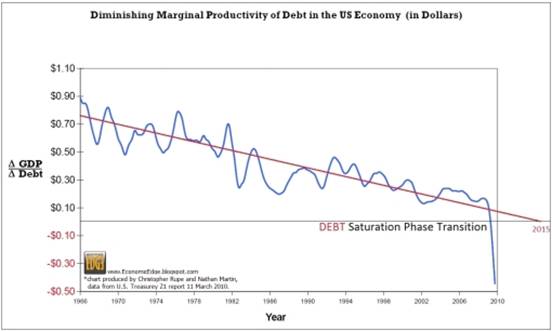

Marginal Utility of Debt Turns Negative

The underlying graphic has been seen in many different places, and with good reason. One of the biggest justifications of borrowing money in any situation is to cause growth. What has become apparent, however, over the past 5 decades is that the utility at the margin has diminished. What this means is that our ‘bang for the buck’ has disappeared. For example, back in 1966, a dollar of debt resulted in nearly $.90 in GDP growth. Today, adding a dollar of debt results in an over $.40 contraction in GDP. While this doesn’t have a direct bearing on national bankruptcy per se, what it is telling us is that our borrowing addiction is now cannibalizing economic growth. Small wonder. However, since economic output has a direct bearing on government revenues vis a vis tax receipts, the broken debt function will sit like an albatross upon our backs as we try to negotiate this brave new world.

We see evidence of the recognition of this reality in Washington as policymakers of varying stripes try to justify a value-added tax to close the gap and give the impression that we are, in fact, serious about austerity. No, this isn’t a joke. As usual, our government is making more colossal mistakes. Of course, real austerity would mean cutting government spending, but it should be clear to all that we will get nothing of the sort; from either bunch.

So, What Exactly is it that Constitutes Bankruptcy?

According to the Kotlikoff-Auerbach model, which is a variant of Irving Fisher’s Two Period Life Cycle Model work circa 1930, the current fiscal gap is approximately $185 Trillion. That number is a week old. Back in July of 2006, the fiscal gap stood at $65.9 Trillion. Anyone see a problem here? This gap analysis includes the full complement of social insurance programs including the new healthcare plan, military spending on wars for global empire, other domestic entitlements, and pretty much anything else you can think of that the Federal government might be involved in. The model looks at future revenues and outlays well into the future using current law and policy and uses the Net Present Value equation to bring the future amounts into present dollars.

To what extent will the Federal government be able to take the output of producers in the economy and dedicate it towards payment of these bills? We were cutting it very close when the number stood at $65.9 Trillion 4 years ago. Instead of addressing it then, we chose to do nothing. $185 Trillion is an unfathomable amount of money, especially for a government that takes in around 1/90 of that each year in tax revenue. And it is a lot for a country, whose total assets don’t even amount to 1/3 of our tab. Simply raising taxes won’t do it. The more marginal tax rates rise, the less incentive there will be to produce in following the old economic wisdom that you always get less of what you tax and more of what you subsidize. The historical landscape is littered with examples of how raising marginal tax rates actually causes tax revenues to decrease. So much for the idea of the VAT saving the day. Taking corporate profits won’t do it either. Raise taxes on corporations and they’ll lay off more employees, raise finished goods prices, and consumption will fall in proportion. So that isn’t going to work either.

An Undesirable Solution

The only real solution to this mess would be to essentially kill off Social Security, Medicare, and Medicaid benefits beyond what those programs actually take in each year on a cash basis. Going hand in hand would be the assumption that the contribution rates of these programs would remain the same. Pay 85% of benefits based on what the forecast is for the program’s revenue for a year, then give recipients a ‘catch-up’ payment at the end of year based what was actually taken in. Then start the next year with a clean slate. No unfunded liabilities. Period. At the same time, government would be turned into a flying gas can, being allowed to spend on only the barest of essentials.

Can you see the myriad of problems that lie in such a course of action? Forget the fact that it would be political suicide for anyone to propose this, which is the only reason I can get away with it – I’m not running for office. The culling of government would result in massive unemployment, with essentially no way to pay the benefits. The same would be true for private sector unemployment. The program cuts in social insurance would put most families over the edge since so many people rely on them. Ostensibly, we have no savings as a nation, with more than 4 in 10 having less than $10,000 set aside for retirement or any type of life emergency. In short, too many people rely on these programs making the social insurance Ponzi scheme too big to fail. At the same time, the sheer magnitude of these programs makes them too big to save.

Fundamentally, the question of American bankruptcy (or any for that matter) becomes the simple matter of looking at the bills that need to be paid and determining if they can in fact be paid. They certainly can’t be paid with revenues; we know that. We are already borrowing heavily and there is no indication that will change. Getting back to the earlier example of Family X, conventional analysis keeps telling us that some time uncertain, such a system arrives a point where there is simply not enough money in the system for external lenders to perpetuate it.

Points to Ponder

For all intents and purposes that has already in fact happened and the Fed is currently monetizing roughly 80% of Treasury auctions and bribing banks NOT to lend to the public by paying them interest on the reserves they keep at the Fed. This is all done to avoid what would normally turn into a hyperinflationary explosion. The bills cannot be paid. America is bankrupt. And we’re not alone. This is one of the reasons I wrote two weeks ago that we’re going to likely see a coordinated devaluation of currencies and then default as central banks slam the door on monetary creation. The monetary aggregates are already showing signs of this. It will not be pretty. At the same time expect more cuts in programs like Medicare, Medicaid, and Social Security. The money will simply not exist to pay all the promised benefits. It will be an in situ default.

There will be those who will say that the above thesis is baloney and that it will be hyperinflation forever and ever. We are so much smarter than we were back in the 1930’s and we should have never allowed that nasty deflationary collapse to occur. However, the debt bubble that exists today on a global scale is several orders of magnitude larger than what existed back then and believe me, banks and governments knew back in the 1930’s about over-issuing paper currencies.

Our national history is littered with these little experiences of wanton money creation. They never ended well. However, looking at it through that lens, the 1930’s allowed the banking elite to ‘reset’ the system and squeeze another 70+ years out of an already broken monetary model. However, the only reason we made it this far is because the first 30 or so of those years we were giving away the national treasure in the form of our Gold to foreigners for the right be the consumers of the world. History doesn’t always repeat, but it sure does rhyme. I certainly don’t have a crystal ball (or inside info for that matter), but to me, the above thesis makes a good deal of sense especially given the untenable financial position we find ourselves in.

We already have what amounts to the sovereign debt equivalent of a commercial signal failure in the case of Greece, and it doesn’t take much thought to come up with the conclusion that nobody wants to step up and bail out an entire country and start the avalanche. It may well end up being that the default occurs for no other reason than it is the path that provides the least resistance.

By Andy Sutton

http://www.my2centsonline.com

Andy Sutton holds a MBA with Honors in Economics from Moravian College and is a member of Omicron Delta Epsilon International Honor Society in Economics. His firm, Sutton & Associates, LLC currently provides financial planning services to a growing book of clients using a conservative approach aimed at accumulating high quality, income producing assets while providing protection against a falling dollar. For more information visit www.suttonfinance.net

Andy Sutton Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.