Global Gold Demand in 2011 Rises 0.4% To $200 Billion - Central Banks, Asia and Europe Diversifying Into Gold

Commodities / Gold and Silver 2012 Feb 16, 2012 - 10:02 AM GMTBy: GoldCore

Gold’s London AM fix this morning was USD 1,716.00, EUR 1,320.51, and GBP 1,094.74 per ounce.

Gold’s London AM fix this morning was USD 1,716.00, EUR 1,320.51, and GBP 1,094.74 per ounce.

Yesterday's AM fix was USD 1,725.50, EUR 1,309.88, and GBP 1,099.33 per ounce.

The World Gold Council released its comprehensive report today, “Gold Demand Trends Q4 and Full Year 2011” looking at demand in gold demand in full year 2011 and the 4th quarter of 2011.

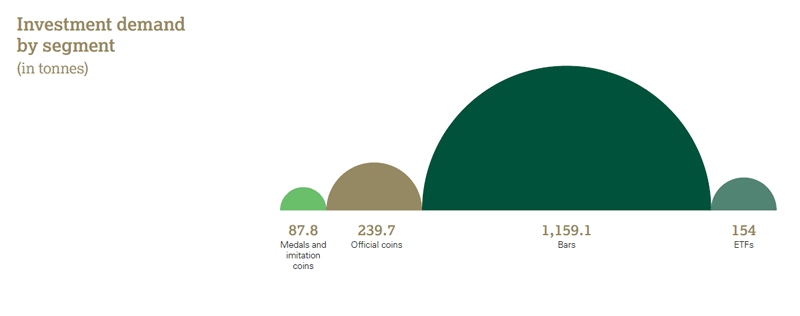

Global Gold Investment Demand - Bar and Coin Demand Larger Than ETF Demand Which Remains Small

The report is 32 pages long and well worth a read if you wish to be informed about the fundamentals of the gold market.

Executive Points

Here are the key points which we have garnered from reading the report:

Global demand for gold in 2011 rose a very sustainable and gradual 0.4% to 4,067.1 tonnes.

Global gold demand was worth a mere US$205.5 billion which is not a substantial sum considering the size of global capital markets today. It was the first time that global demand has exceeded US$200 billion and the highest tonnage level since 1997.

Central banks were net buyers of gold and their demand surged nearly 6 fold (570%) to 439.7 tonnes in 2011 - compared with 77 tonnes in 2010.

Demand from the investment sector was the driving force behind demand for gold reaching a 14-year high in 2011.

The investment sector saw annual demand of 1,640.7 tonnnes up 5% on the previous record set in 2010 and with a value of US$82.9 billion.

Demand for gold bars and coins accelerated, reflecting a blend of positive influences including concern over the financial health and future viability of the euro area; high inflation in some countries; positive price expectations; and the relatively poor performance of a range of alternative investments.

Investment demand globally surpassed the record high of 2010, with China, India and interestingly Europe (primarily Germany and Switzerland) all reporting record levels of demand in 2011.

Investment was the main driver of growth, although jewellery and technology were resilient despite higher and record nominal prices.

Mine production, while rising to a record, increased minimally and was offset by lower recycling activity and significant central bank purchases.

Specifically, European investment demand experienced its seventh consecutive annual gain and accounted for one quarter of all global gold retail investment in 2011.

Demand for gold bars and coins globally contributed to strong investment demand, substantially increasing year-on-year in both volume and value terms.

Investment demand for gold is likely to remain high throughout 2012 as global economic uncertainty, low interest rates and high inflation in many economies reinforce the attraction of gold’s diversification properties.

Central bank were net buyers and had demand which hit their highest amount in forty years.

Buying in China should overtake India this year as the world’s top consumer of the yellow metal.

In Q4 2011, China consumed 190.9 tonnes of gold, compared with India's 173.0 tonnes, ranking China top in terms of consumption, something the WGC had not expected last year.

The data and info graphic show the continuing and often underestimated role of gold coin and bar demand over ETF demand which remains quite small vis-à-vis coin and bar demand and small vis-à-vis other markets

Investment Demand

Global demand for gold reached 4,067.1 tonnes last year, the highest tonnage since 1997, due in large part to a nearly 5% increase in investment demand, which hit a record 1,640.7 tonnes.

Asian countries like China, India, Vietnam, Thailand and others see bullion as a store of value against the growing inflation and the ongoing debasement of their currencies.

The fundamentals for gold in 2012 look good. Continuing low and often negative real interest rates will continue to support gold’s safe haven status. The Fed’s statement that it will continue to see rates remain very low until 2014 is very bullish for gold.

Central banks were net buyers of gold and their demand surged nearly 6 fold (570%) to 439.7 tonnes in 2011 (compared with 77 tonnes in 2010), more metal than at any time since the end of the gold standard in 1971.

The World Gold Council noted that, “The buyers are all ... in Latin America, Asia and the Far East and they are basically enjoying strong growth, fiscal surpluses and growing foreign exchange reserves."

European Demand on Eurozone Debt Crisis

Financial instability and elevated sovereign, monetary and systemic risk continues leading European investors to increasing their purchases of bullion in the form of coins and bars.

The WGC reported that European demand rose by more than 25% year on year to 374.8 tonnes in 2011, with Switzerland and Germany being the main drivers in the region.

Gold demand in the UK and Ireland remains lack lustre – although the data remains poor in this regard.

The ‘Other Europe’ category of demand, at 23.4 tonnes for Q4 and 90.8 tonnes for 2011, now accounts for a considerable proportion of investment in Europe. A substantial amount of this new demand has been generated by countries with previously no or very little interest in gold investment, including the UK and Ireland and a number of Eastern European countries. In value terms, annual demand from the markets grouped within this category amounted to a very small €3.3bn.

Demand for gold in ETF products reached a net 154 tonnes in 2011, compared with 367.7 tonnes in 2010, although more than 1/2 of that total’s investment was solely Q4 of last year alone, when ETP demand accounted for 86.8 tonnes.

Jewellery Demand

Global jewellery demand totalled 476.5 tonnes in the fourth quarter of 2011, a 15% year-on-year decline. In value terms, demand was 5% higher at US$25.9bn, a new quarterly record. On a full-year basis, tonnage demand of 1,962.9 was 3% below 2010, showing resilience given a 28% increase in the average annual price. The value of annual demand grew by 25% to a new record of US$99.2bn

Technology Demand

Gold demand in the technology sector declined 3% year-on year in the fourth quarter of 2011 to 112.3 tonnes, the lowest quarterly figure since the third quarter of 2009. In value terms, this translated to a 19% year-on-year increase to US$6.1bn. Annual demand was measured at a broadly steady 463.5 tonnes, comfortably above the 456.3-tonne average of the preceding five year period. The value of 2011 demand surged 28% and reached a record US$23.4b.

Gold Supply

On the supply side, gold mine output rose just 4% (yoy) but reached a new annual record of 2,809.5 tonnes last year.

The WGC reported that the producer hedge book increased marginally for the first time in a decade last year, with 18 tonnes of hedging added to the estimated outstanding global hedge book of 158.0 tonnes.

Recycling remained high and fell just 2% on the year to 1,611.9 tonnes showing that the ‘(wo)man on the street’ and much of the retail public in many western countries continues to sell gold.

Conclusion

The figures and data shows that the fundamentals of the gold market remain very sound with global demand having increased gradually and sustainably and supply remaining restrained.

Importantly, most of the buying was buy store of wealth and long term diversifiers (Asian and European coin and bar buyers and central banks). This is not ‘hot’ speculative money and therefore this gold is in strong hands and unlikely to be sold for some time.

The recent increase in demand have been very gradual in tonnage terms and is very sustainable given the extremely low level of gold bullion ownership internationally and particularly in the western world. Allocations to gold in global investment portfolios remain negligible.

This in conjunction with a global sovereign debt crisis centred on the appalling fiscal position of most industrialised nations, the risk of global recessions and or a Depression and very significant counter party and systemic risk means that gold’s bull market looks set to continue for the foreseeable future.

World Gold Council: “Gold Demand Trends Q4 and Full Year 2011” Full Report can be read here.

For breaking news and commentary on financial markets and gold, follow us on Twitter.

SILVER

Silver is trading at $33.07/oz, €25.48/oz and £21.12/oz.

PLATINUM GROUP METALS

Platinum is trading at $1,604.00/oz, palladium at $675/oz and rhodium at $1,500/oz.

For the latest news and commentary on financial markets and gold please follow us on Twitter.

GOLDNOMICS - CASH OR GOLD BULLION?

'GoldNomics' can be viewed by clicking on the image above or on our YouTube channel:

www.youtube.com/goldcorelimited

This update can be found on the GoldCore blog here.

Yours sincerely,

Mark O'Byrne

Exective Director

IRL |

UK |

IRL +353 (0)1 632 5010 |

WINNERS MoneyMate and Investor Magazine Financial Analysts 2006

Disclaimer: The information in this document has been obtained from sources, which we believe to be reliable. We cannot guarantee its accuracy or completeness. It does not constitute a solicitation for the purchase or sale of any investment. Any person acting on the information contained in this document does so at their own risk. Recommendations in this document may not be suitable for all investors. Individual circumstances should be considered before a decision to invest is taken. Investors should note the following: Past experience is not necessarily a guide to future performance. The value of investments may fall or rise against investors' interests. Income levels from investments may fluctuate. Changes in exchange rates may have an adverse effect on the value of, or income from, investments denominated in foreign currencies. GoldCore Limited, trading as GoldCore is a Multi-Agency Intermediary regulated by the Irish Financial Regulator.

GoldCore is committed to complying with the requirements of the Data Protection Act. This means that in the provision of our services, appropriate personal information is processed and kept securely. It also means that we will never sell your details to a third party. The information you provide will remain confidential and may be used for the provision of related services. Such information may be disclosed in confidence to agents or service providers, regulatory bodies and group companies. You have the right to ask for a copy of certain information held by us in our records in return for payment of a small fee. You also have the right to require us to correct any inaccuracies in your information. The details you are being asked to supply may be used to provide you with information about other products and services either from GoldCore or other group companies or to provide services which any member of the group has arranged for you with a third party. If you do not wish to receive such contact, please write to the Marketing Manager GoldCore, 63 Fitzwilliam Square, Dublin 2 marking the envelope 'data protection'

GoldCore Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.