The Worst of All Monetary Policies, The Boom That Must End in Depression

Interest-Rates / Quantitative Easing Apr 08, 2012 - 03:54 PM GMTBy: Thorsten_Polleit

I. Monetary Expansion Is Kept Going

I. Monetary Expansion Is Kept Going

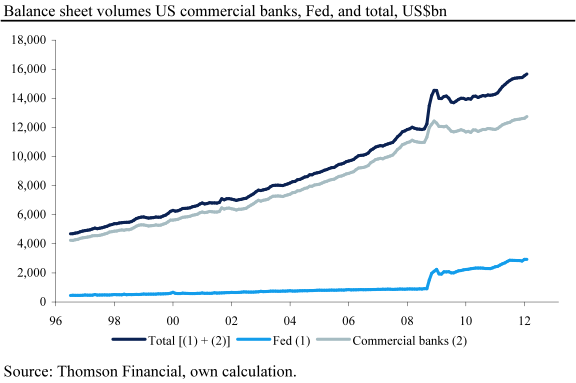

In monetary analyses, the balance sheet of the commercial banking sector is typically kept separate from the balance sheet of the US Federal Reserve (Fed). However, combining the two balance sheets might be much more informative.

First, adding up the business volumes of commercial banks and the Fed provides a (much) better insight into the expansion of the monetary sector as a whole over time — especially so in times of the financial and economic "crisis."

Second, such an aggregation reveals that in times of crisis the central bank unmistakably puts the interest of the banking industry first, with its policy aimed at "restoring the banking sector back to health."

The expansion of the Fed's balance sheet as from the end of 2008 onwards has not only helped prevent the banking industry from shrinking; it has kept the expansion of the monetary system going, as shown by the chart below.

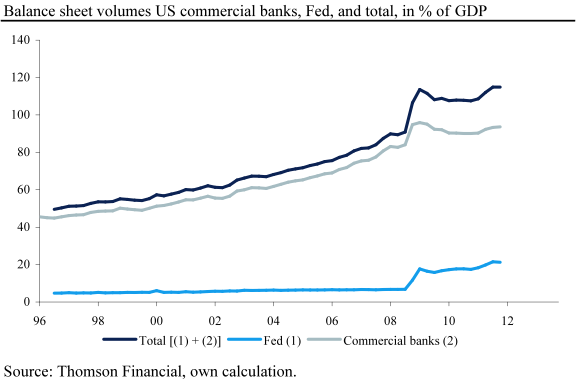

The Fed has expanded its balance sheet through providing additional credit to the commercial-banking system and purchasing (government and mortgage) bonds from banks and nonbanks. As a result, the combined balance sheet of commercial banks and the Fed rose to a record high of close to 115 percent of GDP in Q4 2011.

II. The Increase in the Stock of Payments

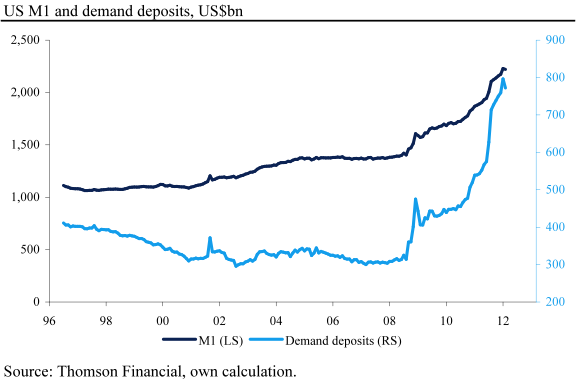

The expansion of the aggregated balance sheet of commercial banks and the Fed has been accompanied by a rise in the stock of payments in the form of M1. It has increased by 58 percent from August 2008 to February 2012.

Within M1, demand deposits went up from $314 billion to $772 billion, a rise of 146 percent. The increase in the means of payment may be in part due to the extraordinarily low interest rates (that is, the extraordinarily low opportunity costs of money holdings).

However, it may also be due to the Fed's purchases of bonds from so-called nonbanks (for instance, private households, pension funds, and insurance companies). Under such operations the Fed increases the means of payments directly; it is a policy of increasing money by actually circumventing bank credit expansion.

The marked increase in the stock of payments in recent years is an unmistakable sign of what can be called, economically speaking, inflation, a view held by the Austrian School of economics.

A rise in the money stock leads, and necessarily so, to a decline in the purchasing power of a money unit — when compared with a situation in which there had not been a change in the money stock.

Most important, a rise in the money stock actually prevents a rise in the purchasing power of money — which would have occurred had the Fed not ramped up the means of payments in the hands of commercial banks and nonbanks.

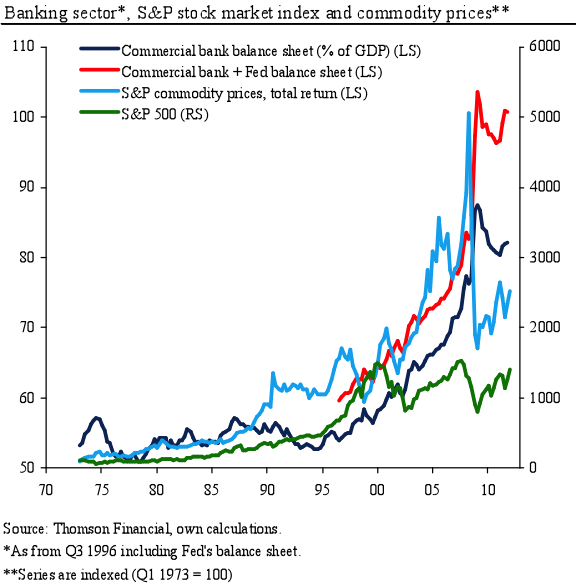

The rise in the money stock can be expected to translate into higher prices — be it prices for consumer goods (via, for instance, higher commodity prices) or prices for assets (such as stocks and real estate).

Rising prices erode the purchasing power of money and do great harm to the (coordination) function of market prices, thereby provoking misinformed decision making of market agents, causing malinvestment.

Such a policy is by no means neutral. The winners of the Fed's policy are, for instance, the holders of goods and assets that are prevented from declining in prices, while the losers of the Fed policy are money holders: they have been prevented from buying at lower prices.

III. The Boom That Must End in Depression

The ongoing expansion of the money supply — a monetary policy of going well beyond measures of just keeping the money stock from shrinking — is indicative of attempts to keep the boom, caused by bank circulation credit expansion, going.

However, such a policy will not cure the economic and political malaise brought about by bank-circulation credit expansion in the first place. In fact, such a monetary policy will make things much worse going forward.

It will not only pave the way toward a deep depression, through which the economy will finally be brought back to equilibrium; it will also ruin the currency. Ludwig von Mises (1881–1973), in Interventionism: An Economic Analysis (1940), noted,

The boom cannot continue indefinitely. There are two alternatives. Either the banks continue the credit expansion without restriction and thus cause constantly mounting price increases and an ever-growing orgy of speculation, which, as in all other cases of unlimited inflation, ends in a "crack-up boom" and in a collapse of the money and credit system. Or the banks stop before this point is reached, voluntarily renounce further credit expansion and thus bring about the crisis. The depression follows in both instances.[1]

Against this backdrop, the conclusion is that the monetary policy of continuing to expand the money supply through bank-circulation credit provided at artificially lowered interest rates is actually the worst of all monetary policies.

Thorsten Polleit is Honorary Professor at the Frankfurt School of Finance & Management. Send him mail. See Thorsten Polleit's article archives. Comment on the blog.![]()

© 2012 Copyright Ludwig von Mises - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.