U.S. Dollar Debt Tipping Point to Price Inflation

Commodities / Gold and Silver 2010 Mar 23, 2010 - 01:16 PM GMTBy: Jim_Willie_CB

The USEconomy is bifurcated, with price inflation advancing on the cost side while price deflation harms on the asset side, to produce a nasty storm that is unlikely to abate. When high pressure zones clash with low pressure zones, hurricanes and tornadoes occur. Calling the resulting near 0% or low 2% price inflation on a net basis a good sign completely ignores the forces pulling the national economy apart. Economists prefer to view the landscape in aggregate, but they miss the picture composed of two important parts enduring very different forces. The financial sector has grotesquely grown, to an extreme.

The USEconomy is bifurcated, with price inflation advancing on the cost side while price deflation harms on the asset side, to produce a nasty storm that is unlikely to abate. When high pressure zones clash with low pressure zones, hurricanes and tornadoes occur. Calling the resulting near 0% or low 2% price inflation on a net basis a good sign completely ignores the forces pulling the national economy apart. Economists prefer to view the landscape in aggregate, but they miss the picture composed of two important parts enduring very different forces. The financial sector has grotesquely grown, to an extreme.

Global financial assets have more than tripled since 1980, relative to GDP. In just this past decade, the volume of Credit Swap Contracts (asset backed bond insurance) increased five-fold in a span of four years. The base value of equity derivatives (stock index contracts) increased almost five-fold in the same four years. Leverage has also grown.Tremendous flaws exist in the prevailing economic counsel that misguides the nation, into one phase of disaster after another. Crisis is indeed the norm.

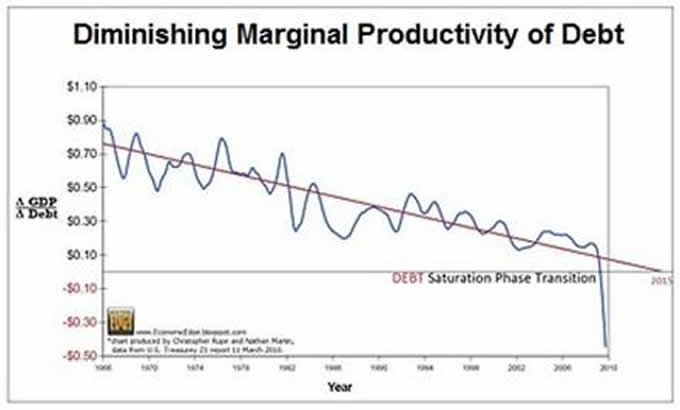

THE FAILED EFFECT OF NEW DEBT

The maestros believe that new money or new debt (hard to tell the difference) can be created, and presto change-o, the USEconomy rebounds. The new money production line is disconnected from the tangible economy. The bankers can thus can tap federal liquidity facilities and ignore their borrowing customers. The banking authorities are resisting the solution, for the clear reason that many from their sector would be destroyed and their power eradicated. The US Federal Reserve has overseen vast money printing for years, and a continuous climax in the past two years. A crescendo awaits.

A tipping point comes, when all the USGovt deficits, all the USTreasury Bond issuance, all the US bank failures lead to a economic recovery, as profound change comes in international sentiment toward the USDollar. They will exit, since the US markets are not permitted to clear, to liquidate, to enjoy the fresh breeze inherent to capitalism. Financial markets throughout the entire USEconomy are essentially frozen. A huge waiting game has emerged between the expectant beneficiaries of USFed efforts to stimulate inflation and economic participants. In the process, the USEconomy deteriorates further.

Consider the shocking graphic above. The resulting impact of new debt in the USEconomy is actually negative. If the 0% official interest rate and the $1.5 trillion federal deficit do not convince the observer of failed policy, failed remedy, and failed structural beams within the system, then this chart should help. The effect of a new US$ of debt is actualy minus 45 cents in economic activity. The engines of debt are totally broken, the saturation levels reached. Ironically and tragically, the response from American leadership will be to press the monetary pedal even harder, thus achieving even worse results. Where is Paul Samuelson now, when his incorrect quantitative theory of money has been discredited? His Nobel Prize should be removed and replaced with a thousand foreclosure notices bound and sealed.

INFLATION VS DEFLATION AT THE TIPPING POINT

James Rickards is Director for Market Intelligence at Omnis, a private analysis group. Rickards is a superstar analyst in my view, quoted in the past in the Hat Trick Letter. He has previously commented upon the justification for a 30% to 50% USDollar devaluation, given all the extreme federal deficits and extensive future obligations. Here he argues that the USEconomy is bifurcated, with price inflation advancing on the cost side while price deflation renders harms on the asset side, to produce a nasty storm that is unlikely to abate. Calling the resulting near 0% or low 2% or climbing to 3% price inflation on a net basis a good sign completely ignores the forces pulling the national economy apart. Its structural defects are not being repaired. Such aggregate views actually point out the spectacular ignorance of US economists, who fail to recommend meaningful remedy, like job creation tax credits, like the return of all US jobs sent to Asia, like elimination of credit derivatives. Ours is nation of ignoramuses running the banking and economic policy, for the benefit of the syndicate.

Rickards builds a foundation that the financial sector has grown to the grotesque. He makes a grand alert that in this dynamically complex system, the size of the maximum potential catastrophe is exponentially greater than ever. He calls it inescapable. Imagine a pendulum swing left and right, with each move farther and higher, producing greater supposed wealth and prosperity on the positive swing but greater recognized destruction and poverty on the negative swing.

Here are some facts to point out the extraordinary extremes that make return to normalcy impossible. The ratio of world financial assets to world GDP grew from 100% in 1980 to 200% in 1993 to 316% in 2005. Over the same 25 year period, the absolute level of global financial assets increased from $12 trillion to $140 trillion. The total notional value of all credit swap contracts (bond insurance) increased from $106 trillion to $531 trillion between 2002 and 2006. The notional value of equity derivatives (stock index contracts) increased from $2.5 trillion to $11.9 trillion over the same period, while the notional value of credit default swaps increased from $2.2 trillion to $54.6 trillion. Margin debt of US brokerage firms more than doubled from $134.6 billion to $293.2 billion from 2002 to 2007, while the amount of total assets per dollar of equity at major US brokerage firms increased from approximately $20 to $26 in the same period. To say that such extensions represent fantastic and monstrous leverage is a gross under-statement. Resolving the current extreme situation is not possible or feasible.

In reaction to financial crises, the emphasis has been on Wall Street taking charge with market controls and on the US Federal Reserve handling needs with vast printed money. Financial markets are not functioning properly, since interventions are the norm and accounting rules are suspended. These rules are likely to be even further suspended with the commercial loan fiasco in progress, with fresh losses to deal with. Remedy and reform are not permitted, thus recovery is an impossibility. Toxic assets sit on bank balance sheets, along with foreclosed properties. The financial markets are not clearing, and that is precisely the jam in the engine against which powerful monetary pressures are building. The banking authorities are resisting the solution, for the clear reason that many from their sector would be destroyed and their power eradicated.

Rickards believes two extreme choices are presented, and only extreme outcomes await. He said, "So while we may have temporarily halted the slide, we have not done anything to solve our problems, which means it is just a matter of time before one of two things happen. Either the slide resumes and we finally arrive at the market bottom that we never hit in 2009, or they keep printing money to paper it over, eventually destroying the dollar and undermining the entire economy. Those are the choices.

What the Fed wants is the one thing they are not going to get: Mild inflation. They are desperately trying to get some inflation going because they are scared to death of deflation. All of their Quantitative Easing [debt purchase with newly printed money] and special programs with the Treasury and the fiscal stimulus are designed to weaken the dollar. They are basically trying to scare the markets into spending money. But right now, all Americans want to do, naturally, is save money, de-lever, pay down debt. All very sensible things to do on an individual basis. But when you do that, in a world where consumption is 70% of GDP, your GDP is going to collapse. That is reflected in the velocity of money.

The whole notion that you can dial up nominal GDP by increasing the money supply rests on another false assumption, which is that velocity is fairly constant. Velocity has dropped through the floor."

The perverted umbilical cord in the Fascist Business Model directs money from the USGovt straight to the big banks, big defense contractors, even the big pharamaceutical firms. Rickards points out the frightening current situation that the USGovt is printing money at unprecedented fast pace, but it cannot revive the housing market, cannot revive business lending, cannot bring the banks back to a solvent condition, and cannot produce price inflation.

Rickards avoids mention of other sources of inflation such as the USGovt reckless spending, the USGovt coverage of AIG and Fannie Mae black hole losses, the USDept Treasury constant investment in financial market interventions, the USFed vast array of liquidity facilities, and the endless USMilitary obscene spending. His central point should be stressed, that a TIPPING POINT comes. If the USGovt and USFed halt their extreme financial support, then deep contraction and reductions follow, complete with convulsions and spasms, in a melt-down. If trouble arises and the official response is amplified financial support, then fast rising price in key structures follows, including home prices and stock prices, in a melt-up. The USEconomy and its overlaid financial system are stuck in gear, the engine jammed hard. The infusion of new money will accelerate to the point of removing the jam. The sudden jerk will be felt as powerful price inflation that takes the nation off guard.

PARALLELS OF WEIMAR HYPER-INFLATION

Hyper-inflation remains a threat, as parallels are strong with 1922 in the Weimar Republic of Germany. Ben Bernanke has been set in contrast to Rudolf von Havenstein, the central banker responsible for Germany's hyper-inflationary period. The parallels are absolutely shocking between the US climate of 2010 and that of the infamous Weimar Republic. Despite 1922 being such a long time ago, the more advanced and sophisticated financial framework and government actions bear frightening parallels to the Weimar Republic. Grasp the parallels. They are as lengthy as they are ominous in foretelling price problems dead ahead.

Von Havenstein monetized debt from the German Govt after World War I, just like Bernanke monetizes the USGovt debt after the Wall Street collapse. The debt purchase dragged on long past the initial stop-gap of debt purchase with printed money, but the war dragged on, just like the insolvency of banks and housing drags on. VonH was praised as a hero, even granted a national hero award, like BenB as Man of the Year. Actions on the monetization path were difficult to stop since price inflation seems under control during the early stages. The national climate was very difficult and strained, with political factions deeply polarized, just like Democrats and Republicans in the USCongress. War Reparations were a huge factor in the debt to cover, just like Wall Street bank extortions and USGovt nationalizations (Fannie Mae, AIG, General Motors) are a huge factor. The mass unemployment and home loss tell a tale about domestic economic and political crisis on both fronts. VonH gave blame to external forces for their economist blunder, much like BenB blames hedge funds for his blunders. VonH Herr missed the connection between the continued issuance of new notes and the rise of commodity prices amidst foreign exchange rate volatility, just like BenB fails to comprehend the link between monetary growth and the oil price or US$ decline.

Claims of greater sophistication are empty and ring hollow. Former USFed Chairman Volcker uttered one of the funniest yet true insults to Wall Street last year. He accused the US bankers of making only one worthy innovation in 20 years, the automatic teller machine for cash dispensing. The US innovation in the financial sector bears no fruit. The US possesses worse, even more dangerous financial devices, and insists on revisionist history for looking at the triggers to the Great Depression. Fractional banking, excessive credit creation, leverage in stock market, foreign influence on US banks, these were principal causes, not the lack of liquidity as Bernanke insists, still stuck with hubris that he can control the inflation monster. BenB and his predecessors know only inflation, but Mother Nature is well along in delivering vengeance. This will end badly.

Badly bruised but undeterred, Tyler Durden of Zero Hedge wrote, "In fact, there is one very clear difference between the hand Von Havenstein had to play then and those today's central bankers have to play now, namely the stability of today's political climate. Clearly this can change, but the class warfare, nationalistic xenophobia, and revolutionary spirit poisoning the political atmosphere of 1920s Germany is at the very least dormant today, and certainly not meaningfully visible across the political landscape. But let's not ignore the parallels either. As is the case for today’s central bankers, Von Havenstein was faced with horrible fiscal problems. As is the case for today's central bankers, the distinction between fiscal and monetary policy had blurred. As is the case for today's central bankers, the political difficulty of deflating was daunting. And as is the case for today's QE-enthralled central bankers, apparently respectable economic theory reassured him that he was doing the right thing." The parallels are vast. See the Zero Hedge article (CLICK HERE).

Durden minimizes the parallel on the hostile toxic political atmosphere from 1922 Germany to US today, steeped with class warfare, xenophobia, and revolutionary spirit, just not as high pitched. The contrived strained story of the War on Terrorism (used to cover vast military contractor profiteering and contraband activity) has a strong hint of politically sanctioned nationalistic fervor that sponsors distrust and disdain for some ethnic and religious groups. Also, class warfare is seething under the US cultural fabric, as animosity and distrust of New York bankers and the USCongress is at an historical peak, ready to overflow. Also the US President cannot be seen in a press conference of speech without at least 15 US flags, the symbol of xenophobia. The European population well recognizes that superfluous flags as a symbol for fascism, something not understood in the United States. As for revolutionary spirit, see the Tea Parties and Tenth Amendment movements across several states. They demonstrate against high taxes, banker bailouts, and oversized government. Several states wish to exit the Union altogether, as they recognize the federalist powers are but a syndicate, whose agenda greatly differs from the people.

THE NEXT DREADED CHAPTER

Weimar Germany did not deal with credit derivatives, leveraged losses, an oversized financial sector, financial engineering gone haywire, and endless finanical firm bailouts. In that respect, the United States avoids a certain amount of new money from hitting the street and pushing up prices. The plan might be to starve the Main Street and its tangible economy until the fires from Wall Street end. That would involve a long wait. The new funds tossed into the USEconomic cauldron essentially neutralize the Black Holes one increment of time per treatment. They are almost entirely wasted, as the shocking negative productivity of debt demonstrates. The treatment of Black Holes from an imploded US leveraged financial structure, the tribute to Wall Street, results in mammoth hidden funds to neutralize their effects.

The USEconomy is more at risk to strong price inflation from the QE2 and the next round of money printing to manage the federal deficits, the new stimulus programs, meaningful home loan modification aid, and urgently needed credit lines WILL be inflationary in the sense that they do hit the street. Quantitative Easing will not go away, only talk of it going away. Recall drastically wrong past assessments. Remember the contained Subprimes? Remember the Green Shoots? Remember the sound equity basis of Wall Street firms? The nation is stuck, and new money will be urgently directed as needed. The next round of Quantitative Easing in England is a certainty, matched by the United States.

Conditions are going to break down. The major currencies are tied together, with no safe haven among them, surely not the USDollar. All the fiat currencies lie in the same basket floating at sea, part and parcel to the debt based monetary system. Threats of sovereign default and/or prolific money printing will spawn a global currency crisis with the USDollar at the epicenter. Debt denominated money will be exposed as a fraud. The climax comes with a USDollar collapse, an event written in stone, the end of the pathogenesis evolved from fiat money. My view is that Austrian theory is prevented from producing hyper-inflation yet, since the explosion of credit derivatives has so far prevented it, whose notional value at one time exceeded $1.4 quadrillion. The monetary press secretly covers such leveraged losses from Fannie Mae, AIG, and a collection of Wall Street giants. The fires will soon be treated with accelerant, as both the USGovt and the UKGovt succumb to pressures and announce the second phase of Quantiative Easing, the powerful monetary inflation they so vigorously deny as necessary.

GLOBAL GOLD BREAKOUT

Uncertainty over Greek sovereign debt lifted demand for gold bullion across Europe as a hard asset. The Euro currency is not fracturing, but rather consolidating as it removes superfluous fatty portions. The European Union is not fracturing, but rather consolidating as it removes the insolvent dead portions. In the process, as the monetary crisis spreads across Europe, gold has been elevated into a currency status.

Great volatility in the European currencies since the latter months of 2009 has prompted demand for gold, the true safe haven. Gold has traditionally served as the ultimate safe haven in times of political and financial uncertainty. A gold breakout has taken place over European soil. Despite a stabilizing exchange rate, the underlying sentiment behind the uncertain Euro has crept into the FOREX arena. The Gold price in Euros is pushing out new highs in a gradual process. A very clear bullish Cup & Handle reversal pattern indicates a sustained breakout. However, the breakout is tentative for Gold in Euros, probably due to the queer US$ benefit. The Gold breakout in price will occur last and most powerfully in US$ terms.

A multitude of extremely powerful factors is aligned to push the Gold price in Pound Sterling terms to new highs. UKGovt debt is out of control. Rescue for banks, economic stimulus, basic outsized federal deficits, and monetization of the finances work to produce a perfect storm. It will push up the Gold price. Reality is soon to strike Britain that not only is another firm Quantitative Ease round due, but the financial situation is not resolvable. Talk of UKGovt debt default will rise to a crescendo level. What happens to Britain will happen to the United States, but with a delayed timing. The next UK general election is expected to result in a hung Parliament. The absence of a firm leading coalition would have an equivalent effect of permitting blood to leak into the waters for all FOREX trading sharks to see.

The consensus is growing for QE2, another powerful round of monetary expansion to compensate for what Britain cannot execute, the accomplishment of a recovery or integration of effective reform. New sterling money must be created in order to buy UKGilt bonds, as gigantic deficits are to continue, forcing debt monetization longer than expected. The Gold price has taken flight over British soil, also in a gradual process. A different type of bullish Cup & Handle reversal pattern is evident, one with an even more bullish neckline tilt bias. It indicates a sustained breakout also. The Gold breakout in price will occur last and most powerfully in US$ terms.

A different story is told for Gold in Australian Dollars and for Gold in Canadian Dollars. My forecast is for the commodity currencies (Canadian & Australian Dollars) to outperform all major currencies in the next chapter of the Competing Currency War. In the process, a gold breakout in those currencies is not possible. One should remember that the Gold breakout in price will occur last and most powerfully in US$ terms.

The consolidation process appears to have come to an end. The 1100 price level has shown solid support since December except for two weeks, enough to permit the next upward thrust to take place. The rising moving averages confirm the trend. Watch the 20-week moving average, which has offered support in the latest assault on price with naked COMEX short positions. They continue to sell gold without benefit of gold collateral, protected by the USGovt and regulatory bodies controlled by Wall Street. When price inflation arrives in force, hardly the tepid variety, after the Tipping Point has been breached, the effect on the gold price will be astounding, remarkable, and breath taking.

Gold investors have been put to sleep. The grand wagon has seen many people fall off or jump off in the last two or three months, typical in the gold bull market. In a world with the USDollar sitting as global reserve currency, the main beneficiary in the Competing Currency War, the gold bull with US$ saddle is the last to run. Americans would do well to observe the gold price in European and British terms, but then again, perspective beyond the US shores is not a trait of its citizens. A small proportion own passports, and a small proportion speak a foreign language. Many Americans cannot even identify correctly several European capital cites. The monetary language to speak in the next chapter is GOLD.

THE HAT TRICK LETTER PROFITS IN THE CURRENT CRISIS.

From subscribers and readers:

At least 30 recently on correct forecasts such as the Lehman Brothers failure, numerous nationalization deals such as for Fannie Mae, grand Mortgage Rescue, and General Motors.

“You freakin rock! I just wanted to say how much I love your newsletter. I have subscribed to Russell, Faber, Minyanville, Richebacher, Mauldin, and a few others, and yours is by far my all time favorite! You should have taken over for the Richebacher Letter as you take his analysis just a bit further and with more of an edge.” - (DavidL in Michigan)

“I used to read your public articles, and listen to you, but never realized until I joined what extra and detailed analysis you give to subscription clients. You always seem to be far ahead of everyone else. It is useful to ‘see’ what is happening, and you do this far better than the economists! I can think of many areas in life now where the best exponent is somebody not trained academically in that area.” - (JamesA in England)

“A few years ago, I was amazed at some of the stuff you were writing. Over time your calls have proved to be correct, on the money and frighteningly true. The information you report is provocative and prime time that we are not getting in the news. I was shocked when I read that the banks were going to fail in one of your prescient newsletters.” - (DorisR in Pennsylvania)

“You seem to have it nailed. I used to think you were paranoid. Now I think you are psychic!” - (ShawnU in Ontario)

“Your unmatched ability to find and unmask a string of significant nuggets, and to wrap them into a meaningful mosaic of the treachery-*****-stupidity which comprise our current financial system, make yours the most informative and valuable of investment letters. You have refined the ‘bits-and-pieces’ approach into an awesome intellectual tool.” - (RobertN in Texas)

by Jim Willie CB

Editor of the “HAT TRICK LETTER”

Home: Golden Jackass website

Subscribe: Hat Trick Letter

Use the above link to subscribe to the paid research reports, which include coverage of several smallcap companies positioned to rise during the ongoing panicky attempt to sustain an unsustainable system burdened by numerous imbalances aggravated by global village forces. An historically unprecedented mess has been created by compromised central bankers and inept economic advisors, whose interference has irreversibly altered and damaged the world financial system, urgently pushed after the removed anchor of money to gold. Analysis features Gold, Crude Oil, USDollar, Treasury bonds, and inter-market dynamics with the US Economy and US Federal Reserve monetary policy.

Jim Willie CB is a statistical analyst in marketing research and retail forecasting. He holds a PhD in Statistics. His career has stretched over 25 years. He aspires to thrive in the financial editor world, unencumbered by the limitations of economic credentials. Visit his free website to find articles from topflight authors at www.GoldenJackass.com . For personal questions about subscriptions, contact him at JimWillieCB@aol.com

Jim Willie CB Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.