Could Greek Debt Tragedy Morph into a Lehman Meltdown Market Crash?

Stock-Markets / Financial Crash Apr 28, 2010 - 02:43 AM GMTBy: Gary_Dorsch

In an eerie sense of déjà vu, German finance minister Wolfgang Schauble pleaded with his country’s citizens on April 20th, to back a joint EU-IMF bail out for Greece worth up to €45-billion, warning that failure to act would risk another global financial meltdown. “We cannot allow the bankruptcy of a Euro member state like Greece to turn into a second Lehman Brothers,” he told Der Spiegel. “Greece’s debts are all in Euros, and it isn’t clear who holds how much of those debts. The consequences of a national bankruptcy would be incalculable. Greece is just as systemically important as a major bank,” Schauble warned.

In an eerie sense of déjà vu, German finance minister Wolfgang Schauble pleaded with his country’s citizens on April 20th, to back a joint EU-IMF bail out for Greece worth up to €45-billion, warning that failure to act would risk another global financial meltdown. “We cannot allow the bankruptcy of a Euro member state like Greece to turn into a second Lehman Brothers,” he told Der Spiegel. “Greece’s debts are all in Euros, and it isn’t clear who holds how much of those debts. The consequences of a national bankruptcy would be incalculable. Greece is just as systemically important as a major bank,” Schauble warned.

The next phase of the global debt crisis could be on the horizon, if Euro-zone politicians fail to take swift action, and prevent Athens from defaulting on its debts. German banks have $330-billion of loan exposure to Greece, Portugal, and Spain, while French banks had $307-billion of claims, and British lenders have $156-billion. However, the European banking Oligarchs, such as Credit Suisse, UBS, Société Générale, BNP Paribas, and Deutsche Bank have a stranglehold on the public purse, and Euro-zone politicians readily submit to the interests of the powerful bankers.

Yet official German backing for a bailout of Athens, failed to stop spreads on Greece’s 10-year bonds from surging 300-basis points over the past two-weeks to 660-basis points over German Bunds, the highest since the launch of the Euro. Two-years ago, Greece’s cost of borrowing for 10-years was only a half-percent above Germany’s. Until recently, Greece’s membership to the Euro club had relieved investors’ fears about currency devaluations and inflation. Trust in Greece’s budgetary statistics was always shaky, but overlooked. The under-pricing of default risk gave Athens easy access to longer-term loans at low interest rates, - until now.

However, Greece needs to raise €50-billion ($68-billion) for each of the next five-years, in order to roll over existing debt and pay interest. The rescue package that’s on the table right now, crafted by the IMF and Euro-zone governments, would only buy a year’s worth of time for Athens to get its financial house in order. But bond investors are looking longer-term, and questioning the resolve of wealthier Euro-zone states to cover Greece’s debts beyond April 2011.

However, Greece needs to raise €50-billion ($68-billion) for each of the next five-years, in order to roll over existing debt and pay interest. The rescue package that’s on the table right now, crafted by the IMF and Euro-zone governments, would only buy a year’s worth of time for Athens to get its financial house in order. But bond investors are looking longer-term, and questioning the resolve of wealthier Euro-zone states to cover Greece’s debts beyond April 2011.

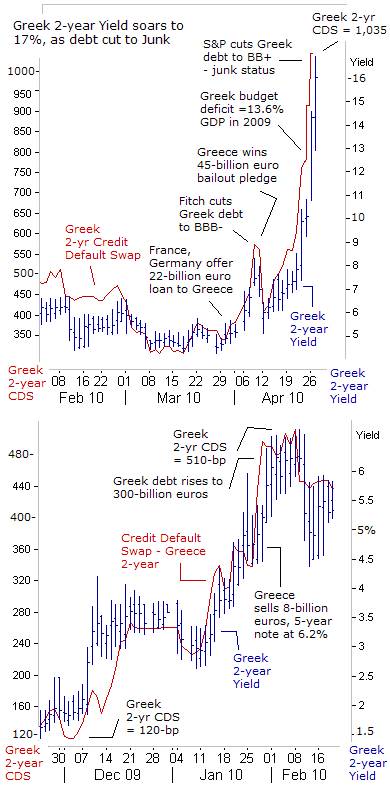

Yields on Greece’s 2-year note soared to as high as 17% week, from as low as 2% at the start of December, after Greece admitted that it auditors missed a few line items on the income statement, resulting in an even bigger budget deficit of 13.6% of GDP in 2009, up significantly from the previous estimate of 12.9%, and nearly double the 7.7% deficit recorded in 2008. That’s far above the average Euro-zone government budget deficit-to-GDP ratio of 6.3% last year.

Germany’s PM Angela Merkel wants Athens to agree to tough austerity measures for the next several years, before handing-out German taxpayer money. But Athens has already slashed public sector wages, and raised taxes, - setting off violent protests and strikes across the country, where unions control half of the nation’s workforce. Greece’s jobless rate rose to 11.3% in January, with 69,000 jobs lost in December. The bitter medicine of fiscal austerity is unpalatable for Athens, and with its membership in the Euro, it lacks the ability to monetize its debts away.

Will Greece become the Lehman Brothers of sovereign credit? Greece’s outstanding debt is roughly equal in size to that of Lehman’s when it collapsed in Sept 2008. If it’s forced into debt rescheduling and restructuring, it could trigger a domino selling effect in other vulnerable European bond markets in Portugal and Ireland, - both wrestling with exploding levels of sovereign debt, and lacking the ability to engage in “Quantitative Easing,” or printing vast quantities of money. Even if the Euro-zone politicians and the IMF can cobble together a bailout of Greece, they simply lack the financial resources to bailout the next wave of European sovereigns.

With G-7 central bank interest rates pegged near-zero percent, global finance houses are able to borrow money at next to nothing and deal in of all types of speculation. Trade is soaring in one of the most speculative forms of derivatives - credit default swaps (CDS), which played a key role in driving Lehman Brothers, Bear Stearns, and American International Group (AIG) into bankruptcy.

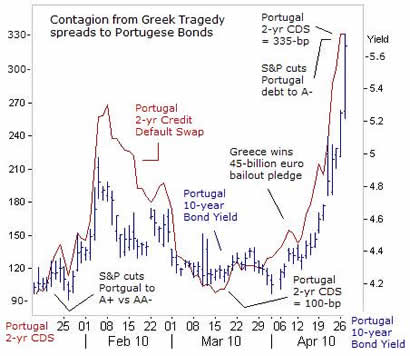

The activities of CDS speculators are not restricted to Greece. In the past few weeks, they have increasingly turned their firepower on Portugal’s bond market. The odds of default for Portuguese debt over the next two years, has shot-up 135-basis points in the month of April to 335-points today. At the same time, the yield on Portugal’s 10-year note has risen 150-basis points from four-weeks ago to 5.75% today.

The bond markets of Greece and Portugal are tiny, with trading volume of less than one billion Euros /day, making them easy and tempting targets for heavy hitters. Greece’s outstanding debt equals 300-billion Euros, and Portugal’s debt is about 126-billion Euros. Still, the nature of CDS trading, which is unregulated, gives speculators a big incentive to push companies or countries toward bankruptcy. There’s an incentive to burn the house down, in order to hit pay-dirt.

Attracted to the highly indebted Greek bond market like vultures to a decaying corpse, CDS traders have moved in for the kill. By attacking Greek and Portuguese bonds, traders have injected greater volatility in the Euro currency, thereby leveraging little nations’ problems into gigantic trading-floor profits. The surge in Portugal’s CDS and bond yields is very uncharacteristic for a country, which enjoys a AA- rating from Fitch and Moody’s, and A- rating from S&P. Could the rating agencies be lagging far behind the eight ball again, getting it right long after the fact?

Attracted to the highly indebted Greek bond market like vultures to a decaying corpse, CDS traders have moved in for the kill. By attacking Greek and Portuguese bonds, traders have injected greater volatility in the Euro currency, thereby leveraging little nations’ problems into gigantic trading-floor profits. The surge in Portugal’s CDS and bond yields is very uncharacteristic for a country, which enjoys a AA- rating from Fitch and Moody’s, and A- rating from S&P. Could the rating agencies be lagging far behind the eight ball again, getting it right long after the fact?

The CDS market is a hotbed of speculation, where banks and hedge funds, can bet on contracts without holding the underlying bonds. The threat of sovereign default, most immediately by Greece, has provided an opportunity for speculators to drive up the price of insuring the countries’ bonds, thereby further undermining confidence in the countries’ debt, and increasing the prospects of contagions sales.

If other Club-Med countries would require a bail-out, the final price tag could be so large, that it could backfire, by forcing French and German bond yields higher, especially if accompanied by a plunging Euro. Despite the specter of a Greek moratorium on its debt payments, - and a replay of the Sept 2008 meltdown of the global stock markets, triggered by the bankruptcy of Lehman Brothers, - in a strange twist of logic, the German DAX-30 Index has been thriving on Greece’s woes, benefitting from a weaker Euro and ultra-low German bund yields.

Even Spain’s IBEX index was climbing higher in tandem with the German DAX, since early February, tracking the Dow Jones Industrials and Transports, figuring the Greek tragedy is strictly an isolated affair, with little risk of contagion fallout to the rest of Club-Med. In any event, traders have seen this horror movie before, and the ending is always the same, - a massive government rescue with a bailout.

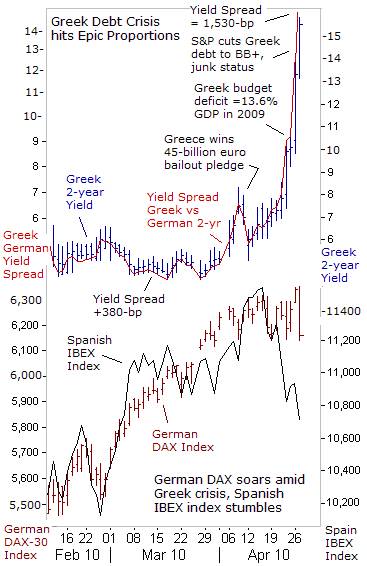

Still, there was a noticeable divergence last week, between the Spanish IBEX index, which tumbled 5%, and the German DAX, which continued to climb 2% higher to the 6,350-level, its highest in 19-months. Spain’s IBEX was dented by a quarter-percent jump in its 10-year bond yield to 4.10%, while Germany’s 10-year bund yield fell 15-basis points to 3-percent. Spain must service 560-billion Euros of outstanding debt, nearly double Greece’s debt, but it’s more manageable, since Spain’s debt-to-GDP ratio is only 53% compared with Greece’s 115%.

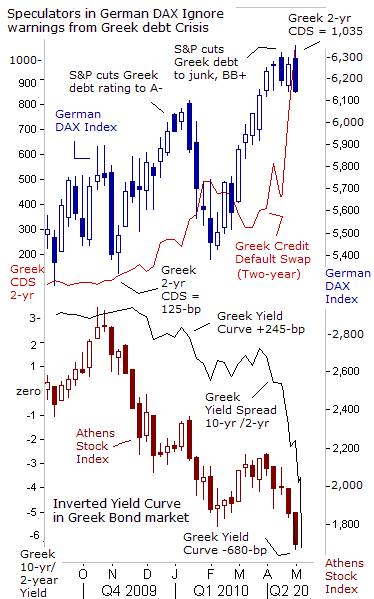

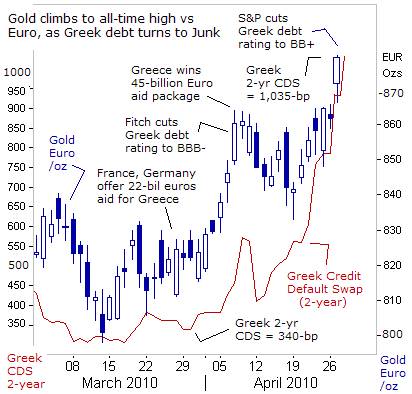

Finally, a bit of reality set in the delusional German DAX Index on April 27th, after S&P shocked the global markets, by cutting the credit rating of Greece three notches to BB+, or junk status, and lowering Portugal’s credit rating two notches to A- from A+ earlier, while putting Ireland on negative watch. In regards to Greece, the outlook is negative, meaning S&P could downgrade the rating again. “In our revised projections, we forecast Greece’s net general government debt-to-GDP ratio reaching 124% of GDP in 2010, and 131% of GDP in 2011,” S&P warned.

Finally, a bit of reality set in the delusional German DAX Index on April 27th, after S&P shocked the global markets, by cutting the credit rating of Greece three notches to BB+, or junk status, and lowering Portugal’s credit rating two notches to A- from A+ earlier, while putting Ireland on negative watch. In regards to Greece, the outlook is negative, meaning S&P could downgrade the rating again. “In our revised projections, we forecast Greece’s net general government debt-to-GDP ratio reaching 124% of GDP in 2010, and 131% of GDP in 2011,” S&P warned.

Within minutes after Greece’s credit ratings were slashed into junk territory, the UK’s FTSE-100, Germany’s DAX, and France’s CAC-40, lost a combined 80-billion Euros in market capitalization. Bullish speculators in the top-3 European bourses had figured that the Greek debt crisis would be fully contained, with the 45-billion euro bailout package, and would no longer be a nagging headache. As John Maynard Keynes famously observed, “The market can stay irrational longer than you can stay solvent.” However, once Greek 2-year CDS rates jumped above the psychological 1,000-level, the German DAX bubble quickly popped and fell 200-points.

The sighting of an “inverted” yield curve is as rare as spotting a lunar eclipse. So it’s of great interest, to observe the deeply “inverted” yield curve in the Greek bond market, where the 2-year note is yielding 680-basis points more than 10-year notes. If the yield curve inversion persists for an extended period of time, the fate of the Greek economy would be perilous, - perhaps, a 1930’s style Great Depression.

The “green shoots” rally on the Athens stock exchange has gone bust, with its economy suffocating under the chokehold of double-digit bond yields. Traders betting on a strong global economic recovery were dumping Greek shares and shifting the proceeds into the German DAX, a safer haven. The Bundesbank said on April 18th, the German economy is on track for a solid rebound in the second quarter, with its manufacturing sector expanding at a record pace in April. German carmaker, Volkswagen said its first-quarter operating profit nearly tripled.

Athens aims to unwind the inverted yield curve as soon as possible. Greek Finance Minister George Papaconstantinou warned CDS speculators they will “lose their shirts,” if they bet cash-strapped Greece will default. He said market rumors of Athens cutting or delaying payments to bond investors, is a “red herring, and restructuring is off the table. Greece will not leave the Euro,” he added.  The next day however, the bottom fell out of the Greek bond and stock markets.

The next day however, the bottom fell out of the Greek bond and stock markets.

Opting out of the Euro currency regime, and reinstituting a sovereign central bank to print Greek drachmas and monetize debt, carries huge risks for Athens. Abandoning the Euro for the drachma could spark hyper-inflation, and send 10-year bond yields soaring into the mid-20% range, which in turn, would send its economy spiraling into a Great Depression. Still, the alternative - adopting draconian austerity measures, tied to IMF and German loans, is also a poison pill leading to severe recession. According to the latest opinion poll, 70% of Greek citizens are opposed to dealing with the IMF, or accepting loans from the European Union.

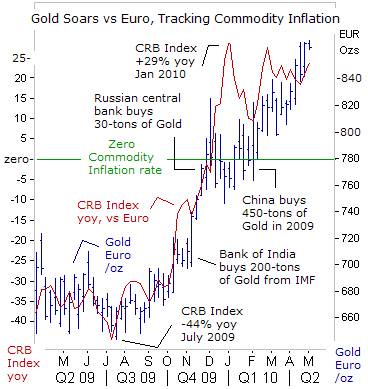

Last week, the ECB kept interest rates at a record low of 1% for the 11th month in a row, pointing to the debt problems facing the Club-med governments. With German and French banks holding more than 650-billion Euros of Club-Med debt, many traders prefer the safety of gold, over German DAX shares, since the Greek tragedy could turn out far worse than anyone could imagine right now.

Gold is soaring to record heights against the Euro, as traders bet that at some point in time, the wealthier Euro-zone governments would lose their resolve to finance Greece over the next five-years. The EU-IMF rescue package of 45-billion-Euros will only cover Greece’s financing requirements for one-year. Fears about a default, restructuring, or rescheduling of Greece’s debt payments in the medium term would still persist. Either scenario could hurt European bank earnings.

In the event that Athens decides to opt out of the Euro, or calls for a moratorium on its debt payments, after the first tranche of EU-IMF bailout money is used-up, gold is a good hedge against a devaluation of the Euro. However, gold is also following time honored fundamentals, such as acting as a hedge against commodity inflation. The CRB Commodity Index is surging +22% higher against the sinking Euro from a year ago, signaling an outburst of inflation in the months ahead, as factories pass along the cost of increasingly expensive raw materials, to end users.

In the event that Athens decides to opt out of the Euro, or calls for a moratorium on its debt payments, after the first tranche of EU-IMF bailout money is used-up, gold is a good hedge against a devaluation of the Euro. However, gold is also following time honored fundamentals, such as acting as a hedge against commodity inflation. The CRB Commodity Index is surging +22% higher against the sinking Euro from a year ago, signaling an outburst of inflation in the months ahead, as factories pass along the cost of increasingly expensive raw materials, to end users.

Bundesbanker Juergen Stark, the ECB’s token inflation hawk, said policymakers must consider the consequences of keeping ECB rates “too-low for too-long,” which create stock market distortions and cause banks to become addicted to cheap money. “Central banks ought to be aware of asset prices. There are times when it would be appropriate to raise interest rates to cool them if they appear to be overheating. Risks to the global inflation outlook are tilted to the upside. A multi-speed recovery of the world economy has the potential to exert upward pressure on prices.”

“In the same vein, we also need to closely monitor the adverse impact from fiscal developments on the inflation outlook. High levels of government budget deficits and debt may push up inflation expectations, and place an additional burden on the monetary policy of central banks. Additionally it could push up the borrowing costs of troubled countries, constraining growth, and leave little capacity to support economies in future crises,” Stark warned on April 15th.

However, his boss, ECB chief Jean “Tricky” Trichet, is strongly opposed to lifting interest rates anytime soon, arguing that inflation is dead. “We have inflation under control and that’s the reason why I have said on behalf of the governing council that interest rates are appropriate,” Trichet said on April 26th. “Raising interest rates too soon would crush the green shoots of recovery,” added Austrian central bank Ewald Nowotny. ECB officials are pointing to phony inflation statistics massaged by bureaucrats, and not viewing commodity inflation that is galloping ahead.

For European banks, Greece is too-big to fail, but it remains to be seen whether the Greek populace would choose to live under the yoke of EU-IMF austerity for the next several years. In the event of the un-thinkable, a Greek exit from the Euro, or debt restructuring, a Lehman style shake-out would ensue, rocking global markets. The odds of that happening are higher than most believe, about a 50-50% chance.

The German economy is emerging from its deepest post-war recession, led by its booming export industry, with two-thirds of Germany’s exports shipped to other Euro-zone countries and 75% sold to Europe. In February alone, Germany earned a trade surplus of 12.1-billion Euros. Germany uses these surpluses for foreign direct investment and bank lending to its Euro-zone partners, which in turn, buy German goods. However, along with the buying binge, huge increases in personal debt have sprung-up in countries such as Greece and Portugal.

The German economy is emerging from its deepest post-war recession, led by its booming export industry, with two-thirds of Germany’s exports shipped to other Euro-zone countries and 75% sold to Europe. In February alone, Germany earned a trade surplus of 12.1-billion Euros. Germany uses these surpluses for foreign direct investment and bank lending to its Euro-zone partners, which in turn, buy German goods. However, along with the buying binge, huge increases in personal debt have sprung-up in countries such as Greece and Portugal.

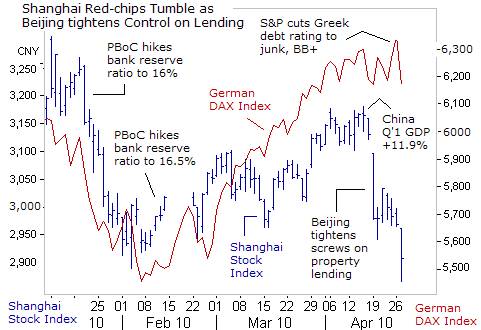

Germany was the world’s biggest exporter of goods for five-years thru 2008, before being overtaken by China. Die-hard bulls bidding-up the German DAX since it hit bottom in early February, are optimistic that German multinationals can deflect a downturn in the Club-Med economies, such as Spain, where the jobless rate is above 20%, by increasing sales to the booming Chinese economy, where GDP expanded at a sizzling +11.9% annualized rate in the first quarter.

However, what’s been overlooked is the recent sharp slide in Shanghai red-chips, skidding 8% lower over the past 10-days, after Beijing ordered local governments to take strong steps to control speculative buying in real estate. Banks listed on the Shanghai and Shenzhen stock exchanges fell sharply on fears that a government clampdown would increase the number of bad loans, since Chinese banks have lent a large amount of money to property companies and speculators. Beijing says property values on average rose 12% from a year ago, but in some sectors of the country, property prices have skyrocketed by 45-percent.

On March 27th, former Fed chief “Easy” Al Greenspan was asked whether there is a real-estate bubble waiting to burst in China. “I think so. To be sure, there are significant bubbles in Shanghai and along the coastal provinces. Some of that is going back into the hinterlands as well. Remember, the bursting of a bubble by itself is not a big catastrophe. We had a dotcom bubble, it burst and the economy barely moved. It is hard to tell when that bubble bursts, what the consequences are, because we do not have enough data on China.” And who would know better than Greenspan, the world’s top serial bubble blower.

The specter of a bursting real-estate bubble in China could wreck havoc upon the global economy. Most impacted would be the satellite countries, which rely heavily on sales to China, such as Korea, Taiwan, Japan, and Australia. A shake-out in Asian stock markets would also ricochet to the European sphere, and eventually hit North and South American markets. The earliest signal of trouble ahead, would be a break-down in the Shanghai index below the key 2,900-level.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2010 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.