Can the Fed Successfully Exit Liquidity Flood Policies ?

Interest-Rates / Credit Crisis 2010 Aug 03, 2010 - 09:18 AM GMTBy: David_Howden

The Federal Reserve Bank of Minneapolis recently interviewed macroeconomist Robert Hall for the June issue of its quarterly magazine, The Region. His words on the Federal Reserve's ability to enact an exit strategy to unwind its unconventional policies were clear and sure: "There are two branches to the exit strategy: There's paying interest on reserves, and there's reducing reserves back to normal levels. They're both completely safe, so it's a nonissue."

The Federal Reserve Bank of Minneapolis recently interviewed macroeconomist Robert Hall for the June issue of its quarterly magazine, The Region. His words on the Federal Reserve's ability to enact an exit strategy to unwind its unconventional policies were clear and sure: "There are two branches to the exit strategy: There's paying interest on reserves, and there's reducing reserves back to normal levels. They're both completely safe, so it's a nonissue."

Before addressing the question of whether the exit strategy is really "completely safe" or a "nonissue", we must first address the specifics of these two components.

Before addressing the question of whether the exit strategy is really "completely safe" or a "nonissue", we must first address the specifics of these two components.

In the wake of the credit crisis of late 2008, the Federal Reserve flooded the banking sector with liquidity. The Fed purchased troubled assets in exchange for base money. Since the banking system was not prepared to immediately loan this new base money, the system's reserves increased dramatically. The Fed concomitantly commenced paying interest on these reserves to remove the incentive for them to be fully used. In theory, by removing the incentive to loan out reserves, price inflation would be minimized: banks would not be constrained by their troubled loans and bad assets, and the Fed would retain credibility as an "inflation fighter."

The result was immediate and effective. As bad assets were removed from their balance sheets, banks were not forced into fire-sale situations by selling their assets to maintain regulatory capital levels. At the same time the Fed was able to save the banking sector via an increase in available credit without causing inflationary pressures to build.

While the short-term effects were seemingly beneficial and controlled, the long-term outlook is much less certain.

The Fed's liquidity injection was made by issuing credit to banks and simultaneously buying back troubled (i.e., subprime) banking sector assets. While the banking sector's balance sheet ballooned with cash and cash equivalents, the Fed's own balance sheet witnessed a sharp rise in the very troubled assets it was removing from the banking system. As Philipp Bagus recently noted, the Fed had become exactly the type of "bad bank" it had tried to rescue.

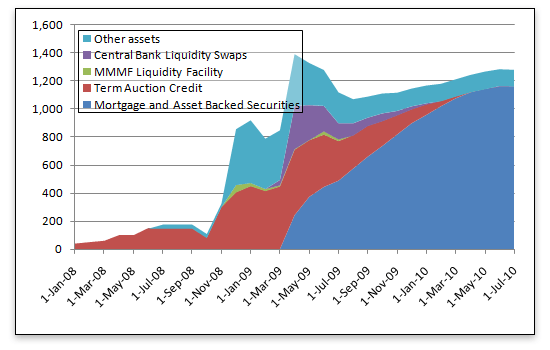

The figure below outlines the growth in the Fed's balance-sheet policies during the crisis.

Figure 1: Banking system loans initiated by the Federal Reserve System

Some of the enacted programs were self-liquidating, and now pose minimal danger to the financial system (central-bank liquidity swaps spring to mind, as does the money-market mutual-fund liquidity provision). Other programs have continued growing and cannot be so easily phased out. Over $1.1 trillion of mortgage-backed securities have been purchased since March 1, 2009. These assets, typically rated subprime, are of questionable quality (with total assets of almost $2.4 trillion as of July 1, 2010, nearly half of the Fed's total assets are subprime). More troubling is that these mortgages cannot be properly valued until they are sold to a willing buyer — buyers who are increasingly in short supply.

This "qualitative easing" — the purchasing of low-quality assets from the banking sector in exchange for high-quality assets from the central bank — persisted until central banks lacked adequate high-quality assets to continue the policy. It was only at this point that the more obvious policy of "quantitative easing" was pursued.

Philipp Bagus and I have been among a minority of economists who have signaled the occurrence of this policy (both by the Fed and the European Central Bank), and, more importantly, its detrimental ramifications. The long-term implications of this policy are now becoming evident.

As the Fed withdrew these troubled assets from the banking system, they were offset by issuing increasing amounts of Federal Reserve liabilities — cash. By offering an interest payment on reserve holdings, banks were incentivized to hold on to this newfound liquidity, thus nullifying any inflationary effects the policy could immediately cause. And as Robert Hall correctly notes, one exit strategy the Fed now has is the continual payment of interest on these reserves. As long as banks can profitably hold the 1.1 trillion extra dollars of monetary base that the Fed has created since August 2008, no inflationary pressures will build.

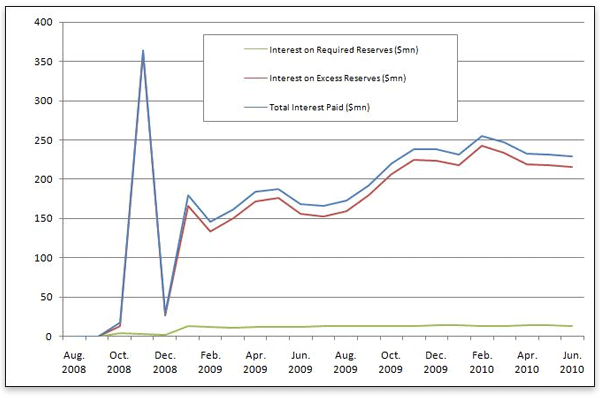

The reality may be very different from what Hall's theory suggests. As the figure below shows, the banking system now receives around $230 million each and every month for doing nothing other than holding on to the assets they passively received in exchange for their low-quality mortgage-backed securities.

Source: Federal Reserve Board of Governors release H.3 (Aug. 2008 — Jul. 2010)

Three billion dollars a year in interest payments is a large portion of the Fed's annual operating profits. The recipients — America's large and not-so-large banking establishments — are now much less hindered by subprime loans than they were two years ago. How much longer the Fed can give the banking sector billions of dollars to hold on to these reserves is questionable. Politically, it seems unlikely that Americans will continue to support these payments. Economically, the Fed is losing a large portion of its operating profits to these payments.

Despite these troubling aspects, the banking system's subprime situation is being alleviated. The Fed continues its policy of buying these mortgage-backed securities from the banking sector in order to maintain stability. This is a show of force, an attempt to demonstrate that the Fed is in full control of the situation.

Full control, however, is exactly what the Fed does not have. The alternative exit strategy, if financial stability is to be maintained without runaway inflation, is for the Fed to simply swap the "bad" assets on its own balance sheet for the "good" assets of the banking system.

Herein lies the rub. Inflationary pressures could be neutralized if the aggregate value of the assets originally purchased by the Fed is equivalent to the aggregate value of the assets now being returned. We should take comfort in knowing that at least one of these numbers is known with some degree of exactness. The cash now resting as reserves, and more importantly excess reserves, on the banking system's balance sheet can be valued at par: more or less, there are $1.1 trillion waiting on the sidelines for the Fed to reabsorb.

The value of the mortgage-backed securities that the Fed holds is far less certain. While the reported value on its balance sheet is $1.1 trillion, we should note that the Fed is balancing its books based on the current face values of these securities. These trillion odd dollars represent the outstanding principle on this debt, which is guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. While these assets may have been purchased originally by the Fed for this recorded amount, the maintenance of this value is questionable.

At what discount are securities backed by and comprised of Las Vegas gambling parlors and Miami vacation rentals selling today? We don't know for certain, and more troubling, we won't know what discount a trillion dollars worth of these securities will sell at until the market finds buyers for them. Presumably, the Fed purchased the lowest-quality assets that the banking system held: removing the most "toxic" assets to aid bank capitalization levels. Knowing that the Fed now holds the most toxic of the subprime assets the banking system could create during the roaring 2000s should leave us with some concern.

What then of the Fed's exit strategy? Ben Bernanke and Robert Hall, along with a multitude of fellow central bankers and economists, have stressed that there is no technical problem in exiting these positions. This is theoretically true — until reality sets in.

Any Fed-enacted swap of its subprime assets for the excess reserves of the banking system will result in some degree of inflation if the two values do not coincide. An upper and lower bound for future price inflation can be approximated from this differential.

At the upper bound, as several commentators such as Robert Murphy have warned, is the outcome where the Fed does nothing to reign in excess reserves. In this case, the Fed will have created $1.1 trillion worth of inflation.

More importantly, we can estimate the lower bound for the Fed-created inflation. The value differential between the excess reserves in the banking system and the subprime assets held by the Fed will remain in the banking sector indefinitely. As the Fed can only purchase back from the banking system reserves of equal value to its available assets, any drop in the value of its own assets will result in excess reserves remaining in the hands of the banking sector — waiting to manifest as price inflation when finally utilized.

Neither bound, upper nor lower, seems particularly attractive.

The silver lining in all this may be that any inflationary pressures will have to wait for another day. The Fed will not enact either exit strategy until the banking sector is back on firm footing, lest a tenuous situation worsen. With several banks entering insolvency weekly, the Fed is in no position to start unwinding any of its balance-sheet policies designed to aid the struggling sector.

Until the day comes when the Fed deems the banking sector able to stand on its own two feet — either with its subprime mortgages back, or without the interest payment on its reserve holdings — inflationary pressure on prices will remain low. But until the Fed finally decides to unwind its subprime balance-sheet positions, entrepreneurs will have to function in an era of uncertainty as to what price inflation lies ahead.

David Howden is a PhD candidate at the Universidad Rey Juan Carlos, in Madrid, and winner of the Mises Institute's Douglas E. French Prize. Send him mail. See his article archives.

Comment on the blog.![]()

© 2010 Copyright Ludwig von Mises - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.