M&A Flurry Can’t Deflect Attention From Dire Market Dataflow

Stock-Markets / Stock Markets 2010 Aug 30, 2010 - 08:49 AM GMTBy: PaddyPowerTrader

Late on Friday, equity markets set up for a relief rally despite bellwether tech giant Intel guiding down its earnings forecast (a development which I for one, thought was mightily disturbing). The trigger for the rally came from the speech of Ben Bernanke in Jackson Hole. He remarked that the Fed stood ready to boost economic growth and had the tools to do so, including increasing the purchase of long-term assets. So although Bernanke tilled no new ground at Jackson Hole in Wyoming, re-launching QE remains an option this Autumn as deflation risks intensify. Additionally over the weekend, the Bank of Japan expanded credit support for banks. These are indications that central banks are willing to support the fragile economic development.

Late on Friday, equity markets set up for a relief rally despite bellwether tech giant Intel guiding down its earnings forecast (a development which I for one, thought was mightily disturbing). The trigger for the rally came from the speech of Ben Bernanke in Jackson Hole. He remarked that the Fed stood ready to boost economic growth and had the tools to do so, including increasing the purchase of long-term assets. So although Bernanke tilled no new ground at Jackson Hole in Wyoming, re-launching QE remains an option this Autumn as deflation risks intensify. Additionally over the weekend, the Bank of Japan expanded credit support for banks. These are indications that central banks are willing to support the fragile economic development.

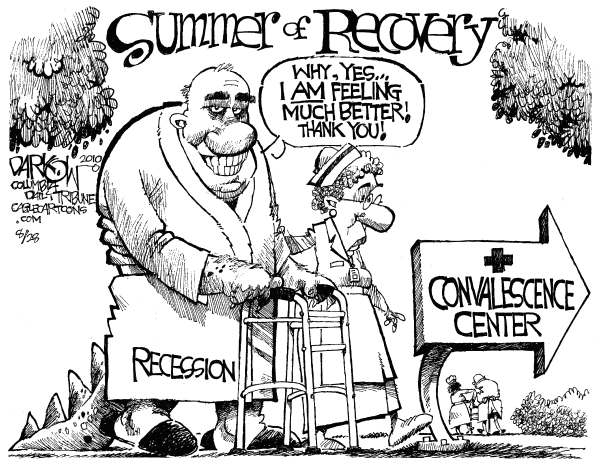

So risk assets wee only slightly down over the course of last week despite the fact that the multiple doom environment remained under full bloom, with relevant data releases surprising on the soft side across the board, fuelling the 3D (double dip/deflation) story. Why? Markets appear to have become less sensitive to bad news recently, suggesting that market participants may have already moved to short positions. This could reduce the downside to risky markets, but cannot prevent further falls if weak economic data raise risks of another recession soon. However , I fear that as a purely practical matter many Northern Hemisphere investors have been on holidays and have not yet absorbed the bad economic news. The rebound in risk appetite may prove short lived.

Today in a UK bank holiday thinned market recent pick up in M&A deals continues apace amongst cash rich companies, with several new tie-ups surfacing. US corporates have by some estimates $2trn in cash sitting on the balance sheets. In Europe shares of Sanofi-Aventis are off 0.2% after the drug maker publicly disclosed its offer to buy U.S. biotechnology company Genzyme for $18.5 billion, or $69 a share. The firms have been in talks since July and financing is already in place. While separately, Sanofi said that a new daily treatment for multiple sclerosis taken by mouth met its primary endpoint in a phase III trial. Bank of America / Merrill Lynch has reiterated their “buy” rating on the stock also this morning

In the aerospace space, engine maker Safran is down 1 percent after French newspaper La Tribune reported it’s preparing a formal bid for airplane-seats specialist Zodiac Aerospace and willing to pay a premium of up to 35 percent. The report, which cited unidentified people, said Safran will not go hostile and will decide whether to proceed with an offer in the coming days. Zodiac shares surged nearly 14 percent. Recall that in July, Zodiac rebuffed a first approach from Safran, arguing the companies have little in common and a deal would yield few cost savings.

Another deal moving the markets on Monday came courtesy of US chip giant Intel who following on from their $7.68bn purchase of McAfee have agreed to acquire the wireless-solutions business of Germany’s Infineon Technologies for about $1.4 billion in cash. Shares of Infineon fell 1 percent in Frankfurt.

Elsewhere, Spain’s biggest lender Banco Santander said it’s bought a portfolio of US car loans from HSBC Holdings Plc for $4 billion. The deal, however, will cost Santander just $342 million as the bulk of the portfolio is already financed. Santander shares rose 1 percent in Madrid.

And Stateside we’ve just learnt that 3M is to pay $10.50 a share or $943m fro Cogent.

Today’s Market Moving Stories

•The week began with all eyes on Japan, with an emergency BoJ meeting in focus. Ahead of the meeting USD/JPY had jumped higher on the belief that concrete action would emerge to weaken the JPY. The risk of disappointment was always high and as expected the BoJ to announced measures to extend loans to banks at 0.1 percent from JPY 20 trillion to JPY 30 trillion with an increase in duration from 3 to 6 months. There were however, no steps to counter JPY strength or any step up in JGB purchases from the current target of JPY 1.8 trillion. Alongside a likely increase in risk aversion once the Bernanke bounce wares off, this will result in USD/JPY moving lower, with a breach of 85.00 likely once again.

•One trigger for Fed action will be a further deterioration in job market conditions and markets will pay close attention to the August US jobs report at the end of the week.

•European Central Bank Governing Council and possible successor to JC Trichet member Axel Weber said the likelihood of a renewed recession in Europe has receded and domestic demand may overtake exports as the driver of growth . “We are bordering on a self-sustaining recovery in Europe and there is not much concern about a renewed recession,” Weber said in an interview with CNBC broadcast today from at the Federal Reserve’s annual monetary symposium in Jackson Hole, Wyoming. “The recovery is on track, not as high growth as before, but moderate growth going forward.”

•European Central Bank President Jean-Claude Trichet said governments risk a “lost decade” of weak economic growth if they delay reversing the surge in public debt triggered by the financial crisis. “The lesson from past history is that dealing with the legacy of accumulated imbalances is not simply a duty to be fulfilled after the economic recovery, but rather an important precondition for sustaining a durable recovery,” Trichet said yesterday in a speech at the Kansas City Federal Reserve Bank’s annual monetary symposium in Jackson Hole, Wyoming. “The primary macroeconomic challenge for the next 10 years is to ensure that they do not turn into another ‘lost decade.’”

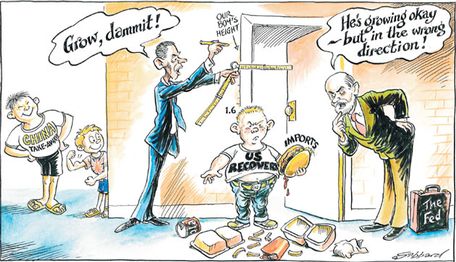

•At the Jackson Hole summit last weekend, which brought together around 110 central bankers and economists, a paper presented by C. M Reinhart, an economist of the University of Maryland, generated considerable debate. The paper basically says that the American economy could experience painfully slow growth and stubbornly high unemployment for a decade or longer as a result of the 2007 collapse of the housing market and the economic turmoil that followed. The paper examined 15 severe financial crises since World War II as well as the worldwide economic contractions that followed the 1929 stock market crash, the 1973 oil shock and the 2007 implosion of the subprime mortgage market. In the decade following the crises, growth rates were significantly lower and unemployment rates were significantly higher. Housing prices took years to recover, and it took about seven years on average for households and companies to reduce their debts and restore their balance sheets. In general, the crises were preceded by decade-long expansions of credit and borrowing, and were followed by lengthy periods of retrenchment that lasted nearly as long.

•Also at the conference Professors James Stock and Mark Watson Inflation could fall much further in the next year, thanks to the enormous slack that built up in the US economy during recession

•The British Chamber of Commerce upgrades its short-term growth forecasts (raising short-term economic growth forecasts; 2010 from 1.3% to 1.7%, 2011 from 2.0% to 2.2%. However, the body warned that the pace of UK economic growth will slow over the medium term as the effects of fiscal consolidation is more fully felt. “UK Growth Set to Slow, Business Group Cautions”

•And UK house prices continues to edge lower on concerns that the austerity drive will crimp UK economic and employment growth over coming months. Aug which has traditionally been a weak month

for UK house prices with buyers on holiday saw prices fell by the most in 16 months declining by 0.3 percent m/m with the y/y coming in at 1.5 percent for its smallest price gain since March according to property data company Hometrack.

•Thilo Sarrazin, a member of the board of the Bundesbank who has just published an anti-immigrant book, is coming under pressure over remarks that “all Jews share a certain gene”. The remarks have caused outrage in Germany, and would normally mark the end of anybody’s political career. But given the Bundesbank’s ridiculously extreme form of independence, there is no legal way for Axel Weber to fire his colleague. Weber has already demoted him after a previous outrage – to the effect that Sarrazin now only deals with the central bank’s internal computer systems. FT Deutschland carries the story on the front pages, and says that the German president could dismiss Sarrazin, but only in cases of “grave misconduct”. It appears as though Germany’s political elite is unwilling to trigger this case http://www.spiegel.de/international/germany/0,1518,713796,00.html

Company / Equity News

•Apax is believed to have approached Santander about the possibility of joining the bank in its bid for AIB assets. The Sunday Times reports that Santander is seeking to conclude its Polish bid, with PKO and BNP, in the final round of negotiations. Santander is also believed to be in negotiations with AIB for its US M&T stake and its UK operations. Apax lost out in previous rounds in the Polish process, and it believed to be preparing to join Santander in its bid, if possible and PKO remains the favoured bidder by the Polish Government. On the M&T side, the bid is complicated by the US management’s pre-emptive rights on the sale of the AIB stake. Note Anglo Irish release their “results” at 8am tomorrow.

•Davy’s report that US oil major Chevron is reported to have been awarded three blocks in a concession offshore Liberia, West Africa. Liberia is part of the West African Transform Margin play that Tullow, Anadarko and others kick-started with the discovery of the Jubilee Field, offshore Ghana. The Liberian basin sits at the western end of this play. In September 2009, the basin prospectivity was upgraded following the drilling of the Venus well, which established the presence of a working hydrocarbon system. The industry continually needs to build reserves and replace production, and the Liberian play is one of a small list of regions where this activity can take place. The arrival of Chevron should not be a surprise, and others will no doubt follow. The arrival of Chevron underpins the underlying prospectivity of the region in general. Tullow has a 25 percent share in three licences at the western end of the Liberian offshore.

•Multiple press reports in the US over the weekend carried a story which outlined Harry Reid’s’ (US Senate majority leader) changing stance on online gambling. As the senior senator from Nevada, Reid is seen as a key decision maker in relation to online gambling and his support will be crucial if it is to become legal in the US. Recently, a number of sources close to the Senator have indicated that he is turning positive on the issue. A story in the Reno Gazette Journal newspaper over the weekend outlined that the Senator would support the legalization of online poker, but would not support any other form of online gaming.

•BP’s internal investigation of the Deepwater Horizon rig disaster found company engineers misinterpreted pressure data that indicated a blowout was imminent, according to a person familiar with the report. BP managers aboard the Transocean Ltd.-owned rig misread a test of the Macondo well’s stability on April 20 and began replacing drilling fluid, which is heavier than oil and natural gas, with seawater, said the person, who spoke on condition of anonymity because the report’s findings haven’t been publicly released.

By The Mole

PaddyPowerTrader.com

The Mole is a man in the know. I don’t trade for a living, but instead work for a well-known Irish institution, heading a desk that regularly trades over €100 million a day. I aim to provide top quality, up-to-date and relevant market news and data, so that traders can make more informed decisions”.© 2010 Copyright PaddyPowerTrader - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

PaddyPowerTrader Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.