Back to Economic Basics GDP = C + I + G + Net Exports

Economics / Economic Theory Jul 17, 2011 - 05:54 AM GMTBy: John_Mauldin

This week we are going to revisit some themes concerning the problems of the debt and the deficit. I am getting a number of questions, so while long-time readers may have read most of this in one letter or another, it is clearly time for a review, especially given the deficit/debt-ceiling debate. I will probably offend some cherished beliefs of most readers, but that is the nature of the times we live in. It is the time of the Endgame, where things are not as black and white as they have been in the past.

This week we are going to revisit some themes concerning the problems of the debt and the deficit. I am getting a number of questions, so while long-time readers may have read most of this in one letter or another, it is clearly time for a review, especially given the deficit/debt-ceiling debate. I will probably offend some cherished beliefs of most readers, but that is the nature of the times we live in. It is the time of the Endgame, where things are not as black and white as they have been in the past.

Let's begin with a question that is representative of a lot of the questions I have been getting, from reader John:

"John, it appears that you're arguing that two contradictory things have the same effect: adding government spending doesn't help the economy, and reducing government spending hurts the economy. Which is it? At first, you say that adding government spending doesn't help, no new jobs are actually created, it fails the sharp pencil test, etc. So, we should reduce this waste, right? Well, yes, you say, but that will reduce GDP too. I just don't get it. You seem to have it both ways: increasing government spending is bad, and reducing it is bad. What is your point?"

Yes, I am saying both things, and they are not contradictory. We are coming to the end of the debt supercycle in the US, and have reached that point in much of Europe, and soon will in Japan. So while I am going to focus on the US, at least this week, the same principles apply to all the developed world.

For some 65-odd years, we have added to the national debt - individually, corporately, and as governments. But as Greece is finding out, there is a limit (more on that later). Eventually the bond market decides that loaning you more money is not a high-value proposition. If your home or your government is debt financed, you are forced to cut back. While the US is not there yet, we soon (as in a few years) will be.

One way or another, the budget deficits are going to come down. As we will see later, we can choose to proactively deal with the deficit problem or we can wait until there is a crisis and be forced to react. These choices result in entirely different outcomes.

In the US, the real question we must ask ourselves as a nation is, "How much health care do we want and how do we want to pay for it?" Everything else can be dealt with if we get that basic question answered. We can radically cut health care along with other discretionary budget items, or we can raise taxes, or some combination. Both have consequences. The polls say a large, bipartisan majority of people want to maintain Medicare and other health programs (perhaps reformed), and yet a large bipartisan majority does not want a tax increase. We can't have it both ways, which means there is a major job of education to be done.

The point of the exercise is to reduce the deficit over 5-6 years to below the growth rate of nominal GDP (which includes inflation). A country can run a deficit below that rate forever, without endangering its economic survival. While it may be wiser to run some surpluses and pay down debt, if you keep your fiscal deficits lower than income growth, over time the debt becomes less of an issue.

Pro Tip : Keep track of all your financial records & data remotely from anywhere on any device(PC/android/iOS) by loading your essential accounting software by Hosting QuickBooks on the Cloud based citrix vdi powered with 24*7*365 days top-notch technical support from Apps4Rent.

GDP = C + I + G + Net Exports

But either raising taxes or cutting spending has side effects that cannot be ignored. Either one or both will make it more difficult for the economy to grow. Let's quickly look at a few basic economic equations. The first is GDP = C + I + G + net exports, or GDP is equal to Consumption (Consumer and Business) + Investment + Government Spending + Net Exports (Exports - Imports). This is true for all times and countries.

Now, what typically happens in a business-cycle recession is that, as businesses produce too many goods and start to cut back, consumption falls; and the Keynesian response is to increase government spending in order to assist the economy to start buying and spending; and the theory is that when the economy recovers you can reduce government spending as a percentage of the economy - except that has not happened for a long time. Government spending just kept going up. In response to the Great Recession, government (both parties) increased spending massively. And it did have an effect. But it wasn't just the cost of the stimulus, it was the absolute size of government that increased as well.

And now massive deficits are projected for a very long time, unless we make changes. The problem is that taking away that deficit spending is going to be the reverse of the stimulus - a negative stimulus if you will. Why? Because the economy is not growing fast enough to overcome the loss of that stimulus. We will notice it. This is a short-term effect, which most economists agree will last 4-5 quarters; and then the economy may be better, with lower deficits and smaller government.

However, in order to get the deficit under control, we are talking on the order of reducing the deficit by 1% of GDP every year for 5-6 years. That is a very large headwind on growth, if you reduce potential nominal GDP by 1% a year in a world of a 2% Muddle Through economy. (And GDP for the US came in at an anemic 1.75% yesterday, with very weak final demand.)

Further, tax increases reduce GDP by anywhere from 1 to 3 times the size of the increase, depending on which academic study you choose. Large tax increases will reduce GDP and potential GDP. That may be the price we want to pay as a country, but we need to recognize that there is a hit to growth and employment. Those who argue that taking away the Bush tax cuts will have no effect on the economy are simply not dealing with either the facts or the well-established research. (Now, that is different from the argument that says we should allow them to expire anyway.)

Increasing Productivity

There are only two ways to grow an economy. Just two. You can increase the working-age population or you can increase productivity. That's it. No secret sauce. The key is for us to figure out how to increase productivity. Let's refer again to our equation:

GDP = C + I + G + net exports

The I in the equation is investments. That is what produces the tools and businesses that make "stuff" and buy and sell services. Increasing government spending, G, does not increase productivity. It transfers taxes taken from one sector of the economy and to another, with a cost of transfer, of course. While the people who get the transfer payments and services certainly feel better off, those who pay taxes are left with less to invest in private businesses that actually increase productivity. As I have shown elsewhere, over the last two decades, the net new jobs in the US have come from business start-ups. Not large businesses (they are a net drag) and not even small businesses. Understand, some of those start-ups became Google and Apple, etc.; but many just become good small businesses, hiring 5-10-50-100 people. But the cumulative effect is growth in productivity and the economy.

Now, if you mess with our equation, what you find is that Investments = Savings.

If the government "dis-saves" or runs deficits, it takes away potential savings from private investments. That money has to come from somewhere. Of late, it has come from QE2, but that is going away soon. And again, let's be very clear. It is private investment that increases productivity, which allows for growth, which produces jobs. Yes, if the government takes money from one group and employs another, those are real jobs; but that is money that could have been put to use in private business investment. It is the government saying we know how to create jobs better than the taxpayers and businesses we take the taxes from.

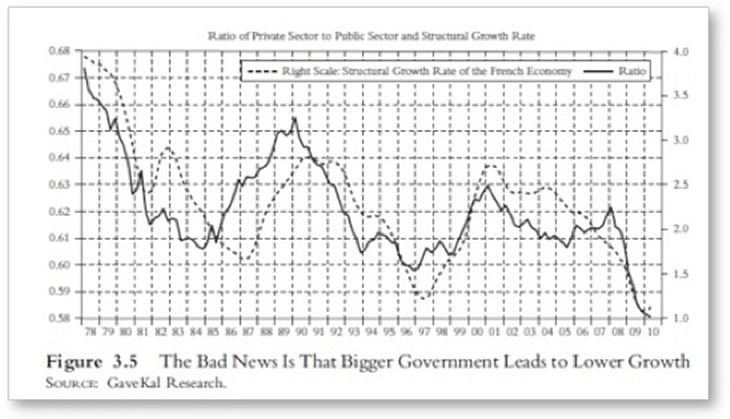

This is not to argue against government and taxes. There are true roles for government. The discussion we must now have is how much government we want, and recognize that there are costs to large government involvement in the economy. How large a drag can government be? Let's look at a few charts. The first two are from my friend Louis Gave, of GaveKal. This first one reveals the correlation between the growth of GDP in France and the size of government. It shows the rate of growth in GDP and the ratio of the size of the public sector in relation to the private sector. The larger the percentage of government in the ratio, the lower the growth.

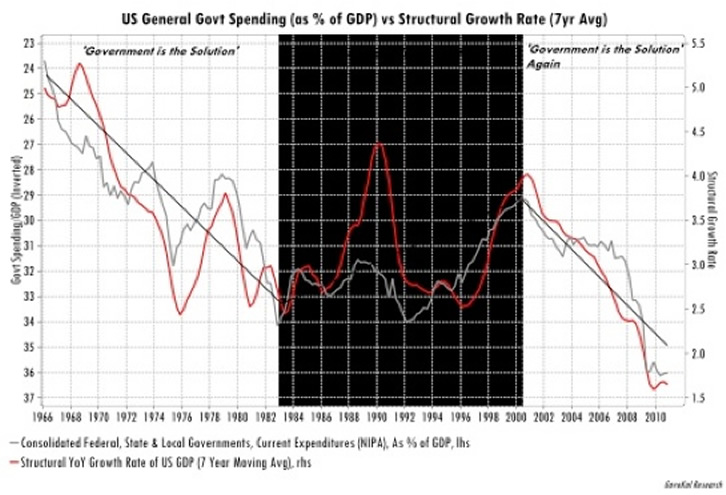

I know, you think this is just the French. We all know their government is too involved in everything, don't we. But it works in the US as well. The chart below shows the combined US federal, state, and local expenditures as a percentage of GDP (left-hand scale, which is inverted) versus the 7-year structural growth rate, shown on the right-hand side. And you see a very clear correlation between the size of total government and structural growth. This chart and others like it can be done for countries all over the world.

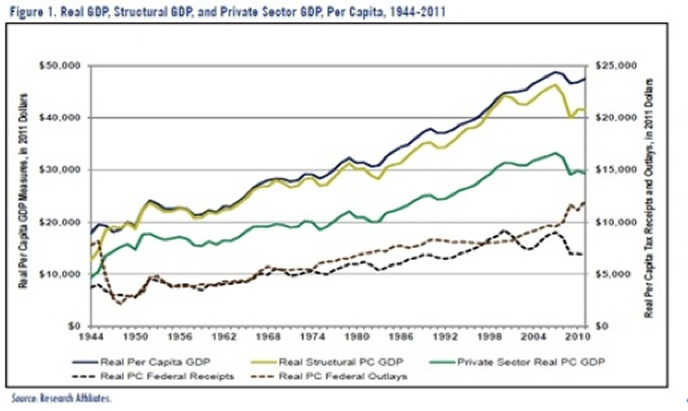

Now let's review a graph from Rob Arnott of Research Affiliates. The chart needs a little setup. It shows the contributions of the private sector and the public sector to GDP. Remember, the C in our equation was private and business consumption. The G is government. And G makes up a rather large portion of overall GDP.

The top line (in dark blue) is real GDP per capita. The next line (yellow) shows what GDP would have been without borrowing. So a very real portion of GDP the last few years has come from government debt. Now, the green line below that is private-sector GDP. This is sad, because it shows that the private sector, per capita, is roughly where it was in 1998. The growth of the "economy" has been limited to government.

Notice that real GDP without government spending or deficits has been flat for 15 years (which, as a sidebar, also explains why real wages for private individuals are flat as well, but that's a topic for another letter). Now, here is what to pay attention to. For the last several years, the real growth in GDP has come from the US government borrowing money. Without that growth in debt, we would be in what most would characterize as a depression.

This is why Paul Krugman and his fellow neo-Keynesians argue that we need larger deficits, not smaller ones. For them the issue is final aggregate consumer demand, and they believe you can stimulate that by giving people money to spend and letting future generations pay for that spending. And sine WW2 they have been right, kind of. When the US has gone into a recession, the government has embarked on deficit spending and the economy has recovered. The Keynesians see cause and effect. And thus they argue we now need more "hair of the dog" to prompt the recovery, which is clearly starting to lag behind what they think of as normal growth.

But others (and I am in this camp) argue that business-cycle recessions are normal and that recoveries would come anyway, and are not caused by increased government debt and spending but by businesses adjusting and entrepreneurs creating new companies. Correlation is not causation. Just because recoveries happened when the government ran deficits does not mean that they were the result of government spending. This is not to argue that the government should not step in with a safety net for the unemployed - again, a subject for another letter.

Let's see what Rob Arnott says about this conundrum:

"GDP is consumer spending, plus government outlays, plus gross investments, plus exports, minus imports. With the exception of exports, GDP measures spending. The problem is, GDP makes no distinction between debt-financed spending and spending that we can cover out of current income.

"Consumption is not prosperity. The credit-addicted family measures its success by how much it is able to spend, applauding any new source of credit, regardless of the family income or ability to repay. The credit-addicted family enjoys a rising "family GDP" - consumption - as long as they can find new lenders, and suffers a family "recession" when they prudently cut up their credit cards.

"In much the same way, the current definition of GDP causes us to ignore the fact that we are mortgaging our future to feed current consumption. Worse, like the credit-addicted family, we can consciously game our GDP and GDP growth rates - our consumption and consumption growth - at any levels our creditors will permit!

"Consider a simple thought experiment. Let's suppose the government wants to dazzle us with 5% growth next quarter (equivalent to 20% annualized growth!). If they borrow an additional 5% of GDP in new additional debt and spend it immediately, this magnificent GDP growth is achieved! We would all see it as phony growth, sabotaging our national balance sheet - right? Maybe not. We are already borrowing and spending 2% to 3% each quarter, equivalent to 10% to 12% of GDP, and yet few observers have decried this as artificial GDP growth because we're not accustomed to looking at the underlying GDP before deficit spending!

"From this perspective, real GDP seems unreal, at best. GDP that stems from new debt - mainly deficit spending - is phony: it is debt-financed consumption, not prosperity. Isn't GDP after excluding net new debt obligations a more relevant measure? Deficit spending is supposed to trigger growth in the remainder of the economy, net of deficit-financed spending, which we can call our "Structural GDP." If Structural GDP fails to grow as a consequence of our deficits, then deficit spending has failed in its sole and singular purpose.

"Of course, even Structural GDP offers a misleading picture. Our Structural GDP has grown nearly 100-fold in the last 70 years. Most of that growth is due to inflation and population growth; a truer measure of the prosperity of the average citizen must adjust for these effects."

And thus the graph above showing private GDP and the difference in the GDP numbers that are reported in the media. I used Rob's entire (and brilliant) piece as an Outside the Box last May. If you missed it, you can go to http://www.johnmauldin.com... and review it.

The Trillion Dollar Question

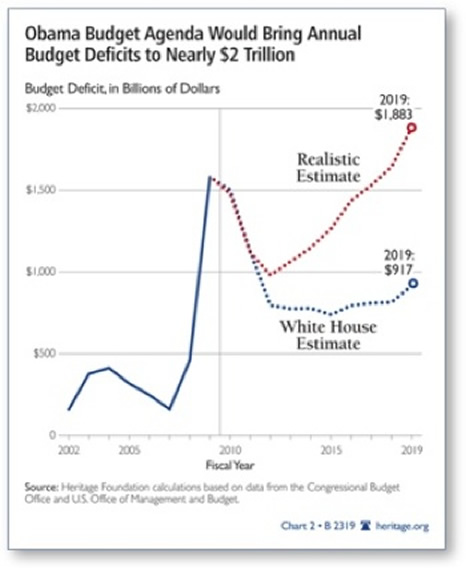

Now, in our review, let's get back to reader John's question. I have used this chart before, but it bears another quick look. This is from the Heritage Foundation. It is a year old, and one can quibble about the specifics. That is not the point of today's issue. The point is that, whatever the deficit is, it is huge. This is a chart of something that will not happen, as the bond market will simply not finance a deficit as large as the one that looms in our future. Long before we get to 2019, we will have our own Greek (or Irish or Portuguese or Japanese, etc.) moment. (Or Spanish or Italian or Belgian - so many countries, so much debt!)

For the sake of the argument and our thought experiment, let's split the difference on that chart. Somehow we must then find about $1.2 trillion in cuts or taxes to get the deficit down to below the growth rate of nominal GDP. And another few hundred billion if we actually want to balance the budget.

And that, gentle reader, is no small hill to climb. Let's say we cut spending and/or raise taxes by $200 billion a year for 6 years. That is more than 1% of GDP each and every year! Go back to the first chart. That means that potential GDP growth will be reduced by over 1% a year! Every year. We would need to rely upon private GDP growth, which Rob's chart shows has been flat for almost 15 years! The growth of the last 11 years has been a government-financed illusion.

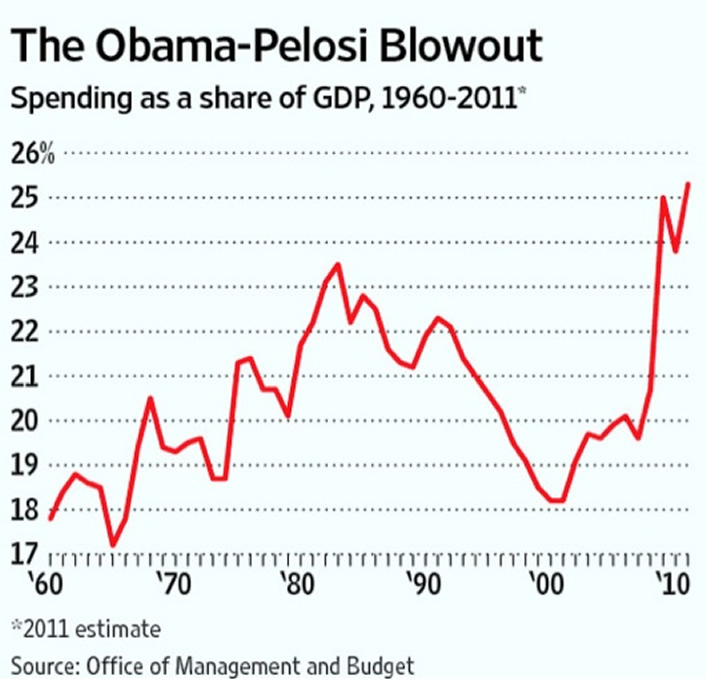

There are no good choices. The time for good choices was years ago. I was and still am a fan of the Bush tax cuts. They were not the problem; a few years after the cuts, tax revenues were up considerably. The problem was a profligate Republican Congress which allowed spending to rise even more. And you can't just blame it on the wars. That contributed, but it was not even close to the lion's share. If we had held the line on spending, we would have paid off the entire debt and been in good shape when the crisis hit in 2008. The following graph is from today's Wall Street Journal editorial page. They use it to show how much Democrats allowed the budget in terms of GDP to rise and spin out of control.

I would point out that in the 8 previous years, under Bush/Hastert/Delay et al., there was also a rise in the growth of government, as the chart shows. While it was not as large, it was clearly there. The drop in the previous period was the Bill Clinton/Newt Gingrich years. How many people are nostalgic for that pairing? Say what you will about them, their collaboration was a good era for growth in the private sector - the last we have had.

And that is the crux of the problem. Either we willingly cut the deficit by a far more significant amount than anyone is discussing, or we hit the wall at some point and become Greece. $4 trillion? No, let's talk about 10 or 12.

And that, John, is the problem. We have painted ourselves into the corner of no good choices. We are left with difficult and disastrous choices. We have condemned ourselves to a slow-growth, Muddle Through Economy for another 5-6 years, at best, as we are forced to right-size government. If we raise taxes to partially solve the problem, we have to recognize that higher taxes will result in slower private growth. That's just the rules. There are no easy buttons to push.

So, we must cut spending and the deficit, and yes, it is going to slow the economy for a period of time. The economic literature suggests that a spending cut will have 4-5 quarters of effect and then be neutral going forward. But we are going to have to make those cuts year after year after year.

I know the Tea Party types want to do it all at once, but that would guarantee a decade-long depression. You just really don't want to go there. It MUST be a slower, controlled "glide-path" approach. I wrote about this back in 2009, along with all the other options. Nothing has changed: http://www.johnmauldin.com/.../.

The present contains all possible futures. But not all futures are good ones. Some can be quite cruel. The one we actually get is determined by the choices we make.

It is getting time to close, so a few quick observations. While choosing a President and Congress next year will be a referendum of sorts, I would like to see a real, non-binding referendum appear on our primary ballots. How much Medicare do we want? Should we raise taxes? How do we get to $10 trillion in cuts? You would have to confirm you have read a 20-page document outlining the choices and consequences, and that should be posted everywhere and mailed to everyone. We need to have a real national conversation.

If Obama says he wants $4 trillion in cuts, then let him give us details rather than asking Congress to give him a plan, as he did today. He has his brain trust; surely they can come up with some details. The problem is that if he offers specifics he will have to show his supporters what he is willing to cut. And those cuts will not be without pain.

The real issue, as I have said, will boil down to how much Medicare we want and how we want to pay for it. Congressman Ryan's cuts don't get us even halfway there.

A Summer of Ultimatums

In closing, this from my friends at GaveKal:

" In the past 24 hours, we have seen the Greek deputy finance minister announce that Athens would fall far short of planned asset sales (this can only come as a surprise to investors born yesterday) and the Greek prime minister publish an open letter to Eurogroup Chairman Juncker warning that Greece has done all that it could. Mr Panandreaou went on to say that the onus is now on European policymakers to meet in a closed forum, with no damaging press leaks, and emerge with a strong, unambiguous message - we have to assume that the irony of asking for more secrecy through an open letter to the general media was perhaps lost on the Greek PM. Diplomacy aside, it seems that Greece is placing an ultimatum on Europe and this for a very simple reason: the end game for the EMU is approaching much faster than most investors had expected. Indeed, the choice between fiscal union or disintegration may well have to be faced this very summer.

"In his eloquent letter, Papandreou boldly stated that, in essence, Greece is no longer prepared to make further concessions and will thus blow up Europe's financial system if it is subjected to any more pressure. In other words, it is now time for all additional concessions to come from the side of Germany, the ECB and the EU. The willingness of Papandreou to speak so boldly is hugely important since it marks a recognition by the debtors that they now have the whip-hand in these negotiations. The Greeks (and Irish) for some reason failed to realize their power last year, but they do now. This transforms the balance of power in the negotiations. As a result, Germany and the ECB have reached the moment of truth - either they comply with the debtor countries' demands or they abandon the euro. This ultimatum probably helps explain why the euro has been so weak and why it should be heading even lower."

There will be yet another emergency meeting next Thursday. The crisis is coming to the final innings. Will Germany and the ECB finance Greece? Print money in a fashion that would make Bernanke and Krugman envious? But if we in the US do not get our own act together, in the not-too-distant future we will face our own moment of truth as the bond market forces us to choose between disastrous and worse. The cuts we will have to make under pressure will be far worse than those we can make now.

I will probably write about Europe next week. I think the brewing crisis could cause a banking crisis and a recession in Europe, which, just as our subprime crisis caused world pain and a global recession, will also bring their pain to our shores. We are not immune. Stay tuned.

Vancouver, New York, and Maine

In a few weeks I head to Vancouver and then to New York City and Maine for the annual fishing trip, one of the outings I truly look forward to each year. Both cities and Maine will afford me memorable times with great friends, which is one of the things that gives life meaning and makes it fun and keeps me young.

And speaking of young, I must admit to a guilty pleasure. I am a Harry Potter fan, and tonight I am going to see the final episode. Joe Morgenstern of the Wall Street Journal, and my favorite movie reviewer, gave it rave reviews. While I have not read the books, I have followed the story and am looking forward to the final chapter. But it is bittersweet, as I will miss my friends who I have watched for all these years. And to watch the film-making technology change over time has been a revelation, too. What a world we live in.

Time to hit the send button. Enjoy your week and spend it with friends when you can.

Your just another muggle tonight analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.