ECB Thinly Veiled Bailout

Interest-Rates / Eurozone Debt Crisis Dec 30, 2011 - 07:14 AM GMTBy: PhilStockWorld

The ECB is borrowing U.S. Dollars from the Fed to bailout European banks. And that is in addition to the Long Term Refinancing Operation (LTRO).

The ECB is borrowing U.S. Dollars from the Fed to bailout European banks. And that is in addition to the Long Term Refinancing Operation (LTRO).

However, the "borrowing" is not called "borrowing." It's called a "temporary U.S. dollar liquidity swap arrangement." Yet it is really borrowing because it's going massively in one direction for the purpose of giving the ECB Dollars to lend to European banks, so the ECB can avoid lending more Euros. The ECB doesn't want to tarnish its "inflation fighting" reputation and further devalue the Euro. Instead, the Fed is taking billions of Euros as collateral for the Dollar swap.

As Gerald P. O'Driscoll Jr., former vice president and economic advisor at the Federal Reserve Bank of Dallas, and senior fellow at the Cato Institute, wrote in the WSJ (The Federal Reserve's Covert Bailout of Europe):

"The ECB would also prefer not to create boatloads of new euros, since it wants to keep its reputation as an inflation-fighter intact. To mitigate its euro lending, it borrows dollars to lend them to its banks. That keeps the supply of new euros down. This lending replaces dollar funding from U.S. banks and money-market institutions that are curtailing their lending to European banks—which need the dollars to finance trade, among other activities."

U.S. Banks and financial institutions do not want to lend European Banks more Dollars, and it would look bad for the Fed to do this unpopular lending directly, so the Fed has found an indirect route.

"The two central banks are engaging in this roundabout procedure because each needs a fig leaf. The Fed was embarrassed by the revelations of its prior largess with foreign banks. It does not want the debt of foreign banks on its books. A currency swap with the ECB is not technically a loan."

In exchange for Euros as collateral, the ECB gets non-technically loaned Dollars which it then lends to European banks. The additional Dollars flowing to the EU banks enable the ECB not to release more Euros to the EU banks and into circulation. According to O'Driscoll, this "Byzantine financial arrangement" was designed perfectly to confuse people.

"The Fed's support is in addition to the ECB's €489 billion ($638 billion) low-interest loans to 523 euro-zone banks last week. And if 2008 is any guide, the dollar swaps will again balloon to supplement the ECB's euro lending...

"The Fed had more than $600 billion of currency swaps on its books in the fall of 2008. Those draws were largely paid down by January 2010. As recently as a few weeks ago, the amount under the swap renewal agreement announced last summer was $2.4 billion. For the week ending Dec. 14, however, the amount jumped to $54 billion. For the week ending Dec. 21, the total went up by a little more than $8 billion. The aforementioned $33 billion three-month loan was not picked up because it was only booked by the ECB on Dec. 22, falling outside the Fed's reporting week. Notably, the Bank of Japan drew almost $5 billion in the most recent week. Could a bailout of Japanese banks be afoot? (All data come from the Federal Reserve Board H.4.1. release, the New York Fed's Swap Operations report, and the ECB website.)

"No matter the legalistic interpretation, the Fed is, working through the ECB, bailing out European banks and, indirectly, spendthrift European governments. It is difficult to count the number of things wrong with this arrangement." (The Federal Reserve's Covert Bailout of Europe)

Mr. O'Driscoll argued that the Fed has no authority to bailout Europe. (Although lack of authority has not stopped the Fed from acting in the past.) Ben Bernanke met with Republican senators on Dec. 14 to discuss the crisis in Europe. According to Sen. Lindsey Graham, Bernanke told reporters that the Fed did not have "the intention or the authority" to bailout Europe. Nevertheless, the week Bernanke claimed he was not going to conduct an EU bailout "the size of the swap lines to the ECB ballooned by around $52 billion."

O'Driscoll also argued that swap arrangements "foster the moral hazards and distortions" resulting from government intervention in the credit markets. "Allowing the ECB to do the initial credit allocation—to favored banks and then, some hope, through further lending to spendthrift EU governments—does not make the problem better." Moreover, this is another example of the Fed's lack of transparency. Non-transparency is a consistent theme of the Fed, in spite of Bernanke's promises to provide more openness. Bernanke's statement just two weeks ago that the Fed had no intention of bailing out Europe is consistent with a long history of secrecy and deceptive behavior.

"The USD swaps totaled almost 84 billion so far, while the ECB lent a net of $289 billion in the LTRO last week after rollovers.

"All central banks create money. That is their function. How they do it, whether by direct lending to government through direct purchase of government debt, or through lending to private institutions or purchasing private debt is a matter of a nuanced difference regarding the conduits through which the money flows into the financial system, the markets, and the economy. It’s a question of targeting.

"The biggest difference between the Fed and the ECB is that the ECB has always lent to all the European banks. Until 2007, the Fed only conducted operations with Primary Dealers. From 2007 to 2010 the Fed had direct operations with a variety of financial institutions. Since QE2, the Fed has gone back to dealing only with the PDs."

Apparently not anymore. The Fed is now using currency swaps to lend to the ECB which is taking the Dollars and lending them to European banks in exchange for a new, and more broadly defined types of collateral. As discussed in this week's Stock World Weekly, Money for Nothing and Your Debt for Free, the ECB's latest LTRO "is making it possible for eurozone member states to sell assets such as government buildings to banks, whereupon the banks turn the properties into asset-backed securities which are then pledged as collateral for borrowing from the ECB... WSE's Russ Winter observed, the ECB just was handed a gigantic can of worms. The ECB balance sheet is now up to $3.5 trillion USD...

“Illustrating the nature of this circular transaction, Bloomberg reports that Unicredit and Intesa, two insolvent Italian banks are using “state guaranteed bonds” as $52 billion collateral to throw at the ECB. So rather than even using actual Italian sovereigns, the ECB accepts something more nebulous down the food chain...”

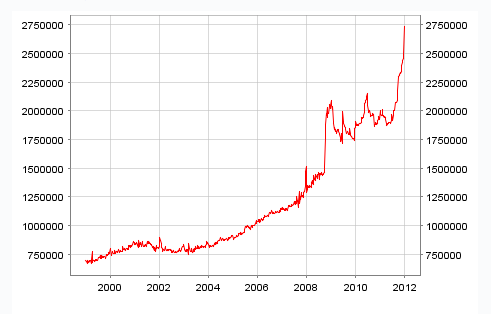

Here's a chart Lee sent me from the ECB's website showing the expansion of assets on the ECB's balance sheet. The numbers on the y-axis are in millions, so the assets are rapidly approaching 2.75 trillion Euros (around 3.5 trillion Dollars).

Lee concluded, "The Fed has opened an unlimited credit line with the ECB and other central banks for which it has so far lent billions of Dollars, with Euros as collateral. The Fed is bailing out European banks; that's not in dispute. The ECB is the guarantor and the conduit, but the banks are the recipients of the bailout, and the Fed's balance sheet is expanding as a result of the loans to the ECB."

Stay tuned. Lee is going to describe how the US Government bond market collapses, and thus, the world ends, shortly.

Philip R. Davis is a founder of Phil's Stock World (www.philstockworld.com), a stock and options trading site that teaches the art of options trading to newcomers and devises advanced strategies for expert traders. Mr. Davis is a serial entrepreneur, having founded software company Accu-Title, a real estate title insurance software solution, and is also the President of the Delphi Consulting Corp., an M&A consulting firm that helps large and small companies obtain funding and close deals. He was also the founder of Accu-Search, a property data corporation that was sold to DataTrace in 2004 and Personality Plus, a precursor to eHarmony.com. Phil was a former editor of a UMass/Amherst humor magazine and it shows in his writing -- which is filled with colorful commentary along with very specific ideas on stock option purchases (Phil rarely holds actual stocks). Visit: Phil's Stock World (www.philstockworld.com)

© 2011 Copyright PhilStockWorld - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.