Surging central bank gold demand adds new dimension to bull market

Commodities / Gold and Silver 2012 Apr 11, 2012 - 12:16 AM GMT

The longer-term trends in gold's supply-demand fundamentals point to a potentially explosive market situation in the years ahead. In short, the supply trend is static to shrinking while global demand trends, particularly from investors and central banks, appear to be in a period of rapid expansion. What's more the political, financial and economic dynamics driving these trends are not likely to undergo any significant reversal anytime soon for reasons explored below.

The longer-term trends in gold's supply-demand fundamentals point to a potentially explosive market situation in the years ahead. In short, the supply trend is static to shrinking while global demand trends, particularly from investors and central banks, appear to be in a period of rapid expansion. What's more the political, financial and economic dynamics driving these trends are not likely to undergo any significant reversal anytime soon for reasons explored below.

Up until now, gold's secular bull market has been driven by a combination of private and institutional investor demand. Though those two components in the demand picture remain well-defined, it is the arrival of deep-pocket central banks in emerging countries like China, Russia, Saudi Arabia, India, Mexico, Brazil, as well as players yet to be named, that have added a whole new dimension to gold's secular bull market.

Investor demand tends to ebb and flow based on changing views about the economy, financial markets, and the price itself, i.e. whether gold is perceived to be over-bought or over-sold. As a result, investor demand is generally viewed as an inconsistent aspect of the supply-demand tables. Central bank demand is more rooted in longer-term policies having to do with the value and safety of national reserves, and these policies tend to play out over the course of years or even decades. As a result, changes in the way gold is viewed by central banks are likely to have a significant, even profound, long-term effect on the market -- in fact, the consistent nature of central bank demand can be viewed as putting a floor under the price. (In late 2011, for example, when the price dropped from all-time highs in the $1900 per ounce range, the Chinese central bank reportedly purchased a significant amount of physical metal.) That makes 2011 -- when central banks for the first time in decades became net buyers of gold bullion -- an important watershed year for the gold market.

China remains the centerpeice in the contemporary gold market. As both the world's leading producer and consumer of gold, it plays an important role on both sides of the supply-demand equation. It should go without saying that gold owners would be well-served to understand how China views gold. Obviously a favorable "official" attitude toward gold from its top consumer and producer would play a hugely supportive role in the years to come; and a dismissive, or negative attitude would act to its detriment. China's central bank and federal government see gold as a hedge against its holdings of U.S. dollars and other currencies subject to debasement. Any number of individuals, ranging from members of its academia to government policy makers and important functionaries in the central bank itself, have warned against the instability of currency reserves and the importance of establishing a reliable hedge. In fact, the Peoples Bank of China advocates a 4000 tonne gold reserve. It now holds about 1200 tonnes. Such thinking affects the supply side in that China is likely to continue "domesticating" its gold production as part of its national reserves. On the demand side, it makes China a ready buyer of any sizable tranches of gold that become available on the market -- no matter the source. In fact, recent reports have surfaced that China has launched a program of buying gold directly from mining companies around the world as a means to building its reserves. The London Telegraph's Ambrose Evans-Pritchard reports one source, predicting that China will acquire "several thousand tonnes of gold over the next five years to match the US stash of 8,000 and the Euro Zone's 11,000."

If you would like to broaden your view of gold market, we invite you to sign-up for our regular newsletter and receive quality commentary like what you are now reading. It's free of charge and comes by e-mail. You can opt out at any time.

The fact that this pro-gold attitude has become ingrained in the "monetary thinking" of China's economic policy makers will figure largely in supply-demand tables in the years to come and will act as a catalyst for similar thinking in other similarly positioned nation-states. Russia, for example, the fifth-leading producing country follows a similar policy; and recently South Africa, the fourth-largest gold producing country, took steps to move away from the dollar and toward China's renminbi, in international currency transactions. How long before it sees fit to follow a gold policy similar to the one in place in China? The three countries together account for 28% of the world's annual gold production.

Central banks becoming net buyers of gold top story for 2011

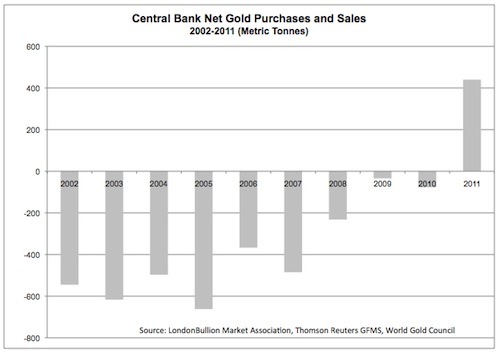

Now, at the end of the first quarter of 2012, we can look back at the events of 2011 with a little perspective. If I were to rank the most important gold market events of 2011, the profound shift of central banks from net sellers to net buyers would sit comfortably in the number one slot. Number two would be the surge in purchases of coins and bars by private investors. Not only are the shifts in sentiment themselves profound, the tonnage involved is striking. Ten years ago, in 2002, central banks sold 545 tonnes in the aggregate. In 2005, net sales reached a peak of 662 tonnes. Five years later, in 2010 those sales had dwindled to 77 tonnes, and in 2011, the central banks became net buyers of 440 tonnes -- a shift of roughly 1000 tonnes from 2002 to 2011. In other words, not only did central banks move in the direction of gold ownership in 2011, they did so with gusto. Physical availability, more so than price considerations, appears to be the greatest restraint to further official sector acquisitions, as more and more dollars pile up in the reserves of export-driven economies.

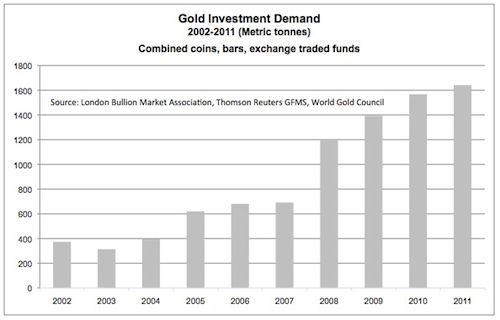

As for the private ownership of gold bars and coins, the growth is equally striking. In 2002, investors globally purchased 373 tonnes in the form of coins and bullion. In 2005, after the first gold exchange traded funds were introduced, total combined investment demand for coins, bullion and exchanged traded funds reached 620 tonnes. From there, gold ownership has been in a steady pull upward, hitting 1196 tonnes in 2008 and 1641 tonnes in 2011. It is interesting to note that exchange traded fund demand turned sharply lower from 2009-2011, while the coin and bullion component turned sharply higher, as a number of hedge fund owners - including John Paulson - opted for outright ownership, probably in the form of allocated storage, over the ETFs.

The combination of strong official sector demand and global investment demand could move gold into the next phase of its long-term bull market, and carry prices to new levels beyond the all-time high of $1895 per ounce. The world of money and finance underwent severe changes in the aftermath of the 2008 financial meltdown, and most significant among them is the way gold is viewed as a long-term store of value by private investors, fund managers, sovereign funds and central banks alike.

Gold's bull market surge came during disinflationary times

We should keep in mind that gold's price surge prior to and just after the crisis came when the economy was experiencing disinflationary circumstances -- something that came as a surprise to many analysts. History tells us that there is no gold bull market like one driven by runaway inflation. Now with key central banks in the industrialized world (Europe, the United States, Japan and United Kingdom) moving to quantitative easing monetary policies -- i.e., running the printing presses -- many feel that the next stage in gold's price evolution could occur under inflationary circumstances. If so, it could make the next few years an interesting time for gold owners. As the monetarist school teaches, monetary inflation generally takes a period of three to five years to translate to price inflation. In the United States, the first wave of quantitative easing began in 2009 and ended in mid-2011. Another round, as you are about to read, could be in the offing. (Please see "Quantitative easing and gold" below.)

In the short run, any number of intervening factors can govern the price of gold -- from the activities of rogue traders, bullion banks and central banks, to software-based systems generating thousands of trades in the blink of an eye. In the long run, though, it is the ebb and flow of physical metal -- the activity of its buyers and sellers-- that truly govern the price. The motivation of the real buyer of the physical metal -- as well as the true motivation of its real sellers -- lies at the heart of the future price of gold, and it is here that the true student of the golden metal will look for guidance. Though market magicians can move the market in one direction or the other by manipulating paper instruments, they cannot govern the dynamics of bull or bear markets over the long run. That is why the patient owner of the physical metal itself over all these years has been the most direct beneficiary of this bull market, and it is why he or she is likely to remain the chief beneficiary in the years to come.

For a free subscription to our newsletters, please click here.

By Michael J. Kosares

Michael J. Kosares , founder and president

USAGOLD - Centennial Precious Metals, Denver

Michael Kosares has over 30 years experience in the gold business, and is the author of The ABCs of Gold Investing: How to Protect and Build Your Wealth with Gold, and numerous magazine and internet articles and essays. He is frequently interviewed in the financial press and is well-known for his on-going commentary on the gold market and its economic, political and financial underpinnings.

Disclaimer: Opinions expressed in commentary e do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. Centennial Precious Metals, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD - Centennial Precious Metals does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.