Stock Market and Interest Rates Forecast 2008

Stock-Markets / Financial Markets Jan 23, 2008 - 03:17 AM GMTBy: Ty_Andros

Introduction

Introduction

The first three weeks of the year started with a BANG and this is set to continue as the public servants wrestle with the consequences of their poor policies. And, instead of creating policies of wealth creation, the result to their decades-long policies of currency debasement and creeping socialism: “Temporary” stimulus plans, front and center with the various public servants trying to outbid each other as to the size of the package.

The one thing they all agree on is that it is temporary and no legislative, tax, or regulatory relief can be expected in the G7. So the wealth creation aspect of the G7 will continue to be destroyed and the wealth destruction aspects are set to continue their cancerous growth path (government is a cancer to business and wealth creation). So, long term nothing has changed in terms of reestablishing capitalism and wealth creation.

Let's refresh our memory as to the dominant pattern of 2008 as it will affect everything and create dominoes of poor policy decisions. Please keep in mind that these are ENORMOUS opportunities, discover what you need to do to thrive and implement them. Investing is not a one way game as people came to think during the low volatility that was characteristic since the March 2003 lows when money printing caused ALL markets to become EXTREMELY correlated.

Now we will review the dominant pattern for 2008 courtesy of John Mauldin (John can be reached at john@frontlinethoughts.com .)

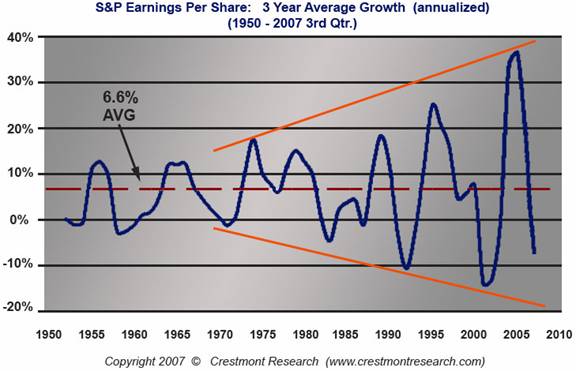

I have updated the chart below from when it was originally published in March of 2007 and included my commentary at the time (in italics) as it is now CRUNCH TIME for this 50-year chart:

We are in a wolf wave, and the amplification of each wave up or down is expanding. A chart of a wolf wave looks like a megaphone, small on one end and amplifying out. Wolves attack and eat things and it is no different with economies and asset markets, they are eaten when a wolf appears. A good example of a wolf wave is from John Mauldin's latest letter and, by extension, Crestmont Research. Here he shows corporate profits since 1950.

(This chart has been updated to reflect through the 3 rd quarter 2007)

See the mega phoneformation? It is called a wolf wave. We are at a fairly good level of profits now, but it projects a nuclear winter in corporate profits dead ahead (see chart below). From Record highs never seen in fifty years, to record lows also not seen in the same period, below the lows of 2001-2002. This chart is a testament to how fiat money and credit creation has made steady growth and economic stewardship become more and more unmanageable over a long period of time. It is clear that monetary policy is also following this wolf wave pattern, either too hot or too cold. Politicians (and their “something for nothing” constituents) in the western world see these enormous profits and are set to attack the creators and holders of this wealth. They want the money and they will put in place new taxes and entitlement mandates to claw back this gusher of wealth, thereby accelerating the downside of this wave. We all want business cycles that cleanse past excesses, but the up and downs are now out of control. There is no consistency, no orderly form to the business and economic cycles, everything now is either booming or busting.

Those words were prophetic in March when they were written in the first “Fingers of Instability” series as was that chart of corporate profits (see Tedbits Archives , this was one of the best of 2007. Read its words then look around you today). Now we are far below the ZERO line and falling fast, so, the gusher the public servants are telling the electorate (that they are going to CLAW back from those greedy corporations and small businessmen, i.e. your employers and neighbors) is now GONE. The lows are scheduled/projected to arrive at election time, making for good decision-making doesn't it?

Federal, State, municipal and individual income is set to plummet. In the case of the government, we are talking about tax and regulatory receipts/fees (taxes in disguise), and in the case of the individual, layoffs and runaway inflation will be the culprits . The reflation that will be required will be ENORMOUS, and to think every politician in the G7 is angling to punish those EVIL corporations and small businessmen for raising their prices to compensate for the lower value and purchasing power of the G7 currencies in which they are paid and priced. G7 corporate profits are only at NOMINAL new highs, and in “REAL” terms they are cratering, just as you saw in stocks and bonds (in part I of 2008 Outlook). Every time the Central banks and financial industry print a trillion dollars their prices go up, but their REAL profits go down!

Ben Bernanke testified in Congress and during the televised hearing in the budget committee, the stock market voted with its feet demonstrating its confidence in both parties, Congress and Bernanke, to deal with current difficulties. The market is set to raise the temperature in the room on both parties in order to deal with emerging economic collapse caused by their poor stewardship and policies.

We have always known Congress is incapable of MICRO-MANAGING the economy and markets, but now we are fully aware of the fact that a school teacher and academic (promoted from the classroom with no real market experience) is in charge of the biggest central bank in the world! His support for money printing and easy money demonstrate his complete lack of understanding of the sources of wealth creation and capitalism.

Take a look at this excerpt from the King Report (www. ramkingsec.com):

A CNBC interview with the speaker of the house, Nancy Pelosi, showed the ECONOMIC incompetence resident on Capital hill as she emphasized the fact that investors, entrepreneurs and small business only have lumps of coal in their futures as Congress has no intention of letting them have rewards for risk taking and job creation. She parroted the standard public servant canard that tax cuts be “timely, targeted, and temporary” signaling the continued growth of leviathan government and public servant refusal to reform themselves! “THE BUSH TAX REDUCTIONS” are set to expire! The most massive increase in taxes in US history is on the near horizon. An almost 3 trillion dollar increase. Do you think this might affect the way investors view the United States, its economic prospects and decide whether to send capital here for investment?

Last week we witnessed the next disaster du jour as the MONO line insurers (Ambac, MBIA, Radian, SC, ACA etc.) and their stock prices indicated that their futures as viable ongoing businesses have basically passed the point of no return; bankruptcy looms in the near future. This CANNOT be allowed to happen as the financing of State and Municipal Bonds and the outstanding issues will be enveloped in a tsunami of capital destruction. Tens of thousands of issues (and trillions of dollars of outstanding bonds) will be downgraded within an instant of their DEMISE. The rescue of Countrywide was a non event compared to the havoc that will be unleashed if these firms are allowed to fail. WASHINGTON, Ben Bernanke and Hank Paulson better have the fire trucks headed in that direction as we write this.

This cannot be allowed to transpire or the wealth that has already gone to MONEY heaven will be dwarfed by the collapse in value of the bonds underpinned by these insurance firms. You will see a Municipal and State Bond COLLAPSE if they go under. CNBC's James Cramer suggests a prepackaged bankruptcy of all the insurers into strong hands (like Berkshire Hathaway,) using the government printing presses as a back stop for the un-payable insurance obligations they now hold on CDO, CMO, MBS derivatives, etc. I Say GOOD IDEA. This has SYSTEMIC risk written all over it!

The financial industry and banks have written down 107 billion dollars so far, so we are on the lookout for the other 200 to 400 billion! Ouch. The credit default swap industry lies exposed for much of this carnage and does not have the funds to pay the obligations. Most of these “over-the-counter and unregulated” obligations are sitting on the trading desks of the money center and investment banks. What will they do? PRINT THE MONEY!

Asset deflation is rampant in the financial and banking industries in the G7 as their paper castles collapse and they will DO ANYTHING to reflate them, especially during an election year. Inflation is rampant in the real economy as the money printing goes into areas other than where the central banks wish it to go. (i.e. into things that can't be printed by brokers, banks or public servants/serpents).

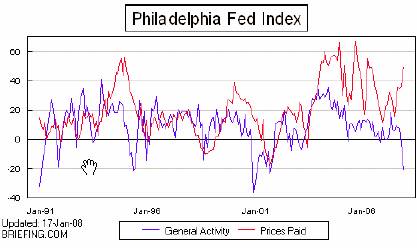

Take a look at the collapse in business conditions in the Philadelphia Fed Index and the explosion in prices confirming the unfolding wolf wave:

Can you say stagflation? And to think they are about to FLOOD the US with liquidity!

Dr. John Hussmann recently pointed out that most of the money and credit creation is being completely consumed by runaway government growth and spending. Well there's a simple solution to that conundrum: PRINT MORE. State and municipal finances are in a historic deficit in 2008, as plunging corporate income and real estate values are devastating their tax bases. PRINT MORE! This is the only solution they know. Reducing taxes and regulation and creating the policies of growth and thriving private sectors is contrary to their goals of control of everything in the G7. They will not consider the required GOVERNMENT reforms until the pain is of extreme proportions.

Public servants and their elite constituent's only wish to fleece and control the public, not serve them! It does not matter which side of the isle they claim to represent left or right, conservative or liberal there is no difference! The only thing growing is the supply of money improperly indexed for inflation so they can move more and more people into what else? HIGHER tax brackets. Look no further than the alternative minimum tax for an example of this. A tax to catch mega wealth in the late 1960's is now knocking on the doors of the former middle class and their paper-inflated incomes. The Mandarins of Washington DC view you as their servants, not their constituents and employers.

The howl of pain from inflation and collapsing business is only set to increase in 2008. It will drive everything economic; so what's the solution to this problem? PRINT MORE MONEY! Take more of it from the private sector to give to their special interest friends and supporters. Public servants are creatures of control, never expect them to reduce it or relinquish it! Take a dollar from the private sector and send back a dime, this is the recipe the candidates for president and congress are proposing in the upcoming elections! This is a recipe for wealth destruction, not wealth creation! It is clear you have no chance to be elected if you do not support these poor policies. What G7 constituents want is what is most destructive to their futures!

G7 public servants use the growing NOMINAL numbers to exploit the loss of wealth by the middle class which their own monetary systems are foisting on their constituents (theft of funds while it sits in the bank or in bonds) to create class envy to bolster their continuing “nationalization” of private-sector businesses and wealth.

Real Estate has cracked in the UK and Spain. In the UK prices fell 6.5% in one month and in Spain they are down 20% in many areas. In Shanghai and Shenzhen China real estate is also imitating HONG KONG a decade ago. The hyperinflationary bloodbath is just beginning and will probably last for years.

Money has four purposes:

- Medium of exchange

- A store of value

- Measure of value

- Method of accumulating wealth, building upon it and moving it into the future

G7 currencies now fail three out of four of these definitions and are about to accelerate their losses in the last three of these definitions in 2008! YOU MUST UNDERSTAND THIS and adjust your investment plans accordingly. If you are holding cash or bonds then you LOST 20 to 30% of your wealth that was stored in them in 2007! The monetary systems in the world are breaking down and people will be scrambling for shelter in the coming year and decade!

Stocks!

Three phrases define G7 stock markets in the developed world: OUTSIDE DOWN, KEY REVERSALS, CAMBRIDGE HOOKS. These phrases all mean basically the same thing: LOWER! Devastating technical damage is clearly visible. The quarterly charts of these markets are all pointing down and giving sell signals as I write this. Weekly charts signal firm tops are in place. Most markets made new all-time highs in Q 3 or 4 and closed lower then the previous quarter's closing level. And it doesn't end there, as Bellwether “real economy” stocks such as Warren Buffets Berkshire Hathaway are confirming the market action. As the dominant pattern in 2008, the WOLF WAVE signals the direction of the intermediate stock market direction. The wolf wave signals that we should look for lows in new profits near 20-30% year-over-year decline. Once this is priced in, you will be offered a FABULOUS buying opportunity. In the meantime, SELL RALLIES.

Confirming the coming explosion in stock prices is this weekly chart of the VIX gauge - it has tipped its hand and activated the pattern last week - a measure of volatility and fear by options market:

Ouch, this VIX chart is a coiling explosive pattern and it has REACHED maturity (maturity in pennants like these generally occur when they are 80% complete; they don't go the tip.) As it raises out of the top of the pattern it signals an explosive drop lower in stock prices and increase in volatility. The measuring objective is a 20% move in volatility UP from the breakout point. FEAR is on the rise and set to increase.

As it goes through the top, the bottom drops out of the stock markets in a chorus with a 2008 dominant wolf wave pattern in corporate profits prophesies being realized. Keep in mind, the charts from last week's missive outline the total lack of savings and a huge rise in debt. It doesn't bode well for rising corporate profits as consumers have no money left to buy things.

Keep in mind that stocks are priced in PAPER currencies and, as such, have a bid from the depreciation of them by printing press. They can go down short and intermediate term, but they will rise “long term” to reflect the lower purchasing power of the currency in which they are priced. This is why you can always expect markets to go up over time - much of the gains are illusions though.

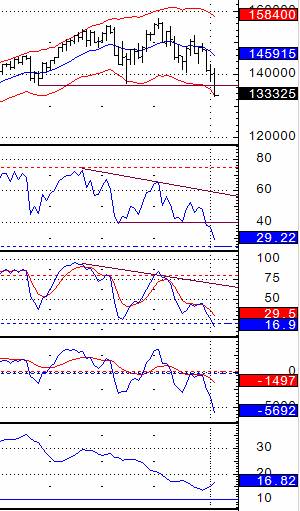

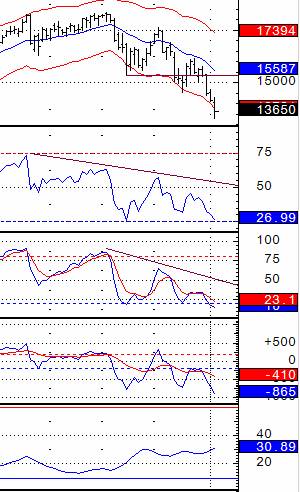

When viewing technical charts one must keep in mind that quarterly bars are more powerful then monthly bars, monthly bars are more powerful the weekly bars and weekly bars are more powerful then daily bars. The longer the duration of the bar, the more dominant it is on the shorter time frame. Those of you who wish to read headlines and invest on market fundamentals must understand that all the fundamental information available on any given trading day is in the price at the end of any trading day, week, month, quarter and year. You must keep this in mind as we work through the various sector forecasts. Now let's take a brief look at selected markets in the G7: S&P 500 in the US, FTSE 100 in the UK, DAX 30 in Germany, and the Nikkei 225 in Tokyo:

Quarterly chart 2007 weekly

The S&P 500 has just had an outside down on the quarterly charts and the weekly's (with price projections signaling a loss equal to what's occurred since the highs) signal a top is firmly now in place. The action in the first three weeks of 2008 confirms the signal RSI (relative strength index) is firmly in decline and Slow Stochastic's and MACD are both on sell signals. The trend line since 1990 is firmly in tact and probably will be tested before this pullback is over. A bounce to try and move back into the old range, relieve oversold conditions and revert to the 20 week exponential moving average can be expected, but you should consider selling into the rally and lightening up your existing portfolio or getting outright short. Measuring objectives of the top on the weeklies project another 15% loss from here. Now let's take a look at the FTSE 100 in the UK:

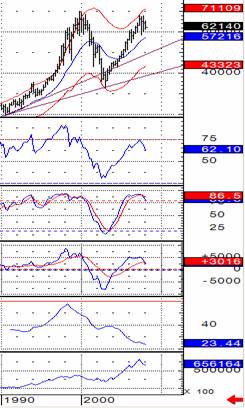

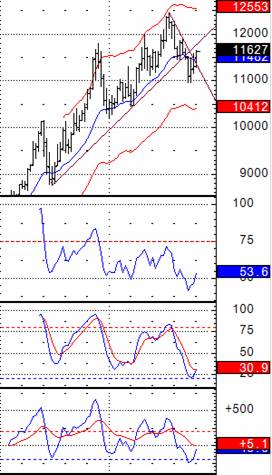

Quarterly chart 2007 weekly chart

This is the same story as the S&P 500, only it was the July quarter where the outside down bar occurred. Firm sell signals are in effect in the slow Stochastic's, and the MACD. On the weeklies, bearish divergences are clearly in evidence. A test of the trend line since 1990 seems to be in the cards but, as in all the charts I am illustrating, I expect it to be a fairly quick trip. ADX is low so we are looking for a pattern and it is clear: BOMBS AWAY. Now let's peek at the German DAX 30:

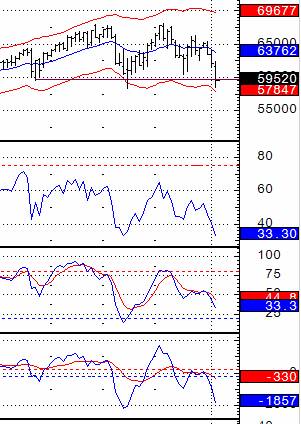

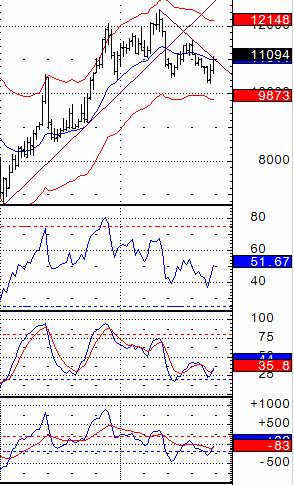

Quarterly Dax 30 Dax 30 Weekly 2007

The Dax is the main bourse in the European Union outside the UK and it is a big DITTO of the UK as it also had its quarterly reversal in the 3 rd quarter. One exception is that we have yet to receive the sell signal off the MACD. These markets are poised to fall and destroy another repository of wealth in unison. Now let's head to the Pacific Rim and Japan Nikkei 225:

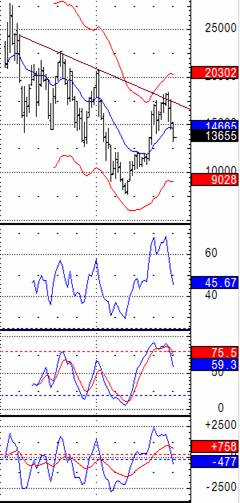

1990 2000 2007 Weekly

This is the picture of the unrelenting 18 year bear market in Tokyo. Many analysts called a bottom but the bear trend line HELD and the bear is now fully back in control. This makes it a chorus to the downside and the quarterly Stochastic's have a double hook sell signal. Once again we are waiting for confirmation from the MACD indicator. The weekly chart is firmly in TREND mode signaling the bear is about to make a move short term.

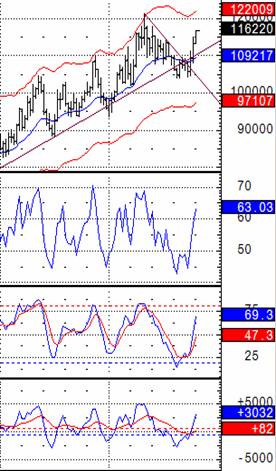

In conclusion, the G7 stock markets are in the early innings of a significant correction and bear market. The emerging markets are better supported as those economies are creating wealth, they have savings, their banks are properly reserved and their economies are more Austrian in nature. But a double top is clearly visible in Shanghai and outside down quarters are under construction in China and India. I am a tape reader and there are real sellers in the market.

There are now huge amounts of overhead supply and that implies that every rally will quickly be sold into by the public seeking to GO TO CASH and to the sidelines. Fierce “short covering” rallies can be expected, but use them to lighten up, get defensive or get SHORT. The market could easily rally into the fed meeting at the end of the month and crash into March. The VIX pattern is explosive in nature and fear is stalking the stock markets. The herd clearly has turned and you could easily expect a stampede to develop for the exits. Ultimately they will turn higher as the money and credit creation kick in and the stocks price in the deflation of the purchasing power of the currencies in which they are priced - creating a natural buoyancy. When the markets go low enough, you can also expect foreign holders of US IOU's known as dollars, Euros, Yen and Pounds to exchange them for Units of Production known as STOCKS! Stocks are a form of things that can't be printed. The unfolding “Crack up Boom” is in its infancy.

Interest Rates

This is quite clear: Long term interest rates are headed lower, in the US and throughout the G7. Below are quarterly charts of US 10 year notes, German Bunds, and London Gilts. They are all breaking higher and giving buy signals signaling the BROAD deflationary fires in their banking and financial systems, while the PAPER assets they hold, created or have financed and invested in collapse in value and purchasing power. Let's look at US 10 year notes, German bunds and UK Gilts:

1990 2000 1990 2000

US 10 years notes, quarterly German 10 year Bunds, quarterly

• 2000

UK 10 year Gilts

These are quarterly charts and they are marching in unison and signal rallies in long term interest rates contracts and lower, long term nominal rates in the near horizon to combat the recessions on the near horizon. Interest rates are deeply NEGATIVE and are poised to become more so as easy money is the only thing underpinning the G7. Wealth creation is but a memory of the Reagan years. There is not much to say here that wasn't covered in part 1 of the 2008 outlook. Interest rate instruments and the currencies in which they are denominated are certificates of confiscation. Money fails to serve its functions except as a medium of exchange!

In conclusion: Events are unfolding FAST, far faster than the powers that be are prepared to handle. Those Mono line bond insurers are a nuclear bomb to the financial and banking system and they are already priced for their demise - their stocks are down 70 to 90%, MBIA bonds are at 75 cents on the dollar and Ambac is at 36 cents on the dollar. In other words, JUNK. They are triple AAA only in the eyes of the ratings agencies which have been the fathers of soooo much of this situation in which we find ourselves. Ben Bernanke and the Mandarins of Washington DC need to just walk down the street and deposit money into their accounts, PERIOD. They cannot be allowed to fail! Trillions of dollars of bond valuations are on the line, not to mention the gigantic loss of confidence that will unfold if they are allowed to fail.

Ty Andros & Tedbits LIVE on web TV. Don't miss Ty interviewed live by Michael Yorba from Commodity Classics every week discussing this week's commentary and unfolding news. Catch the show every Wednesday at www.MN1.com or www.CommodityClassics.com at 4:15pm Central Standard Time . Archived video casts are available there as well.

If you enjoyed this edition of Tedbits then subscribe – it's free , and we ask you to send it to a friend and visit our archives for additional insights from previous editions, lively thoughts, and our guest commentaries. Tedbits is a weekly publication.

By Ty Andros

TraderView

Copyright © 2008 Ty Andros

Hi, my name is Ty Andros and I would like the chance to show you how to capture the opportunities discussed in this commentary. Click here and I will prepare a complimentary, no-obligation, custom-tailored set of portfolio recommendations designed to specifically meet your investment needs . Thank you. Ty can be reached at: tyandros@TraderView.com or at +1.312.338.7800

Tedbits is authored by Theodore "Ty" Andros , and is registered with TraderView, a registered CTA (Commodity Trading Advisor) and Global Asset Advisors (Introducing Broker). TraderView is a managed futures and alternative investment boutique. Mr. Andros began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Di ego , and the University of Miami , majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis, creating investment portfolios designed to capture these unfolding opportunities as the emerge. Ty prides himself on his personal preparation for the markets as they unfold and his ability to take this information and build professionally managed portfolios. Developing a loyal clientele.

Disclaimer - This report may include information obtained from sources believed to be reliable and accurate as of the date of this publication, but no independent verification has been made to ensure its accuracy or completeness. Opinions expressed are subject to change without notice. This report is not a request to engage in any transaction involving the purchase or sale of futures contracts or options on futures. There is a substantial risk of loss associated with trading futures, foreign exchange, and options on futures. This letter is not intended as investment advice, and its use in any respect is entirely the responsibility of the user. Past performance is never a guarantee of future results.

Ty Andros Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.