Audit the Out of Control Fed, Restore “Free Markets for Free People”

Interest-Rates / Central Banks Aug 02, 2012 - 03:42 AM GMTBy: Gary_Dorsch

When will the Fed’s folly and madness come to an end? Perhaps next year, we’ll begin to see big changes at the Federal Reserve, including the sacking of Fed chief Ben Bernanke, and his henchmen of addicted money printers, who have tossed aside the notion of “Moral Hazard,” a long time ago, and instead, are engaging in “financial repression” in the bond markets, and the rigging of the stock market, much to the chagrin of believers in free markets. However, in order for this shake-up at the Fed to occur, the Republican Party would have to beat the odds, by capturing the White House, and majorities in both chambers of Congress.

When will the Fed’s folly and madness come to an end? Perhaps next year, we’ll begin to see big changes at the Federal Reserve, including the sacking of Fed chief Ben Bernanke, and his henchmen of addicted money printers, who have tossed aside the notion of “Moral Hazard,” a long time ago, and instead, are engaging in “financial repression” in the bond markets, and the rigging of the stock market, much to the chagrin of believers in free markets. However, in order for this shake-up at the Fed to occur, the Republican Party would have to beat the odds, by capturing the White House, and majorities in both chambers of Congress.

Perhaps the most important piece of legislation to come down from Capitol Hill this year was HR #459, sponsored by Texas’s Ron Paul, a long-time critic of the Fed. By an overwhelming 327-98 vote, the House on July 25th voted to authorize Congress’ chief investigators to begin a forensic audit of the Fed’s secret activities in the markets, including its dealing with crony capitalists on Wall Street and in Europe. Nearly half of the Democrats in the House voted for the passage of HR #459, supporting the high-water mark for Mr Ron Paul, who has been pushing the slogan “End the Fed” for many years, and more recently “Audit the Fed.”

Before the House vote, Mr Paul noted that since the 2008 financial crisis erupted, the Fed has in essence, become the fourth branch of the US-government. “Today we have a combination of a secret Federal Reserve dealing with private banks who collude with private banks to set interest rates. At the same time they collude with the executive branch. They claim, they say we can’t have an audit of the Fed because it would make it political,” Paul said.

“Well, how can it be more political if the Treasury Department from the executive branch gets together with the Fed and bails out their friends? And then they want it kept secret. And they say it would be chaotic. Yea, it would be chaotic for those people who have been ripping us off. That’s why they don’t want to have it. They talk about, ‘I want transparency.’ And they talk about independence. Independence to them means secrecy,” Mr Paul declared.

Mr Paul also got political support from a far-left leaning Democrat, who is retiring from Washington politics at the end of this year. “The Fed wants to be spared a full audit,” said Rep. Dennis Kucinich, Ohio Democrat on July 25th. “They want monetary deliberations private. They then use that privacy shield to keep irregularities from regulators and from congressional view, exposing investors and consumers to massive losses. When things fall apart, to whom does the banks come to clean up the mess? Congress! ” Kucinich said.

“The Fed creates trillions of dollars out of nothing and gives it to banks. Congress is in the dark. The Fed sets the stage for the subprime meltdown. Congress is in the dark. The Fed takes a dive on LIBOR. Congress is in the dark. The Fed doesn’t tell regulators what is going on. Congress is in the dark. It’s time that we stood up to the Fed that right now acts like some kind of high, exalted priesthood, unaccountable to democracy,” Kucinich added.

Despite the broad support in the House, a senior Democrat in the Senate signaled that bill #459 isn't likely to go anywhere in that chamber in the near future. With the US-economy teetering on the brink of a “double-dip” recession, after muddling through the most anemic recovery since the 1930’s, the White House and leading Democrats, see the Fed as the only savior left, that can prevent a sharp slide in the US-stock market before the Nov 6th Elections. After all, a sudden slide in the US-stock market indexes of -10% or more, if left unchecked, could raise anxiety levels among a jittery American public. A sharp drop in the stock market could dampen consumers’ spirits further, lead to further cutbacks in spending by business, and usher in a new round of lethal jobs cuts.

Historically, the process of “price discovery” in the US-financial markets, has been determined by the collective judgments of millions of individual investors, and thousands of money managers, analyzing streams of news and information, used to set market prices. Likewise, the US-government’s policy towards the “price discovery” mechanism in the financial markets was summed up by the term, - “Laissez-Faire,” or leave it alone. Today however, the value of a wide range of bonds and stocks that are traded electronically on US-exchanges are increasingly determined by a handful of central bankers sitting on the Fed’s Board. There are wide spread suspicions that the Fed is actively intervening in the stock index futures markets, cushioning the market after sharp declines and engineering short squeeze rallies.

“Allowing the Fed to operate our nation's monetary system in almost complete secrecy leads to abuse, inflation, and a lower quality of life for every American,” Mr Paul warns. Indeed, in March of 2011, the Federal Reserve, under judicial order from the US Supreme Court, posted details of its “shadow bailout” scheme, in which it doled out upwards of $20-trillion of electronically printed monies, to rescue Wall Street bankers from the results of their own recklessness speculation. The Fed’s Primary Dealer Credit Facility, started in March of 2008, has lent $9-trillion in overnight loans to the largest investment banks. These vast sums were loaned out at rock-bottom interest without any strings attached.

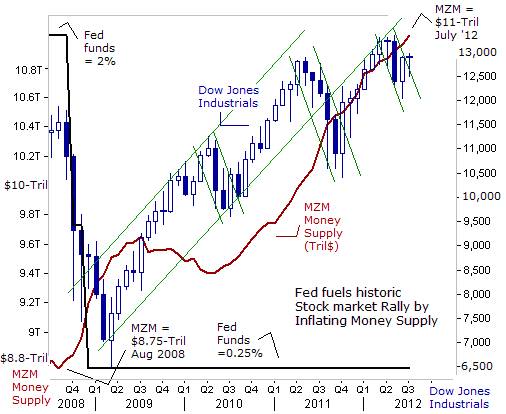

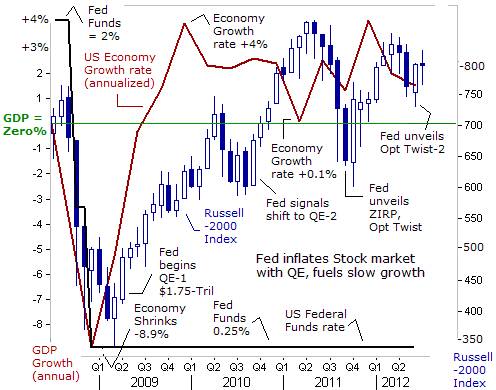

Since then, over the past 3-½-years, Mr Bernanke has been experimenting with several “Unorthodox” monetary schemes, - that are designed to artificially inflate the value of the stock market, and simultaneously boost the value of various types of marketable bonds, which are the principal assets held by the Wall Street banking Oligarchs. Essentially, the Fed is utilizing the blueprints designed by the Bank of Japan (BoJ) – the pioneer of several radical schemes, such as the “Zero Interest Rate Policy,” (ZIRP), “Quantitative Easing,” (QE), and large scale purchases of exchange traded funds in Tokyo, linked to the Nikkei-225 index.

Although the BoJ hasn’t succeeded in engineering a rally in the Nikkei-225 index above the 10,000-level, with the nuclear weapons in its toolbox, the Fed has been enormously successful with its intervention schemes. By leveraging $2.35-trillion of QE injections into the coffers of the Wall Street Oligarchs, since March of 2009, and more recently, mixed with ZIRP and “Operation Twist,” – a $665-billion scheme to drive long-term bond yields lower, the Fed has engineered an improbable doubling of the market value of the S&P-500 index.

The Russell-2000 index, which measures the value of the 2,000 smallest publicly traded US companies, has also doubled from its crisis bottom low hit in March of 2009. The US small-cap companies are more of a homegrown variety, earning less than 20% of their revenues from outside the US’s borders. That’s less than half of the exposure of the larger cap S&P-500 companies that collect about 45% of their earnings from overseas. Thus, the Russell-2000 index, should in theory, be less susceptible to the business cycles in foreign economies, and instead, should be mostly influenced by consumer and business demand in the US-economy. Still, while there are variations at the margins, the swings in the Russell-2000 index usually track the gyrations in the broader S&P-500-companies.

What’s most remarkable about the post-March 2009 recovery rally on Wall Street is that it marks the first time ever that the US-stock market has doubled in value in such a short time frame – of just three years. Since 1956, the average gain for the S&P-500 index, after three years of recovery from a Bear market low, has been �percent. Strangely enough, the US-stock markets’ outsized gains over the past 3-¼ years were accompanied by the weakest economic recovery since the 1930’s. Since the “Great Recession” officially ended in June of 2009, the US-economy has grown by +6.7%. That’s far less than the Reagan recovery, when the US-economy grew +18.5% over a three-year period, after the 1982 recession ended.

Clearly, the US-stock market’s outsized gains, blowing through the headwinds of an anemic economic recovery, is an anomaly that’s best explained by the Fed’s ultra-easy money policies. Today, the US-stock markets are under the “command and control” of the Federal Reserve, and in coordination with the US Treasury - wielding its powerful influence in the markets, through its ability to print unlimited amounts of US-dollars, and according to conspiracy theorists, the Fed also engages in clandestine intervention forays in the marketplace, through strategic purchases of stock index futures contracts. Only a complete “Audit of the Fed” can uncover the trail of the central bank’s secret dealings, and either confirm or deny the validity of long held conspiracy theories of clandestine Fed intervention.

With only 100-days before the upcoming Presidential election, the Obama White House cannot afford to suffer through a crash in the stock market before Nov 6th. Yet Macro traders are baffled by the resiliency of the US-stock market, including the Russell-2000 index, even in the face of mounting evidence that the US-economy is sliding into a recession. For example, US-retail sales have declined for 3-straight months. Since the end of World War II, there’s been 27 occasions when retail sales fell for three months in a row, and in 25 of those instances, the US-economy was already in recession or was within 3-months of entering into a recession.

A big reason that US-economic growth is so weak is the decisions of US-consumers to save more and spend less. Personal saving rose by $56-billion in the second quarter, almost equal to personal spending of $60-billion. However, spending in Q’2 was sharply less than the $143-billion of outlays in Q’1. In effect, consumers decided to save nearly one out of every two dollars in additional income, a clear indication of mounting concern over job security and the rising cost of living. Yet there are no alarm bells ringing on Wall Street.

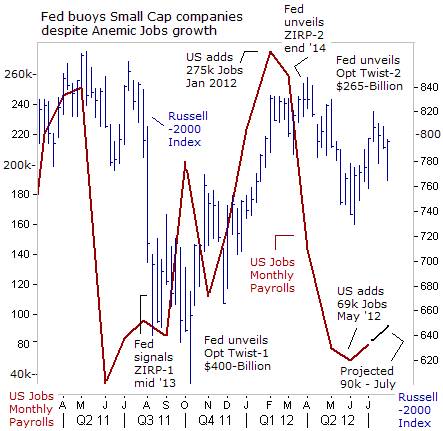

The US-economy is already sliding into a downward spiral, as long-term unemployment and the lack of new job creation is curbing consumer spending. Confidence among US-small companies dropped in June by the most in 2-years, driven by worries that future sales will continue to deteriorate. Fewer small employers plan to hire, accounting for the sluggish growth in payrolls. A net 3% of small companies plan to increase staff over the next three months, according to a survey taken by the National Federation of Independent Business. Instead, employers are relying on existing workers and temporary hires to avoid growing their payrolls. A net 5% of small business owners thought it was a good time to expand.

In Q’2, the US-economy created just 225,000 new jobs, a third of which were temporary or part time. That’s just a third of the amount of jobs that were created in the first quarter. Government spending is a net drag on the economy, still declining over the past two years, while corporations are sitting on a cash hoard of $1.7-trillion, and refusing to invest or hire new workers, while banks are sitting on $1.5-trillion in excess reserves, and refuse to lend.

During the months of April and May, more than $1-trillion was erased from US equity values as the S&P-500 index fell -10% to the 1,280-level. Yet since June 4th, the S&P-500 index has suddenly surged higher, in a powerful upside explosive rally to the 1,385-level. The stock market is climbing sharply higher even in the face of a rapidly deteriorating economic background. The Russell-2000 index has also tagged along for the ride, but is lagging behind the large caps. This has led to suspicions that the Fed is concentrating its firepower in the Dow Industrials futures contract, in order to get the biggest bang for the buck.

Typically, the direction of the US-stock market anticipates the trends in the business cycle by six months in advance. Given the severely weakened state of the US-economy, one could’ve expected that the Russell-2000 index would’ve fallen into correction territory by now, if the majority of traders truly believed that the US-economy was sliding into a “double-dip” recession that could badly crimp earnings. So far, that’s not happening. Instead, the expectation that the Fed could launch a $500-billion QE-3 printing spree is elevating the stock market, in a gravity defying magic act.

One year ago, sharp declines in retail sales and anemic jobs growth, combined with an upward spiral in Italian bond yields above 7-percent, triggered the “Crash of 2011,” that knocked the S&P-500 index for a sudden and unexpected loss of -20%. The Dow Industrials lost 2,000-points during the onslaught, and the Russell-2000 index fell into a mini Bear market, losing a quarter of its value. Fearing a replay, the Fed has intervened aggressively in the marketplace in recent weeks, and regularly sends signals through the financial media, about its threats to begin a new round of money printing, (QE) on a massive scale, that in turn, could be used by speculators to bid-up commodities and equities. Thanks to the Fed’s “serial bubble blowing,” the gulf between a booming stock market and a sinking US-economy has never been wider.

“Auditing the Fed” would remove the veil of secrecy that cloaks the central bank from public view, while it prints trillions of dollars out of thin air, without accountability or transparency. The Fed’s QE monies end-up in the hands of hedge funds and other big speculators, and it’s agents on Wall Street, that’s used to bid-up the prices of key commodities, such as in the energy and grains markets. If the Fed should decide to print $500-billion of extra cash in the future, under the guise of QE-3 operation, who would benefit and who would suffer?

Considering the fact that the richest 10% of Americans control 81% of the shares in the US-stock market, - this group would certainly be the biggest winner. However, half of US-households own no stocks at all, and they would be the biggest losers, since QE-3 could fuel an upward spiral in the cost of food and energy. The lowest income earners already spend a third of their budgets on food and energy. Americans living on fixed incomes and those with stagnant wages would find that their US-dollars buy less at the grocery store and the gasoline station. Yet the Fed doesn’t even consider the prices for food and energy in its inflation equation. A fresh blast of QE-3 would only further widen the gap between rich and poor.

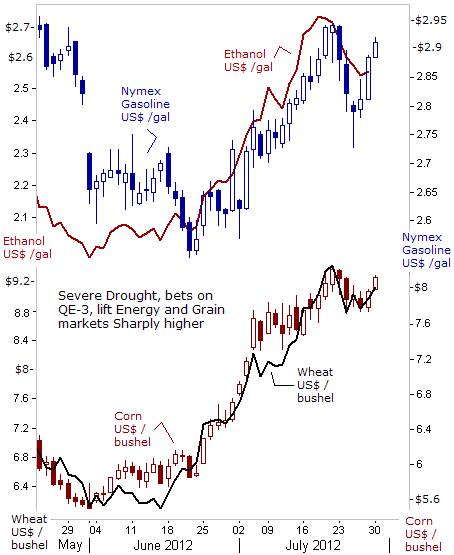

Unleashing QE-3 is a wrong headed economic policy. QE-3 could backfire on the Obama re-election campaign, if it manages to spike the price of gasoline, or jack-up the cost of a loaf of bread. Already, the price of food staples, such as corn and wheat have surged +50% higher since June 4th, and soybeans have soared above $17 /bushel, as the worst drought since the 1934 Dust Bowl continues to plague more than half the country. The wholesale price of unleaded gasoline has climbed 35-cents a gallon higher in recent weeks, on speculation that the Fed could unleash QE-3. The cost of Ethanol, used as an additive in gasoline, has increased by 65-cents a gallon over the past 6-weeks. Mixing the elixir of QE-3 with the Dust Bowl in the Midwest region would be like dropping a lit match into a tinderbox of explosives that could ignite powerful rallies in the agricultural and gasoline markets, above and beyond their already elevated levels, and fueling a whole new round of inflation.

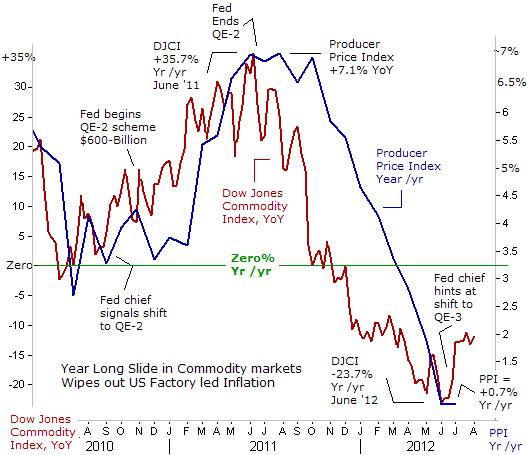

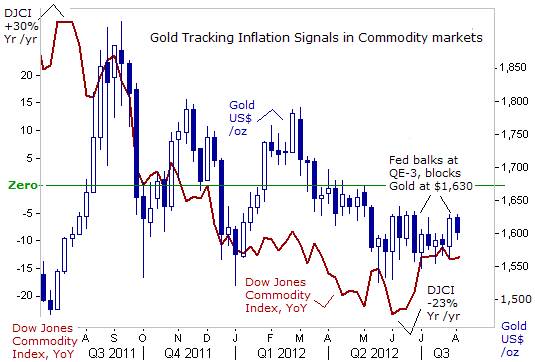

NY Gold Tracking Inflation Signals in Commodity markets, Sounding the alarm bells and warning about a whole new round of inflation, sounds extremist and rings hollow at this point, following a year long slide in commodity prices, that knocked the Dow Jones Commodity Index (DJCI) as much as -24% lower in the month of June, compared with a year earlier. There were deep losses in the soft agricultural markets, sizeable losses in metals, and shallower losses in the energy markets, for crude oil and gasoline.

Once the Fed switched off the QE-2 printing press, at the end of June 2011, the inflationary pressures that were emanating from the commodity markets began to quickly unwind. The Euro’s year long slide against the US-dollar, falling -17% in value, also weighed heavily on the global commodities markets. By of June 2012, the drop in commodity prices had whittled down the US’s producer price index (PPI) to just +0.7% compared with a year earlier, and sharply below its peak level of +7.1% in Q’2 of 2011. Gyrations in the broad commodity indexes are reliable indicators of the future course of inflation rates in many countries.

With the PPI’s rate of inflation tumbling to a razor thin cushion above zero percent, the Fed could’ve been justified in taking pre-emptive action against the threat of deflation, from taking hold in the US-economy, by launching a third round of QE. At the core of Bernanke’s radical thinking is a determination to avoid deflation at any and all costs, usually by flooding the banking system with a tsunami of cheap “money,” in order to prevent prices from falling. This strategy is based on the idea that “too much money, chasing too few goods and services, can at least prevent a fall in the general price level.”

Much of the Fed’s thinking on the extreme importance of fighting deflation is described in a Fed study, published in 2002. The Fed study - written by 13 economists, asserts that Japan’s experience with deflation shows that the central banks should go extra lengths to revive a slumping economy well before inflation dwindles to zero. That’s because deflation is more debilitating to economies - and harder to control - than inflation. Accordingly, as interest and inflation rates sink closer to zero, policymakers should “take out sufficient insurance” against the prospect of deflation, the study says. In today’s world, that means QE and ZIRP.

The year long unwinding of inflationary pressures in the commodity markets, ending in June, has also taken a toll on the Gold market, which fell by -20% from its all-time high of $1,925 /oz, reached in August 2011, to as low as $1,550 /oz in Q’2 of 2012. Gold fell to the threshold of a Bear market, with its -20% slide, before stronger handed buyers suddenly emerged, jumping into the yellow metal, at the same time the deflationary trend in commodities was fizzling out. Buoyed by the drought in the US’s Farm Belt, and big bets wagered on the Fed’s dangling promises of QE-3, the Gold market began to stabilize within a sideways trading range, with support seen at the $1,550 /oz level, and stiff resistance at $1,630 /oz.

On August 1st, the Fed disappointed the Gold Bugs by keeping its QE powder dry, - and taking no new additional actions to jolt the US-stock market higher. Without the magic elixir of QE-3, the Gold market fell prey to profit-taking at $1,630 /oz and soon wilted below $1,600 /oz. It was one of the few times that Fed chief Ben “Bubbles” Bernanke has disappointed the Bullish crowd on Wall Street. Risk-On traders have become programmed to expect the exercising of the “Bernanke Put” and they were bullying the Fed into launching QE-3 by lifting the Dow Jones Industrials above the 13,000-level.

However, the annualized rate of decline in the Dow Jones Commodity Index (DJCI) has already been cut in half since June 4th, to around -12% today. If the DJCI’s market value can hold steady near today’s 145-level by late September, its year-over-year change would reach zero-percent, and extinguish the threat of deflation from taking hold in the US-economy. The Fed figures it can wait until the next scheduled meeting set for Sept 12th, to see if the deflationary trends in the commodity markets continue to unwind.

Yet the headwinds blowing against President Obama’s re-election campaign are getting stronger. The US-economy is sinking towards the edge of a “double-dip” recession. Small business owners, responsible for 2/3’s of the hiring in the United States, are clamping down on spending. The U-6 jobless rate including the under-employed is stuck near 15%. Six of the 17 countries in the Euro-zone are stuck in a recession, saddled with an average 11.2% jobless rate. Emerging economies in China, Brazil, India, Korea, and Taiwan are also slowing and exports are contracting. The general consensus is that QE-3 in the United States or backdoor QE in the Euro-zone wouldn’t ignite a Trans-Atlantic economic recovery.

For the seven Presidents returned to the White House since World War II, the US’s economy’s growth rate averaged +4.7% during the first nine months of their re-election year. Ronald Reagan’s economy expanded at a +6.3% annualized rate during the first nine months of 1984. Bill Clinton headed toward re-election in 1996, with the economy growing at a +4.5% clip. Bush was re-elected with growth averaging a scant +2.8% the first nine months of 2004. However, for Obama, growth has averaged just +1.7-percent. Yet at the online betting parlor at Intrade.com, Obama is the odds on favorite to win re-election, by a 57% to 41% spread.

Traders are Intrade.com are a bit lazy, simply figuring that the direction of the Dow Jones Industrials between now and Election Day would determine the winner on Nov 6th. With the Dow hovering closer to the 13,000-level, Obama’s odds of winning re-lection are pegged at 57%. If the Dow suddenly skids towards the 12,000-level, Obama’s odds of winning would fall towards 52%, essentially a dead-even race with the Republican challenger Mitt Romney. If the Dow falls below 12,000 however, Obama could lose the upcoming election.

Right now, Bernanke is playing the stock market like a fiddle. Strongly hinting at QE-3 to the media in order to jig the market upwards, - then disappointing market Bulls after big rallies, by holding pat and keeping his powder dry. Mr Bernanke aims to stay politically neutral ahead of the Nov 6th elections, and the last window of opportunity to launch QE-3 before Nov 6th has probably closed. If the Fed unleashed QE-3 before Nov 6th, and if the Republicans capture the White House, the Fed chief would pay a heavy political price in January. The “Audit the Fed” bill would become a reality and so would the dismantling of the Fed’s secretive interventionist schemes in the marketplace. Mr Ron Paul has set the wheel in motion, - only time will tell if American voters are ready to restore the slogan, “Free Markets for Free People.”

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2012 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.