The "Fear" Trade, Gold the Only True Safehaven

Stock-Markets / Financial Markets 2012 Aug 17, 2012 - 12:45 PM GMTBy: Richard_Mills

Stocks and interest rates are back to late spring – pre latest European fear levels - and the Jefferies/Thomson Reuters CRB index is at a three-month high.

Stocks and interest rates are back to late spring – pre latest European fear levels - and the Jefferies/Thomson Reuters CRB index is at a three-month high.

Risk assets are obviously back in favor with investors - possible action by the European Central Bank (ECB) and the US Federal Reserve (Fed) could offer an explanation why:

- There is speculation Fed Chairman Ben Bernanke could signal another round of quantitative easing at the Jackson Hole, Wyo. end of August Fed meeting

- ECB President Mario Draghi promised to defend the euro so markets are expecting a move from Europe’s central bank

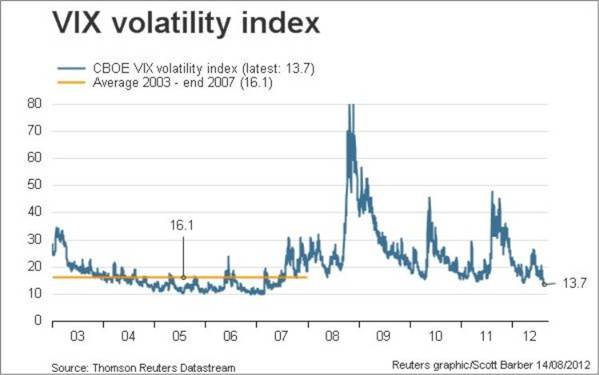

The CBOE Market Volatility Index, the VIX or “Fear Index” as it’s known recently hit its lowest level since the global credit crisis erupted five years ago.

Mike Dolan offers us an explanation of what the VIX is and questions why such high levels of investors complacency…

“Given almost biblical gloom about the world economy at the moment, you really have to do a double take looking at Wall Street’s so-called “Fear Index”. The VIX, which is essentially the cost of options on S&P500 equities, acts as a geiger counter for both U.S. and global financial markets.

Measuring implied volatility in the market, the index surges when the demand for options protection against sharp moves in stock prices is high and falls back when investors are sufficiently comfortable with prevailing trends to feel little need to hedge portfolios. In practice — at least over the past 10 years — high volatility typically means sharp market falls and so the ViX goes up when the market is falling and vice versa. And because it’s used in risk models the world over as a proxy for global financial risk, a rising ViX tends to shoo investors away from risky assets while a falling ViX pulls them in — feeding the metronomic risk on/risk off behaviour in world markets and, arguably, exaggerating dangerously pro-cyclical trading and investment strategies.

Well, can that picture of an anxiety-free investment world really be accurate? It’s easy to dismiss it and blame a thousand “technical factors” for its recent precipitous decline. On the other hand, it’s also easy to forget the performance of the underlying market has been remarkable too. Year-to-date gains on Wall St this year have been the second best since 1998. And while the U.S. and world economies hit another rough patch over the second quarter, the incoming U.S. economic data is far from universally poor and many economists see activity stabilising again.

But is all that enough for the lowest level of “fear” since the fateful August of 2007? The answer is likely rooted in another sort of “put” outside the options market — the policy “put”, essentially the implied insurance the Fed has offered investors by saying it will act again to print money and buy bonds in a third round of quantitative easing (QE3) if the economy or financial market conditions deteriorate sharply again.” Mike Dolan, Put Down and Fed Up, blogs.reuters.com

reuters.com

Risk On

There is no doubt in this author’s mind most people believe the world’s governments and central banks will step in with some form of quantitative easing. Current market conditions are clearly showing this.

In a risk on type of situation, meaning Draghi and Bernanke come through, commodities would seem like a good place to have my money.

Why? Well the long-term average ratio of the Commodities Research Bureau Index versus the S&P 500 is 1.5 times. This ratio indicates how much S&P 500 stock you can buy with a fixed basket of commodities.

The ratio was recently at 0.2 times - an all time low valuation between hard assets and financial assets.

Risk Off

There are many reasons “risk on” could suddenly become “risk off”:

- Continued negative headlines from Europe

- Weaker U.S., Chinese and global growth

- Slowing corporate profits

- Draghi or Bernanke, or both, fail to act

Bonds and gold are “risk off,” Fear Trade investments people buy when they want safety.

Bonds

Unfortunately there’s something most bond investors do not understand – negative REAL interest rates.

“Over time even small levels of inflation can make a big difference in the purchasing power of your investment…If your rate of return isn’t greater than the rate of inflation, then the real value of your investment (the inflation adjusted value) drops and, with it, your spending power. So even though it looks like you have more money, you can actually buy less with it.” inflationdata.com

The benchmark US 10-year note currently yields 1.63 percent, yields on 30 year bonds are 2.75 percent.

The following is the inflation data for the first six months of 2012, the Inflation rate is calculated from the Consumer Price Index (CPI-U) which is compiled by the Bureau of Labor Statistics (BLS).

Jan 2.93%, Feb 2.87%, Mar 2.65%, Apr 2.30%, May 1.70%, June 1.66%

Treasury Inflation Protected Securities (TIPS) adjust your investment value according to changes in the Consumer Price Index (CPI) - the inflation rate - when there is inflation, or a rise in the CPI, the principal increases and, with deflation, the principal decreases.

John Williams, author of the newsletter Shadow Government Statistics, takes issue with the statistical methodology used by the US Bureau of Labor Statistics (BLS).

Williams says if the BLS hadn't altered its statistical practices over the years, inflation, as measured by the governments CPI, would have been reported about seven percentage points higher each year.

"the Committee expects to maintain a highly accommodative stance for monetary policy. In particular, the Committee decided today to keep the target range for the federal funds rate at 0 to 1/4 percent...at least through late 2014. The Committee also decided to continue through the end of the year its program to extend the average maturity of its holdings of securities…This continuation of the maturity extension program should put downward pressure on longer-term interest rates" U.S. Federal Reserve Reaffirms Low-Rate Policy, June 20th 2012

Gold The demand for gold moves inversely to interest rates - the higher the rate of interest the lower the demand for gold, the lower the rate of interest the higher the demand for gold.

The reason for this is simple, when real interest rates are low, at, or below zero, cash and bonds fall out of favor because the real return is lower than inflation - if your earning 1.6 percent on your money but inflation is running 2.7 percent the real rate you are earning is negative 1.1 percent - an investor is actually losing purchasing power. Gold is the most proven investment to offer a return greater than inflation (by its rising price) or at least not a loss of purchasing power.

Gold's price is tied to low/negative real interest rates which are essentially the by-product of inflation - when real rates are low, the price of gold can/will rise, of course when real rates are rising, gold can fall very quickly.

Fact - as long as real interest rates are low gold is in a bull market, there are no plans to raise interest rates for at least two years, indeed the Fed is actively working to lower longer term rates.

Consider:

- Since 1913 the US dollar has lost over 95% of its purchasing power

- Gold has gone from US$20 an ounce to currently over US$1600.00 per ounce in the same time frame

- Continuing low interest rates, combined with higher inflation rates will continue to cause low to negative real rates of return

The “Fear” Trade comprises bonds and gold, if bonds aren’t worth holding because of negative real interest rates that leaves gold as the only true safe haven asset.

Conclusion

Is it risk on, or risk off? Are we looking at a fear trade situation where gold is the only true safe haven asset? Or will the world’s central banks open the monetary floodgates as many suspect is going to happen?

The actions of the world’s central banks should be on everyone’s radar screen. Are they on yours?

If not, maybe they should be.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including:

Wall Street Journal, Market Oracle, SafeHaven , USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2012 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.