How Social Security Trust Funds Will Change Private Retirement Income

Politics / Pensions & Retirement Mar 12, 2014 - 06:15 AM GMTBy: Dan_Amerman

It can be difficult to completely avoid a $5 trillion elephant in the middle of one's own living room.

It can be difficult to completely avoid a $5 trillion elephant in the middle of one's own living room.

In an ironic twist, millions of people who are investing for retirement specifically to escape from dependence on Social Security may find that no matter where in the room they go - that elephant is still there. And over the years ahead, the spending down of the $5 trillion in Treasury bonds held in Social Security and other government trust funds may be transforming the returns on their private savings in ways they never anticipated.

As we will explore herein in this nonpartisan analysis - using official government data - there are no real assets, but instead the government trust funds consist of $5 trillion of unfunded liabilities. With the only source of funds for paying the trust funds being to borrow still more money.

At the same time, despite the lack of real assets in the trust funds,neither the national debt nor the federal deficit will directly rise as a result of paying out the promised retirement benefits. However, these headline measures of total debt and total deficits are only the surface level.

What will matter for investors is what will be happening beneath the misleading surface, with reality being that the government has to come up with the missing $5 trillion from somewhere. Which will necessarily involve a radical transformation of the nature of the federal debt, in terms of who is providing the funds, and potentially how much interest will need to be paid.

And this whole process could threaten the very solvency of the United States government.

Unless, that is, countermeasures are taken. And it is those countermeasures that could impact investment performance in multiple categories for decades to come. It is those countermeasures that could reduce retirement investment income over the long term for tens of millions of private investors.

To understand this overlooked but potentially transformative issue, we will start by looking at what the trust funds really are, from three different perspectives. We will then "follow the money" through four different stages to find out the market-changing ways in which those trillions of dollars will be moving around, which aren't captured by most measures of debt or deficits.

The First Level Of Reality: The Public Facade

The way that Social Security is officially presented is that it is not really a tax - but a government-mandated and guaranteed retirement fund that exists for the benefit of American workers.

Each worker is required to take a portion of their paycheck and invest it in the Social Security trust funds. And as the narrative goes, these monies are taken by the US government and responsibly invested in the safest of all assets - those being the obligations of the United States Treasury.

As the population ages and reaches the point (as it now has) where the monies coming in from payroll taxes are no longer enough to pay out what is required, the US government will then begin to responsibly draw down this available cash that was invested for the benefit of retirees, so that payments can be made to retirees without needing to either increase taxes or increase borrowings.

The whole thing looks and sounds pretty darn good.

But is that what's really happening?

The Second Level Of Trust Fund Reality: Economic Literacy

There is a quite different - and I would argue much more reality-based - view of Social Security and other trust funds, that has been understood among the most financially and economically literate parts of society for some decades now. One of my favorite quotes on the subject is from Peter Peterson, who was at the time chairman and founder of the Blackstone Group, one of the world's largest and most prestigious money-management firms:

"The term 'government trust fund' is a fiscal oxymoron. You shouldn't trust them and they are not funds. In fact, government trust funds accomplish no savings at all. The money is spent as soon as it is collected. Whether you have a trust fund or not is economically irrelevant. With or without the trust fund, you're either going to have to undertake huge, and I think, unacceptable tax increases, or sudden and draconian cuts in benefits." (CFA Magazine, January/February 2004 issue)

What really happened with Social Security payments over the decades was that the government took the receipts from payroll taxes, sent most of the payments to current beneficiaries, and immediately spent every penny of what remained on general government purposes.

And in exchange for taking that money and spending it, the government wrote itself an IOU in the form of US Treasury bonds.

This is somewhat akin to your writing yourself a check for $1 billion.

The only way that you can pay off that check is to come up with $1 billion.

If you don't come up with $1 billion, the check isn't good - and if you do come up with $1 billion, well you didn't need the check in the first place. So the existence of the check is irrelevant either way.

This is really very simple. There are no stocks in the trust fund, there are no corporate bonds, there are no bonds from other nations - there are no real investments in the sense that most people would view savings or assets.

The government collected a steeply regressive tax from many millions of lower and middle-income workers, it spent every dime, and what is called the Social Security trust fund is nothing more than a collection of IOUs written to itself. And the government needs to come up with the money to pay off those IOUs, or they won't get paid.

This could also be likened to funding your retirement by following a disciplined schedule of writing yourself a check each month and putting it in a drawer. Everything looks great - until you retire and start trying to cash the checks.

While this is all very sound and simple logic, it is simultaneously a perspective that politicians won't touch with a 10 foot pole - and the media doesn't seem all that eager to shine a light on it either.

The Third Level Of Reality: The Assets Aren't Real, But The Liabilities Are

To understand the third - and governing - level of reality for Social Security and other government trust funds invested in government bonds, let's continue with the analogy of writing a monthly retirement check and putting it in a drawer.

Except this time, the check isn't written to ourselves - but to our employees, as part of a legally-binding pension obligation. When the checks start getting pulled out of the drawer to be cashed many years later, we must either find the money to make good on the checks - or we have to declare bankruptcy.

What a reversal! Instead of having a drawer full of assets, we now have a drawer full of legally-binding obligations. And if we don't scramble to come up with the money to put into our account to pay off those checks over time, it's game over - default and bankruptcy.

To understand that analogy is to understand the true relationship between the Federal Government and the Social Security trust funds.

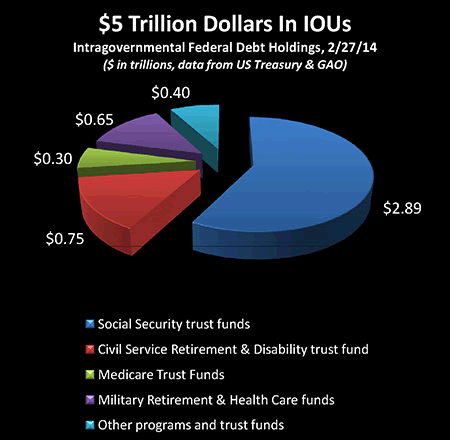

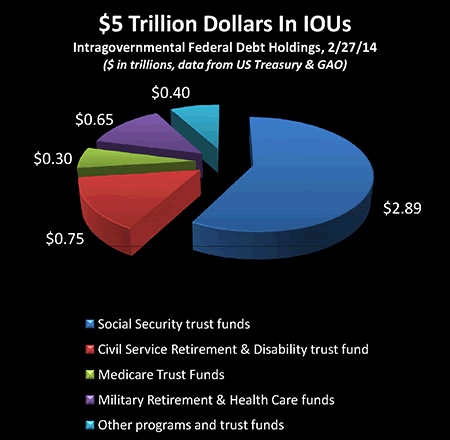

Now while there may not be any real assets in Social Security or other government trust funds, the liabilities are entirely real. Indeed, as can be seen in the graph above, the Social Security trust funds hold about $2.9 trillion in US Treasury obligations, and other government retirement trust funds hold about $2.1 trillion worth, for a total of $5 trillion.

That $5 trillion must be paid - or the US government has failed to meet its contractual obligations and is insolvent.

Following The Money

No matter how complex they may seem, many financial deceptions can be unraveled by a basic process - just follow the money.

To see what is currently almost universally being missed about Social Security and other government retirement trust funds, we merely need to follow what is actually going on at four distinct points: 1) when the money comes in; 2) the years during which the money is "invested"; 3) the redemption of the principal due; and 4) the aftermath of the redemption.

The 2nd half of this article follows the money step by step, it integrates the government trust funds with what the Federal Reserve has been doing with monetary creation to buy Treasury bonds, and shows why the future may be very different from the past.

Daniel R. Amerman, CFA

Website: http://danielamerman.com/

E-mail: mail@the-great-retirement-experiment.com

Daniel R. Amerman, Chartered Financial Analyst with MBA and BSBA degrees in finance, is a former investment banker who developed sophisticated new financial products for institutional investors (in the 1980s), and was the author of McGraw-Hill's lead reference book on mortgage derivatives in the mid-1990s. An outspoken critic of the conventional wisdom about long-term investing and retirement planning, Mr. Amerman has spent more than a decade creating a radically different set of individual investor solutions designed to prosper in an environment of economic turmoil, broken government promises, repressive government taxation and collapsing conventional retirement portfolios

© 2014 Copyright Dan Amerman - All Rights Reserved

Disclaimer: This article contains the ideas and opinions of the author. It is a conceptual exploration of financial and general economic principles. As with any financial discussion of the future, there cannot be any absolute certainty. What this article does not contain is specific investment, legal, tax or any other form of professional advice. If specific advice is needed, it should be sought from an appropriate professional. Any liability, responsibility or warranty for the results of the application of principles contained in the article, website, readings, videos, DVDs, books and related materials, either directly or indirectly, are expressly disclaimed by the author.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.