A Recession Indicator for Independent Thinkers

Economics / Recession May 28, 2018 - 08:23 AM GMTBy: F_F_Wiley

Last month we took sides in the ongoing debate about the Great Yield Curve Scare—we argued that the curve hasn’t flattened enough to deliver a strong recession signal at this point in time. We showed that the recent flattening is similar to those that occurred at various stages of the last nine business-cycle expansions, but usually before the midpoints. In other words, history places today’s curve in an early- or mid-cycle position, not late-cycle as commonly believed. We concluded that the recent flattening isn’t all that interesting as far as the business cycle is concerned.

Last month we took sides in the ongoing debate about the Great Yield Curve Scare—we argued that the curve hasn’t flattened enough to deliver a strong recession signal at this point in time. We showed that the recent flattening is similar to those that occurred at various stages of the last nine business-cycle expansions, but usually before the midpoints. In other words, history places today’s curve in an early- or mid-cycle position, not late-cycle as commonly believed. We concluded that the recent flattening isn’t all that interesting as far as the business cycle is concerned.

Now we’ll broaden the discussion to consider a related indicator, one that we like because it looks directly at the bank credit cycle. Our bank credit indicator is worth watching, for two reasons. First, the latest readings are more interesting than the latest yield curve readings, as you’ll see in Part 2. Second, bank credit is arguably more fundamental to the business cycle than any other measurable piece of the economy.

If you’ve followed our recent work, neither of our two claims should surprise you. This isn’t the first time we’ve written about bank credit—we’ve occasionally tried to popularize a way of thinking about banks that’s distinctly unpopular, albeit consistent with certain heterodox schools of macro. In fact, this article is a companion piece to “An Inflation Indicator to Watch,” a follow-up to “Learning from the 1980s,” and we’re also drawing from our book Economic for Independent Thinkers. We’ll recap a few points from that earlier work here, but to make our repetition seem a little less repetitive, this time we’ll explain the points differently. Namely, we’ll ask you to picture yourself as part of the story.

See the Banker, Be the Banker

Imagine you’re an experienced banker who understands both the legalities of bank charters and the mechanics of loans, and you’ve been asked to prepare for a new assignment by refreshing your understanding of two big, broad and overlapping topics—the economy and the business cycle. You’ve cleared your schedule and holed up in a quiet room with only a stack of relevant books and papers, a thick pad of paper and your deep thoughts. I’ll call you IT, short for Independent Thinker.

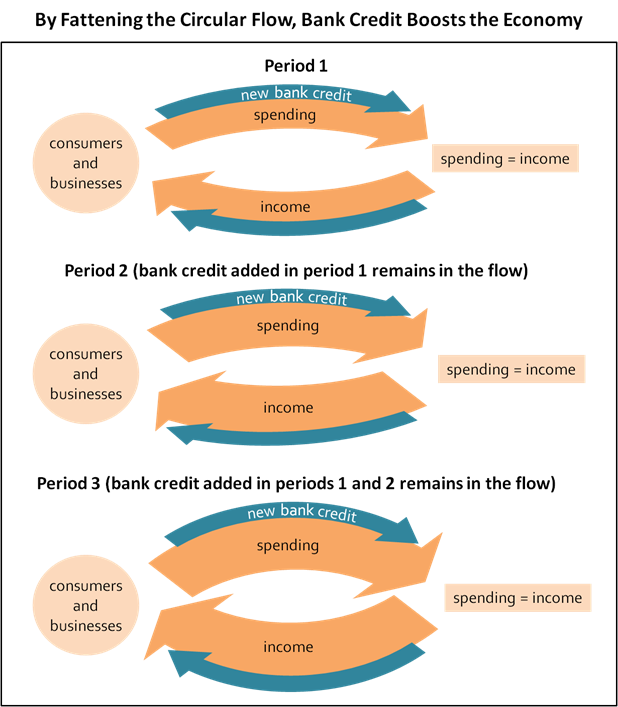

Now imagine a second character, the CEO of your bank, whom I’ll call him BBM for Big Boss Man. BBM is the one who handed down your assignment and hopes to benefit from your preparations. One day, he knocks on the door of your room and asks if you wouldn’t mind fielding a few questions about how your bank fits into the big picture. Happy for the chance to put your growing pile of notes to good use, you hand him your latest sketch:

You remind BBM that bank loans create money—in the form of deposits or cashier’s checks—from virtually nothing, and that the new bank-created money flows directly into nominal GDP as borrowers spend it. It might boost GDP’s real growth component or its inflation component or both real growth and inflation, but regardless of which component is most affected, bank lending is fundamentally different to the lending that takes place outside the banking system. Loans that aren’t extended by banks require the lender to accept a reduction in purchasing power in favor of the borrower, whereas bank loans require no such trade-off.

You then explain that your diagram also operates in reverse—the circular flow contracts when old loans are redeemed, sold or written off at a faster pace than new loans are extended, or in other words, when bank balance sheets shrink. Stating the obvious, you conclude that banks have quite a lot to do with the business cycle.

If the Keynesians Have Fixed Keynesianism, Then I’m Elvis Presley

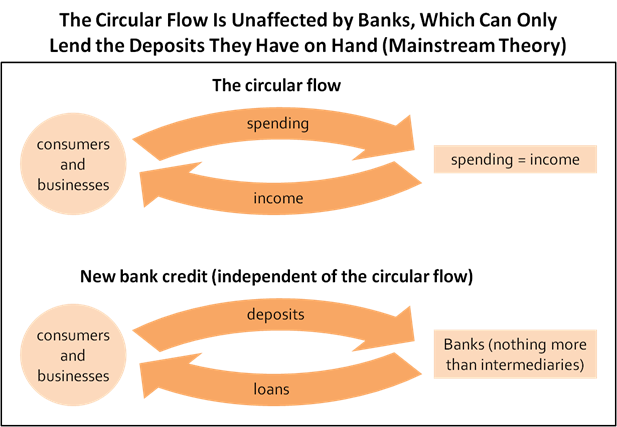

BBM offers a slight nod of approval, and then pulls out a competing sketch from the whippersnapper your bank recently hired as an economic analyst, fresh from a prestigious Ivy League program. I’ll call him AC for Abundant Credentials. AC’s diagram looks like this:

As you and BBM compare the diagrams, in walks one of your asset management division’s sharpest portfolio managers, one who never whiffs on an opportunity to trash economic theory. I’ll call him DT for Doubting Thomas. We’ll pick up the conversation as DT explains that he couldn’t reach BBM by phone.

DT: “BBM, can’t you hear me when I call?”

BBM: “Sorry, we’re deep in thought here. Good timing, though—didn’t you ditch a graduate program because you wanted to live in the real world, not the world of abstract theory?”

DT: “Something like that. My passion is the macro economy, and the curriculum for that subject is garbage.”

BBM (handing over AC’s diagram): “You mean like this?”

DT: “Yup, 100% garbage. Ever since the earliest Keynesian model, students are led to believe that money is one thing, lending is entirely independent of money, and banks are irrelevant—they’re nothing more than intermediaries. And those assumptions then lead to a whole lot of other illogical beliefs.”

BBM: “But don’t many economists admit those problems and claim to have fixed them?”

DT: “Sure they do, but they’re claiming to have extinguished a blazing house fire with squirt guns and water balloons. The problems are too widespread and deep-rooted. Fixing them means just about starting over—it means going back to where macro was before Keynesianism and then working forward from those economists who objected to Keynesian modeling, such as Joseph Schumpeter. And when you do that, you’re not in the mainstream anymore.

IT: “I have to agree with Tom. Every day I see commentary that fails the simple test of allowing that the circular flow expands and contracts with changes in bank credit.”

DT (increasingly animated and preachy): “Everyday commentary, textbooks, countless papers, many supposedly seminal papers and all of the foundational models in mainstream macro get money and banking wrong. It’s far from the only chasm in mainstream theory, but it’s an absolute killer—a Grand Canyon of wrongheadedness. Building macro theory without a proper role for banks is like building language without vowels, chemistry without water. It’s like—”

Nevermind Your Ms, Vs, Ps and Qs

DT stops as the door opens again and our fifth character walks in. We’ll call him UM for Useful Monetarist, “useful” because this character, as if in some corny comedy, can’t tell a lie. After some small talk, UM learns that BBM, IT and DT were discussing connections between banks and the economy. Curious, he decides to stick around. BBM then resumes his questioning.

BBM: “Let’s say I’m looking for indicators that pick up the banking system’s economic effects. What should I choose?”

UM: “Why don’t you look at money? Didn’t you know, MV=PQ. You could look at M2 along with the velocity of M2 and that gives you the M and the V.”

DT (more composed now but still on edge): “Why would we do that? M2 hasn’t worked since the 1970s—ever since it lost its correlation to bank lending, it’s been uncorrelated to GDP. It’s been so bad that the Conference Board finally chucked it out of its Leading Economic Index (LEI) in 2012. And V is just the answer you give when someone asks ‘What’s GDP divided by M?’ It’s neither independently measurable nor predictive, and it probably never will be predictive.”

UM: “But the longer history for M2 is strong. Just look at Milton Friedman and Anna Schwartz‘s A Monetary History of the United States, 1867–1960, which might be the greatest empirical work ever.”

DT: “Well, a lot of people would agree with you, but in fact that book wasn’t about M2. The authors used measures that mostly tell you about bank balance sheets and, therefore, bank lending (also coinage and lending-related currency issuance, neither of which are especially relevant anymore). So their research was excellent as long as you accept that it revealed the economic effects of bank lending and that it said nothing about M1, M2, M3 or any of the other monetary aggregates, which only later became the hip and intelligent-sounding indicators to include in your chart books.”

BBM: “So you’re telling me to look at bank credit and ignore the monetary aggregates?”

DT: “Exactly. Think about how the early Monetarists chose components for all of their Ms. They used criteria such as liquidity, stability and the effectiveness of each component as a medium of exchange, as if there’s a greater truth hidden in how many twenties we carry in our wallets versus our CD and money market holdings. Ideally, economists should have been looking at something else entirely. They should have asked a single question: How much money are banks injecting into the spending flow by expanding the supply of credit? The answer to that question approximates how much fresh purchasing power banks are creating from thin air, and that’s what we’d really like to know.”

IT: “Not only that, but in their books, papers and interviews, Monetarists such as Friedman admitted they never figured out how money affects the economy. They were candid (to their credit) about not truly understanding the so-called transmission mechanism. Essentially, they jumped from correlation to causation and then wondered aloud why they made that leap, all the while challenging each other to craft a proven theory that never materialized. So it makes perfect sense that a poor understanding of banking, as in AC’s diagram, would lead them astray.”

DT: “And the real irony is that the measures used in A Monetary History have actually retained their correlations to GDP. Like I said, those measures tell us mostly about bank balance sheets and bank lending, so it’s not surprising that they continue to correlate with the economy. If the Monetarists hadn’t pulled a bait and switch from data in A Monetary History to their Ms, they might not have spent the 1980s and 1990s with the proverbial egg on their faces.”

UM: “Um. Geez, look at the time. I’m sure I had something I need to do—I’d better be going.”

Uncomfortable Truths

BBM jumps up and blocks the path to the door. He politely asks UM for another five minutes—to give the devil’s advocate view, or at least to offer some reaction to DT’s and IT’s comments. UM looks unhappy but sits down and agrees to share his thoughts.

UM: “Okay, I’m the character who can’t tell a lie, so here’s the deal. You might think of macro as an industry dominated by a few massive companies as in, say, aerospace. But in macro the big companies have an extra advantage—they don’t need to turn a profit. They operate within a self-governed bureaucracy, not a competitive market, and that means they can maintain their dominance by merely enforcing allegiance to a few core tenets. If you happen to work for—

BBM (interrupting): “Hang on a second UM, let me play that back and make sure I’ve got it. These macro ‘companies’ get away with defective products because they govern themselves. That’s human nature—poor oversight, poor results. And the core tenets are bad ideas that never die—they live on because the companies’ founders and executives built their careers and reputations on them. Long ago, the core tenets may have been subject to debate, but they quickly became company rules that no one dares question, even when they prove a lousy match for the real world. Is that what you’re saying?”

UM (frowning): “I wouldn’t word it exactly like that, but yes, you’re basically right.”

BBM: “Can you give an example?”

UM: “So if you work at Keynesianism, Inc., you have to accept that your equilibrium modeling factory churns out all major products. Your mantra and advertising slogan is ‘Anything else is just pictures and talk.’ In fact, Keynesians share that slogan with New Classicals and Co., another industry giant. Keynesians and New Classicals insist that the only acceptable way to do macro is with systems of equations that yield equilibrium solutions (the outputs of their respective modeling factories), even though they’ve been at it for eighty years now and have never designed a system that works.”

DT (preachy again): “And they never will. The economy isn’t simple and static enough—it’s complicated as hell and always changing. You can’t mimic its behavior with a few equations or even lots of equations—it’ll change again before you can say ‘pseudoscience.’”

IT: Huh, so if Tom’s right we can look forward to another eighty years of cruddy models. But where do you fit into this, UM? You’re an old-style Monetarist, right?”

UM: “Well, my company insists all products have to be constructed from four materials—M, V, P and Q. And our only supplier for M, by the way, is the central bank, with commercial banks being relatively insignificant as at the other major firms. Those are the two most important of our core tenets.

BBM: So you’re ignoring reality.

UM: I am, and I’m sure you can understand why this discussion makes me uncomfortable—I need to keep up the façade if I’m to maintain my nice position at Monetarism, LLC. Now if you’ll excuse me, I’d like to catch up on a few blog posts by my mentors at the MC. I’ll go read them now, and then I’ll troll the nonbelievers in the comment threads and feel like myself again.”

Various: “Wait, did that just happen?” “I’ve never before heard a mainstream economist come clean like that.” “Thank you for your honesty.”

UM (speaking faintly and to no one in particular as he exits the room): “MV=PQ… MV=PQ… MV=PQ…”

Summary and Part 2 Preview

Although we’ve left little doubt about where we stand in relation to the five characters above, we imagine readers having a variety of reactions. In your own case (not the character we conjured but the real you), maybe we’re singing to the choir, maybe you’re a mainstream economist and would like us to stop writing these articles, or maybe you’re on fence. Wherever you stand, we encourage you to consider the evidence that supports our way of thinking, which you can find in a few places.

In “Learning from the 1980s,” we shared statistics showing that the money measures used in A Monetary History have retained their correlations to GDP, whereas other measures such as M2 have not. In “An Inflation Indicator to Watch,” we used the circular-flow approach to develop an inflation indicator with an excellent historical record. And in the second part of this article, we’ll provide possibly the most useful evidence—we’ll add to the analysis included in our book that supports a shin bone to the thigh bone–close connection between bank credit and the business cycle.

If you’re willing to entertain that bank credit might be more revealing than mainstream commentators give it credit for—macro theory getting it badly wrong and all—you might like to pay attention to the indicator we’ll discuss in Part 2.

F.F. Wiley

F.F. Wiley is a professional name for an experienced asset manager whose work has been included in the CFA program and featured in academic journals and other industry publications. He has advised and managed money for large institutions, sovereigns, wealthy individuals and financial advisors.

© 2018 Copyright F.F. Wiley - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.