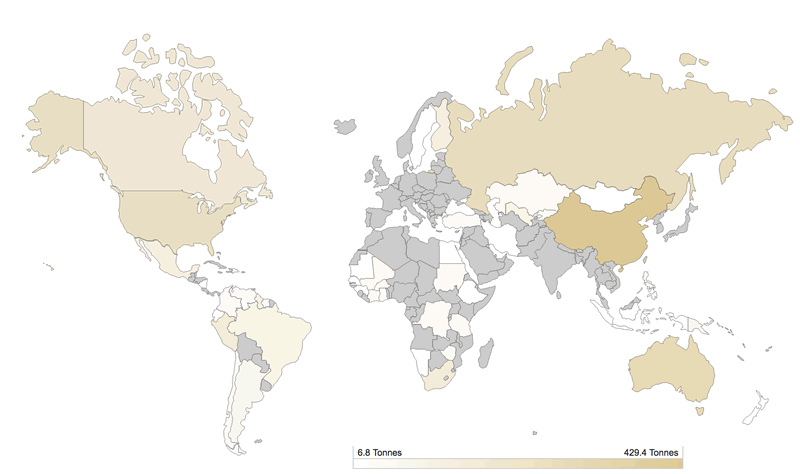

Gold Mine Production by Country

Commodities / Gold & Silver 2019 Jan 10, 2019 - 03:34 PM GMT

Gold mine production by country Divergent paths among the major global producers tell an important tale

Sources: MetalsFocus and the World Gold Council with permission.

|

||||||||||||||||||||||||||||||||||||||||

When you take in the table to the left, it inspires little beyond a shrug until you consider the policies toward gold of the countries involved. China, for example, is the world’s top gold producer, but its production is essentially sequestered, i.e., it stays in the country and winds up at the central bank as part of its monetary reserves. Russia, the world's third largest producer, also channels its production into central bank reserves. Thus, 23% (700+ tonnes) of the world’s gold production in 2017 did not see the light of day on international markets. Of the top-ten producers that still make their production available to the rest of the world, production is level for two – the United States and Australia. Of the three countries experiencing production growth – Canada, Russia and China – only one, Canada, makes its production available in international markets.

In short, the world is a different place now than it was prior to the 2008 financial crisis in terms of gold production. Should physical demand soar once again as did in the 2009-2013 period, we could get the same price response we did then. Even as it is, substantially less metal is reaching the marketplace at a time when central banks have become net buyers of the metal and investor demand, though presently in a lull, is generally on the rise.

The trends now favor "strong-handed" long-term gold investors holding for asset preservation purposes and capable of weathering the market's ups and downs. As for the official sector, the trend toward building gold reserves is likely to continue. More and more emerging countries are likely to see diversification as in their best interest while established states are likely to hold close the gold reserves they already own.

Wild market swings will give 'seasick investors' opportunity to jump ship

Gold is enjoying a run of positive forecasts of late and acquisition recommendations from various financiers. BlackRock, one of the world’s largest hedge funds, came out in gold’s favor at the start of the year. “’We’re constructive on gold,” portfolio manager Russ Koesterich told Bloomberg on Friday. “We think it’s going to be a valuable portfolio hedge. We’re multi-asset investors: we think about its effect on the entire portfolio, and what we see value in right now is gold’s value as a diversifier.”

Metals Focus, the London-based market analyst, reflected the prevailing opinion on gold as we start the year. “For much of 2018," said the firm, "investors tended to focus on other, higher-yielding asset classes [than gold],but we do expect this position to gradually change, especially during the latter part of 2019…[as] a slowdown in the US economy will encourage the Fed to adopt a far more dovish stance towards its interest rate policy." Metals Focus went on to say that "a bull market in gold [will] emerge from late 2019 onwards," and that uptrend will then "remain in place for two to three years.”

One of Europe’s biggest banks, the Netherlands’ ABN-Amro, weighs in on gold for 2019 with a ringing endorsement for the future. It sees gold at $1400 by year-end resulting from a confluence of factors covered briefly at the link above.“ We are of the view that the US dollar and US Treasury yields have peaked," says Georgette Boele, precious metals and FOREX strategist at the bank. "We also expect that US economic growth will peak this quarter. During the next two years, we expect lower US economic growth and lower 2y and 10y US Treasury yields. We expect the Fed to hike in December 2018 and one more time in 2019, some time during the first half. Going forward, the 2y US Treasury yields will probably rise in tandem with inflation expectations. So real yields will likely not rise. All these factors support our view that the US dollar has peaked and will weaken in 2019 and 2020. Therefore, we expect gold prices to rally in 2019.”

Gold finished 2018 down 1.6%, but ended the year on an optimistic note – up 2.1% for the month of December. The mostly sideways performance for the year aside, gold has been a steady performer since the turn of the 21st century – registering gains in fourteen of the first eighteen years.

As we begin the new year, the word "change" superimposes itself over our New Year thinking – change that likely will present challenges and test our skills in the year ahead. Gillian Tett, the Financial Times columnist, recently made an attempt to explain the wild swings in financial markets. In doing so, she passes along an interesting observation from Seth Klarman, founder of the Blaupost hedge fund.

“In 2008,” he says, “we had massive disguised [debt] leverage. Now we have less financial leverage, but there is psychological leverage.” He goes on to warn about “algorithmic leverage” and “computer herding” – problems we have written about on these pages for years.

Ms Tett, who has written with distinction about the financial markets, ends with the observation that the propensity toward wild swings rather than a sudden, full-out crash gives “seasick investors opportunity to jump ship.” That is a course of action worth pondering as we head into the start of what could be another eventful year. Jumping ship, we will point out, is one thing, establishing a solid portfolio hedge is another. The first without the second may turn out to be an empty exercise.

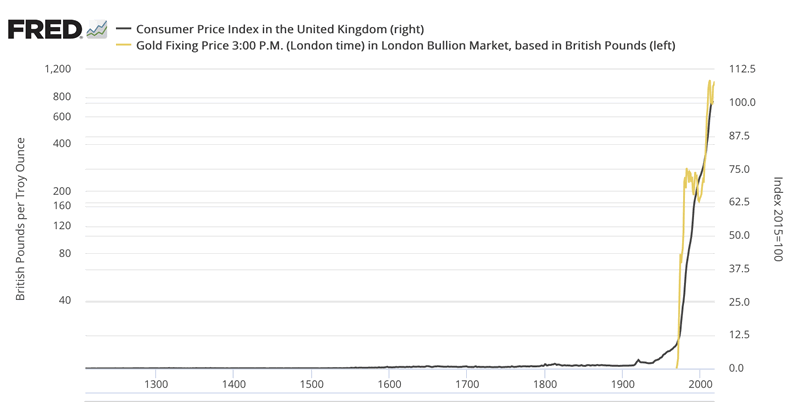

One for the history buffs: 730 years of a strong British pound ends in 1931 with gold standard exit

The St. Louis Federal Reserve recently released this interesting chart on consumer prices from 1209 to present. We added the price of gold to the chart to show the direct relationship between declining purchasing power in the British pound and the sterling price of gold after 1931, the year Britain departed the gold standard. Prior to 1931, there was an occasional minor bump higher in the price of gold, but for the most part it followed along the same flat line as consumer prices. It was only after Britain separated the pound from gold in 1931 that the price began to move radically higher in terms of the currency. It gained significant momentum after 1971 when the Bretton Woods agreement was abolished. Currencies and gold were then allowed to move freely in international markets. Though interesting from an historical perspective, the real lesson in this chart is that when a nation-state goes from gold-backed to fiat money, gold coins and bullion become a logical and worthwhile alternative for citizen-investors – even after 730 years of relative price stability.

Sources: Bank of England, ICE Benchmark Administration Limited, St. Louis Federal Reserve [FRED]

The naughty boy who blurts out unpleasant truths

"In the first place, the ‘classic’ writers, without neglecting other cases, reasoned primarily in terms of an unfettered international gold standard. There were several reasons for this but one of them merits our attention in particular. An unfettered international gold standard will keep (normally) foreign-exchange rates within specie points and impose an ‘automatic’ link between national price levels and interest rates. The modern mind dislikes this automatism, as much for political as for economic reasons: it dislikes the fetters this automatism clasps on government management of the economic process – dislikes gold, the naughty boy who blurts out unpleasant truths. But most of the economists of the period under survey liked it for precisely the same reasons. Though they compromised in practice as in theory and though they admitted central-bank management, the automatism – a phrase beloved by Lord Overstone [Samuel Jones Loyd, 1st Baron Overstone] – was for them, who are neither nationalists nor etatistes, a moral as well as an economic ideal.”

–– Joseph Schumpeter, History of Economic Analysis (1954) Published posthumously

Editor's note: To Dr. Schumpeter’s well-considered discourse on the practical merits of the gold standard, I will add a simple thought of my own: Absent the gold standard, the prudent investor who stores gold benefits in concert with the blurting out those unpleasant truths.

If you have an interest in the kind of analysis you are now reading, you might appreciate our LIVE DAILY NEWSLETTER – news, opinion and analysis as it happens. Always timely and posted for gold and silver owners or for those thinking about owning it.

The world's biggest hedge fund is getting whacked

“The SNB (Swiss National Bank)," writes Dollar Collapse's John Rubino, "loaded up on Big Tech like Apple, Amazon and Microsoft, and rode them to massive profits, which enriched both the Swiss people and the SNB’s stockholders (in another departure, it’s a publicly traded company as well as a central bank). But live by the sword, die by the sword. Turning your central bank into the world’s biggest hedge fund means outsized profits in good times, but potentially serious losses if those aggressive bets go wrong.” There was a time when gold was the centerpiece of the Swiss international banking enterprise. It seems, as Rubino points out, the SNB has departed from its original impeccable standards to mixed results.

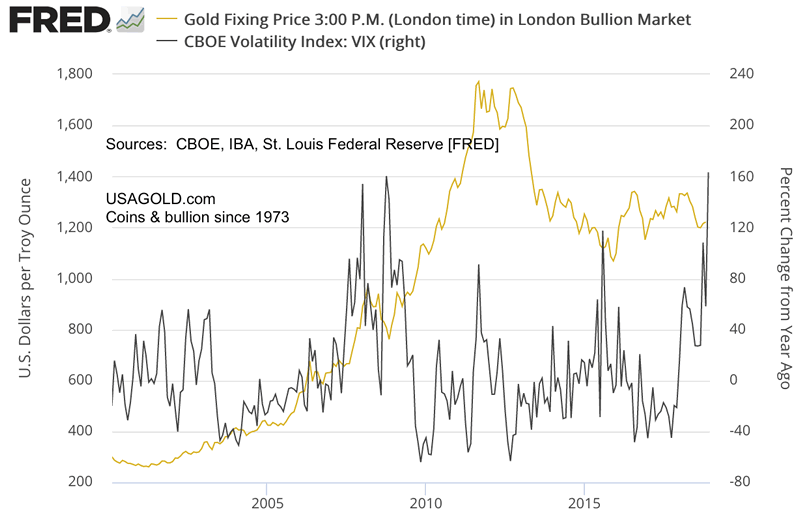

Will high volatility lead the gold market higher as it has in the past?

High volatility in the past has preceded the upward movement in the gold price. In a recent article under the headline “Wild days return to stock market as VIX surges like never before,” Bloomberg points out that volatility is now running at levels not seen since the 2008-2009 breakdown and, in fact, “the biggest annual surge on record.” As you can see in the chart below, there was a lag in gold’s response to the early phases of the 2008-2009 financial crisis. Its move upward came once investors realized the full extent of the crisis. From there gold pushed to its all-time highs.

Did we learn anything from the last crisis?

“At this point, the prevailing view holds that QE ‘worked,’" writes Credit Bubble Bulletin's Doug Noland. "Moreover, central banks are seen ready and willing to call upon 'money printing' operations as need. The great virtue of this policy course, many believe, is that there is essentially no limit to the scope and duration of ‘QE infinity.’ The FT quoted Mario Draghi: ‘[QE] is permanent and may be usable in contingencies that the governing council will assess in its independence.’ Melvyn Krauss, from the Hoover Institution, captured conventional thinking: ‘No one willingly walks into a room from which there is no exit. Because QE proved temporary, because it worked and because it has ended, it is likely to be used again.’"

When we read of the credit bubble inflated in the form of collateralized loan obligations (CLOs), as explicitly identified recently by former Fed chair Janet Yellen, one wonders if we learned anything at all from the credit crisis of 2008 and its aftermath. We subsequently learned that Japanese banks were at risk for over $1 trillion in sliced, diced and reconstituted CLOs.

Noland’s concerns are well-considered. In fact, as the highly respected hedge fund manager Henry Druckenmiller recently pointed out, “we’ve tripled doubled down on what caused that crisis. And we tripled down on it globally.” CLOs in the contemporary context are today what mortgage-backed securities were to financial markets in 2007. And to a great degree, the general public is not even aware such a thing exists. . . . . . Noland’s remarks in full are highly recommended.

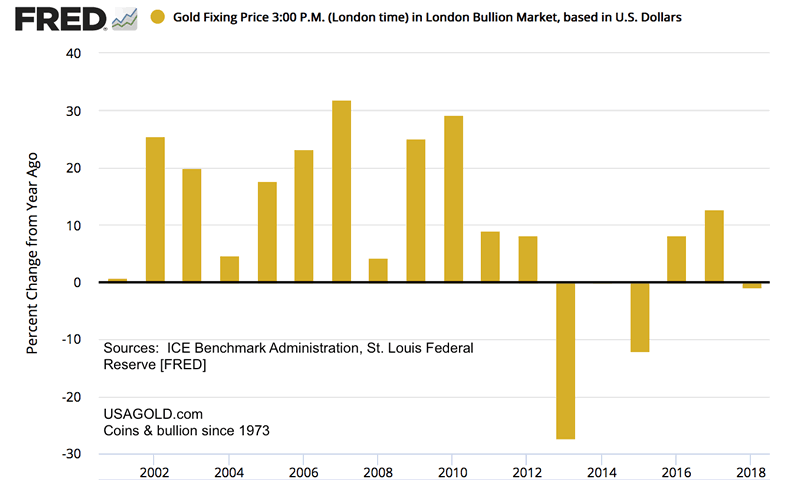

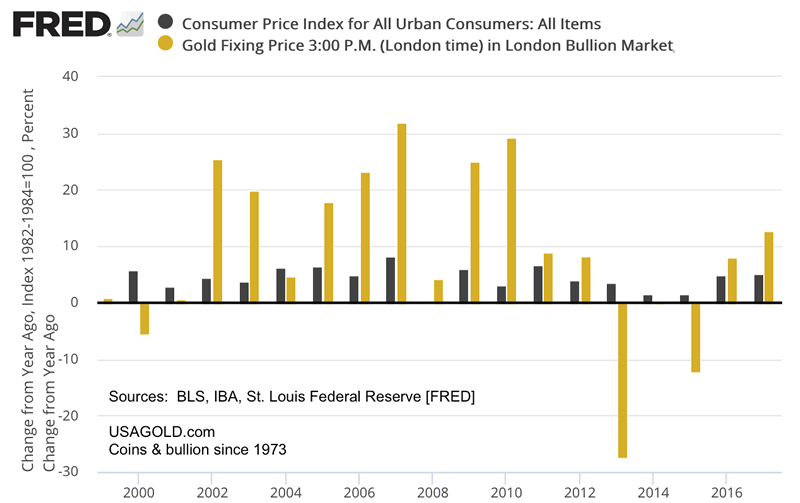

Gold's provided a real rate of return in twelve of the last eighteen years

Since the turn of the new century, gold consistently provided a real rate of return on investment when measured against inflation. In fact, it provided a real rate of return in twelve of the eighteen years represented on the chart. The period was one of subdued inflation. Gold’s performance, as a result, took many analysts and professional money managers by surprise and altered the perception among money managers that the precious metal is solely an inflation hedge.

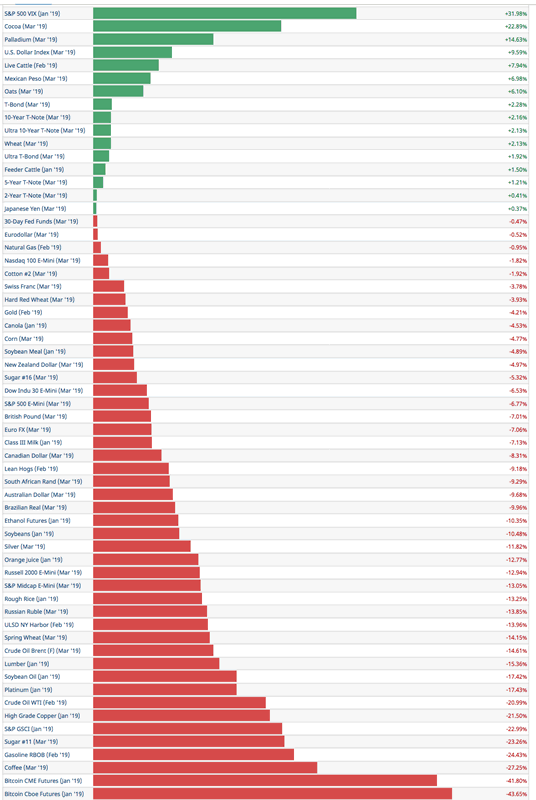

2018 ends in sea of red

Amidst a sea of red for 2018, stock market volatility comes out the clear winner in what many will see as appropriate for a year that will be remembered as one that most would like to forget. Bitcoin came out at the bottom of the list – down 43.65%. Gold, in a victory of sorts, finished down only 4.21% on the year. Silver by contrast was down 11.82% and the Dow Jones Industrial Average was down 6.53%.

Notable Quotable

“Problems are likely to continue in emerging markets, compounded by rising interest rates and the US Fed’s monetary policy which has drained global dollar liquidity. We have already seen the impact on the Turkish and Argentinian currencies. We remain concerned about geo-political problems including Brexit, North Korea and the Middle East, at a time when populism is spreading globally. The resolution of these problems in this unpredictable era will surely be difficult. In 9/11 and in the 2008 financial crisis, the powers of the world worked together with a common approach. Co-operation today is proving much more difficult. This puts at risk the post-war economic and security order. In the circumstances our policy is to maintain our limited exposure to quoted equities and to enter into new commitments with great caution.” – Lord Jacob Rothschild, RIT Capital Partners, Half-Yearly Financial Report, June 30, 2018

“At this stage of an ageing economic cycle, investors have good reason for concern as they try to work out whether the rout in equity and credit markets represents a final correction in this cycle or the start of lengthy decline. We have not begun a new year in such a glum mood since the start of 2009 and before that, 1999.” – Michael Mackenzie, Financial Times

“As the unwind continues, Financial Assets inflated by the free-money effects of QE are still finding new equilibrium valuations. Markets will remain volatile. Tech change and supply fundamentals will continue to shock us – look at oil prices for an example; turning a good year for oil and energy into a question mark. Or look at how iPhone sales in India have fallen off a cliff as people buy cheaper phones that do the same – commoditisation! The thing that scares me most is liquidity – the lack of it.” – Bill Blain, Blain’s Morning Porridge

“Alan Greenspan says the party’s over on Wall Street. The former Federal Reserve chairman who famously warned more than two decades ago about ‘irrational exuberance’ in the stock market doesn’t see equity prices going any higher than they are now. ‘It would be very surprising to see it sort of stabilize here, and then take off,’ Greenspan said in an interview with CNN anchor Julia Chatterley. He added that markets could still go up further — but warned investors that the correction would be painful: ‘At the end of that run, run for cover.'” – Donna Borak, CNBC

Editor's note: Greenspan over the years has consistently advocated gold ownership as a means to hedging the next financial crisis.

“Europe has brought us a depression worse than 1929. It has led to entire peoples being broken and humiliated, like the Greeks, all for the sake of preserving the infernal instrument of the euro. This whole disaster has been adorned by a chain of lies, shouted ever louder because they are afraid that the colossal damage they have done will be discovered.” – Claudio Borghi, Catholic University of Milan

“Nobody knows what would happen if Britain’s LCH or Germany’s Eurex Clearing came under stress. They have thin layers of capital compared to banks. Before the 2008 crisis most derivatives were cleared by trading parties in direct dealings. The G20 shift has lifted the share of CCPs [central counterparties] for interest rate derivatives from 20 to 60 percent. The effect is to concentrate risk. The BIS warns that the system may encourage a rush for the exit in events of extreme stress. The International Monetary Fund has also flagged the dangers. It warned this year that CCPs ‘increase the risk of a failure of the infrastructure itself’ and could lead to a ‘catastrophe’ if all the layers of defense were overrun by a big default. It would be like the failure of the Maginot Line.” – Ambrose Evans-Pritchard, BIS warns of seizure at heart of financial clearing system

“For we have reached a critical point. In a sense, it is true that the mists are lifting. We can, at least, see clearly the gulf to which our present path is leading. Few of us doubt that we must, without much more delay, find an effective means to raise world prices; or we must expect the progressive breakdown of the existing structure of contract and instruments of indebtedness, accompanied by the utter discredit of orthodox leadership in finance and government, with what outcome we cannot predict.” – John Maynard Keynes, The Means to Prosperity (1933)

“I’m fond of saying how crazy things get near the end of Bubbles. Convinced this is History’s Greatest Bubble, I’ve been anticipating a pretty astonishing variety of ‘crazy.’ Watching this all unfold with increasing trepidation, I sense an important line has been crossed. It’s time to retire ‘crazy’ – find a replacement that conjures up something more foreboding – more disturbing. And markets, well, they’re seemingly fine with it all; at times almost giddy. And that’s the fundamental problem: Dysfunctional markets continue to promote incredibly risky policy behavior – the polar (bear) opposite of imposing discipline.” – Doug Noland, Credit Bubble Bulletin

“Gold is scarce. It’s independent. It’s not anybody’s obligation. It’s not anybody’s liability. It’s not drawn on anybody. It doesn’t require anybody’s imprimatur to say whether it’s good, bad, or indifferent, or to refuse to pay. It is what it is, and it’s in your hand.” – Simon Mikhailovich, Tocqueville Funds (with thanks to Ron Stoeferle and Mark Valek at Incrementum AG)

By Michael J. Kosares

Michael J. Kosares , founder and president

USAGOLD - Centennial Precious Metals, Denver

Michael J. Kosares is the founder of USAGOLD and the author of "The ABCs of Gold Investing - How To Protect and Build Your Wealth With Gold." He has over forty years experience in the physical gold business. He is also the editor of Review & Outlook, the firm's newsletter which is offered free of charge and specializes in issues and opinion of importance to owners of gold coins and bullion. If you would like to register for an e-mail alert when the next issue is published, please visit this link.

Disclaimer: Opinions expressed in commentary e do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. Centennial Precious Metals, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD - Centennial Precious Metals does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.