How Central Bank Gold Buying is Undermining the US Dollar

Currencies / US Dollar Apr 17, 2019 - 08:16 AM GMTBy: Richard_Mills

Ahead of the Herd has been digging into why central banks are buying a lot of gold recently . What we’ve found is eyebrow-raising, to say the least. It may be the best reason you’ve ever read for wanting to buy gold.

Ahead of the Herd has been digging into why central banks are buying a lot of gold recently . What we’ve found is eyebrow-raising, to say the least. It may be the best reason you’ve ever read for wanting to buy gold.

Take this headline from the Northern Miner: “Editorial: Central banks are major gold buyers in 2019”. Citing statistics from the World Gold Council, the Northern Miner reports that central banks netted 51 tonnes in gold purchases, the most since October 2018, when they increased gold held in central bank vaults by 105 tonnes. Switching to ounces, the Miner states that gold holdings grew by a startling 2.9 million ounces in January and February 2019, versus 1.9 Moz during the same period of 2018. This is the highest level of gold buying by central banks since the first two months of 2008 - during the financial crisis.

Central banks backed up the truck for gold in 2018, buying 651.5 tonnes versus 375 tonnes in 2017. That’s the largest net purchase of gold since 1967.

The Miner suggests that anti-US sentiment is at the root of all this central bank gold buying. “And yes, there is a distinct geopolitical element to it all, as these central bank buyers are predominantly from countries that stand in direct economic or political opposition to the U.S., and so are keen to move away from the U.S. dollar as a foreign reserve currency.”

Case in point: the top two purchasers were Russia and Turkey.

Russia is actively seeking to reduce its dependence on the greenback in an effort to skirt US sanctions for, among other things, interfering in the US presidential election and invading Crimea. The Kremlin stopped buying foreign currency in September 2018 to prevent the ruble from crashing due to sanctions. Instead the Russian Central Bank turned to gold, buying a record 274.3 tonnes in 2018, according to BNE Intellinews, while selling a whack of US Treasuries - bringing its share of the US dollar as a foreign reserve down from 43.7% to 20%. Between March and May of last year, Russia sold off 84% of its US debt holdings, leaving just $14.9 billion in its US reserve account.

Turkey needs gold to protect itself against a sluggish economy (over the past year the lira has lost 30% of its value making it difficult for consumers to buy imported goods). Gold-buying is one way to support the lira versus purchasing US Treasuries, which is difficult to do with the relative strength of the US dollar. A couple of years ago Turkey’s President Erdogan called on citizens to buy gold, and they have: “Those who keep dollar or Euro currency under their mattresses should come and turn them into Liras or gold.”

Goldcore summarizes the situation in Turkey viz a viz gold:

The push for support for gold is two-fold, first it is an attempt to boost trust in the central banking system which is in increasingly dire straights, the second is to support the underlying currency which is central to the ‘axis of gold’ (h/t Jim Rickards) that is Russia, China, Turkey and Iran. Both of these things push back against US dollar hegemony.

And there we have it. The reason for central banks’ recent gold accumulations has little to do with safe havens and a lot to do with chipping away at the US dollar’s role as the reserve currency. This article will explain what is happening.

Rise of the petrodollar

In July 1944, as Allied troops were racing across Normandy to liberate Paris, delegates from 44 nations met at Bretton Woods, New Hampshire and agreed to “peg” their currencies to the US dollar, the only currency strong enough to meet the rising demands for international currency transactions.

What made the dollar so attractive to use as an international currency, the world’s reserve currency, was each US dollar was based on 1/35th of an ounce of gold (35.20 US dollars an ounce), and the gold was to be held in the US.

The US began to send larger and larger amounts of dollars overseas to fund their increasing trade deficits.

The glut of US dollars held abroad began to threaten US gold reserves – remember US dollars were redeemable for gold – and worldwide demand for gold was soaring. By the late 1950’s US gold reserves had began to dwindle rapidly.

With the Gulf of Tonkin incident in late 1964 and the acceleration of the Vietnam war in 1965, US Military spending exploded. This was compounded by President Lyndon B. Johnson's Great Society project spending and not raising taxes.

Since Johnson refused to raise taxes to pay for the social welfare reforms undertaken earlier and the war in Vietnam, the US was now running massive balance of payment deficits with the world.

In October of 1960 panic buying caused gold’s price to rise to over US$40 per oz. A night-time emergency call was made by the US Federal Reserve. The Bank of England was to immediately flood the gold market with enough supply to reduce and stabilize the price of gold. The US had just made it abundantly clear that stopping the drain of its gold reserves, and the depreciation of its currency against gold, was a huge priority.

The US, the Bank of England and the central banks of West Germany, France, Switzerland, Italy, Belgium, the Netherlands, and Luxembourg then set up a gold sales consortium to prevent the market price of gold rising above US$35.20 per oz. This consortium was known as the London Gold Pool. This meant that the dollar would now be backed not only by the gold in Fort Knox but all the other pool members’ gold as well.

Despite the Cuban Missile Crisis and escalating tensions between Moscow and the US, gold prices remained fairly stable; the London Gold Pool was a success.

With the Gulf of Tonkin incident in late 1964 and the acceleration of the Vietnam war in 1965, US Military spending exploded. Since US President Johnson refused to raise taxes to pay social welfare reforms and the war in Vietnam, the US was now running massive balance of payments deficits with the world.

Gold demand skyrocketed.

Several planeloads of gold were emergency airlifted from the US to London. Gold demand continued to escalate with the London Gold Pool selling 175 tons one day and the very next day selling an additional 225 tons. This broke the back of the London Gold Pool. Members were tired of draining their countries’ gold reserves to pay for the US’s Vietnam War and social reform policies.

An official “two-tiered” price for gold was announced to the world - the official price of US$35.20 would remain for central banks dealings, the free market could find its own price.

In February 1970 the closing gold price on the London market averaged US$34.99. On August 15, 1971, US President Nixon ended the convertibility of the dollar into gold. With gold finally demonetized, the Fed and the world’s central banks were now free from having to defend their gold reserves and a fixed dollar price of gold. The era of Bretton Woods was over.

For more economic history, read our Demise of London Gold Pool ends Vietnam War

Recognizing that the US, and the rest of the world was going to use a lot of oil, and that Saudi Arabia wanted to sell the world’s largest economy (by far the US) that oil, Nixon and Saudi Arabia came to an agreement in 1973 whereby Saudi oil could only be purchased in US dollars. This caused an immediate and strong global demand for the buck.

By 1975 all OPEC members had agreed to sell their oil only in US dollars - thus ushering in the period of US “petrodollar” dominance that continues to this day.

Exorbitant privilege

In the 1960s French politician Valéry d’Estaing complained that the United States and its exporters enjoyed an “exorbitant privilege” due to the dollar’s status as the world’s reserve currency. He had a point. Because the dollar was, and is, the world’s currency, the US can borrow more cheaply than it could otherwise (lower interest rates), US banks and companies can conveniently do cross-border business using their own currency, and when there is geopolitical tension in the world, central banks and investors buy US Treasuries, keeping the dollar high and the United States insulated from the conflict. A government that borrows in a foreign currency can go bankrupt; not so when it borrows from abroad in its own currency.

The dollar is the most important unit of account for international trade, the main medium of exchange for settling international transactions, and the store of value for central banks. The Federal Reserve is the lender of last resort, as in the 2008-09 financial crisis, and is the most common currency for overseas borrowing by governments and businesses.

Wall Street generates significant income from selling banking services in USD to the rest of the world, and the US manages the world’s most important settlement systems, allowing it to monitor and limit funds used for illegal activities.

US$ losing its privilege

Barry Eichengreen, author of “Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System,” names three unique attributes to the dollar that no other currency has: size, stability and liquidity.

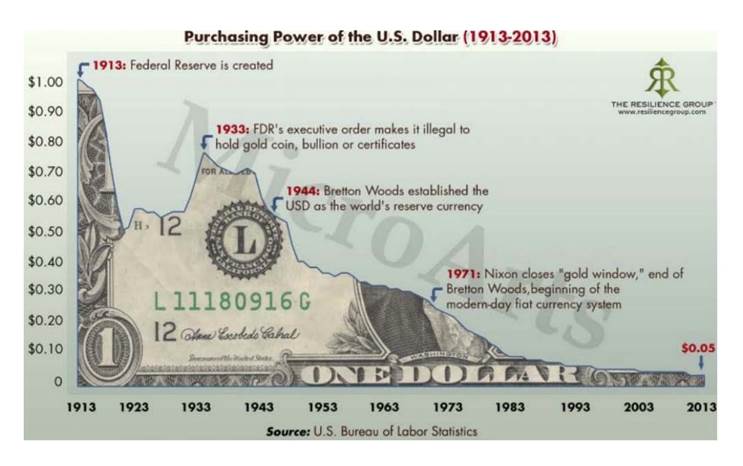

While the attendees at the Bretton Woods conference in 1944 envisioned the USD enjoying these advantages in perpetuity, the reality is the greenback has been in decline for some time. Since the Federal Reserve was created in 1913, the dollar has lost 95% of its value. (see graph below). Over 100 years ago a buck was worth a buck; in 2013 it was valued at 5 cents – its worth eroded by inflation.

Then there’s the US debt, currently sitting at over $22 trillion and growing daily.

Jeffrey Sachs, writing for Project Syndicate, argues “the dollar punches far above America’s weight in the world economy,” producing just 22% of world output, but accounting for 50% or more of cross-border invoicing, reserves, settlements, liquidity and funding. Due to US fiscal and monetary mismanagement, as described above, the Bretton Woods financial system set up in 1944 collapsed. The breakdown of a gold-backed dollar led to high inflation in the US and Europe, then a fall in inflation in the early 1980s.

Sachs argues the turmoil of the dollar was a key factor in motivating Europe to embark on monetary union, resulting in the euro’s launch in 1999. Same with America’s mishandling of the 1997 Asian debt crisis which led to China wanting to internationalize the renminbi, or Chinese yuan.

The 2008-09 financial crisis which started in the US through the sub-prime mortgage debacle, was another flag to the rest of the world signaling a move away from the dollar toward other currencies, notes Sachs. “America’s monetary stewardship has stumbled badly over the years, and Trump’s misrule could hasten the end of the dollar’s predominance.”

The quantitative easing program that saw the Fed’s assets skyrocket from $900 billion to $4.5 trillion between 2019 and 2015 (through the buying up of Treasuries, paid for by printing money), made it inexpensive for the US government to continue to borrow and spend - with rates close to zero.

However, QE also showed other countries that no longer was the United States following a sound fiscal policy; all it was doing was printing money. Countries started to diversify their foreign exchange reserves and reduce their dependence on the dollar. According to the IMF, USD foreign exchange reserves have dropped from 72% of the world’s forex in 2001 to 62% today. 7

Saudi Arabia’s ‘nuclear’ option

The price of crude oil and gasoline have surged since January, causing alarm within the Trump Administration. The commander-in-chief has been sending angry tweets directed at OPEC, blaming the oil cartel for high gas prices. Indeed, fuel prices have risen about 50 cents a gallon over the past 90 days, in step with increased crude prices, which on Wednesday closed at $63.58 a barrel (WTI) from $48. 452/barrel on Jan. 7.

It wasn't long ago that everyone was complaining about oil prices being too low!

In response, the House Judiciary Committee passed a bill allowing the United States to sue members of OPEC for manipulating the oil market. The so-called “NOPEC” bill has been proposed under past administrations, but no previous presidents have dared to threaten the US-Saudi relationship.

Trump in typical cavalier fashion is the first to do so. He thumbed his nose at the Arab world by recognizing Jerusalem as the capital of Israel and Israeli sovereignty over the Golan Heights.

The unconventional president has picked at the threads of the US-Saudi relationship, leading to its unraveling. As a presidential candidate, Trump called the Saudi regime the world’s biggest funder of terrorism.

To be fair, Saudi Arabia’s Crown Prince, Mohammed bin Salman (MBS), has shown a disturbing recklessness in foreign policy - from the bloody Yemen conflict, to the blockade of Qatar, the kidnapping of the Lebanese prime minister, and the near-collapse of the Gulf Cooperation Council.

The low point came when the US did not defend MBS amid widespread condemnation over what appeared to be a premeditated killing of a Saudi journalist, Jamal Khashoggi.

There is also concern over the construction of Saudi Arabia’s first nuclear reactor and whether its nuclear capability could be put to use making weapons. While the two reactors are meant for energy production, MBS said last year that the kingdom would develop nuclear arms if Iran did so.

Recently the US Congress passed a bill cutting off aid for the Saudi war in Yemen - exhausting any goodwill left between the two nations.

Back to the NOPEC bill, the move to expose OPEC members to US antitrust lawsuits put Saudi Arabia on the defensive. The oil-soaked nation is threatening to kill the petrodollar if the US moves forward on the legislation, by selling its oil in non-dollar currencies.

Oilprice.com reports the effects of OPEC members rejecting dollar dominance in oil sales would be extremely bad for the US economy. This is the so-called “nuclear” option:

The global oil market is almost entirely conducted in dollars, which provides the foundation for dollar domination in the global financial system. Introducing new currencies in the oil trade could undercut demand for the dollar, diminish American influence over global finance, weaken American influence over sanctions, and thus, undercut its geopolitical reach. It’s hard to assess how serious Saudi Arabia is, but the implications of such a move are far-reaching and hard to overstate.

The willing beneficiaries of oil traded in other than US dollars, include China, Russia and the European Union, all of which have expressed frustration at the Trump Administration’s treatment of other countries, and called for a resetting of the dollar-based international system.

China and Russia have inked energy deals whereby trade is conducted in rubles and yuan; China has also started a yuan-denominated oil futures contract, based in Shanghai.

And perhaps most significantly, in a major snub to the US, Iran and the EU agreed to set up a new payments system to enable trade with Iran, in order to avoid US sanctions arising from the scrapping of the 2015 Iran nuclear deal. (Trump said in May 2018 that “any nation that helps Iran in its quest for nuclear weapons could be strongly sanctioned”). The “special purpose vehicle” is effectively the EU’s own SWIFT, the Society for Worldwide Interbank Financial Telecommunications used for transferring money between countries - which conducts transactions in USD.

Perfect storm for gold

Amid rising regional tensions that has Saudi Arabia, the world’s largest oil exporter, looking beyond its special relationship with the US, and wider geopolitical strains between the US, China and Russia (think about the US-China trade war, naval posturing in the South China Sea, Russia supporting outcast Venezuelan President Maduro in what has traditionally been the US’s backyard), we have more evidence to show that the vaunted USD is under threat.

Consideration of an alternative, loony-left economic theory that should have been dismissed outright by American lawmakers is actually being taken seriously, due to the untenable position the US finds itself in regarding its mounting pile of debt.

Modern Monetary Theory posits that rather than obsessing about how large the debt has grown (over $2 trillion) and the ongoing annual deficits that fuel debt, government should target certain spending programs that will cause minimal inflation.

Curb inflation and the debt can keep growing, with no consequences. This is because the US government can never run out of money. It just keeps printing money, because dollars are always in demand (with the dollar being the reserve currency, and commodities are traded in dollars).

Government is therefore given a free pass on spending, because the only thing that we have to worry about with the national debt is inflation.

Fiscal policy on steroids is, according to its proponents, to be the new engine of US growth and prosperity.

Even if MMT isn’t adopted, and it’s extremely unlikely that it would be, just the idea of the US dollar losing its role as the world’s reserve currency is alarming.

If it happened suddenly, a massive sell-off of US Treasuries would result, crashing the value of the dollar. It would make the financial crisis of 2008-09 look like a mere stock market correction.

Recall the frenzy of central bank gold buying described at the top. Countries holding large amounts of US Treasury bills must be concerned about the ability of the US to keep financing its debt. If OPEC kills the petrodollar, its value could halve overnight. And if the debt burden become so onerous that lawmakers decide to try MMT, the greenback would take a massive hit.

In light of these risks, is it any wonder central banks are bulking up on bullion?

Indeed, gold’s status as store of value, as money, the only currency available when yours is worthless, has come into play with respect to the drama that has been unfolding in Venezuela over the last couple of years.

Gold gives all of us something that fiat currencies (paper money), or any other financial innovation, cannot deliver. Gold is insurance, irreplaceable in its functions.

Wall Street turned its back on gold because it can’t produce growth “sprouts”, but international banking rules recently changed to accommodate the yellow metal.

Under the old Basel I and II rules, gold was rated a Tier 3 asset. Under Basel III Tier 3 has been abolished, making gold bullion a Tier 1 asset, as of March 29. Tier 1 capital is the measure of a bank's financial strength, from a regulator's point of view. Also, and this is important, under Basel III a bank’s Tier 1 assets have to rise from the current 4% of total assets to 6%.

Because gold is now a Tier 1 asset, banks can operate with far less capital than is normally required. Gold is the new backstop for debt, currencies and bank equity capital.

Central banks clearly see the value of holding gold over paper assets; after 2008, mortgage-backed securities (MBS) lost most of their value and they have also suffered massive value destruction by holding sovereign securities ie. Greece and Italys, that are today, also near worthless). Perhaps almost a doubling of gold bullion purchases in 2018 over 2017 indicates that central banks believe gold is a better Tier I asset than government debt and MBS? There is also that 2% increase in total assets to 6%, which now needs to be filled, likely by gold.

In another way though, central bank gold buying is undermining the dollar. It’s sending a signal to the US government, and the Federal Reserve, that the buck is no longer as important as it once was. It’s no longer risk-free, and the US is no longer considered to be the most powerful nation in the world, carrying the biggest stick and the fattest wallet.

What will be the future world currency? The yuan? Euro? A basket of currencies aka “special drawing rights” SDR set up through the IMF? Where will gold fit in a new currency arrangement?

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2019 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.