Investment Opportunities in Municipal Bonds?

Interest-Rates / US Bonds Oct 22, 2008 - 11:40 AM GMTBy: Richard_Shaw

The $2.66 trillion municipal bond market is embroiled in the overall credit market mess, creating an unusual complex of risks and opportunities.

The $2.66 trillion municipal bond market is embroiled in the overall credit market mess, creating an unusual complex of risks and opportunities.

The supply-demand forces in the municipal bond market have been unfavorable in the past year, causing prices to decline.

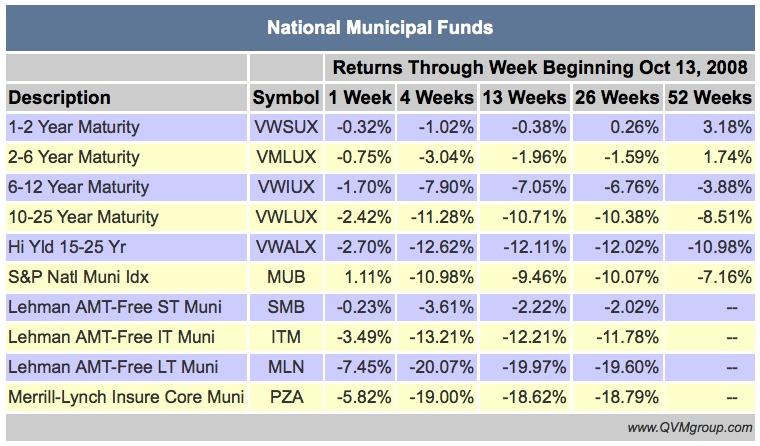

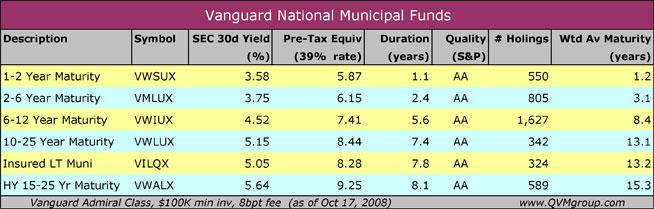

The mutual funds in this table are Vanguard Admiral class. The minimum investment is $100,000, but the expense ratio is only 8 basis points. Their Investor class shares carry a 15 basis point expense ratio. Either expense is lower than most alternatives.

Negative Forces on Muni Market:

Some of the adverse circumstances impacting muni prices and rates include:

- Credit downgrades for municipalities

- Near-bankruptcy of the muni bond insurers

- Unwinding of muni bond positions by hedge funds deleveraging

- Failure of the auction rate muni market

- Rise in long-term muni issuance as short-term rates became burdensome

- Rotation from muni to Treasury bonds in flight from risk of all sorts

The very short-term muni market is still high cost for issuers and not guaranteed the way the corporate commercial paper market is federally guaranteed.

Oct. 17 (Bloomberg) — The Federal Reserve said its backstop for the commercial-paper market isn't open to state and local governments who use the source of short-term financing.

Closed-End Muni funds:

There are many closed-end muni funds, mostly quite small, none as large at the 20 billion of the Vanguard Intermediate muni fund. The following is a table of the 20 largest muni CEFs by asset size.

(table from Yahoo Finance)

Muni CEFs can go to substantial discounts or premiums and most use some degree of leverage (perhaps 25% to 40%) which makes returns more volatile.

They may or may not be liquid.

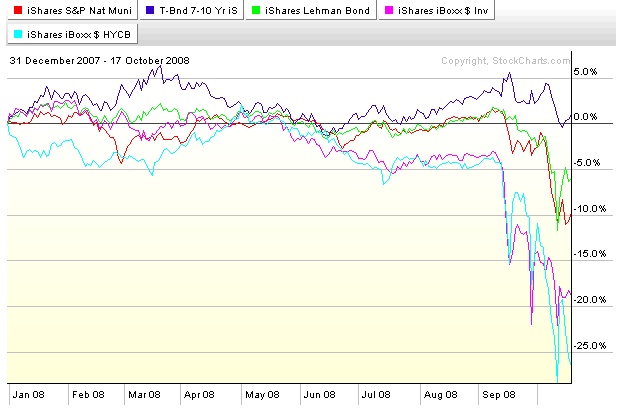

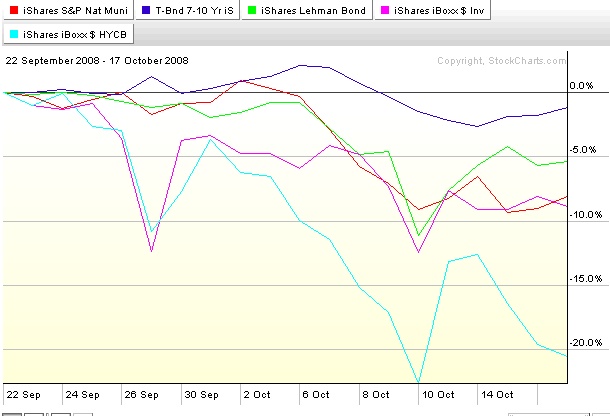

Muni's vs Treasuries, Total Bonds ex Muni's, Corporates & Hi-Yield:

The following two charts show how muni's (proxy MUB) have performed relative to intermediate (7-10 year) Treasuries (proxy IEF), the overall US bond market excluding muni's (proxy AGG), investment grade corporate bonds (proxy LQD) and junk bonds (proxy HYG).

YTD Performance

20-Day Performance

You can see from both charts that there was a big drop in performance for municipal and bonds generally during October. Muni bonds and investment grade corporates declined about equally (junk bonds got hammered). Aggregate bonds, which exclude muni's, have recovered more than muni's, because they are a mixture of government and corporate bonds.

Historic Tax-Free Yield:

According to Bloomberg, the yield on 20-year general obligation muni bonds rose to 6.01 percent this week — the highest since 2000. More dramatic than high rates is that muni bonds yield more than comparable maturity Treasuries. Bloomberg states that the current muni rates are a record 1.77 percentage points more than Treasuries. That compares to an average over twenty years during which muni's yielded 0.67 points less than Treasuries.

(Bloomberg, Oct 17) “This is viewed as a historic opportunity for the individual investor,” said Joe Darcy, who manages $5 billion in municipal bonds for Dreyfus Corp. in New York.

Federal & State Tax Reciprocal Agreement:

Note : we are not tax advisors, just investors coping with taxation issues — consult your personal tax advisor.

Under a reciprocity principle, states cannot tax interest on federal debt, and the federal government cannot tax interest on state debt (with exceptions). That is the foundation of tax-free muni income.

State specific muni interest is both state and federal tax-free for residents of that state (except for AMT exposure on private purpose bonds). National muni bond funds are federal tax-free on all of the AMT-free interest; and state tax-free for interest generated on bonds from the state of residence of the bond owner.

These are general principles to which there may exceptions or state variations of which we are not aware. For example, we are not certain how state taxes do or would work on state specific muni's in states where state income tax is a percentage of federal tax.

The important exception to the state-federal reciprocal tax arrangement over muni bonds relates to municipal bonds that fund private purpose projects. They are federal tax-free in the regular calculation, but are exposed to tax in the AMT (alternate minimum tax) calculation.

That exception to the state/federal reciprocal tax agreement could conceivably be the camel's nose under the tent to justify further tinkering by a tax seeking federal government.

Any increase in taxation of muni bonds would correspondingly decrease their return — prices would decline and rates would increase to compensate for additional taxation. Because of the burden that would place on towns, cities and states, we doubt the tax treatment will change.

Far Out, Unlikely Tax Scenario:

The muni tax rules probably won't change, but they could change in a low probability scenario. We have no particular idea how they might change, except to say that tax seeking legislators are clever and motivated.

Obama is likely to the next president, and the Congress is likely to be controlled by the Democrats. He and they have committed to raising taxes on the wealthiest 5% of households – the group most likely to be holders of municipal bonds.

The muni market is owned about 66% by institutions and about 34% by households (about $912 billion of muni bonds are owned by households).

The billions of interest on that $912 billion of bonds are currently mostly tax-free (mostly AMT-free). While we hope munis remain tax free, the tax benefit is realized predominantly by the wealthy who are the target of the contemplated wealth redistribution.

Federal taxes on muni interest may be eyed by tax legislators as a significant potential source of income, particularly if there is an observable shift away from taxable investment income to tax-free investment income.

Except for the fact that taxing muni bond income at the federal level would harm the economic interests of states and cities, we'd be skeptical about the future of tax-free interest of any kind.

Changing the tax status of muni's would be highly disruptive, making new taxes on muni interest highly unlikely, but not inconceivable. The current world credit meltdown was also extremely highly unlikely, but it happened.

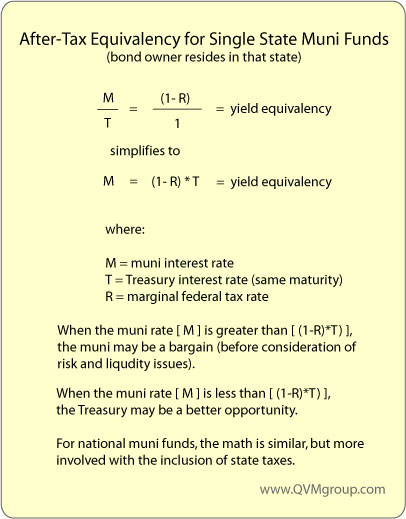

Yield Equivalency:

Relativity:

Are Treasury rates low, or are muni rates high? That is a key question.

Are muni rates higher than Treasuries because Treasury rates are low due to the flight to quality, or because investors perceive special risks in muni bonds themselves, or both? We think both.

- To the extent that Treasury rates are driven low by high demand, muni rates may be OK and capital gains potential would be low.

- To the extent that muni rates are driven high by their own internals, muni rates would be expected to fall over time and capital gains could be important.

Inflation or Deflation?

If inflation increases (perhaps due to excess Treasury issuance), muni rates may be too low — rates too low imply more price declines. Jim Rogers is in that camp:

(Bloomberg Oct 16) The risk is that yields rise as the U.S. increases debt sales to fund the bank rescue plan and pumps money into the economy, said investor Jim Rogers, chairman of Rogers Holdings …

“The U.S. government is taking on gigantic amounts of debt,” Rogers said in an interview in Singapore, where he lives. “They're printing gigantic amounts of money. Printing money has always led to more inflation. The last bubble in the world that I can find is long-term U.S. government bonds.”

Rogers said he is “shorting” 30-year debt, or betting prices will fall.

If deflation arises and prevails, bonds would do well until and unless the deflation weakened the ability municipalities to collect sufficient taxes to pay their obligations, or weakened the ability of revenue bonds to be supported by the funded projects. Elements in the Federal Reserve have deflation concerns:

(WSJ Oct 18) Federal Reserve officials view broad-based deflation as unlikely but possible. Federal Reserve Bank of San Francisco President Janet Yellen said in a speech this week that the plunge in oil prices along with slackening demand for labor and goods should “push inflation down to, and possibly even below, rates that I consider consistent with price stability.”

… The Japanese economy in the 1990s and the U.S. during the 1930s illustrate how deflation can choke a weak economy and spiral out of control.

Which direction you feel prices will go is critical to your bond holding decision.

Tax Driven Increase Driven Rotation to Muni Bonds:

If federal tax rates are to increase, it stands to reason that, in the absence of special risks, the demand for muni bonds should increase.

Current Attributes of Muni Funds:

The following chart of muni fund attributes is based on the Vanguard funds in the return table above.

The nominal yields for AA credit quality bonds range from 3.58% to 5.64% in this fund selection.

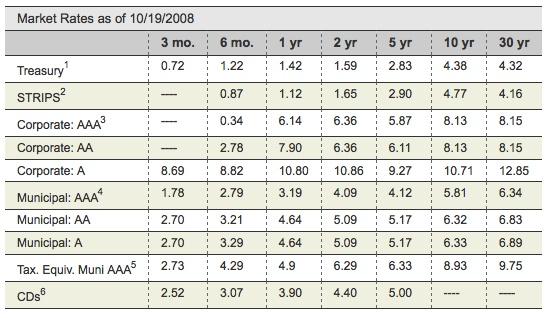

A comparison of current muni market rates with other key fixed income rates is made in this chart from Schwab:

Capital Gains:

Capital gains are not normally a large part of muni investing, but the inverted yield relationship portends the possibility of solid gains when the historical relationship is restored.

If the recent declines were reversed, muni's (and corporates) appear to be able to generate 8% to 9% one-time capital gains.

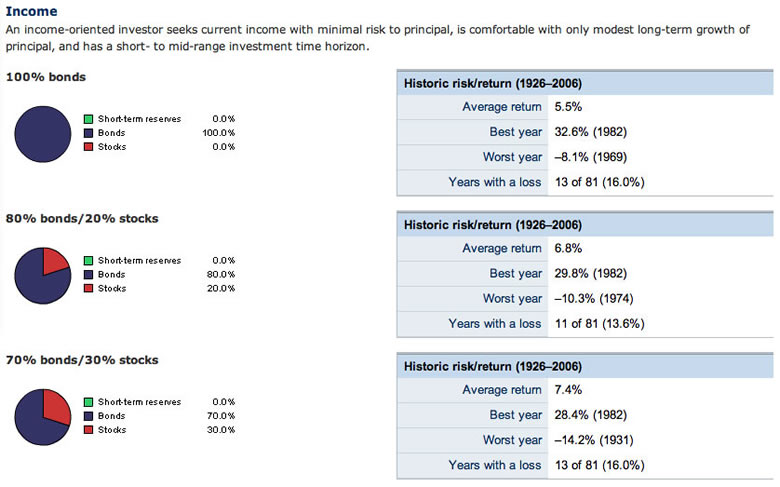

Risk and Return:

We expect the risk in muni bonds not exceed that of stocks, yet the yield attributes (before consideration of possible gains) are similar to a conservative taxable bond/US stocks portfolio.

That may create a reasonable risk diversification with minimum return sacrifice for the conservative income investor.

Here are some historical return and draw down charts from Vanguard for income oriented portfolios consisting of different proportions of the Lehman Aggregate Bond index and the S&P 500 index.

Securities Mentioned:

- Mutual Funds : VESUX, VMLUX, VMIUX, VWLUX, VWALX, VILQX

- ETFs : MUB SMB, ITM, MLN, PZA, IEF, AGG, LQD, HYG

- CEF s: NUV, NIO, MYI, EIM, VGM, PML, NPP, NPI, NQU, NMO, VKI, BFK, NMA, MYD, PMO, VKQ, MVF, MVI, NPM, NZF

Our Preference:

We favor the Vanguard funds over the muni ETFs for several reasons:

- lower expense ratios (very important with fixed income)

- daily liquidity at NAV (discount possible with ETFs)

- no Bid/Ask spread on purchase and sale (spread can be high on low volume ETFs)

- better spread of risk through greater number of holdings

- longer portfolio history

Conclusion:

We don't know if the markets in general are done going down. We think probably not, but we don't know. A lot is yet to transpire before and during January 2009 that could lead to surprises. On the other hand, the massive government liquidity injections will most likely eventually get credit moving again.

There could well be more negative impacts on muni bonds, but the municipal bond market will eventually normalize. When that happens, yields will revert to their traditional relationship to Treasuries.

In the balance of rate adjustments by Treasuries and muni bonds, we expect that muni rates will fall, producing capital gains.

To the extent that a taxable portfolio is invested now (as opposed to standing aside in cash), we think municipal bonds have a constructive role to play in an asset allocation program.

By Richard Shaw

http://www.qvmgroup.com

Richard Shaw leads the QVM team as President of QVM Group. Richard has extensive investment industry experience including serving on the board of directors of two large investment management companies, including Aberdeen Asset Management (listed London Stock Exchange) and as a charter investor and director of Lending Tree ( download short professional profile ). He provides portfolio design and management services to individual and corporate clients. He also edits the QVM investment blog. His writings are generally republished by SeekingAlpha and Reuters and are linked to sites such as Kiplinger and Yahoo Finance and other sites. He is a 1970 graduate of Dartmouth College.

Copyright 2006-2008 by QVM Group LLC All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Richard Shaw Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.