Gold: Evergrande Investors' Savior

Commodities / Gold and Silver 2021 Oct 07, 2021 - 10:26 PM GMTBy: The_Gold_Report

Sector expert Michael Ballanger links debt and wolf packs in this exploration of the effects that the troubled Chinese company will have on gold.

When I first launched the GGMA Advisoryservice in January 2020, the very first Forecast Issue dealt with the globe's number one ailment, and it was not then, and is not today, related to mankind's physical health but rather its financial health. The word that kept resonating throughout that issue was debt.

If the global financial system was a human body, debt would be the fatty tissue that surrounds and clogs our organs, while recessions would be the fasting that rids the body of type 2 diabetes, obesity and depression. The problem that I identified as early as 2008 was that those that would manage our lives (whether elected or unelected) carry a belief system that holds that the best cure for obesity is a bowl of chicken noodle soup followed by six Big Macs and a big slice of apple pie.

"Debt default in tough times is the economic wolf pack that culls the economy of inefficient businesses and excesses."

In other words, it has been debt that has caused the past two major financial upheavals, and both involved the unprecedented creation of mind-boggling amounts of debt in order to avoid the natural cleansing of debt that occurs during economic downturns.

In the book "Never Cry Wolf," by Canadian legend Farley Mowat, the moral of the story is that the much-maligned wolf packs of the northern tundra, which were believed to be responsible for decimation of the herds of caribou that roamed the north country, were actually not the culprits at all. It turned out the wolves are invaluable "cullers of the herd," and eliminated the sickly and genetically inferior from the ranks allowing only the fittest to survive thus ensuring its future strength and vitality.

Debt default in tough times is the economic wolf pack that culls the economy of inefficient businesses and excesses, but both policymakers and central banks decided to circumvent a natural process that had worked imperfectly yet effectively since the Industrial Revolution. When the dot.com bubble burst in 2000, rather than letting markets find their footing, they dropped rates and issued debt to stimulate a stock market that had already started from its Volcker-esque nadir in 1982 from a level under 800 on the Dow.

Then, a mere eight years later, after the bankers loaded up on sub-prime mortgages and grew outrageously obese on illicit profits and shoddy risk controls. Another swath of debt was issued and these undisciplined behemoths were allowed to survive and, in fact, surpass their exploits in financial gluttony to the extent that there is no longer even an infinitesimal shred of respect for the purchasing power of currency held by legislators or their central bank hitmen.

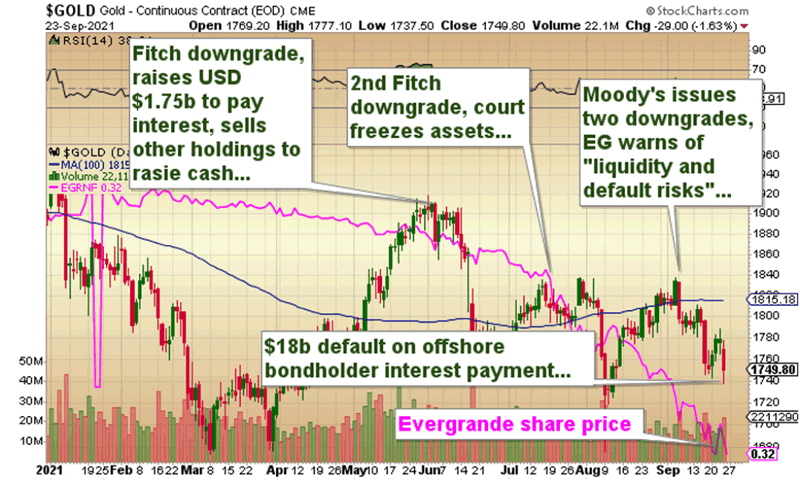

It all boils down to debt, and no better evidence of that disease rearing its ugly head again than in the recent Evergrande (China) fiasco, where this company (which has been in trouble since 2017) began to really unravel around June of this year.

Importantly, not only does the chart and timeline of Evergrande reveal a story of greed and debt destruction, but it also represents a clear corollary between these events and the role of gold bullion as a store of value. From the lows of April at US$1,670/ounce, gold was clipping along in great shape until June when, for no apparent reason (until now), it suddenly reversed. It matches perfectly with the first Fitch downgrade for Evergrande in June of this year, the same time that gold peaked above $1,900.

While the finger-traders out there who look at gold as the answer their relationship problems, Evergrande bondholders are thankful for their safe-haven position in bullion, without which they would be holding only a half-empty bag of malodorous animal waste. While they are finding it difficult to eliminate the stench of their bondholder bereavement, they at least can celebrate the wisdom of owning an asset that has rescued millions over the past five thousand years, including retirees, portfolio managers and refugees.

'If history is any guidepost, we can expect another massive global debt creation jamboree."

Now, is that cause for celebration for those of us who are perched on skyscraper ledges awaiting a suitable moment to surprise a passing tour bus with a sudden "thought I'd just drop in and say hello" moment? The answer is a categoric "not on your life." This has been an aggravation of the highest order for those who count their golden riches each night before bed, to the extent that even I am getting frustrated answering countless emails asking what it is going to take to get gold back in vogue again.

My answer is always the same: Nothing is wrong with gold if you have owned it at various prices since 2001, but it is if you were unable to spell the word "gold" until March 2020, when you flipped on your Instagram account and read that some anonymous guru claiming to be a teenage billionaire was loading up on gold and that "you should too!" — then, it is understandable that you are concerned.

The fact remains that the gold market has been absorbing a great deal of Asian selling because if Evergrande is the tip of the Chinese iceberg that many of my colleagues are now "onto," then with 30% of global liquidity now provided by the Chinese, any hiccup will undoubtedly cause a further desperate scramble for liquidity. If history is any guidepost, we can expect another massive global debt creation jamboree not unlike the post-COVID one that sent gold to US$2,089 in the summer of 2020.

I know — now you are rolling your eyes and saying "Well, that's just great, but WTF do I do about my November call options, which are seriously underwater, and all my junior golds that have gone 'no bid' lately?" The answer is really not as terribly convoluted as it might appear; gold is approaching $1,750 support, and while it has knifed down through it a couple of times this week, it feels like the selling pressure is abating. With the commercial traders still short some 23,245,000 ounces of paper gold, and with some legislative deadlines approaching, I think that downside probes such as the one we had this week are coming to a rapid and well-deserved conclusion, after which a run for the highs in in order and long overdue.

Back to the topic of Evergrande and China, it seems that the Middle Kingdom is experiencing somewhat of a "come to Jesus" moment, with electricity shortages popping up all over the country. But with the revelation that the CCP has officially branded all crypto transactions as "illegal," there is the definite odor of "desperation verging on panic" in the air and that is certainly not a bearish setup for gold, unless the crisis is one of debt liquidation or debt default, which, in themselves, are abjectly deflationary. At this point, it is the response of the CCP that will drive gold. Bailouts are gold-bullish; debt defaults are gold-bearish — period.

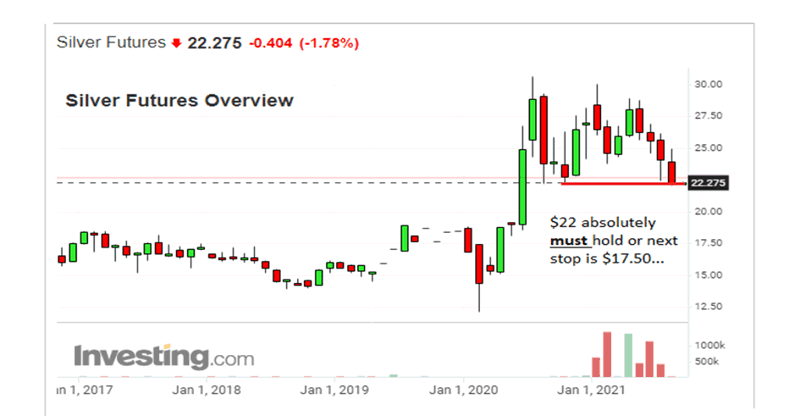

Ever since February and the #Silver Squeeze insanity that essentially bagged a bunch of newbie traders with the lure of sudden riches (and the encompassing anatomical enhancements), I have been a vocal opponent of the cymbal-clashing and pompom-waving that has dominated the silver narrative. But since everything is a function of relative value and price, and not vengeance upon the bullion bank behemoths (!), I am now looking at December silver a tad differently. On a risk-reward basis, you have those important lows in September and November of 2020 and August and September (today) in the US$22.02–22.35/ounce range, so by my logic, I can take a big position right here (for the first time in ages) and risk down to US$21.90 (on a two-day closing basis only) on the assumption that $22 is the near-term floor for the shiny metal.

As for the mining shares as a group, I recall a certain mining industry legend speaking last fall about how fundamentals for the miners had never been better, with high prices for their product (gold) being accompanied with terrific prices for their input costs (like energy). But here we are a year later, and those input costs are rising faster than Jerome Powell can say "transitory" because, in case no one cares, oil prices now carry a 70-handle versus the 30-handle of last October.

Now, these miners are sporting the best balance sheets they have had since the 1970s, and since "ounces in reserve" no longer drives valuations, they are now focused on "profitability" — while it has not yet caught on with the generalist fund managers who still think that these guys are classic ripoff artists, which, I should add, is a moniker well-deserved from their actions during wthe last bull cycle. What should occur in the next phase of the golden bull is that oil prices stabilize as gold prices resume a more appropriate spread over energy input costs, allowing for enhanced profitability.

This chart shows the importance of deal selection in navigating the gold space. 2021 has been a brutal year for gold and silver investors, yet top-ranked Getchell Gold Corp. (GTCH:CSE; GGLDF:OTCQB) has been able to fend off the boo birds successfully, thanks to great continuing results from Fondaway Canyon (Nevada) drilling. (More news pending this month.)

As for the juniors, the best thing that can happen for them is to have the seniors enjoy a valuation expansion based on their pristine balance sheets, which are, in case you take the time to do a comparison, infinitelybetter than many of the S&P 500 "zombies" that cannot cover interest expense without doing a financing. Whether it is government debt, household debt, or corporate debt (created to enrich the C-Suites through buybacks), it is the debt that keeps me 100%-invested in the precious metals sector, with honorably-appropriate positions in copper and uranium.

Keep your search engines tuned into "China" and "Evergrande," because I have a distinct sensation that we have not heard the last from this chapter. At the point where China liquidity issues morph into safe-haven buying for the precious metals is the precise point that the golden bull returns and the true definition of the term "ever grand" presents itself.

Follow Michael Ballanger on Twitter @MiningJunkie. He is the Editor and Publisher of The GGM Advisory Service and can be contacted at miningjunkie216@outlook.com for subscription information.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.