U.S. Real Estate Ownership and Investing Dangerous Myths

Housing-Market / US Housing Apr 03, 2009 - 04:58 PM GMTBy: Jennifer_Barry

In March, I started reading a new rush of positive news headlines about U.S. real estate. According to the U.S. Census Bureau, new home sales increased 4.7% in February in comparison to the January revised figures. This was the biggest leap since 2003. MDA Dataquick reported existing home and condominium sales jumped 43% year-over-year. Mortgage applications also rose 32.2% in the third week of March.

In March, I started reading a new rush of positive news headlines about U.S. real estate. According to the U.S. Census Bureau, new home sales increased 4.7% in February in comparison to the January revised figures. This was the biggest leap since 2003. MDA Dataquick reported existing home and condominium sales jumped 43% year-over-year. Mortgage applications also rose 32.2% in the third week of March.

However, not all news was good, as median house prices fell 15.5% year-over-year. Most home loans were initiated to refinance mortgages, not to buy real estate. New home sales hit their lowest number since tracking started in 1963, down 41.1% from February 2008. The 4.7% increase is a dubious figure, as the Census Bureau admits this statistic has a margin of error of 18.3%. In effect, the numbers could be up 23% or down 13.6%, it's impossible to say.

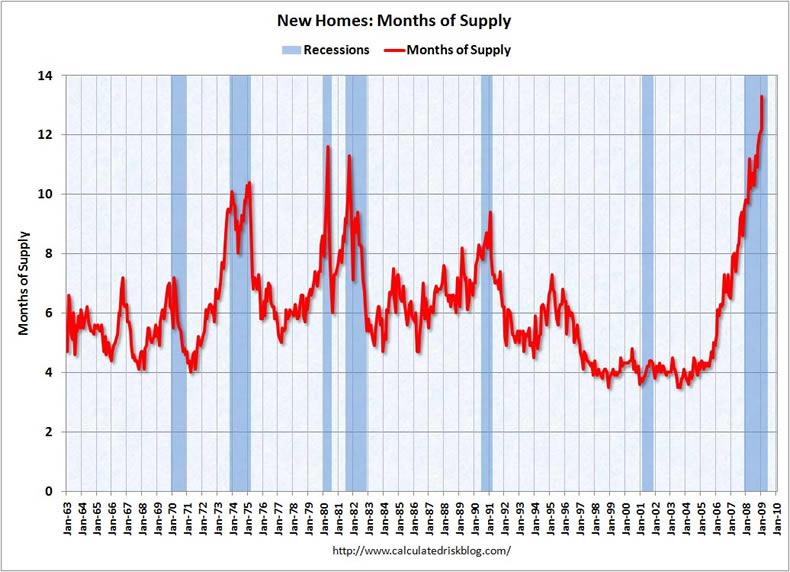

Even if new homes were easier to sell last month, one month doesn't make a trend. New home sales have plunged at a frightening rate, as buyers are incentivized to purchase much cheaper existing homes, especially those in foreclosure. History indicates new homes will bottom first, relatively early in the cycle. This doesn't mean prices have stopped falling, as the U.S. has more than 12 months inventory of unsold residences, a 36 year high. In fact, in my neighborhood builders are still constructing condos even with so many units unsold because they have already secured the loan. Whether they repay it or not is another question.

Unfortunately, I fear that many people will be encouraged by the sunny headlines and jump into the housing market too soon. Many potential homeowners are sick of waiting, and want validation of their emotional decision to purchase. I've talked to many acquaintances who refuse to believe that housing could take several years to rebound.

Frankly, the media has called a bottom several times since 2006, and they are misinterpreting the data again. After missing the giant bubble to begin with, their judgement and motives are both suspect. The real estate industry is an important advertiser, and few want to think that the economy is in a depression.

Myth Busting

It's not surprising that people wish to buy a house. In the United States, homeownership implies success, stability, and adult responsibility. Owning your residence gives you more control over your environment than renting, plus increased privacy and tax savings. When prices are rising, building equity through real estate makes sense for many people. However, in a housing crash, marketing techniques used to sell homes can convince families to make a catastrophic financial decision. I debunk the top housing myths below:

1. Real estate is a great long-term investment. Some investors made fortunes during the housing bubble, flipping condos for a quick profit. However, this kind of high-risk speculation requires liquidity and excellent timing. Those who failed to exit before the bust are facing bankruptcy and foreclosure. Most people who bought homes in 2004 or later are now “underwater,” owing tens of thousands of dollars more than their property is worth.

In contrast with homes, gold has been a great investment this decade. The median home cost 605 ounces of gold in 2000, but would require just 218 today, demonstrating that precious metals have risen during the housing crash.

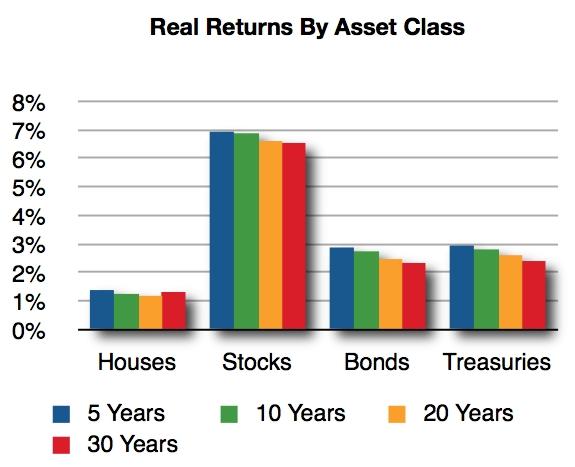

Even homeowners willing to hold real estate for many years will not see a fat profit, and may not have their house appreciate at all. Looking at the last major housing correction of 1990 for guidance, the S&P/Case-Shiller Index shows that the market didn't truly recover until 1996. I expect the unwinding of this housing bubble will take longer, due to the severity of the economic crisis and the record number of foreclosures predicted by the adjustable rate mortgage data. Even over a thirty year period, Fidelity researchers found that housing just barely outperformed the Consumer Price Index, lagging stocks and bonds.

Your home price may never recover in your lifetime. In the 1926 Miami real estate bubble, it took 80 years to recoup an investment in nominal terms, not adjusted for inflation!

2. Homeownership seems more expensive, but it's cheaper once you calculate the tax benefits. It's true that mortgage interest and property taxes can be deducted from your U.S. income tax bill. Using an online calculator, I estimated that buying a house with a $150,000 mortgage would save over $5,000 per year in taxes, if I itemized my deductions.

With the new stimulus plan, Congress passed a first time homebuyer credit which can be applied to either your 2008 or 2009 taxes, but the property must be purchased this calendar year. It totals 10% of the house price with a maximum of $8,000.

However, there are some preconditions. Families must remain in the home at least three years, and it must be a primary residence. The borrower cannot have owned a home in the last three years. The credit is also applied on a sliding scale, so it helps lower income citizens more. Singles earning more than $75,000 or married couples earning over $150,000 are totally ineligible.

Before you run out and buy a house, determine if you would actually benefit from the tax credits on a long-term basis. Your savings may be excellent the first year, but subsequent years will show a much smaller discount. If you have to sell the home soon due to a move or job loss, the IRS will demand repayment of the credit. If you are in a market like Las Vegas with steeply plunging real estate prices (down 33% year-over-year), it does you no good to save $14,000 on your taxes next year but lose $20,000 in equity.

3. Purchasing a home builds equity, which is a form of savings. This only works if real estate prices are stable or rising, and you steadily pay down your mortgage. If prices fall, you can achieve negative equity, and you owe the lender money even after you sell your house. Even if you have equity saved, you can lose it if you suffer a financial setback like unemployment. You may not be able to sell your home fast enough in this difficult market. If your bank seizes your house for nonpayment, the lender keeps all that equity.

4. Buying is cheaper than renting. I have seen some news stories claiming this, but frequently their methodology is flawed. I have owned two houses in the past, and I know there are a number of hidden costs real estate agents don't include when calculating your monthly expenses. In addition to the mortgage, property taxes can be substantial. Most people must pay homeowners' association or condominium fees. Yards are expensive, and you must pay for landscaping or buy the tools and materials to do the work yourself. In addition, you should have savings to fix the items that regularly need repair like fences and driveways. In an apartment, renters can ask for new appliances and paint when necessary, but homeowners bear these costs themselves. Kitchens and bathrooms periodically need replacement due to leaks and heavy wear, but few property owners plan for these costs. Of course, you can neglect maintenance but that will be reflected in the price when you attempt to sell your house.

Don't be fooled that housing is a bargain just because it's “on sale.” It may be cheaper, but historically, real estate is still tremendously overpriced. For over two decades, the ratio between the median home price and median household income was 2.8. Based on the latest government figures, the ratio is now a stratospheric 4. Wages were based on 2007 statistics, so income is probably lower today after the sharp spike in unemployment. Add in the wealth destruction effect from home equity losses, constriction of credit, and a shaky job market and you have a public who is disinclined to pile on additional mortgage debt.

So how can you tell if buying a home is a good deal? A traditional metric is that the house price should be about 100 times rent. Unfortunately, this is not even remotely close to current market prices for most Americans. Another tool to evaluate your area - as all real estate is local - is this handy calculator which tells you how long you will have to wait for homeownership to save more money than renting. Be sure to click on “Advanced Settings” so you can add in all your expenses, like realtor commissions and renovation costs. However, potential buyers should weigh the risk that their equity could disappear if home values drop.

5. Only college students and losers rent. My husband and I h ave professional careers, so many acquaintances are surprised when they find out we rent. They are even more astonished when we tell them that we owned a house, but we sold it in March 2006 to avoid the housing bust.

During the subprime mortgage boom, almost everyone could get a loan. The common assumption is that renters must be broke or otherwise undesirable or they would own a home. Another misconception is that houses are nice places to live, but rentals are trashy, and no place for children. The truth is, many beautiful homes are available for rent, and some apartments are roomier and more luxurious than houses. Realtors played up the snob appeal of homeownership because it helped them earn commissions. Buy real estate if it makes financial sense for you, not because you want to impress the neighbors.

Nevertheless, the rising rate of foreclosures means that renters should take some precautions. If you are not renting from a large property management company, be wary of signing a lease with a speculator stuck with a house that she or he can't sell. You don't want to rent from these individuals, as they may get foreclosed on and you may be evicted with little notice. To avoid becoming the victim of fraud, check your local deed records to make sure that your landlord is the registered owner and is not in foreclosure. In addition, check the tax rolls to see if the owner is delinquent. If he or she bought the house in the past five years, that's a huge red flag. The landlord may pocket your rent money instead of paying on the loan.

6. The government will fix the housing mess. For almost two years, the federal government has promised to help homeowners avoid foreclosure. As the economic crisis deepened, much was debated but little concrete help was extended. Last summer, Congress passed HOPE for Homeowners to great fanfare. This bill was supposed to spend up to $300 billion and assist up to 400,000 families. Instead, this voluntary program has been a colossal failure, as 752 homeowners applied and only one foreclosure was prevented. Most lenders refused to participate, as the terms included forgiving part of the mortgage. Banks would have to write down the value of their loan portfolio in an environment where capital was evaporating.

President Obama's newest initiative, the Homeowner Affordability and Stability Plan (HASP), would appropriate $75 billion to reduce monthly payments by lowering interest rates or extending loan terms. Even if HASP is more successful than HOPE, I question the wisdom of keeping families in overpriced real estate they can't afford. Most attempts to modify mortgages have still ended in foreclosure, only the borrower spent more time futilely making payments. It would be better for most homeowners to go into bankruptcy now rather than suffer for years to service a burdensome loan for no economic benefit.

The Administration's plan seems to be another back door subsidy to financial institutions, rather than a reasoned attempt to aid distressed borrowers. The banks can continue to earn income off these toxic mortgages which should have resulted in huge losses. The U.S. government has already spent trillions bailing out corporations from Fannie Mae to AIG. The rationale is that the financial system must be stabilized so that banks can make loans again, but why should taxpayers give these corporations money and hope they will lend it back at interest?

In reality, sending every homeowner a check would be more sensible than the current plan. According to U.S. Global Investors, just $1 trillion would be enough to buy all of the single-family and multi-family residences in the state of Texas. Instead, yet-unborn generations are on the hook for the tremendous government borrowing to fund the bailouts, and the children of today are unlikely to be able to afford a house in 20 years.

Purchasing real estate is an important decision, with a large financial impact. It may be the right move for you. However, it's essential to make your decision based on facts, rather than emotion or propaganda from the real estate industry. While I hope the market turns around soon, the data doesn't support that view. Until it does, I will continue to rent.

by Jennifer Barry

Global Asset Strategist

http://www.globalassetstrategist.com

Copyright 2009 Jennifer Barry

Hello, I'm Jennifer Barry and I want to help you not only preserve your wealth, but add to your nest egg. How can I do this? I investigate the financial universe for undervalued assets you can invest in. Then I write about them in my monthly newsletter, Global Asset Strategist.

Disclaimer: Precious metals, commodity stocks, futures, and associated investments can be very volatile. Prices may rise and fall quickly and unpredictably. It may take months or years to see a significant profit. The owners and employees of Global Asset Strategist own some or all of the investments profiled in the newsletter, and will benefit from a price increase. We will disclose our ownership position when we recommend an asset and if we sell any investments previously recommended. We don't receive any compensation from companies for profiling any stock. Information published on this website and/or in the newsletter comes from sources thought to be reliable. This information may not be complete or correct. Global Asset Strategist does not employ licensed financial advisors, and does not give investment advice. Suggestions to buy or sell any asset listed are based on the opinions of Jennifer Barry only. Please conduct your own research before making any purchases, and don't spend more than you can afford. We recommend that you consult a trusted financial advisor who understands your individual situation before committing any capital.

Jennifer Barry Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.