Why Investors Need to Pay Attention to These Emerging Markets

Stock-Markets / Emerging Markets Sep 13, 2010 - 06:25 AM GMTBy: Money_Morning

Jon D. Markman writes:

The U.S. market showed improvement last week, but is still falling short of the continued growth and profit opportunities that emerging markets have to offer.

Jon D. Markman writes:

The U.S. market showed improvement last week, but is still falling short of the continued growth and profit opportunities that emerging markets have to offer.

Stocks inched higher on Wall Street over the past week, taking heart from news of a modest improvement in jobs and a narrowing of the U.S. trade deficit. Both acted to counter the argument that the U.S. economy is speeding for a cliff in a foreign-badged car.

Bonds finished down slightly, crude oil rose 2.6%, and gold was down slightly.

A tad dull, sure. But the fact that there wasn't a rout after the big gains of the first week of the month, though, has to be considered a win for the bulls.

And some updates from the corporate world and overseas markets should keep investors cheering this week.

Positive corporate news was word that McDonald's Corp. (NYSE: MCD) logged a 4.9% jump in same-store sales worldwide, and Apple Inc. (Nasdaq: AAPL) ended its dumb battle with Adobe Systems Inc. (Nasdaq: ADBE) over the use of the smaller firm's software on the iPhone and iPad.

And finally there was more peace-pipe smoking in Silicon Valley when Oracle Corp. (Nasdaq: ORCL) and NetApp Inc. (Nasdaq: NTAP) agreed not to keep suing each other over patent infringement claims.

NetApp, described in detail to people who have attended my MoneyShow seminars in the past year on the best stocks for the mobile Internet and cloud computing, is one of the handful of technology leaders in this era. It's one of the few companies -- like F5 Networks Inc. (Nasdaq: FFIV), Akamai Technologies Inc. (Nasdaq: AKAM) and ARM Holdings Plc (Nasdaq ADR: ARMH) -- that is in growth investors' current pantheon for its steady growth and ability to surpass expectations. If you loved owning Microsoft Corp. (Nasdaq: MSFT), Intel Corp. (Nasdaq: INTC) and Dell Inc. (Nasdaq: DELL) back in 1990s, these four smaller companies are just like that now. Don't leave your portfolio without them.

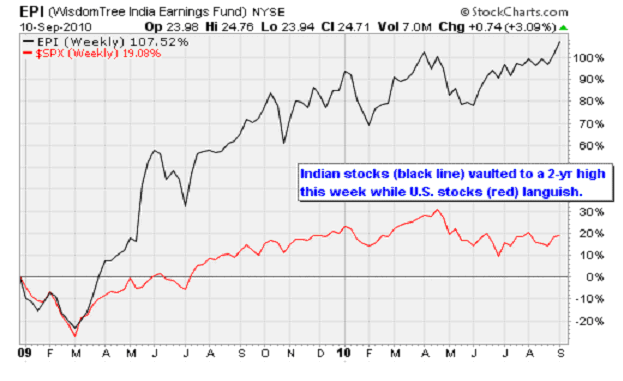

But the big story of the day, like so many of the past year, was overseas, as iShares MSCI Thailand Index Fund (NYSE: THD) and WisdomTree India Earnings Fund (NYSE: EPI) stocks rocked the set with roaring advances to new two-year highs.

.I've been talking about these overseas markets a lot this year, but we can't get jaded. You need to realize that what is happening is quite remarkable. These are not debt-funded manias as we saw a decade and a half ago, but rather the result of some sharp business people taking advantage of improved domestic industriousness and global opportunities.

If you see them as just something crazy that's happening in the southern hemisphere, you've got an outdated investment model in your head. Fifteen years ago you would have had to buy a global mutual fund to have access to foreign markets -- and the ones oriented toward emerging markets were very expensive, with high loads and expense ratios. Even when they ultimately went no-load there was little transparency: You never knew exactly what was in those funds or who was managing them, and costs were still high.

But now we can buy an indexed exchange-traded fund that represents the bulk of the market capitalization of the countries at minimal cost. Or if you prefer, you can buy a very liquid American Depository Receipt, such as Infosys Technologies Ltd. (Nasdaq ADR: INFY). These are great advances for investors, and if you're new to the game you need to realize that owning stocks or whole exchanges in other countries should be considered a very normal course of activity, much like you would equally consider buying a Toyota Motor Corp. (NYSE ADR: TM) or a Ford Motor Co. (NYSE: F) truck based on its features and value rather than its country of origin.

In other words, the whole point of investing is to make money from the appreciation of under-valued assets that rise in price -- preferably in a non-volatile way. Just like the purpose of buying a car is to obtain safe transportation. When we look across the spectrum of choices, we see on the one hand that most major U.S. and European indexes are really struggling, while the ones in faster growing regions are performing well, and are still relatively cheap. It shouldn't be a hard choice.

Aussie Economy: No Wonder From Down Under

Holding shares back a bit this week was the release of the Federal Reserve's Beige Book, which described "widespread signs of deceleration" in the U.S. economy. Thanks for noticing, guys.

ISI analysts at the same time put out a note stating that most of their U.S. company surveys are turning down.

And as for Europe, analyst Tim Backshall at Credit Derivatives Research put out a note Wednesday afternoon stating, "I have to say that everyone we spoke to, and that includes the many voices in our heads, saw European data and actions as much less positive than the markets appeared to. German IP [industrial production] rose less than expected and exports started to drop, Spanish IP rose less than expected, Dutch IP fell more than expected, the French deficit rose more than expected, UK house prices rose slower than expected and IP was low but as expected, and Greece and Portugal revised GDP down. As if that was not enough, the new Portugal bond issue, while having a decent bid-to-cover (thank you ECB), went out notably higher in yield than the last one and incredibly higher in the longer-dated issue -- getting close to the magic 6% yield that so many remain fearful of."

Meanwhile, over in Asia risk sentiment had a lot more positive data to lean on: The India index is breaking through a channel and hitting new highs in concert with a report that auto sales in that country grew by 33% for the month of August.

Also driving the conversation in Asia: The Australian jobs report for August was a high quality upside surprise, as total jobs increased 30,900; that was well ahead of the market's expectation of a 25,000 gain. The composition of growth was highly skewed to full timers, with part-time positions falling. The unemployment rate meanwhile has reached a new cyclical low at 5.1%.

No wonder Australian consumer income and spending levels are up. The Aussie economy has been on fire, and its success feeds into the rest of Southeast Asia, as its citizens, for instance, have more money to travel to Indonesian resorts and buy vacation condos in Thailand. The entire region is on a positive feedback loop, while the greater U.S. region is basically out of the loop.

I have no doubt that the American markets will rise again at some point, but in the meantime there's no point in waiting around in Standard & Poor’s 500 Index funds. If you're not already in synch with us with emerging-market funds and stocks, I hope you'll start soon.

Week In Review

It was another intriguing week in the silent world of data that measures world productive output and consumption. There was a little for the worriers and a little for the optimists. Investors took it all in and battled to a tie. Bonds finished down slightly, crude oil rose slightly, and gold was up slightly to a new high year to date. The Dow Jones Industrial Average is up 0.3%, the S&P 500 down 0.5%, Nasdaq Composite down 1.2% and Russell 2000 Index up 1.8%.

Here are milestones, with a hand from the analysts at Econoday.

-- Stocks inched higher, consolidating gains of last week. The S&P 500 rose a grand total of four points. The fact that there wasn't a rout after the big gains of the first week of the month has to be considered a win for the bulls.

-- U.S. trade deficit shrank a touch in July. U.S. exports are finally trending up again. The rebound in exports combined with a dip in imports to reduce our deficit with the world quite a bit, to $42.8 billion from $49.8 billion in June. Consensus was looking for a $46.3 billion deficit. Exports rose 1.8% after falling 1.3% in June. Imports fell 2.1% after rising 3.1% in June. Outside of oil, imports fell 3%, after a 4.6% advance in June The report will give third-quarter GDP a positive jolt.

-- Export strength came from capital goods. Looking at the end-use column, the lift in exports was led by a $2.3 billion jump in non-auto capital goods. About half of that was civilian aircraft. (Thank you, The Boeing Co. (NYSE: BA)!) Industrial supplies were up half a billion. Consumer goods ex-autos were flat.

-- The drop in imports was broad based. Consumer goods fell $1.9 billion, autos were down $0.7 billion, capital goods ex-autos declined $0.6 billion, and industrial supplies (including oil) fell $400 million. The meaning of this number: Businesses prepared for a leaner holiday season by cutting their orders of consumer goods. U.S. businesses also appeared to be paring plans to invest in equipment, which is why non-auto capital goods imports fell.

-- Consumer credit remains weak. Households continue to deleverage, as consumer credit contracted again, down $3.6 billion in July. That was the sixth straight monthly decline. Revolving credit (mostly your credit cards) fell $4.4 billion. This is all partly due to tighter lending standards that were put in place in financial reforms, but it also reflects individuals' decision to pay down card debt and spend less. Also, banks are still writing off bad debt (at a slower pace) so they're not sending out all those come-ons through the mail. From an investment perspective, we kind of want people to start spending again, but the data always shows it's very dependent on employment gains.

-- The Fed's Beige Book showed the recovery continuing, though at slower pace. Five of the twelve regional Federal Reserve banks reported moderately paced economic growth and two pointed to ''positive developments or net improvements.'' The other five said conditions were mixed or decelerating. Overall, the Fed found the economy suffered from ''widespread signs of a deceleration,'' in its growth proceeding at a "modest pace." But hey, no second recession in sight.

-- The Fed sees consumer spending increasing despite continued caution that limited non-essential purchases. (Good for groceries, bad for Lady Gaga). Within manufacturing, weakness was largely related to construction while strength was in auto-related production, including steel. Housing was down and non-residential construction was weak.

--Inflation was subdued but the Fed saw isolated sources of inflation pressures, including for specialized workers. In Fedspeak: ''Upward price pressures remained quite limited for most categories of final goods and services, despite higher prices for selected commodities such as grains and some industrial materials. Wage pressures also were limited, though a few districts noted increased upward pressures in a narrow set of sectors experiencing a mismatch between job requirements and applicant skills.”

Bottom line: The U.S. economy is inching along due to modest strength in exports. Consumers are not helping -- but they're not collapsing into a molten pool of crocodile tears. Consumers remain sub-par relative to past recoveries due to a major shift in attitudes about debt as they deleverage. Still, there is no convincing evidence of a double dip.

The theme of the coming week in economic data will be trends in manufacturing and consumer spending, and a look at inflation pressures.

The Week Ahead

Monday: Treasury will report the deficit for August. It will be big.

Tuesday: Retail sales for August will be announced. They were up 0.4% in July and down 0.3% in June. We know motor vehicle sales were relatively soft in August and chain store sales were okay. The consensus is to expect a gain of 0.3%, with a range of gaining 0.1% to 0.5%. Also business inventories for August will be counted. Expect them a bit higher, up 0.6%. Earnings: Best Buy Co. Inc. (NYSE: BBY).

Wednesday: Empire State Manufacturing Survey was a positive in August, up two points to 7.1, but suggested a slowing trend. Figure a gain of 5% this time, with shipments down. Industrial production in August will be reported. Capacity utilization figures have been trending positive, and regional reports are break-even. Call it a draw, at up 0.1%.

Thursday: The producer price index for August will be announced. In July it rebounded 0.2%, after a 0.5% fall in June. Recent reports show food prices are up and autos and drugs are up. Figure a 0.3% increase in PPI. Take that, deflationistas! Initial jobless claims were down a bunch in the September 4 week, falling 27,000 to 451,000. That's the lowest level in two months. Consensus is looking for a 4,000 person gain to 455,000. My metrics are looking for a slight decline, to 450,000. Earnings: FedEx Corp. (NYSE: FDX), Oracle Corp. (Nasdaq: ORCL), Research in Motion Ltd. (Nasdaq: RIMM).

Friday: Quadruple witching day! Spooky. It's the day every three months when stock index futures, stock index options, stock options, and single stock futures all expire at the same time. It makes for a lot of volatility on Wednesday and Thursday, then the Friday is usually mild.

[Editor's Note: Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today's markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what's been the toughest market for investors since the Great Depression, it's time to sweep away the uncertainty and eradicate the worry. That's why investors subscribe to Markman's Strategic Advantage newsletter every week: He can see opportunity when other investors are blinded by worry.

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.]

Source : http://moneymorning.com/2010/09/13/emerging-markets-3/

Money Morning/The Money Map Report

©2010 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or 72 hours after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.