Investor Sentiment Improves on Worst of Credit Crisis Behind Us

Stock-Markets / Financial Markets May 04, 2008 - 12:31 PM GMT

“The world's favorite season is the spring. All things seem possible in May,” said Edwin Way Teal.

“The world's favorite season is the spring. All things seem possible in May,” said Edwin Way Teal.

And so it seemed during the past week as we witnessed a further improvement in investor sentiment and risk appetite, supported by the viewpoint that the worst of the credit crisis might be behind us. The end result by Friday's close was strong gains for stock markets (with the Volatility Index at its lowest level since December), a further recovery of the US dollar, a sell-off of most commodities, and a weak undertone in government bond markets.

The Fed laid the foundation for investors' actions at its policy meeting on Tuesday and Wednesday, the outcome of which was the FOMC cutting the Fed funds rate by 25 basis points to 2.0% – the lowest level since late 2004.

The accompanying press statement cited weakness throughout the US economy and stress in financial markets. It noted higher inflation, but also said that inflation should moderate in the near term. In a departure from the previous wording, the statement made no reference to downside risks to growth.

Overall, the market interpreted the Fed's directive to imply that it was most likely to pause and await the impact of the 325 basis point reduction in the Fed funds rate, the economic stimulus package, and other programs put in place. Interest rate futures price in a rate rise towards the end of the year.

The US dollar's strength was rooted in the expectation that the Fed was possibly done with reducing rates for the moment. However, the Fed was not done with its efforts to improve liquidity in stressed markets as indicated on Friday when it raised the amounts available for depository institutions at its biweekly term-auction facilities by 50% and broadened the types of acceptable asset-backed collateral.

Although the US GDP growth rate was very weak in the first quarter – just 0.6% at an annualized rate – this was better than the consensus expectation of 0.2%. Growth was also 0.6% in the fourth quarter of 2007. Compared with the fourth quarter, however, investment in inventories was a positive for growth. This was offset by stronger imports, a decline in nonresidential construction, and weaker growth in consumer spending.

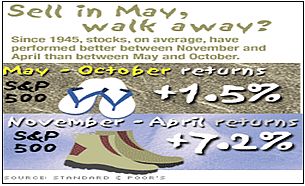

But investors have also nervously wondered whether stock markets were nor getting ahead of themselves. After all, May has a reputation as the advent of six “bad” months in the stock market, hence the axiom “Sell in May and go away”. (Click here to read my recent post on whether this is fact or fallacy.)

Before highlighting some thought-provoking news items and quotes from market commentators, let's briefly review the financial markets' movements on the basis of economic statistics and a performance round-up.

Economy

In addition to the FOMC's rate announcement and the GDP numbers, the past week saw a myriad of economic reports.

Summarizing the upshot of the most recent batch of statistics, John Mauldin ( Thoughts from the Frontline ) said: “Real (inflation-adjusted) retail sales have been flat for the last six months. Incomes are stagnant. Consumer spending is showing every sign of slowing even more. This employment report was ugly, when you look at the numbers under the headline statistics. Consumer sentiment is at 25-year lows.

“You can count on it that the National Bureau of Economic Research (NBER) will show a recession starting in the fourth quarter of last year and continuing at the least through the first quarter of this year. This one could last another six months. I still think long and shallow with a very slow recovery.”

Elsewhere in the world, the European Commission's economic sentiment indicator fell sharply in April, the eurozone's manufacturing PMI continued to ease, and German retail sales contracted as households struggled against higher prices for food and energy.

In the UK, the Nationwide Housing Price Index fell by 1.0% in year-ago terms in April – the first contraction in annual price growth in more than a decade. Consumer confidence continued to slide as households worried about their finances and the UK economy.

The Bank of Japan held interest rates unchanged at 0.5%, but cut its growth estimates for the year ahead, citing higher raw material prices and a slowing US economy.

WEEK'S ECONOMIC REPORT

| Date | Time (ET) | Statistic | For | Actual | Briefing Forecast | Market Expects | Prior |

| Apr 29 | 10:00 AM | Consumer Confidence | Apr | 62.3 | 62.0 | 61.0 | 65.9 |

| Apr 30 | 8:15 AM | ADP Employment | Apr | 10K | - | -60K | 3K |

| Apr 30 | 8:30 AM | GDP -Adv. | Q1 | 0.6% | 0.7% | 0.5% | 0.6% |

| Apr 30 | 8:30 AM | Chain Deflator-Adv. | Q1 | 2.6% | 3.0% | 3.0% | 2.4% |

| Apr 30 | 8:30 AM | Employment Cost Index | Q1 | 0.7% | 0.8% | 0.8% | 0.8% |

| Apr 30 | 9:45 AM | Chicago PMI | Apr | 48.3 | 49.0 | 47.5 | 48.2 |

| Apr 30 | 10:30 AM | Crude Inventories | 04/26 | 3848K | NA | NA | 2421K |

| Apr 30 | 2:15 PM | FOMC Policy Statement | - | - | - | - | - |

| May 1 | 12:00 AM | Auto Sales | Apr | - | 5.1M | NA | 4.9M |

| May 1 | 12:00 AM | Truck Sales | Apr | - | 6.3M | NA | 6.2M |

| May 1 | 8:30 AM | Initial Claims | 04/26 | 380K | 358k | 360K | 345K |

| May 1 | 8:30 AM | Personal Income | Mar | 0.3% | 0.4% | 0.4% | 0.5% |

| May 1 | 8:30 AM | Personal Spending | Mar | 0.4% | 0.3% | 0.2% | 0.1% |

| May 1 | 8:30 AM | PCE Core Inflation | Mar | 0.2% | 0.2% | 0.1% | 0.1% |

| May 1 | 10:00 AM | Construction Spending | Mar | -1.1% | -1.0% | -0.7% | 0.4% |

| May 1 | 10:00 AM | ISM Index | Apr | 48.6 | 49.0 | 48.0 | 48.6 |

| May 2 | 8:30 AM | Average Workweek | Apr | 33.7 | 33.7 | 33.7 | 33.8 |

| May 2 | 8:30 AM | Hourly Earnings | Apr | 0.1% | 0.3% | 0.3% | 0.3% |

| May 2 | 8:30 AM | Nonfarm Payrolls | Apr | -20K | -70K | -75K | -81K |

| May 2 | 8:30 AM | Unemployment Rate | Apr | 5.0% | 5.2% | 5.2% | 5.1% |

| May 2 | 10:00 AM | Factory Orders | Mar | 1.4% | 0.4% | 0.2% | -0.9% |

Source: Yahoo Finance , May 2, 2008.

The next week's economic highlights, courtesy of Northern Trust , include the following:

1. International Trade (May 9): The trade deficit is predicted to have narrowed to $61.5 billion in March from $62.3 billion in February, based on the assumptions in the advance estimate of GDP. Consensus : $60.8 billion.

2. Other reports : ISM non-manufacturing (May 5) and Pending Home Sales (May 7).

Markets

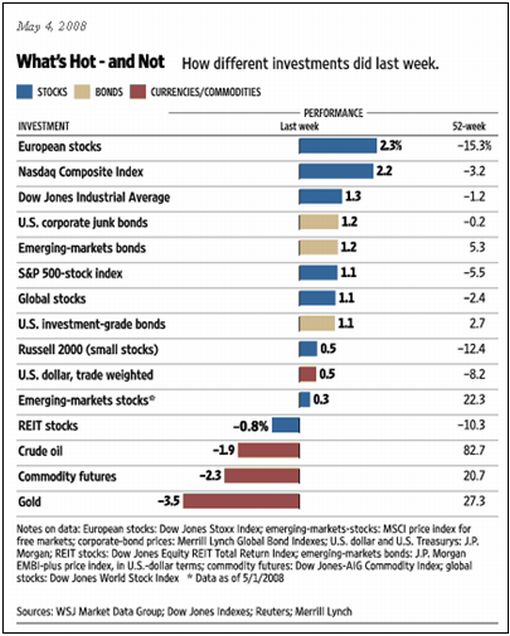

The performance chart obtained from the Wall Street Journal Online shows how different global markets performed during the past week.

Source: Wall Street Journal Online , May 4, 2008.

Equities

Global stock markets were in rally-mode and added to the previous week's gains, with the MSCI World Index closing 1.1% higher on Friday. European stocks (+2.3%) fared the best among the mature markets, whereas emerging markets (+0.3%) lagged the major markets.

The Brazilian market was a highlight of the week with the Bovespa Stock Index surging by 6.4% to hit an all-time high on the back of Standard & Poor's awarding the country an investment grade rating. The Bovespa Stock Index has registered a gain of 438% since its low of August 2003.

The Brazilian market was a highlight of the week with the Bovespa Stock Index surging by 6.4% to hit an all-time high on the back of Standard & Poor's awarding the country an investment grade rating. The Bovespa Stock Index has registered a gain of 438% since its low of August 2003.

The Chinese market also performed well with the Shanghai Stock Exchange Composite Index improving by 3.8% (on top of the previous week's gain of 15.0%), while the Hong Kong Hang Seng Index and the Bombay Stock Exchange Sensex 30 Index both finished 2.8% higher.

The strongest stock market index was again the Nasdaq Composite Index with a gain of 2.2% (YTD: -6.6%), followed by the Dow Jones Industrial Index with +1.3% (YTD: -1.6%), the S&P 500 Index with +1.1% (YTD: -3.7%) and the Russell 2000 Index with +0.5% (YTD: -5.3%).

A number of key technical resistance levels were breached as a result of the improvement in prices, most notably the S&P 500 Index's 1,400 level (closing level: 1,414). The next resistance level is at 1,435 where the Index will encounter its 200-day moving average. The Dow Jones Industrial Index has already crossed this barrier on Friday.

Fixed-interest instruments

US government bonds rallied for the first four days of the week, but sold off on Friday on the back of better-than-expected jobs data.

The yield on the two-year US Treasury Note closed the week 3 basis points higher at 2.46%, whereas the US Treasury Note yield declined by 2 basis points to 3.86%.

Government bonds elsewhere in the world followed a mixed pattern.

The lower Fed funds rate pulled US mortgage rates down sharply, with the 15-year fixed rate dropping by 16 basis points to 5.41% and the 5-year ARM rate falling by 33 basis points to 5.48%.

Money market stress eased somewhat as far as the three-month US dollar interbank rate was concerned, but euro rates tightened further.

Currencies

Following the FOMC's rate cut on Wednesday, many pundits argued that it could be the last reduction for a while. This boosted the US dollar to a five-week high against the euro and a two-month high against the Japanese yen.

Following the FOMC's rate cut on Wednesday, many pundits argued that it could be the last reduction for a while. This boosted the US dollar to a five-week high against the euro and a two-month high against the Japanese yen.

The euro declined on the back of a perception that the ECB may be moving closer to a rate cut as the economic outlook in the eurozone deteriorated further.

The stronger dollar impacted negatively on commodity prices and the currencies of commodity-producing countries such as the Canadian dollar.

High-yielding currencies such as the Australian dollar and the New Zealand dollar strengthened markedly as a result of a resurgence of carry trade transactions. On the other hand, the Japanese yen and Swiss franc came under selling pressure.

Commodities

The improving US dollar caused the correction in commodity prices to intensify, as illustrated by the following graph:

Source: StockCharts.com

Now for a few news items and some words and charts from the investment wise that will hopefully assist in steering our investment portfolios on a profitable course.

Hat tip: Barry Ritholtz's The Big Picture

Business News Network: Donald Coxe – How to structure a global portfolio

Source: Business News Network , April 30, 2008.

MarketWatch: Peter Bernstein – Saving for survival

Click here for a written version of E.S. Browning's interview.

Source: MarketWatch , April 29, 2008.

CNBC: Bill Gross – “Euphoric” stock market rebound may be premature

Source: CNBC , May 1, 2008.

Financial Times: Bank of England signals worst is over

“The correction in the credit markets has gone too far, the Bank of England says, in a signal that it believes the worst of the global crisis could be over.

“The bank's twice-yearly Financial Stability Report, issued on Thursday, says the credit markets ‘overstate the losses that will ultimately be felt by the financial system and the economy as a whole'. The view represents a big departure from its 2006 and 2007 warnings that risk was underpriced. It added that financial institutions would soon come to see that some assets now ‘look cheap'.

“John Gieve, deputy governor, said: ‘While there remain downside risks, the most likely path ahead is that confidence and risk appetite will return gradually in the coming months.'

“In becoming the first big official institution to offer a cautiously optimistic outlook for the financial sector, the bank shrugs off indications of falling house prices, noting that most households have lots of equity in their homes. Figures from Nationwide Building Society on Wednesday showed the first annual fall in house prices for 12 years, with values in April 4% down on their peak six months earlier and 1% lower than a year earlier.

“The optimistic outlook also contrasts strongly with last month's publications from the International Monetary Fund.

“Its report argues that if current market prices are to be believed, they imply ‘unprecedented' levels of default on mortgage-backed assets. Some 76 per cent of US subprime mortgages sold in the first half of 2007 would default with a loss of 50% on each of these impaired mortgages if market prices were correct, the bank calculated.

“Instead, it thinks there will be no defaults on triple A-rated subprime mortgage-backed securities even with a continued decline in US house prices, making these securities far too cheap in the market at the moment and causing banks to suffer unnecessary losses based on marked-to-market accounting. It said the market prices therefore reflected uncertainty about eventual losses, greater investor aversion to such uncertainty and illiquidity in the markets.”

Source: Chris Giles and Gillian Tett, Financial Times , April 30, 2008.

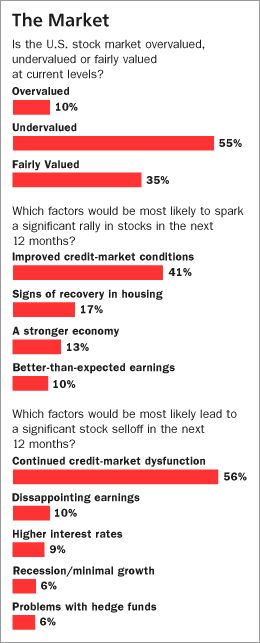

Barry Ritholtz (The Big Picture): US professional money managers are bullish

“Barron's does a regular ‘Big Money Poll' with domestic portfolio managers. Their most recent survey is the cover story for this week's mag.

“Barron's does a regular ‘Big Money Poll' with domestic portfolio managers. Their most recent survey is the cover story for this week's mag.

“What's the state of the professional fund manager's psyche? Bullish! Consider these numbers:

50% consider themselves ‘Bullish (43%) or Very Bullish (7%)'

12% consider themselves ‘Bearish (12%) or Very Bearish (0%)'

38% consider themselves ‘Neutral'

“Most pros are ‘looking over the valley' to an economic recovery: 74% believe the US is in a recession, but only 32% believe this will lead to a world wide recession.

“As to the state of the stock market, according to the managers, it is cheap: 55% believe it is undervalued, while only 10% think it is overvalued (35% chose fairly valued).

“The greatest risks to equities was surprising: It was not, according to the managers, disappointing earnings (10%) or higher interest rates (9%) or a recession (6%) or even hedge funds (6%) – rather, it was continued credit market dysfunction (56%).

“Lastly, 87% plan on being buyers of equities over the next 3 – 6 months; Only 13% said they expect to be sellers. Most are exposed to large cap (64%) versus midcaps (19%) and small caps (15%).”

Source: Barry Ritholtz's The Big Picture , April 28, 2008.

Jeffrey Saut (Raymond James): “Being There?!”

“For the past few months we have fallaciously suggested that interest rates were going to rise, the US dollar was going to firm, crude oil was subsequently going to decline (along with most other commodities), and that the major US indices, led by the financials, were going to rally; emboldened by the steepening yield curve, which implies the economy is going to recover.

“While we are often early, over the years we have tended to be generally correct. And last week, that envisioned sequence materialized with the financials, and early-cycle stocks, coming to the fore. Even though we believe it is a ‘false move', the difference between perception and reality is where investors' opportunities lie!

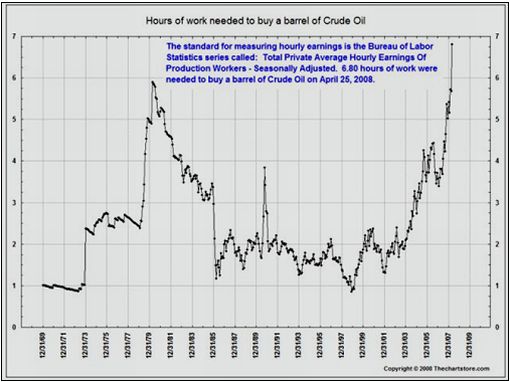

“Verily, we think the real surprise, going forward, may be that inflation rears its ugly head in 2009 as seen in the chart of how many work-hours it takes to buy a barrel of crude oil. Just yesterday, we filled the tanks of our boat to the tune of $1,000 ($4.50/gallon for regular gas); as well, we bought steaks on the way home at $27.00 per pound, yet the Fed tells us there is NO inflation! Clearly, this is sophistry, and we continue to invest/trade accordingly …”

Source: Jeffrey Saut, Raymond James , April 28, 2008.

Bill King (The King Report): Inflation – Americans don't buy with “core” dollars

“The Fed and much of Wall Street convinced themselves that the only inflation measure that matters is ‘core inflation', which excludes food and energy. The Fed's monks devised that measure to avoid an overreaction to commodity price movements, but instead they have used it to pretend that food and energy prices don't matter. Throughout this decade, they pointed to core inflation to argue that ‘inflationary expectations remain well anchored', even as the dollar and commodity price signals were telling us that the opposite was true. Americans don't buy gas and groceries with ‘core' dollars.”

Source: Bill King, The King Report , April 29, 2008.

Reuters: Inflation could become new No.1 enemy for investors

“Inflation threatens to supersede the credit crisis as investors' biggest enemy later this year as fears of a deep economic downturn recede and commodity prices show no signs of easing.

“Growing relief that the global economy has so far escaped the worst case scenario from the eight-month-old credit crisis has stabilized financial markets. World stocks, as measured by MSCI, are hitting three-month highs and pulling the dollar off its March record low against major peers.

“Many central banks, faced with the twin problem of the credit crisis and rising prices, have cut interest rates to ease the flow of credit, leaving inflation issues for tomorrow.

“However, the relentless surge in resource prices from oil to rice and the resilience of emerging economies risks are turning inflation into the bigger worry for policymakers and asset markets.

“Japanese inflation, which hit a decade-high in March triggering one of the biggest ever sell-offs in yen bonds on Friday, is a case in point.

“‘If the global economy has struggled out of the frying pan of the credit crunch, it seems destined to fall into the fire of high inflation … High inflation is cruel to the owner of financial assets,' said Tim Bond, head of global asset allocation at Barclays Capital.

“‘Equity markets will rally for a limited period of time on belief that weakness in earnings will be short-lived. Moving into next year, you will see markets come off on the inflation story. Investors who see some of the rise in earnings being driven by inflation generally take the view that's not sustainable.'”

Source: Natsuko Waki, Reuters , April 25, 2008.

Click Here for Part 2 of Words from the (investment) wise

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2008 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.