No More Rocking the Boat in Stocks But Gold?

Commodities / Gold and Silver 2021 Mar 13, 2021 - 05:04 PM GMTBy: Submissions

Stocks sharply reversed intraday, and closed just where they opened the prior Friday. That indicates quite some pressures, quite some searching for direction in this correction that isn‘t over just yet. Stocks have had a great run over the past 4 months, getting a bit ahead of themselves in some aspects such as valuations. Then, grappling with the rising long-term rates did strike.

So did inflation fears, especially when looking at commodities. Inflation expectations are rising, but not galloping yet. What to make of the rising rates then? They‘re up for all the good reasons – the economy is growing strongly after the Q4 corona restrictions (I actually expect not the conservative 5% Q1 GDP growth, but over 8% at least) while inflation expectations are lagging behind.

In other words, the reflation (of economic growth) is working and hasn‘t turned into inflation (rising or roughly stable inflation expectations while the economy‘s growth is slowing down). We‘re more than a few quarters from that – I fully expect really biting inflation (supported by overheating in the job market) to be an 2022-3 affair. As regards S&P 500 sectors, would you really expect financials and energy do as greatly as they do if the prospects were darkening?

So, I am looking for stocks to do rather well as they are absorbing the rising nominal rates. It‘s also about the pace of such move, which has been extraordinary, and left long-term Treasuries trading historically very extended compared to their 50-day moving averages. Thus, they‘re prone to a quick snapback rally over the next 1-2 weeks, which would help the S&P 500 regain even stronger footing. And even plain temporary stabilization of theirs would do the trick.

This is taking me directly to gold. We have good odds of long-term rates not pressuring the yellow metal as much as recently, and inflation expectations are also rising (not as well anchored to 2% as the Fed thinks / says). As I‘ll show you in the charts, the signs of decoupling have been already visible for some time, and now became more apparent. And that‘s far from the only suggestion of an upcoming gold upswing that I‘ll bring you today.

Just as I was calling out gold as overheated in Aug 2020 and prone to a real soft patch, some signs of internal strength in the precious metals sector were present this Feb already. And now as we have been testing for quite a few days the first support in my game plan, we‘re getting once again close to a bullish formation that I called precisely to a day, and had been banging the bearish gold drum for the following two days, anticipating the downside that followed. Now, that‘s what I call welcome flexibility, extending to accentuated, numerous portfolio calls.

And the permabears keep (losing capital through many bullish years in a row in some cases) calling for hundreds bucks more downside after a respite now, not even entertaining the thought that gold bottom might very well not be quarters ahead. It‘s easier to try falsely project own perma stickers onto others. Beware of wolves in ill-fitting sheep clothing. Look at full, proven track records, compare varying perspectives of yesteryear too, and wave off cheap halo effects.

It‘s the above dynamic between nominal rates taking a breather, dollar getting back under pressure, commodities continuing their rise and stocks gradually resuming theirs – see the ebbing and flowing that I‘m laying down in the daily analyses on the revamped homepage, and you‘ll get a knack for my timings of local tops or bottoms just the way I did in the early Sep buying climax or in the corona crash.

True mastery is in integrating and arguing opposing views with experience and adaptability daily. People are thankfully able to recognize these characteristics on their own – and they have memory too. Who needs to be told what to read and consider by those embracing expertise only to turn against it when the fruits were no longer theirs? Sour grapes. Narrow thinking is one of the dangers of our era replete with empty and shallow shortcuts. Curiosity, ingenuity and diligence are a gift to power mankind – and what you get from financial analysts – forward in a virtuous circle.

If gold prices rise from here, they have bounced off support. Simple as that, especially given the accompanying signs presented. There is time to run with the herd, and against the herd – in both bull and bear trends, constantly reevaluating the rationale for a position, unafraid to turn on a dime when justified.

Whatever else bullish or bearish I see technically and fundamentally in rates, inflation and dollar among much else, I‘ll be duly reporting and commenting on as always. It‘s the markets‘ discounting mechanism of the future that counts – just as gold cleared the deflationary corona crash in psring 2020, just as it disregarded the tough Fed tone of 2H 2018, just as it sprang vigorously higher in early 2016 stunning bears in all three cases with sharp losses over many months, or just as stocks stopped declining well before economic news got better in April 2020 or March 2009.

Make no mistake, the markets consider transitioning to a higher inflation environment already now (the Fed timidly says that reopening will spike it, well, temporarily they say), when inflation expectations are still relatively low, yet peeking higher based on the Fed‘s own data. Such were my Friday‘s words:

(…) Let‘s keep the big picture – gold is in a secular bull market that started in 2018 (if not in late 2015), and what we‘re seeing since the Aug 2020 top, is the soft patch I called. The name of the game now, is where the downside stops – I am not capitulating to (hundreds dollars) lower numbers below $1,650 on a sustainable basis. The new precious metals upleg is a question of time even though the waiting is getting longer than comfortable for many, including myself.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

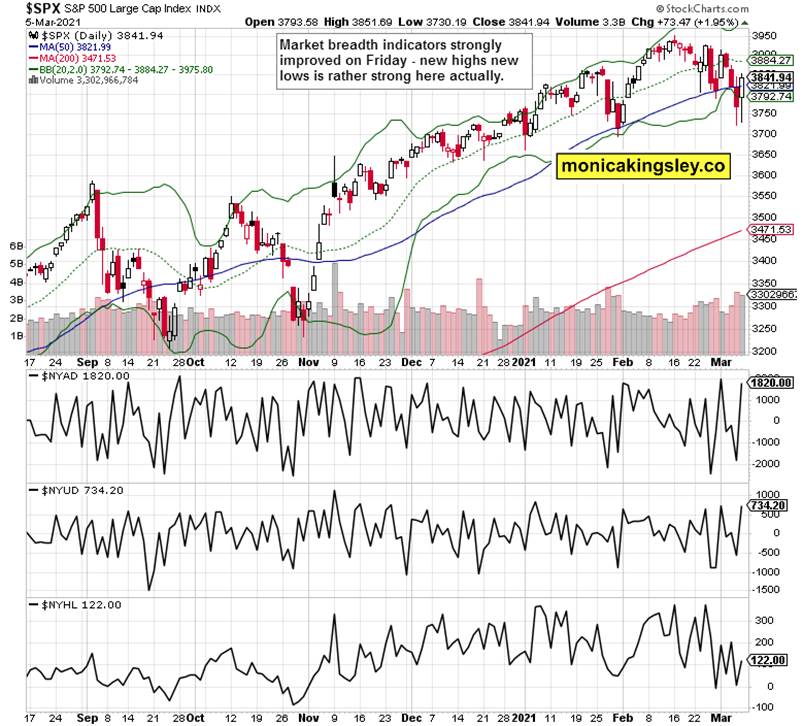

S&P 500 Outlook and Its Internals

Strong rebound after more downside was rejected, creating a tweezers bottom formation, with long lower knots. This is suggestive of most of the downside being already in. The Feb 25 upswing had a bearish flavor to it, while the Mar 1 one looked more constructive – and Friday‘s one is from the latter category. That doesn‘t mean though this correction won‘t be in the 5% range. The 3,900 zone is critical for the bulls to pass so as to clear the current precarious almost no man‘s land.

The market breadth indicators are actually quite resilient given how far this correction has reached. New highs new lows are holding up still very well, yet they too indicate that this correction has further to go in time. While the bullish percent index still remains in the bullish territory, it indicates how far the correction has progressed technically, and that we can‘t declare the bullish spirits as having returned just yet.

Credit Markets

High yield corporate bonds (HYG ETF) ilustrate this fragility for they haven‘t rebounded as strongly as stocks. This correction doesn‘t appear to be as really over just yet, also given the sectoral picture that I am showing you next.

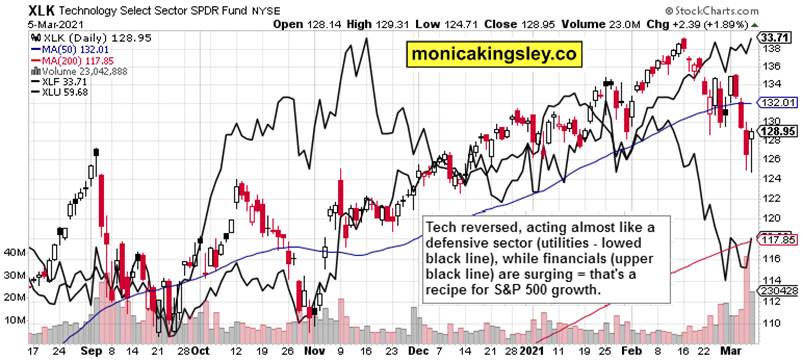

S&P 500 Sectoral Look

Tech reversed, but higher volume would be welcome to lend the move more credibility. This sector is still the weakest link in the whole S&P 500 rebound, and not until I see the $NYFANG carve out a sustainable bottom (this needn‘t happen at the 200-day moving average really), I can declare this correction as getting close to over.

The bullish take on the volume is that the value sector has undergone strong accumulation, as can be readily seen in the equal weight S&P 500 index (RSP ETF). The above chart shows that cyclicals are performing strongly – with industrials (XLI ETF) and energy (XLE ETF) leading the charge as the tech and defensives are trying to stabilize, and the same is true about consumer discretionaries (XLY ETF).

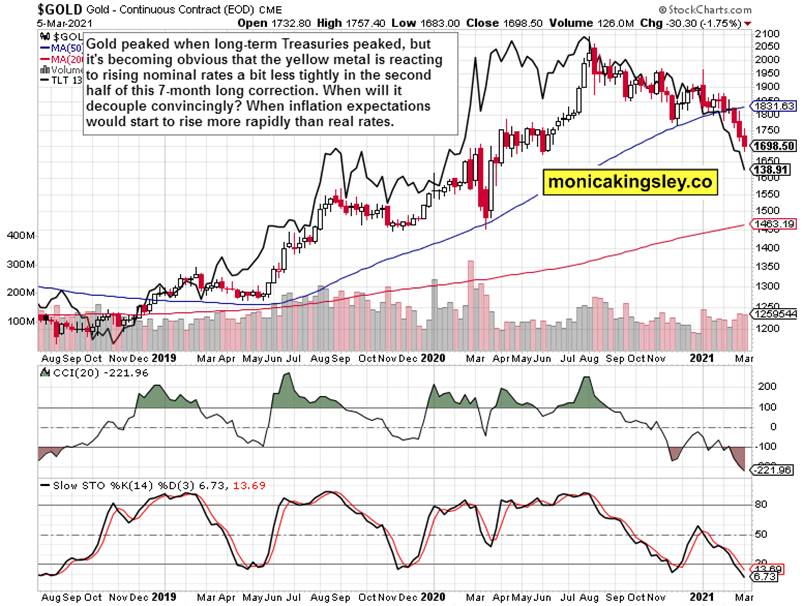

Gold‘s Big Picture View

Gold‘s weekly chart shows two different stages in the reaction to rising long-term rates. The first half was characterized by the two tracking each other rather closely, yet since late Dec, the nominal rates pressure has been abating in strength within the mutual relationship. While TLT plunged, gold didn‘t move down as strongly.

Real rates are negative, nominal rates rose fast, and inflation expectations have been trending higher painfully slowly, not reflecting the jump in commodities or the key inflation precursor (food price inflation) just yet – these are the factors pressuring gold as the Fed‘s brinkmanship on inflation goes on.

Once the Fed moves to bring long-term rates under control through intervention – hello yield curve control or at least twist – then real rates would would be pressured to drop, which would be a lifeline for gold – the real questions now are how far gold is willing to drop before that, and when that Fed move would happen. Needless to add as a side note regarding the still very good economic growth (the expansion is still young), staglation is what gold would really love.

Copper and Silver Big Picture View

The red metal keeps rising without end in sight, reflecting both the economic recovery and monetary intervention. This is a very bullish chart with strong implications for other commodities and silver too. That‘s the essence of my favorite play in the precious metals – long silver short gold spread, clearly spelled out as more promising than waiting for gold upswing to arrive while the yellow metals‘ bullish signs have been appearing through Feb only to disappear, reappear, and so on.

As you can see, silver performance approximates commodity performance better than gold one. And as the economic recovery goes on, it‘s indeed safer to be a silver bull than a gold bull – another of my early Feb utterances.

Miners to Gold Big Picture View

This gold sectoral ratio made an encouraging rebound last week, but isn‘t internally as strong as it might appear, because the juniors (GDXJ ETF) aren‘t yet outperforming the seniors (GDX ETF), which had been the case in early 2021 and late in Feb as well – right till I sounded the alarm bells on Feb 23-24. This is precisely why I was not bullish in tone at all in the past week, as gold hadn‘t been acting as strongly now as it had been right before the Feb 22 upswing that I called. And I am missing this ingredient at the moment still.

Summary

Stock bulls stepped in and repaired much of Thursday‘s damage, flipping the balance of power as more even at the moment. While the medium-term factors favor the bulls, this correction is slated to go on still for longer, as all eyes are on tech (big names) as the deciding sector.

Gold still remains acting weak around the lower border of its support zone, silver is refusing to decline more, and signs overall favoring a rebound, are appearing. It‘s still a mixed bag though, with especially gold being far from out of the woods yet.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for both Stock Trading Signals and Gold Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

www.monicakingsley.co

mk@monicakingsley.co

* * * * *

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.