Is the U.S. Dollar Heading For a Mighty Crash?

Currencies / US Dollar May 21, 2009 - 02:16 AM GMTBy: Gary_Dorsch

Each month, the US Treasury publishes its International Capital account, (TIC) which foreign currency traders and bond dealers use to gauge the flows of money from around the world, into and out-of the US-capital markets. The demand for a nation’s bonds and stocks, combined with international trade flows for goods and services, plus behind the scenes intervention by central banks, all act in concert to influence the foreign exchange market which handles $4-trillion per day.

Each month, the US Treasury publishes its International Capital account, (TIC) which foreign currency traders and bond dealers use to gauge the flows of money from around the world, into and out-of the US-capital markets. The demand for a nation’s bonds and stocks, combined with international trade flows for goods and services, plus behind the scenes intervention by central banks, all act in concert to influence the foreign exchange market which handles $4-trillion per day.

A surplus in TIC inflows is generally seen as a positive for the US-dollar, because it signals that foreigners are willing to increase their holdings of US-securities, displaying greater confidence in the currency. On the other hand, a TIC deficit is generally interpreted as bearish for the US-dollar, because it means that foreign inflows into the US aren’t sufficient enough to fund government borrowing.

The release of the TIC report often sparks a flurry of trading activity in the foreign exchange market, due to speculators seeking to earn a fast profit. However, the initial knee-jerk reaction to the news headlines, can be very misleading, and often isn’t long-lasting. For instance, the US-Dollar Index, measured against a basket of six-currencies, defied conventional logic in February, by climbing +2.7% higher, even in the face of a net outflow of $91-billion in the TIC account.

Instead, large off-shore traders are influencing exchange rates, and their betting patterns are difficult to discern on the G-20’s radar screens. The finance ministers of the “Group-of-20” (G-20) recognize the growing threat to their control over the currency markets, and are calling for increased regulation of hedge-funds and shadow-bankers, insisting on full disclosure of their locations and other information to assess the risks they pose to the manipulations of the major central banks.

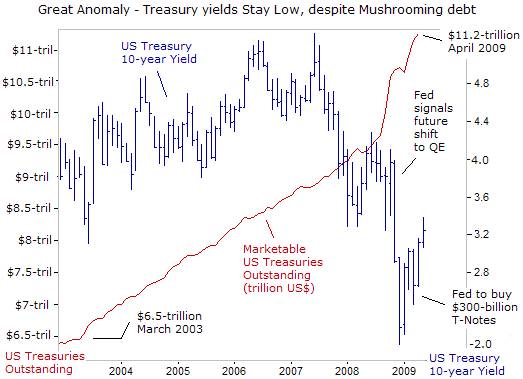

The United States is dangerously reliant upon the whims of foreign investors, to help finance its $2-trillion budget deficit this year, and prevent a surge in long-term interest rates, which could have a devastating impact on the US-economy. If bond or currency traders detect that big investors in US-government bonds, - such as China, Japan, OPEC, Russia, and Brazil, have ceased to buy US Treasury debt, or worse yet, are becoming net sellers, it could spark a sharp slide in US-Treasury notes, sending yields sharply higher, and ignite a free-fall in the US-dollar.

The United States is dangerously reliant upon the whims of foreign investors, to help finance its $2-trillion budget deficit this year, and prevent a surge in long-term interest rates, which could have a devastating impact on the US-economy. If bond or currency traders detect that big investors in US-government bonds, - such as China, Japan, OPEC, Russia, and Brazil, have ceased to buy US Treasury debt, or worse yet, are becoming net sellers, it could spark a sharp slide in US-Treasury notes, sending yields sharply higher, and ignite a free-fall in the US-dollar.

Last week, the US Treasury tried to reassure bond and currency traders, that foreign investors haven’t abandoned the American debt markets, despite the avalanche of new debt that is swamping the market. The US Treasury claims that China and Japan were net buyers of a combined $48.5-billion of Treasuries in March, and that Moscow was a net buyer of $8.3-billion. Yet the reliability and accuracy of the TIC report should be viewed with a grain of salt, and a healthy dose of suspicion, - perhaps, the figures were conjured-up under the guise of “mark-to-make-believe” accounting.

White House economic adviser Lawrence Summers defended the size of the US Treasury debt outstanding, reaching $11.2-trillion in April, saying US-dollar holders would suffer much more if full-scale deflation sets in and the US-economy collapses. A Treasury spokeswoman declared, “The US Treasury market remains the deepest and most liquid market in the world.” White House spin-artist Robert Gibbs added, “There’s no safer investment in the world than in the United States.”

But President Barack Obama’s stimulus program could have a destabilizing effect on the US-economy. No one is asking who will purchase the $1-trillion of US Treasuries to be offered to the market by September. Once that colossal amount of paper is bought, who will purchase another $5-trillion of Treasury paper over the next four-years, as the US-government plunges deeper into insolvency. The Federal Reserve would be forced to print (monetize) vast quantities of US-dollars to pay the principal and interest on the national debt that is not covered by tax revenue.

The US-dollar’s surprising strength since last July was largely attributed to “de-leveraging” and “risk-aversion,” which are references to the unwinding of “carry trades,” in the foreign exchange market. On April 6th, famed hedge-fund trader George Soros remarked, “The US-dollar is not strong because people want to hold the dollar, but it’s strong because people have debt in dollars.”

The enormous fortunes of Wall Street’s aristocracy were built-up on the leveraging of debt, including “carry-trades,” in order to buy exotic securities built around sub-prime mortgages, and other instruments of financial speculation. But when the global commodity and stock markets began to meltdown following the collapse of Lehman Brothers, carry-traders began massive de-leveraging, - the selling risky assets and buying US-dollars and Japanese-yen, to pay-down margin loans.

There was also a stunning contraction in the US-trade deficit, narrowing from $62.5-billion in August to $26-billion in February, its lowest level in nine-years, bolstering the greenback. The US current account deficit, which had increased for five straight years, fell to $673-billion in 2008 from $731-billion in 2007. The deficit equaled 4.7% of the overall US-economy last year, down from 5.3% in 2007.

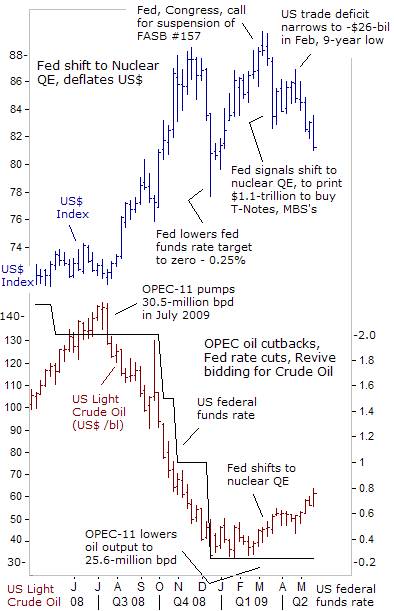

But the US-dollar’s “risk-aversion” rally came to an abrupt end on March 18th, when the Federal Reserve shocked the markets by announcing that it would unleash its nuclear weapon, - “Quantitative Easing,” (QE) by printing $1.1-trillion US-dollars off its electronic printing press, to monetize US T-Notes and mortgage backed securities, in an all-out effort to prevent a deflationary spiral in the US-economy, which in turn, could lead to widespread defaults on debt and bankruptcies.

By pumping vast quantities of US-dollars into the global money markets, - easily outstripping the money printing operations in England, the Euro-zone, Japan, and Switzerland, the Fed has headed-off the prospect of deflation. Instead, the Fed has reawakened the “Commodity Super Cycle,” led by the kingpin crude-oil market, which if feeding-off a weaker dollar, and ultra-low interest rates worldwide, climbing above $62 per barrel today, from as low as $35 in January.

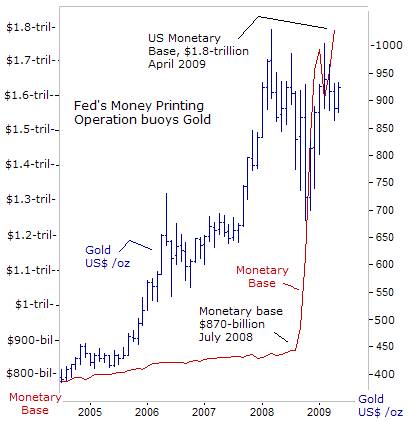

The Fed has pumped $1-trillion into the banking system since July, increasing the monetary base to a record $1.87-trillion, while pegging the fed funds rate near zero-percent. Super-easy money, beloved by Fed chief Ben “Bubbles” Bernanke, US Treasury chief Tim “Turbo-tax” Geithner, corrupt Washington politicians and Wall Street Oligarchs, is a traditional recipe for an asset bubble. While the rapid expansion of the US-monetary base is buoying the gold market above $900 /oz, other G-20 central banks are also letting the inflation-genie out of its bottle, providing the yellow metal with a huge advantage over government toilet paper.

The Fed has pumped $1-trillion into the banking system since July, increasing the monetary base to a record $1.87-trillion, while pegging the fed funds rate near zero-percent. Super-easy money, beloved by Fed chief Ben “Bubbles” Bernanke, US Treasury chief Tim “Turbo-tax” Geithner, corrupt Washington politicians and Wall Street Oligarchs, is a traditional recipe for an asset bubble. While the rapid expansion of the US-monetary base is buoying the gold market above $900 /oz, other G-20 central banks are also letting the inflation-genie out of its bottle, providing the yellow metal with a huge advantage over government toilet paper.

“Our actions have succeeded in pulling the financial markets and the economy from the edge of the abyss, beating back deflationary pressures, and set the stage for a recovery,” declared Dallas Fed chief Richard Fisher on April 15th. Fisher argues the US-economy’s low capacity utilization rate, near 69%, would keep inflationary pressures under wraps. “It is doubtful that inflation will raise its ugly head until employment picks-up and capacity utilization tightens,” he said.

Higher inflation down the road means the Fed must at some point, break its addiction to easy-money, and dismantle the QE framework, which has flooded the money markets with hundreds of billions of dollars. “Nobody I know on the FOMC wants to maintain our current posture for any longer and to any greater degree than is minimally necessary to restore the efficacy of the credit markets and buttress economic recovery without inflationary consequences,” Fisher said.

The FOMC “can ill afford to be perceived as monetizing that debt, lest we come to be viewed as an agent of inflation, rather than an independent guardian against future inflation,” the Fed’s propaganda artist said. Typically however, Fed officials continue to keep the printing presses rolling at full-speed, long after inflation has already reared its ugly head, and hyper-inflationary psychology becomes deeply embedded within the minds of commodity traders and the public at large.

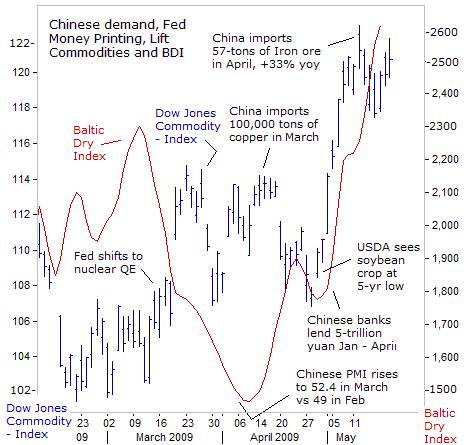

Already, “green-shoots” of inflation are sprouting forth in the commodities market. Base metals, energy, grains, and fertilizer are charging higher, spurred along by China’s great sucking sound, as Beijing pursues a major effort to stockpile raw materials, with prices hovering near multi-year lows. Beijing is spending 4-trillion yuan on infrastructure, to bring its roads, ports, airports, power-generation capacity and other infrastructure systems up to speed.

The Baltic Dry Index, a measure of shipping costs for commodities, rose to a seven-month high of 2,645, in London on strong Chinese demand for iron ore, coal, and grains. Crude oil rose above $60 a barrel after China increased crude imports by 14% in April to 3.9-million barrels a day. Soybeans rose to $11.65 /bushel, as US-stockpiles are dwindling to a five-year low of 130-million bushels, the USDA said.

China imported 57-tons of iron-ore in April, up +33% from a year ago, setting a record for a third month. China’s State Reserves Bureau SRB may have imported 300,000-tons of refined copper in the first quarter of this year. Most base metals will experience “severe” supply constraints in coming years as a lack of investment and exploration prevents miners from meeting demand when the global economy recovers, Ernst & Young warned on May 12th. “When that happens, expect metal prices to set new record highs.”

In this case, the revival of the “Commodity Super Cycle,” is also getting charged-up by Beijing’s printing press, where the ruling elite are expanding the Chinese M2 money supply at a blistering +26% annualized clip, far above the +14.8% rate seen last November. Chinese banks have extended 5.2-trillion yuan ($750-billion) of new loans in the first four-months of this year, and much of the freshly printed yuan has been funneled into the Shanghai stock market.

“Significant changes in the growth rate of money supply, even small ones, impact the financial markets first. Then, they impact changes in the real economy, usually in six to nine-months, but in a range of three to 18-months. The leads are long and variable, though the more inflation a society has experienced, history shows, the shorter the time lead will be between a change in money supply growth and the subsequent change in inflation,” according to the late economist Milton Friedman.

Capitalizing on the still privileged position of the US dollar, the American ruling class is funding bailouts of the Wall Street Oligarchs through the sale of massive volumes of debt on world markets. The Fed’s policy of printing vast quantities of money, in part to finance the Treasury’s debt has an inflationary lag-effect that has generated an extremely nervous reaction from other powers, most noticeably China, which has over $1 trillion in dollar-denominated bonds. These assets would plunge in value in the event of a major upswing in inflationary pressures.

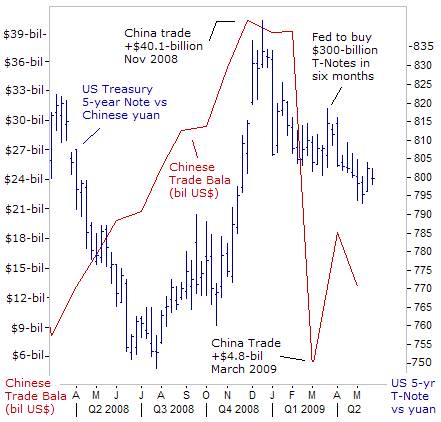

The latest TIC report claims that China, the largest holder of US-Treasury securities, increased its holdings of US-Treasury bonds by $23.7-billion in the month of March to a record $767.9-billion. Yet the US-Treasury’s figures are at odds with stark warnings issued by top Chinese monetary officials on March 25th. Zhou Xiaochuan, chief of the Chinese central bank is calling for a new international currency to replace the US-dollar. Li Xiangyang of the government-backed Chinese Academy of Social Sciences called the Fed’s radical QE policy “irresponsible,” and asked for “specific measures on the part of the US to insure the value of Chinese holdings.”

Earlier, on March 13th, Chinese Premier Wen Jiabao held a news conference to send a blunt message to Washington. “We have lent a massive amount of capital to the United States. Of course we are concerned about the safety of our assets. To be honest, I am a little bit worried,” said Wen. Furthermore, China’s trade surpluses are shrinking compared with a year ago, less than half compared with a year ago, leaving Beijing with fewer dollars to re-invest in the Treasury market.

It’s a vast stretch of imagination to believe the TIC reports are accurate, and not the configurations of “mark-to-make-believe” accounting. Yet China is caught in a bind. If it tries to lighten-up on its US-bond portfolio, it could trigger a global stampede to dump US-debt securities and shoot itself in the foot. Still, it’s highly possible that the US-Treasury is doctoring-up the TIC data, in order to prevent an imminent collapse of the debt bubble, which could send interest rates sharply higher.

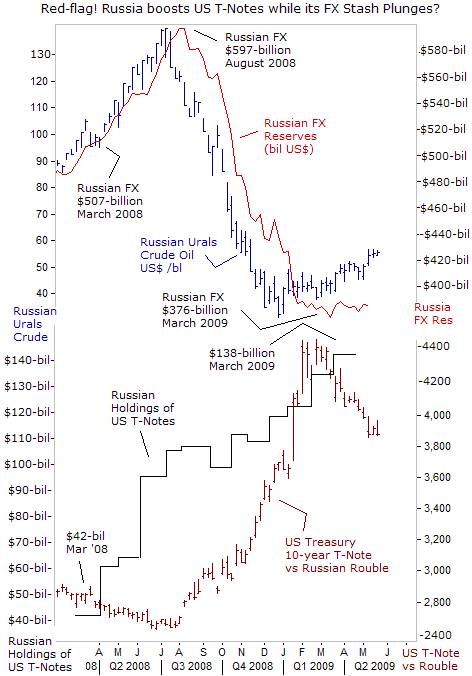

Very few analysts, if any at all, have questioned the accuracy of the TIC data. The most glaring red-flag is the US Treasury’s claim that the Kremlin boosted it holdings of US Treasury debt by $30-billion from August 2008, until March 2009, to a record $138-billion. Yet over the same time span, the Kremlin sold $221-billion US-dollars from its foreign currency stash, in a heroic defense of the Russian rouble from the whims of speculators, and massive capital flight from the Russian markets.

Furthermore, the US-dollar's share of Russia’s FX stash fell to 41.5% from 47.0 last year, according to Bank Rossii. Russia, along with China, has raised the idea of replacing the US-dollar as global reserve currency, as the Fed tries to massively inflate its way out of the recession and bailout Wall Street Oligarchs. By any stretch of the imagination, it’s impossible to believe the accuracy of the US Treasury’s TIC report, claiming that Moscow increased its exposure to US-bonds.

Brazil and China are working towards directly exchanging their own currencies in trade transactions rather than using the US-dollar as an intermediary, according to Brazil’s central bank and aides to Luiz Inácio Lula da Silva, Brazil’s president. “What we are talking about now is Brazil paying for Chinese goods with reals and China paying for Brazilian goods with renminbi.” The move follows other challenges by Beijing to the status of the dollar as the world’s leading reserve currency, such as currency swaps with Argentina and Indonesia.

The other key players in the US-dollar, the Arab oil kingdoms, are sticking with their archaic dollar pegs, and still demanding US-dollars in exchange for their oil. No wonder US-president Barack Obama decided to bow before Saudi king Abdullah on April 2nd, at the G-20 meeting in London, - a friendly gesture, but also sending an ominous signal of the US-dollar’s precarious position.

On May 20th, Iranian president Mahmoud Ahmadinejad said his army tested a missile that could hit Israel and US-military bases in the Persian Gulf; coming a day after Iran’s supreme leader the Ayatollah Khamenei accused the Americans of promoting terrorism. “The Sejil-2 missile, which has an advanced technology, was launched today, and it landed exactly on target,” Ahmadinejad said. That target was the crude oil pits in London and New York, - lifting Iran’s foreign exchange income, and the value of its gold reserves in one quick-blow.

Defense Minister Mostafa Mohammad Najjar said Sejil has “great destructive power” and that mass production of the missile had started, rattling the nerves of the neighboring Arab oil monarchies. The Obama team was unmoved however, - and still seeks “vigorous” diplomacy with Tehran’s mullahs.

This article is just the Tip-of-the-Iceberg of what's available in the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2009 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.