Bill Gross Say FED Will Exit Easy Monetary Policy, Quantitative Easing in March 2010

Interest-Rates / US Interest Rates Jan 10, 2010 - 10:37 AM GMTBy: G_Abraham

The latest PIMCO newsletter suggests that 2010 will be year of caution and change. And yet he gives ample suggestions to the coming holocaust in financial markets if things do not go as planned.

The latest PIMCO newsletter suggests that 2010 will be year of caution and change. And yet he gives ample suggestions to the coming holocaust in financial markets if things do not go as planned.

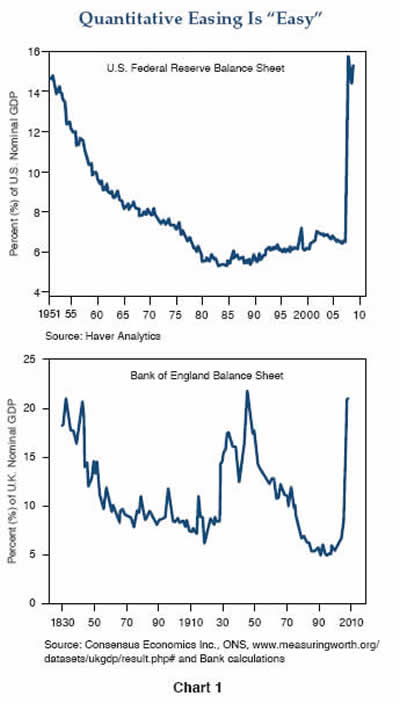

The latest US and UK deficit is graph straight for the records. It is almost eclipsing the vertical rise of equity markets in 2009.

What amazes me most of all is that politicians can be bought so cheaply. Public records show that combined labor, insurance, big pharma and related corporate interests spent just under $500 million last year on healthcare lobbying (not much of which went to politicians) for what is likely to be a $50-100 billion annual return. The fact is that American citizens have never been as divorced from their representatives – and if that description fits the Democratic Congress now in control – then it applies to Republicans as well – past and present. So you watch Fox, or is it MSNBC? O’Reilly or Olbermann? It doesn’t matter. You’re just being conned into rooting for a team that basically runs the same plays called by lookalike coaches on different sidelines. A “ballot box” pox on all their houses – Senators, Representatives and Presidents alike.

There has been no change, there will be no change, until we the American people decide to publicly finance all national and local elections and ban the writing of even a $1 check for our favorite candidates. Undemocratic? Hardly. Get on the internet, use Facebook, YouTube, or Twitter to campaign for your choice. That’s the new democracy. When special interests, even singular citizens write a check, it represents a perversion of democracy not the exercise of the First Amendment. Any chance that any of this will happen? Not one ghost of a chance. Forward Don Quixote, the windmills are in sight.

What amazes me most of all is that politicians can be bought so cheaply

Gross once again underscores his point, that 2010 will be a year to sell US and UK bonds. While FED is counting on private institutions to take up the cheque once the stimulus fades in March, here is the largest bond market maker, shaking off any dreams that FED might be harboring.

He makes quite an astute comparison to passengers having a choice in flying any airline in 2009 and gladly chose “United” in 2009. That may no longer be the case in 2010.

Distressed as I am about the state of American democracy, a rational money manager cannot afford to get mad or “just get even” when it comes to investing clients’ money. Still, like pilots politely advertise at the end of most flights, “We know you have a choice of airlines and we thank you for flying ‘United’.” Global investment managers likewise have a choice of sovereign credits and risk assets where stable inflation and fiscal conservatism are available.

When a man like Gross begins to say “distressed about american economy…”, it should awaken the sleepiest bear out there and start flexing.

If 2008 was the year of financial crisis and 2009 the year of healing via monetary and fiscal stimulus packages, then 2010 appears likely to be the year of “exit strategies,” during which investors should consider economic fundamentals and asset markets that will soon be priced in a world less dominated by the government sector. If, in 2009, PIMCO recommended shaking hands with the government, we now ponder “which” government, and caution that the days of carefree check writing leading to debt issuance without limit or interest rate consequences may be numbered for all countries.

When someone as well connected as Gross sticks his neck out and suggests that March could be the beginning of the end for US easy monetary policy, one should sit back and definetly take note. Interestingly, the qualification added by using the word “attempted” next to “exit” suggests that Gross thinks that the Fed may be making a misjudgment which will then need to be reversed with a new policy of more accommodation.

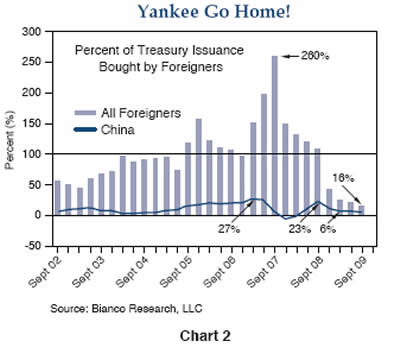

Here’s the problem that the U.S. Fed’s “exit” poses in simple English: Our fiscal 2009 deficit totaled nearly 12% of GDP and required over $1.5 trillion of new debt to finance it. The Chinese bought a little ($100 billion) of that, other sovereign wealth funds bought some more, but as shown in Chart 2, foreign investors as a group bought only 20% of the total – perhaps $300 billion or so. The balance over the past 12 months was substantially purchased by the Federal Reserve. Of course they purchased more 30-year Agency mortgages than Treasuries, but PIMCO and others sold them those mortgages and bought – you guessed it – Treasuries with the proceeds. The conclusion of this fairytale is that the government got to run up a 1.5 trillion dollar deficit, didn’t have to sell much of it to private investors, and lived happily ever – ever – well, not ever after, but certainly in 2009.

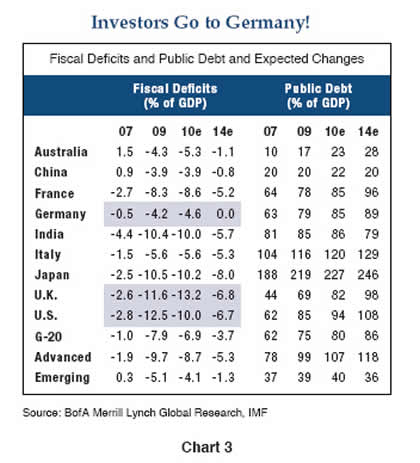

Now, however, the Fed tells us that they’re “fed up,” or that they think the economy is strong enough for them to gracefully “exit,” or that they’re confident that private investors are capable of absorbing the balance. Not likely. Various studies by the IMF, the Fed itself, and one in particular by Thomas Laubach, a former Fed economist, suggest that increases in budget deficits ultimately have interest rate consequences and that those countries with the highest current and projected deficits as a percentage of GDP will suffer the highest increases – perhaps as much as 25 basis points per 1% increase in projected deficits five years forward. If that calculation is anywhere close to reality, investors can guesstimate the potential consequences by using impartial IMF projections for major G7 country deficits as shown in Chart 3

Gross is quite sure that FED is making a mistake in exiting the stimulus in March and uses Thomas Laubach studies to validate that. Bill then goes on to explain that if so were the case then rates in US,UK and Japan will start to tick up, maybe by 100 bps. It may already have started if you watch the yield curve.

Using 2007 as a starting point and 2014 as a near-term destination, the IMF numbers show that the U.S., Japan, and U.K. will experience “structural” deficit increases of 4-5% of GDP over that period of time, whereas Germany will move in the other direction. Germany, in fact, has just passed a constitutional amendment mandating budget balance by 2016. If these trends persist, the simple conclusion is that interest rates will rise on a relative basis in the U.S., U.K., and Japan compared to Germany over the next several years and that the increase could approximate 100 basis points or more. Some of those increases may already have started to show up – the last few months alone have witnessed 50 basis points of differential between German Bunds and U.S. Treasuries/U.K. Gilts, but there is likely more to come.

The problem is that if we backdate the Thomas technique and look back 5 years from 2007, then rates should be closer to 7% today. It may not be entirely correct to relate deficit and rate hikes as there far more pressing variables that affect rate matters.

Gross while has dealt quite at length with almost all facets of the economy, he seems to have ignored inflation and how different governments react to the fear of price rise. On thing is for sure, EURO zone will raise rates even if they do not need to, as they will target inflation once if goes beyond their prescribed 2% range. There is normally very little negotiations about eurozone way of working when it comes to rate hikes. There fore Gross might just be wrong when he says German bunds yields will tick down.

But am completely with Bill Gross, that FED will make an “attempted” exit and it will fail miserably towards October which is when we should expect the next major mega crisis. I like to call it the currency crisis and more or less dwarfs all the previous crisis put together. It is the kind of upheaval in currency markets which will shut down all forms of supply chains albeit for short period yet will be painful reminder on how global markets need to be balanced at some point.

Gross last section is a superb read. I like hi language as he leaves a lot unsaid and yet would have said everything that was needed to point the careful investor.

The fact is that investors, much like national citizens, need to be vigilant and there has been a decided lack of vigilance in recent years from both camps in the U.S. While we may not have much of a vote between political parties, in the investment world we do have a choice of airlines and some of those national planes may have elevated their bond and other asset markets on the wings of central bank check writing over the past 12 months. Downdrafts and discipline lie ahead for governments and investor portfolios alike. While my own Pollyannish advocacy of “check-free” elections may be quixotic, the shifting of private investment dollars to more fiscally responsible government bond markets may make for a very real outcome in 2010 and beyond.

Additionally, if exit strategies proceed as planned, all U.S. and U.K. asset markets may suffer from the absence of the near $2 trillion of government checks written in 2009. It seems no coincidence that stocks, high yield bonds, and other risk assets have thrived since early March, just as this “juice” was being squeezed into financial markets. If so, then most “carry” trades in credit, duration, and currency space may be at risk in the first half of 2010 as the markets readjust to the absence of their “sugar daddy.” There’s no tellin’ where the money went? Not exactly, but it’s left a suspicious trail. Market returns may not be “so fine” in 2010.

If ever there was a doubt about who bought S&P and supported it from March through December in one of worst economic crisis, that should have been removed after reading Bill Gross.

Source: http://investingcontrarian.com/?p=2328

Wish you a great trading and investing week ahead

God Bless.

Godly Abraham

http://investingcontrarian.com/Formerly a hedge fund analyst for India's largest fund house and currently a Private Equity fund analyst with a swiss firm, Godly Abraham is an active writer at INVESTING CONTRARIAN which is a daily online publishing house, covering investing ideas and economic analysis on wide ranging topics but mainly specialized to covering US,UK, EU and BRIC countries and their political ramifications.

© 2010 Copyright Godly Abraham - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

{kind=link}

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.