U.S. October Employment Report Shows Economy is Slowly But Surely Retreating From the Cliff

Economics / Economic Recovery Nov 06, 2010 - 05:41 AM GMTBy: Asha_Bangalore

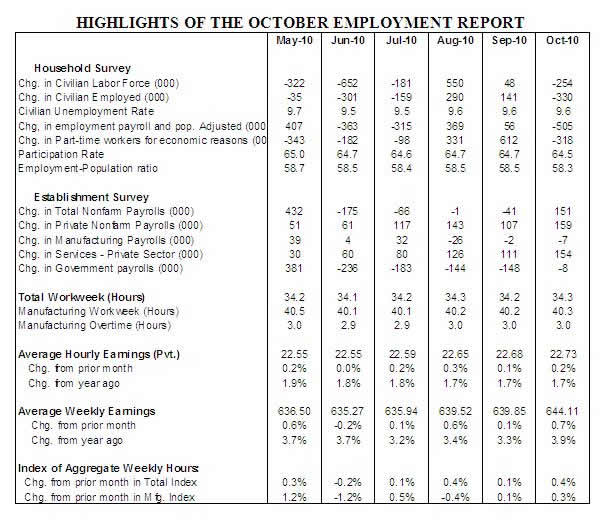

Civilian Unemployment Rate: 9.6% in October, virtually steady for five straight months. The unemployment rate was 5.0% in December 2007 when the recession commenced. Cycle high for recession is 10.1% in October 2009 and the cycle low (for the expansion that ended in December 2007) is 4.4% in March 2007.

Civilian Unemployment Rate: 9.6% in October, virtually steady for five straight months. The unemployment rate was 5.0% in December 2007 when the recession commenced. Cycle high for recession is 10.1% in October 2009 and the cycle low (for the expansion that ended in December 2007) is 4.4% in March 2007.

Payroll Employment: 151,000 in October vs. -41,000 in September. Private sector jobs increased 159,000 after a 107,000 increase in September. Net gain of 93,000 jobs after revisions of private sector payroll estimates for August and September.

Private Sector Hourly Earnings: $22.73 in October vs. $22.68 in September, 1.7% yoy increase in October matched the gain seen in September.

Household Survey - A note of clarification before moving on to detailed comments: The unemployment rate held steady at 9.6% in October, but nonfarm payrolls advanced 151,000. These headlines are from two different surveys and should be interpreted with care. The outcome of the household survey is the unemployment rate, participation rate, long-term unemployment, and so on. The establishment survey collects information about payrolls, hourly and weekly earnings, overtime hours, employment by sectors, and so on. The jobless rate is lagging indicator, while nonfarm payrolls are a coincident indicator; signals could be mixed in the early stages of a recovery on a month-to-month basis.

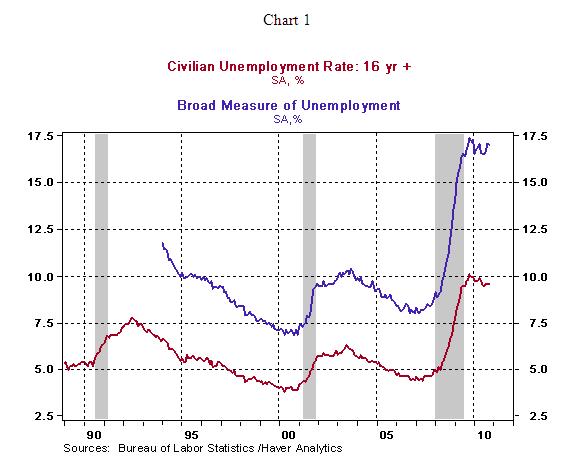

The steady unemployment rate came about because the labor force declined and hiring fell, thus offsetting both changes. The broader measure of unemployment ((including those working part-time because they cannot find full-time jobs and those not looking for work but want and are available in addition to those included in the tally of unemployed in the headline jobless rate) edged down to 17.0% from 17.1%.

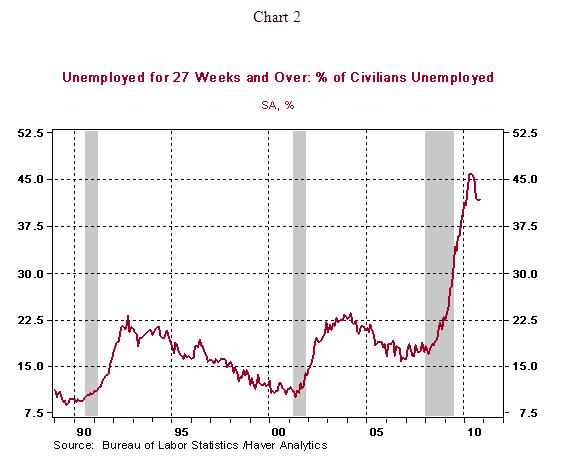

The percentage unemployed for six months and over moved up one notch to 41.8% in October. The elevated level of long-term unemployment remains problematic.

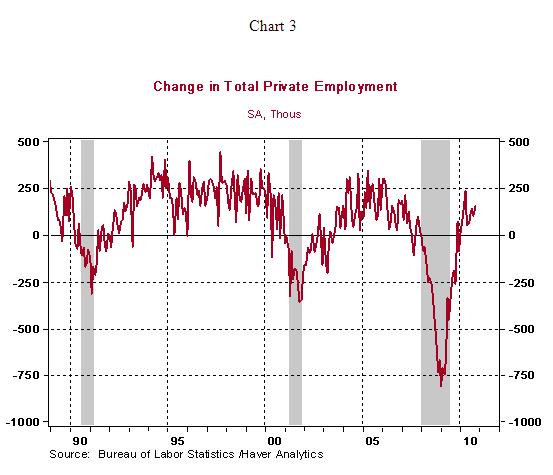

Establishment Survey - Total nonfarm payrolls increased 151,000 after a four-month stretch of declines reflecting losses of temporary Census-related government jobs. Private sector payrolls rose 159,000 in October, following upward revisions in each of the two prior months which resulted in a net gain of 93,000 jobs. Year-to-date, 1.115 million jobs have been added vs. a loss of 4.6 million jobs in the first ten months of 2009. On a year-to-year basis, private sector payrolls have risen 0.88% in October, the strongest reading since November 2007 (see chart 4)

There were widespread gains in jobs, with the 46,000 jump in the professional and business services component, 34,900 increase in temporary help, and 24,100 health care jobs at the top.

Highlights of changes in payrolls:

Construction: +5,000 vs. -8,000 in September

Manufacturing: -7,000 vs. -2,000 in September

Autos: +3,300 vs. -300 in September

Private sector service employment: +154,000 vs. +111,000 in September

Retail employment: +27,900 vs. +11,600 in September

Professional and business services:+46,000 vs. +19,000 in September

Temporary help: +34,900 vs. 23,800 in September

Financial activities: -1,000 vs. -2,000 in September

Health care employment: +24,100 vs. +22,800 in September

The average workweek was longer in October (34.3 hours) vs. September (34.2 hours), while the factory workweek also increased 0.1 hour to 40.3 hours and factory overtime held steady. Hourly earnings moved up 0.2% to $22.73, putting the year-to-year increase at 1.7%. Labor costs present no inflationary threat at the present time. The manufacturing man-hours index increased 0.3% in October vs. a 0.1% in September, which is indicative of an increase in industrial production in October. The earnings and payroll data point to a slightly more-than-moderate gain in personal income during October.

Conclusion - Details of the October employment report indicate that labor market conditions are showing signs of improvement. The gains reported in the October ISM survey results - manufacturing and non-manufacturing--and the increase in auto sales during October (12.26 million vs. 11.76 million in September) are consistent with the message from the October employment report. If this positive trend prevails in the months ahead, additional quantitative easing will not be necessary in the second-half of 2011. The nature of the October economic reports, along with the Fed's recently announced plan of quantitative easing, have reduced the probability of the economy posting significant weakness in the months ahead.

Asha Bangalore — Senior Vice President and Economist

http://www.northerntrust.com

Asha Bangalore is Vice President and Economist at The Northern Trust Company, Chicago. Prior to joining the bank in 1994, she was Consultant to savings and loan institutions and commercial banks at Financial & Economic Strategies Corporation, Chicago.

Copyright © 2010 Asha Bangalore

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.