Using Options To Hedge Against a Gold GLD ETF Collapse

Commodities / Gold and Silver 2012 Jan 06, 2012 - 01:43 AM GMTBy: Bob_Kirtley

At SK Options Trading, we primarily use the SPDR gold trust (Symbol: GLD) for exposure to the gold price. GLD is an exchange traded fund, designed to track the price of one tenth of an ounce of gold. GLD currently holds around 1280 tonnes of physical bullion, the sixth largest holding in the world, preceded only by the U.S. Germany, the IMF, Italy and France. The major benefit of using an ETF such as GLD is that one can gain exposure to the gold price as easily as buying a stock and one can effectively trade gold options as easily as trading stock options.

At SK Options Trading, we primarily use the SPDR gold trust (Symbol: GLD) for exposure to the gold price. GLD is an exchange traded fund, designed to track the price of one tenth of an ounce of gold. GLD currently holds around 1280 tonnes of physical bullion, the sixth largest holding in the world, preceded only by the U.S. Germany, the IMF, Italy and France. The major benefit of using an ETF such as GLD is that one can gain exposure to the gold price as easily as buying a stock and one can effectively trade gold options as easily as trading stock options.

However, some are concerned over the stability of GLD in the event of a run on the fund. This concern is mainly based on the following risks:

·Systemic risk: In the event of total financial collapse, will the trust fulfil the traders claim on their gold.

·Counterparty risk: Whether or not counterparties in a trade will fulfil their contractual obligations. Basically, the ability to exercise one’s claim on GLD for the physical gold.

·Accounting risk: Inconsistent accounting treatment of gold leading to possible “double counting” of reserves held, with multiple claims on that gold. Essentially, the gold you think you have purchased having other, higher priority claims on it. OR GLD lending out the gold they claim to have possession of.

The full explanation of these risks is tedious and prolonged, but the basic premise is that GLD could collapse if they didn’t hold the gold they claim to. GLD is allowed to lend out gold to third parties. Imagine if GLD lent a large quantity of gold to JPMorgan who then lent it out on various smaller deals. If JPMorgan were to collapse, and basically said we can’t find/gain possession of the gold we’ve lent out (and investors actually own), GLD would find itself up a creek without a paddle. Even if only half of their gold was lost, it is unlikely the share price would merely halve. Everyone would be dumping GLD shares under the cloud of uncertainty going forward. Irrespective of the intrinsic value of the gold they say they hold - if proven to be liars, all faith in the trust is gone. As the saying goes “there is never only one cockroach”.

We are still very comfortable using the GLD trust as our primary gold trading vehicle but as responsible traders and investors, it is our duty to consider all possible scenarios however unlikely they may appear to be.

We do not believe GLD will run into financial difficulty or liquidation at any stage – this is not to say it couldn’t happen, but our estimation is that the probability of this event is very low. The term for this type of event is often referred to as tail risk, defined as the price of a security moving 3 standard deviations or more from its current price. In other words, it would be a very rare event that has a very low chance of occurring.

If the price of gold dropped significantly, GLD would have a much lower book value (the value of its assets having plummeted) and like any business, simple or complex, liquidity becomes an issue and risk increases. Conversely, if the price of gold were to sky rocket in the event of a financial collapse, one must ponder the likelihood of their claim in GLD being honoured, whether by the custodians, sub custodians, government or even the trust itself, given that a financial collapse would have severe repercussions for the credit worthiness of such institutions.

There are various reasons for holding gold as a long term investment; whether they are using it as a hedge against inflation, devaluation of a currency or even protection against financial collapse. If one aims to profit from or hedge against a financial collapse from holding gold, holding physical is the most prudent decision. The chance of a GLD collapse or a situation arising in which one cannot access the gold they rightfully own (in GLD), significantly rises during a financial collapse. The end of a monetary system would likely leave a state of partial or even pure anarchy in the financial markets and the rules that once applied in a peaceful society no longer do. If it were every man for himself, it’s unlikely one would be able to get hold of the gold owned by an ETF such as GLD. SK Options Trading is a trading operation therefore does not hold positions for the long term, but if we aimed to hold gold in the anticipation of a possible financial collapse, it would be physical bullion and not an ETF such as GLD.

One way to possibly hedge against these risks is to use options as an insurance policy, for example by buying low strike, long dated puts on GLD. Buying a put to cover your long position is generally considered a hedge, however in this scenario we are fundamentally buying insurance by paying a small premium to protect against sizeable loss. A possible series of options that could fit this criterion are the March 2013 $80 puts. Currently the bid is $0.75 and the ask is $1.16. This is a very large spread, a result of poor liquidity and extremely low open interest in these contracts of only 432.

If GLD were to collapse, the holder of an out of the money put originally costing (approximately) $1 would see the value of their position rise by enormous amounts. 5000%+ returns are more than conceivable. Remember that GLD does not have to fall to the strike of the put for the insurance to pay off, there only has to be a significant drop.

Also remember an increase in volatility increases the value of an option, and the possible collapse of GLD is only going to send volatility one way; up.

Insurance of the aforementioned form is most useful to a holder of GLD shares, rather than your typical derivatives trader who may use more dynamic hedging strategies. For example a trader holding GLD calls doesn’t want to see a drop in the value of the GLD, but if a loss is unavoidable, they would more often than not be indifferent between a 10% and 100% drop in the price of GLD, since in either scenario, their position would have been obliterated. The biggest loss one such trader can suffer is the value of the original premium paid. However a holder of shares in GLD, using the index as their allocation of physical gold, is far more sensitive to a collapse.

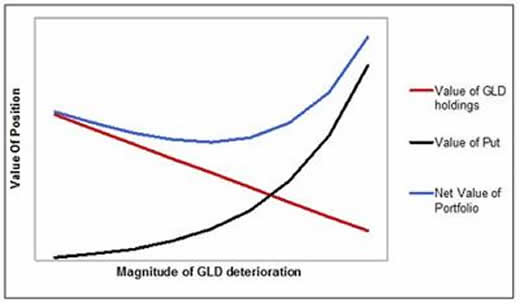

As an example, imagine investor X, a holder of 1000 shares in GLD (the equivalent of roughly 100 ounces). The current value (time of writing) of his holding is $155,230 ($155.23 per GLD share).

A 75% drop in value of GLD following news of a collapse would see his holding reduce in value to $38,807.50.

Now imagine investor X insured himself against the risk of GLD collapse by buying some low strike, long expiration puts. Each put (or call) covers 100 shares, so to cover his position, investor X could buy 10 puts. Assuming the premium as quoted above is around $1, this costs investor X $1000 ($1*100 shares*10 puts). A collapse in GLD would see the value of the investors puts rise significantly. 1000% is a very conservative guess, but it could be 5000% or more (the $1 put now worth $50). On the low side, the insurance could see him mitigate $10,000 of the $116,422 loss; on the high side, $50,000 or more. To completely cover his position from a collapse, (based on our estimates) the investor would need to purchase a maximum of 30 puts, costing $3,000. If the value of the puts were to rise 5000% ($1 put rising to $50), then the total increase in value is $147,000, more than offsetting the $116,422 loss sustained by the long position in GLD shares.

If the puts were bought 1 year out (March 2013 is roughly a year away), the cost of “insurance” is $250 per month or $3000 per year. Is this cost justified on a $150,000+ position? Well that depends on one’s estimation of the probability of a collapse. Again, we see this risk as very limited and therefore the cost of the insurance outweighs the risk of GLD collapse in our opinion.

The assumption that a $1 GLD put would rise to $50 is nothing more than estimation, albeit one made on current pricing in the options market. It is hugely difficult to predict how large the market for puts would become in a GLD collapse scenario. The value of puts would also be defined by the rise in implied volatility. The difficulty in predicting this statistic is the main difficulty in predicting how large the value of puts would increase.

A possible method to decide whether insurance is worthwhile is as follows:

This insurance costs $3000 p.a. for a return of $150,000 if GLD collapses. Hence, a 2% probability of a GLD collapse in the next year makes the investor indifferent between buying the insurance and not ($3,000/$150,000 = 0.02). Therefore, if one views the risk of GLD collapsing as higher than 2%, then the insurance is worthwhile, and (puts) should be purchased. If the investor views a collapse as less likely then 2%, insurance is unaffordable and should be avoided. The value of insurance is all down to an individual’s estimation of the risk involved in such a collapse.

What we are presenting is an interesting case. It could easily be argued that if one is long GLD, they could see a collapse as possible – unlikely, but possible. If one sees gold rising in the medium - long term (hence long position), for whatever reason; whether it be financial collapse or devaluation of U.S. dollar, they are at the same time giving GLD a greater chance of failure. As argued earlier in this article (and others), gold rises often with uncertainty whether that be economic, political or societal. The risk of GLD collapsing also rises with this uncertainty, giving rise to a double edged sword of sorts.

Some more sophisticated or more risk tolerant traders may consider selling puts on the gold futures market to offset the cost of buying GLD puts. This strategy works under the assumption that if GLD collapses, the futures market will still be functioning, and the gold futures price would not crash, as a GLD crash doesn’t have a huge bearing on the market for futures. This is based on the premise that GLD as a fund has collapsed, but futures market based on physical gold has not. Sure, the gold price (and hence prices on futures markets) would take a hit with a collapse of the sixth largest holder of the commodity, as fears of forced fire sale of GLD bullion emerges, but the increase in value of the GLD puts would be far outweighed by the amount lost on the written futures puts. Assuming one agrees with the assumptions presented above, the pay-offs for a holder of GLD shares is as follows with each strategy:

Buying GLD puts as insurance against a GLD collapse:

Profit is made if GLD rises in value, and position is insured against a GLD collapse. Upside is less substantial barring a collapse, due to the cost of insurance eating into returns.

Buying GLD puts as insurance against a GLD collapse, and also writing puts on gold futures:

Profit is made if GLD rises in value. Profit is not reduced by the cost of insurance, as the value of the written futures puts offsets it. If a collapse were to occur, insurance pays out, but the trader may not be in as good a position they would’ve been had the collapse not occurred, as the short position on futures puts could be showing negative returns if the futures price of gold also fell. This strategy is optimal if a gold bull sees the likelihood of collapse as very low, but still wants some protection against it.

Both of the above trading strategies can be executed by someone with no GLD position as a speculative trade betting on a GLD collapse.

It is important to note these are simply rough guidelines to demonstrate a hedging strategy. They are not certain protection, but in our opinion provide the potential insurance against a possible GLD collapse.

If one truly believed in the financial system collapsing, physical bullion, canned food and medical supplies are the best investments to be making, not hedging risk with options.

To stay updated on our market commentary, which gold stocks we are buying and why, please subscribe to The Gold Prices Newsletter, completely FREE of charge. Simply click here and enter your email address. (Winners of the GoldDrivers Stock Picking Competition 2007)

For those readers who are also interested in the silver bull market that is currently unfolding, you may want to subscribe to our Free Silver Prices Newsletter.

DISCLAIMER : Gold Prices makes no guarantee or warranty on the accuracy or completeness of the data provided on this site. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This website represents our views and nothing more than that. Always consult your registered advisor to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this website. We may or may not hold a position in these securities at any given time and reserve the right to buy and sell as we think fit. Bob Kirtley Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.