Prepare for When the New MyRA Becomes "TheirRA"

Personal_Finance / Pensions & Retirement Feb 10, 2014 - 02:47 PM GMTBy: Money_Morning

Peter Krauth writes: In his recent State of the Union Address, President Obama unveiled something new: a retirement savings account to "help" Americans build a nest egg, coining it the "MyRA."

Peter Krauth writes: In his recent State of the Union Address, President Obama unveiled something new: a retirement savings account to "help" Americans build a nest egg, coining it the "MyRA."

Something immediately felt wrong about the proposal... but I couldn't put my finger on it.

So I researched the new MyRA and found details to help you understand just how it works.

But I also saw some potential dangers there that you need to prepare for now...

What MyRA Really Means

Like most government programs, getting to their essence can take some sifting. So I've distilled here what I think are the principal components of MyRA.

- Individuals earning up to $129,000 and couples earning up to $191,000 are eligible if their employers offer the account;

- The minimum initial contribution is $25, then at least $5 through payroll deductions;

- The maximum contribution is $5,500 per year ($6,500 if over 50 years of age);

- Once the balance reaches $15,000 or has existed 30 years, it must be rolled into a Roth IRA;

- Total contributions to a person's IRAs cannot exceed $5,500 annually;

- Like a Roth IRA, withdrawals will grow and be redeemable tax-free;

- Principal can be redeemed any time, but earnings withdrawn before age 59 ½ are taxable and subject to 10% penalty; and

- Only one investment available: Treasury bonds paying variable interest-rate return

MyRA Is Set to Lose the Inflation Battle

Essentially, the MyRA is like a Roth IRA that your employer opens for you, allowing for low individual contribution requirements.

But if that's what you want, you can already set up your own Roth IRA with a no-fee, no-minimum account requirement at discount brokers like TD Ameritrade or E*Trade. And then your investment options are practically limitless.

In his speech, Obama said that "MyRA guarantees a decent return with no risk of losing what you put in." So let's look at the underlying investment a little more closely.

Your MyRA contributions would go into a variable interest rate bond investment, comparable to the Government Securities Fund in the Thrift Savings Plan (TSP) for federal employees.

That fund's recently been paying 2.5%, which admittedly is way better than the 1% you can get from the highest yielding savings accounts. And that looks OK, until you consider... inflation.

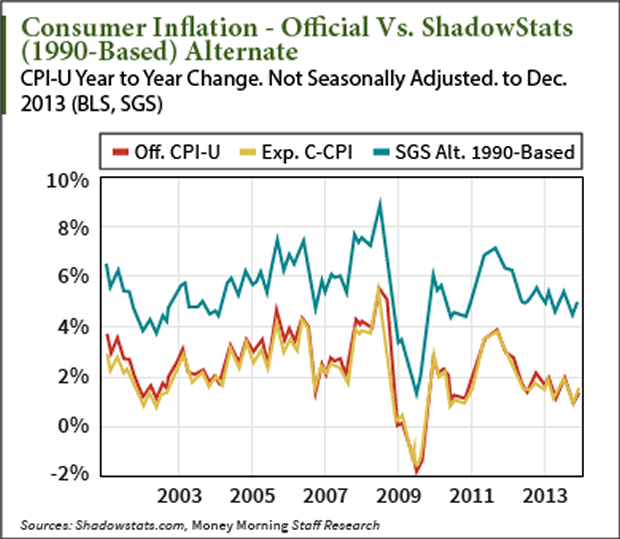

Right now official U.S. inflation has been 1.5% through the 12 months ended December 2013. If instead we look at a truer inflation rate, like the more realistic one calculated by ShadowStats, the emerging picture is altogether different.

Shadowstats finds inflation running at 5%, rather than the more benign "official" 1.5%. At 5% inflation, MyRA investors will be losing 2.5% annually.

With interest rates near all-time historic lows, odds are rates will go higher, not lower. And as interest rates rise, the MyRA could find it increasingly challenging to offer an attractive return to investors.

You've Just Become the Government's New Lender

It's no secret that the United States is running out of buyers for its bonds.

China, the largest foreign owner, has been reducing its purchases and has repeatedly said it has enough. Nations worldwide engaged in their own quantitative easing are busy buying their own bonds. Now, the Fed itself has begun the tapering process.

As the U.S. debt and deficits continue to balloon, the government is desperate for a new source of funding. Obama's proposed MyRA looks to Americans to buy up its "junk bonds."

In fact, new demand for bonds is so badly needed, it's easy to see how the MyRA could eventually move from voluntary to mandatory.

Account holders would automatically contribute through payroll deductions, funding the government's IOUs. And those won't pay out for decades until retirement.

This sounds a lot like another government scheme from which Americans can't opt out: Social Security.

Eventually, the need to fund a mushrooming debt could lead to compulsory government bond buying in retirement accounts. At first, it might be 10% to 20% of all new contributions, then perhaps 10% to 20% of existing balances. With over $5 trillion in U.S. retirement accounts, it's easy to see how a mandate for 20% (or more) directed into Treasuries will help extend and pretend.

Consider that Japan's debt to GDP ratio is 140%, already way above the 100% level considered problematic. This is possible in large part because so much of the national debt is held by its own citizens rather than foreigners.

So it's not a huge stretch to imagine America heading down the same path.

Eventually, retirement accounts could even be at risk of partial or even outright confiscation as debt levels become increasingly unsustainable. A desperate government will look to take desperate actions.

If you think I'm exaggerating, consider what's happened elsewhere.

In just the last five years, there have been government confiscations of retirement assets in no fewer than six countries, including Argentina and Poland, as I alluded to in a November article.

In that piece, I said:

Back in January 2010, Bloomberg BusinessWeek reported, "The Obama administration is weighing how the government can encourage workers to turn their savings into guaranteed income streams following a collapse in retiree accounts when the stock market plunged."

Then in February this year, the Washington Times reported: "Consumer Financial Protection Bureau director Richard Cordray recently mentioned these [401(k)] accounts in a recent interview, stating 'That's one of the things we've been exploring and are interested in, in terms of whether and what authority we have.'"

As follow-up, I mentioned that the International Monetary Fund (IMF) was considering the potential of a "'capital levy' - a one-off tax on private wealth - as an exceptional measure to restore debt sustainability."

And if you think this could never happen in the good ol' U.S. of A., consider that back in 1933, President Roosevelt seized privately held gold by signing into law Executive Order 6102.

FDR's official motive was to "provide relief in the existing national emergency in banking, and for other purposes." Desperate times, desperate measures.

The Best Way to Keep Your Retirement Yours

What can you possibly do to protect yourself? Here's where thinking "outside the box" is vital.

The alternatives are simple, but they do require some effort and planning.

There are updates to some key points I've alluded to in the past: there are three basic things to do, and they apply equally to both good and bad times.

- Own and invest in hard assets like gold, silver, energy, and real estate. You can buy physical precious metals; you can buy physically backed ETFs; you can own quality resource equities, including your own home; and you can own income-producing properties and land. Assets in non-retirement accounts are more difficult to expropriate.

- Hold plenty of cash. Cash is king, despite the risks of inflation. Hold it as a bank balance, but watch FDIC deposit insurance limits, and consider diversifying into other currencies. Be sure, however, to hold some physical cash as well, as this could be crucial during a "bank holiday."

- Hold assets internationally. This is largely the same as in owning hard assets, as above, but in another country. Consider opening a foreign bank account. It's not easy for Americans - thanks to FATCA - but holding something outside your country of residence makes it tougher for a desperate government to grab.

Remember, as government debt grows to even more unmanageable levels, and interest rates cause most government income to service the debt, they will become increasingly desperate.

Sidestep the trap.

Don't let your MyRA become Uncle Sam's.

Source : http://moneymorning.com/2014/02/10/prepare-now-new-myra-becomes-theirra/

Money Morning/The Money Map Report

©2014 Monument Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution (electronic or otherwise, including on the world wide web), of content from this website, in whole or in part, is strictly prohibited without the express written permission of Monument Street Publishing. 105 West Monument Street, Baltimore MD 21201, Email: customerservice@moneymorning.com

Disclaimer: Nothing published by Money Morning should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized investent advice. We expressly forbid our writers from having a finan

cial interest in any security recommended to our readers. All of our employees and agents must wait 24 hours after on-line publication, or after the mailing of printed-only publication prior to following an initial recommendation. Any investments recommended by Money Morning should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Money Morning Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.