Long on Natural Gas, Longer on Crude Oil

Commodities / Oil Companies Dec 01, 2010 - 02:13 AM GMTBy: The_Gold_Report

Even if the pace of China's growth slows dramatically, count on the commodities boom to continue, says Adrian Day Asset Management Chairman and CEO Adrian Day. That bodes well for oil, as China's huge population will at least double per-capita consumption of oil over the next decade—maybe even drive it up fivefold. In this Energy Report exclusive, Adrian discusses Indian and Chinese demand and why he isn't worried long term about natural gas.

Even if the pace of China's growth slows dramatically, count on the commodities boom to continue, says Adrian Day Asset Management Chairman and CEO Adrian Day. That bodes well for oil, as China's huge population will at least double per-capita consumption of oil over the next decade—maybe even drive it up fivefold. In this Energy Report exclusive, Adrian discusses Indian and Chinese demand and why he isn't worried long term about natural gas.

The Energy Report: Adrian, you recently published Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks, your first book in 28 years. Why write a book now?

Adrian Day: I think the topic is remarkably crucial and important. Everybody understands the main drivers behind the increase in resources prices but most people, including those in the business, aren't yet fully grasping the scale of the resource shortage that I see coming. They know China's demand is going up. They know it's more difficult to get permitting and more difficult to find new deposits. But I don't think they really appreciate the extent of the problem.

TER: What is the most important thing for people to know?

AD: One of the keys is to really understand what kind of investor you are because what you buy and how you trade depends on that a lot.

- Can you tolerate risk? Or, will you panic if stocks decline 50%? Rick Rule, one of my friends in the business, keeps telling us that volatility is a fact of life. How you use volatility determines whether you're successful. Make volatility your friend.

- How much time are you willing to devote?

- And frankly, how much money do you have to invest? If you don't have a lot of money, perhaps you want to be invested in one or two mutual funds. The more money you have, the more you can invest in different sectors and different areas.

TER: You talk about this enormous resource shortfall. Surely, the U.S. doesn't appear to be on the brink of any boom. Why is it so big, especially considering that there was no shortage 5 or 10 years ago, when our economy was booming? Even China isn't growing at the rate it was.

AD: It doesn't matter whether the U.S. is booming or not. It doesn't matter whether Europe is booming or not. China has been driving the resource market and will continue to drive it for the next decade. That's what really matters; that's why I say it doesn't really matter if China's economic growth slows from 9.5%–5%. The demand for resources will still be very dramatic, and much higher than it is now. Just think about it. Everybody in China wants the same things we do. They want houses with electricity and running water and indoor plumbing. That takes steel and copper. If they move from a rural area into the city, at some point, they want a car. That takes aluminum and platinum, rubber for the tires and, of course, oil to run it. Obviously, cars are much more resource-intensive than bicycles and China is changing from bicycles to cars.

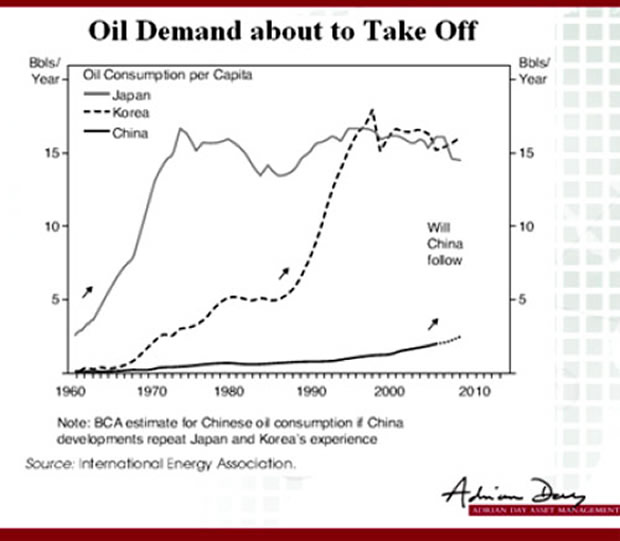

When countries industrialize, they tend to go through a characteristic pattern. Typically, the demand for commodities—resources—starts to grow as the GDP increases. It starts from a very low base and slowly over a period of 10–15 years, or even longer, begins to gather momentum to double that level. When the GDP reaches a certain level, the industrializing economies hit that takeoff point. Then the demand for resources starts to accelerate. It took longer for Germany and America 100 years ago, but it was over 10 years for both Korea and Japan that demand accelerated until the economy industrialized and matured, and then the demand reached a plateau. The demand doesn't decline; it reaches a plateau. The critical thing is that demand for resources increases and accelerates at that takeoff but it increases on a per-capita basis. Just to give two examples if I may.

Look at Japan and Korea at different stages—Japan starting in the '60s, Korea starting in the '80s. Per-capita consumption of oil as they started to industrialize went from a very low base of less than one barrel per person per year to two barrels, then up by another half-barrel per person per year. At that takeoff point, over a decade it shot up to 15 barrels per person. The typical oil consumption of all industrialized countries around the world varies from about 14–15 barrels per person. The U.S., of course, is an outlier as it is in many things but if you look at Denmark or Japan, Germany, Britain or Canada, if you look at a sparsely populated or a densely populated country, a green or not-so-green country, it's about 15 barrels of oil per person per year. That's what it takes to run a modern industrial society.

TER: And where is China's demand for oil now?

AD: From less than half a barrel per person 15 years ago, China now is at about 2.7 barrels per person. Already this year, it has surpassed the U.S. as the #1 consumer of oil in the world. But now, it's at that takeoff point. Suppose for a moment that China doesn't go to 15 barrels per person. Suppose it only goes to a third of the world average, which is a pretty conservative assumption. Suppose it takes longer than 10 years. That's still more than doubling China's oil consumption on a per-capita basis.

China represents 20% of the world's population. So, unless its industrialization reverses—not slows down but reverses—the demand for resources is about to accelerate.

TER: So slow acceleration brings an evolving country to a tipping point, after which the demand grows exponentially.

AD: Absolutely. And we could look at copper. . .at all of the resources. The pattern of consumption would be similar. It has much more significance than what happened in Korea or even Japan, because it's China—due to the population.

TER: How do the other BRIC countries figure into your equation?

AD: India is a long way behind. India today is about where China was 10 years ago. As China's economy reaches a mature stage—mature in terms of the consumption of commodities, which probably will be 10–15 years from now—India will be just about at that takeoff point.

TER: So, we have two tidal waves coming?

AD: Absolutely. India right behind China, and then Brazil and another country with a large population, right behind India.

TER: Why aren't the general investment markets seeing this?

AD: I think that in very long-term, dramatic trends, people always tend to be playing catch-up. You see it with individual companies with big discoveries that continue to grow. The stock price goes up, but it's still good value because investors also generally have difficulty with a big trend getting ahead of them. Their understanding of it is always lagging.

TER: What makes your book different?

AD: It's very accessible. My book is very much a primer, if you like, not aimed at experts in the field but rather for educated investors who don't really know much about resources. I think it is particularly helpful perhaps for newer investors, or investors who are new to resources, because I try to write without jargon. I try to make it understandable to ordinary, intelligent people who know a little about investing but don't necessarily know anything about resources. I don't cover every single resource out there but I cover the main resource areas in separate, short chapters. In the energy area, we cover oil and gas, of course, plus uranium, coal and geothermal primarily.

TER: You've talked a lot about quantitative easing (QE) in the U.S. in conversations, lectures and interviews. How does that factor into the trend toward higher commodities prices?

AD: There are always two major areas to consider any time you look at commodities—the supply/demand factors and the overall economic environment. Other things being equal, a declining dollar means higher commodity prices. More money being put into the system and low interest rates also mean higher prices for commodities. Well, guess what? We've got a falling dollar, more money being put into the system and low interest rates. So, we have the perfect economic environment on top of the perfect supply/demand situation.

TER: An accelerant on the flames.

AD: I have no doubt that, at some point in the next few years, we're going to see an upward, albeit temporary, correction in the dollar. I have no doubt that we're going to see a slowdown in China. When China's GDP growth drops from 9.5%–5%, 4% or 3%, everybody will think the world's ending—but that's still pretty good, positive growth. But it wouldn't surprise me if we had setbacks. Let's not forget that during the U.S. industrialization from 1870 to the start of World War I, the U.S. had a depression, a recession, strikers getting shot in the streets—all sorts of problems. Think of England's industrialization after the Napoleonic War, from 1815–1840, when Britain transformed from an agrarian to an industrial economy. Again, recession, deflation. . .all sorts of problems going on intermittently. I have no doubt that will happen in China, too; but if you take the big-picture view and don't let these setbacks scare you, you'll look back to see that they only last a short time.

TER: Right.

AD: Resources are more cyclical than most things and there are basic economic reasons for that. If you look back in history, the longest sustained periods of rising prices for commodities across the board always can be identified by a new source of demand—not a shortage. So, if you look at resources from 1870–1914, you see a long, upward move in resources. The same goes for the period from 1815–1840.

Investors must understand major market drivers and why the industrialization of China, and the growing middle class that goes with it, are so important. People in cities use more resources than people in the countryside. Middle-class people buy things that use more resources than poorer people, etc.

If we come into a slowdown, look at whether those major drivers have reversed and are no longer valid. Is this the end or just a temporary slowdown? If you agree that this is a long-term super cycle, don't let the corrections scare you.

TER: What basic strategies do you tell people to employ?

AD: The main strategic advice I give to people is to be really careful not to sell out too soon. I believe this is a multiyear bull market in resources. We'll see resources prices go much higher. I don't want to sound as if I'm waving my arms because I don't normally talk that way. Still, over 5, 10, 15 years, I think prices will go higher than we can imagine right now. Part of that will be in deflated dollars, of course; but if you buy quality companies with sound balance sheets that own resources in the ground in good jurisdictions, avoid the temptation to sell when the stock moves a little bit. You may not have the opportunity to buy back.

TER: When you say a bull market in resources, how do you define resources?

AD: I must admit I switch around a bit between the words "resources" and "commodities," but in this context I'm talking about everything from precious metals to base metals to energy—oil, gas, uranium, geothermal—as well as agriculture. I think agricultural assets will be among the best-performing assets over the next decade.

TER: What is your macro perspective on the growing demand, specifically for energy resources?

AD: Energy is a key ingredient as a country industrializes and its economy grows, and as it moves from a rural to an urban society. It needs energy for power and transportation, so the demand for energy will go up as much as the demand for any other commodity. China gets much more of its power from coal than do other countries and plans to get more from uranium than other countries.

TER: Wind or solar?

AD: Surprisingly to some, China also gets a higher percentage of its power from renewable sources than most of the green countries around the world—everything from wind to solar to biomass. And it's going to need every energy source it can get. Just to give you one way of looking at the potential—in China, one third of the people rely on traditional biomass fuels for cooking.

TER: What sort of investment opportunities in coal can you tell us about?

AD: The problem is that the "purer" coal companies, such as Teck Resources Ltd. (NYSE:TCK; TSX:TCK.A, TSX:TCK.B), are not exceptionally cheap right now. Probably one of the best ways for the ordinary investor to get exposure would be through one of the large diversified resource companies like BHP Billiton Ltd. (NYSE:BHP; OTCPK:BHPLF), clearly not exclusively coal but a very large coal producer. It's very close to the main market in China and is expanding its coal.

TER: China and Mongolia have massive coal resources. Do they really need to expand nuclear?

AD: Absolutely. They've gone from being a net exporter of coal to a net importer. Most of their coal mines tend to be rather old, extremely dangerous. So, China's own deposits of coal are in no way a solution to China's power needs.

TER: How rapidly will China expand its nuclear energy resources?

AD: It has more than 40 power plants on the drawing board currently or in various stages of production as part of a process that will be staggered over the next seven or eight years. Some are being built already, some are in development and some are still on the drawing board. This compares with 13 currently in operation and a further 23 under construction, but as many as 120 have been proposed beyond those. This phenomenal growth will mean huge demand for uranium.

TER: China has uranium mines. Will it have to import uranium, too?

AD: Oh, absolutely. There simply isn't enough uranium that we know about in China to feed its own demand. It just signed a 20-year contract to buy uranium from Cameco Corp. (NYSE:CCJ; TSX:CCO), and it's making these deals around the world.

With nuclear energy, one component that's a little different from other sources is the plant itself. The largest part of cost from discovery through to output is the capex for building the plant. Relative to other power sources, operating costs tend to be low once you build a nuclear plant. The cost of uranium as a percentage of overall cost of that power for 20 years is extremely low; but, by the same token, a nuclear power plant cannot switch to coal or gas. So, once you've put all those billions of dollars into building a plant, it's critical to get the uranium—at almost any price. I won't say it doesn't matter how much, but it is certainly not a project killer if uranium runs up to $300/lb. The uranium price is far less important than the dependability of supplies.

TER: So, why hasn't the price of uranium gone up?

AD: Well, China's big demand increase for its nuclear plants won't really start until 2015, 2016. India and other countries haven't really started yet. At the same time, we have excess supply now. Kazakhstan, which is acting as a swing producer, has a lot of excess capacity; so it can increase its production relatively easily as the price moves up and pull back if the price goes down. That's the main reason uranium is fairly low. That said, because markets tend to look ahead and discount, I don't think we're going to have to wait until 2015 to see shortages start. In the second half of this decade, we'll see a real supply/demand imbalance. At that point, prices will go up.

TER: Is there enough uranium exploration underway to address that shortage to some extent?

AD: There's a reasonable amount of exploration. Uranium has certain attributes—both real and imagined—that differ markedly from, say, gold or copper. Few people want a uranium mine next door, so it takes a lot longer to get exploration permits. Several current deposits in the U.S. could be mined but they're still in the permitting stage.

Another issue is that exploring for an economic uranium deposit is technically more difficult. With a big open-pit copper operation, you can miss the core of the deposit by half a mile but still mine the deposit. With many uranium deposits, it's a bit like looking for a needle in a haystack—they tend to be extremely rich but very small.

TER: What are some uranium companies you like?

AD: On the exploration side, I like to minimize risk and prefer the simplest, most direct investment with the least downside. But rather than look for a pure-uranium exploration play that may or may not find an economic deposit, and may or may not get the permits even if it finds one, I prefer more broadly diversified explorers that have exposure to uranium. Altius Minerals Corporation (TSX.V:ALS) has two uranium exploration joint ventures (JVs) with other companies. So, if the uranium price goes up sufficiently you'll get the exposure.

TER: What else is Altius invested in?

AD: Gold, iron ore, nickel and uranium are the four main products. It has the large royalty in Voisey's Bay, a gold mine in production in another JV and also phosphates. Everything it does is JV, so it's low risk.

TER: Any other uranium explorers you want to talk about?

AD: I don't do much with the explorers. I look more at producers and other companies in the uranium business. In uranium, Canada's Uranium Participation Corp. (TSX:U) is a good way of buying. It's a closed-end fund, so it trades at a premium and sometimes a discount. You should avoid buying when the premium is too high. But that holds uranium, so it's a direct play on the uranium price. You don't have the exploration risk, but you don't have the upside either.

TER: How about among the uranium companies themselves?

AD: AREVA (PAR:CEI) is an explorer and producer that's JV'd with Cameco on many of its projects and is part owner of Cigar Lake. It also has other exploration projects. More importantly, in JV with other companies, it builds power plants and also is involved in depleted uranium disposal—really a one-stop shop for uranium.

TER: It's virtually integrated.

AD: That's right. The problem with AREVA is that it's owned mostly and controlled totally by the French government, so you can't be sure what's going to happen from day to day. But CEO Anne Lauvergeon is first-class, well respected around the world. It's a great company. I like AREVA.

TER: Any others?

AD: Among the smaller producers, I think Paladin Energy Ltd. (TSX:PDN; ASX:PDN) in Australia is a good company with a lot of upside potential.

TER: What intrigues you about the renewable sector?

AD: With growing consumption for energy, we're going to need to get it from every source we possibly can. I'm not a big greenie, but I don't like pollution anymore than anybody else. The more green sources we can get the better. Some of these are also renewable, which is the best of all. Solar is not renewable in the sense that you get rid of the solar panels when they run out after 10 years or so.

TER: But geothermal. . .

AD: The best of all worlds because geothermal has a very small environmental footprint. When the plant is running it doesn't disturb much of the environment. It's essentially permanent, totally renewable with no toxic byproducts. It's a small sector, though, and obviously you don't produce geothermal energy in California and ship it off to China. So, the China story doesn't come into play with geothermal except to the development of its own geothermal resources; and China's demand for energy generally will affect the economics of power everywhere.

TER: Do you follow any geothermal companies?

AD: The largest pure play is Ormat Technologies Inc. (NYSE:ORA), which isn't particularly inexpensive right now. Chevron Corporation (NYSE:CVX) is the largest U.S. geothermal company but, obviously, you don't buy Chevron just for geothermal exposure. Some juniors in the middle include Ram Power Corp. (TSX:RPG) and Magma Energy Corp. (TSX:MXY), both of which are well diversified country wise. Ram has a good balance sheet; Magma has significant capital needs in coming months. But both have access to capital, which is critical.

A lot of very small companies are capital-constrained. You don't get government grants until you've spent the money, so they're in a Catch-22. If they could only get the money to explore, they could get the government grant to pay it back; but they're too small to get access to capital. Thus, many of them have been taken over on disadvantageous terms, which I think soured people a little on the entire sector. The whole geothermal area is starting to bounce back, but it had declined dramatically over the last 18 months.

TER: So, it's a buying opportunity.

AD: I think so. They've come off the bottoms quite significantly, but I still think this is a very good time to buy them. Magma's at about $1.47—up from about $1, down from about $2.

TER: Has Magma worked out its differences with singer Bjork, who was among the Icelandic celebrities opposing its purchase of HS Orka?

AD: Very interesting story. Magma now owns essentially all of HS Orka, which is the largest geothermal source in Iceland. Ross Beaty, Magma's CEO, did offer to sell Bjork either one-fourth or one-third of the power plant if she wanted to pay him at cost, no profit. She said, no. He didn't understand; she didn't want to own it—she just didn't want him to own it. So has it been solved? Yes, the near-term situation has been solved. A government panel was set up to investigate and ruled that everything was in accordance with Iceland's rules.

TER: You said this is a near-term solution?

AD: Yes. No question, there is a fundamental issue in Iceland about foreign financiers coming into the country. It had a bad experience in the credit crisis in 2008, which left underlying sentiment against foreign financiers. There's also an underlying sentiment against foreigners taking over its key assets, energy being one. They don't have a lot in Iceland. Geothermal is just one of the things they do have.

Ross has said publicly and he keeps repeating it—he wants an Icelandic partner. And he's not only willing to sell a minority, 25%, 33%, but at his cost. He said he doesn't want to take a loss but doesn't want any profit, either. So far, no one's stepped up.

TER: An Icelandic partner makes sense.

AD: Yes, in part to defuse the political situation there. In any country, it's always good to have a local partner; and frankly, to free up some money and put it to work in Magma's Chilean and U.S. properties.

TER: Does Magma have power agreements in place for those U.S. projects yet?

AD: Not yet. Ram is a little more advanced in its U.S. projects. It has a better balance sheet and it has the power agreements, though it, too, will have to juggle to ensure it has the necessary capital for its development and exploration projects at the right time over the next few years.

TER: Plus an existing power plant in Nicaragua, that's doing something like 10 megawatts. Ram is also developing larger operations there, isn't it? How is that progressing?

AD: Things are developing well, pretty much on schedule. There are always delays in this business, but no extraordinary delay. Ram has a very broad portfolio and acquired Sierra Geothermal Power Corp. this summer, which gives it more early stage property to develop.

TER: Are there any other opportunities for geothermal investment?

AD: For those who are more aggressive and can tolerate the volatility and higher risk, some of the smaller U.S. companies are good buys. US Geothermal Inc. (NYSE.A:HTM) and Nevada Geothermal Power (TSX.V:NGP), for example, are probably the largest of the small ones. But remember, the smaller companies are also potentially nearer-term takeover targets; and when a company is taken over because it can't raise money, the sale doesn't necessarily command a good premium.

TER: Can you give us your high-level viewpoint on oil and some investment opportunities in that space?

AD: My high-level viewpoint on oil is not all that different from what I see for copper, zinc and everything else—a huge demand increase from China. It will need oil to fuel its cars, and it also uses oil in power generation, just not as great a percentage as other countries. Now, there is no meaningful substitute for oil, and certainly not for China. Yet, this huge demand increase for oil is building but we're not finding sufficient new sources of oil to replace what we use, let alone to meet greater demand.

We discovered the most oil way back in the mid-1960s when we discovered oil in the North Sea and Alaska at the same time. Those were huge fields. Looking back, this was closer to World War I than it is to today. From then to today, it's been a fairly steady decline with a few peaks and valleys. But on rolling three- or five-year basis, we are finding less new oil every year.

In the early 1980s, oil demand surpassed oil production. And annual oil consumption has exceeded that of discovery every year since, by an increasing amount. All of these big fields, including offshore Brazil, are wonderful. And many oil fields last a long time, so I won't say we're running out of oil anytime soon. But we can see an impending problem coming, because we've stopped discovering as much as we did previously and we're using more than we produce. Clearly, we're reaching the point where oil demand will greatly exceed production and the oil price has to go up.

TER: Does that mean the investment opportunity in oil is more due to the prospect of higher prices than new discoveries?

AD: Yes, I think so. The exploration and production (E&P) companies are always exploring and finding new sources, but many of those simply aren't significant in a long-term global view.

TER: If the oil price is going to go up, why not just go with big, heavily oil-focused players like BP Plc (NYSE:BP; LSE:BP), rather than look at options like the Canadian tar sands?

AD: Good question. It varies but the big global companies tend to be vertically integrated, exploring, refining and selling, and a higher oil price doesn't necessarily benefit them across all operations. Some are actually oil-price neutral. The large integrated oil companies also have an enormous replacement issue. Independents like Apache Corporation (NYSE:APA), EOG Resources (NYSE:EOG) and Devon Energy (NYSE:DVN) have nowhere near the serious replacement issue as Exxon Mobil Corp. (NYSE:XOM). For the global majors, most oil-reserve improvements come from either acquiring other companies or revising existing reserves—not new discoveries.

That can go on for only so long. I don't invest much in the big integrated companies other than short-term moves when they get oversold. If I were to pick any company, it would probably be BP because a much larger percentage of its revenue comes from E&P than refining. But even BP has a huge replacement problem.

So then, the next thing to look at would be the large impendent E&P companies. There are some very good companies in that space. Devon is one of the best—great balance sheet, less than 20% debt to capital, growing production. It recently sold all its offshore assets, including those in the Gulf of Mexico, shortly before the Deepwater Horizon disaster. It also sold a lot of other offshore assets around the world to focus on North American onshore. Devon is one I like.

We also own Chesapeake Energy Corp. (NYSE:CHK) and Encana Corporation (TSX:ECA; NYSE:ECA), which also has some oil sands, and those are very long-lived assets. They are high-cost assets, too; so as the oil price moves up, you have much greater leverage with oil sands than with traditional oil producers. The U.S. will likely continue to have much greater access, so it won't have the supply problem buying oil from Canada that it might have with Saudi Arabia, Venezuela or a host of other countries.

TER: Do you have some specific oil sands companies that you like?

AD: Canadian Oil Sands Trust (TSX:COS.UN), which is a unit trust, is one of my favorites. I also like Cenovus Energy Inc. (TSX:CVE; NYSE:CVE), which was created when Encana separated its gas assets (in Encana, now a pure gas play) and its tar sands assets (in Cenovus). Suncor Energy Inc. (TSX.V:SU; NYSE:SU) is a good company, too, but I think it's a little expensive right now.

TER: But Canadian Oil Sands looks good now?

AD: The other ones I would wait for, but at roughly $26, Canadian Oil Sands is a great long-term buy, and it's cheap relative to the rest of the sector. When we think of oil trusts, we think of something like the ARC Energy Trust (TSX:AET.UN) or something that pays a high and dependable yield. That never was the COS story, though it sports a very nice yield—over 7% currently. Still, uncertainties over the end of favorable tax treatment for unit trusts—despite that it's not an issue with Canadian Oil Sands—affects all the trusts.

TER: Would you be interested in an ETF for exposure to higher oil prices?

AD: No. GLD, the gold ETF, is a great way to play gold and Uranium Participation Corp. is a great way to directly play uranium, though the latter is a closed-end fund—not an ETF. The problem with commodity ETFs is that, by and large, they invest in futures contracts, not the commodities themselves. With some commodities, oil particularly, you have very high contangos—the difference between forward and spot prices. So, they're continually rolling over contracts at higher prices. Oil is a classic example; while the oil price is up this year, the oil ETF has actually lost money—over 11%. They're always buying high and selling low, which is not exactly the road to successful investing.

TER: Are you long on gas?

AD: We are definitely long on gas, but even longer on oil. We'll have to wait a bit for gas. Because of the new shale that's come on, we've gone from what everybody saw as a permanent gas shortage to a permanent gas glut. Many gas producers have since started shifting over to more oil; for example, EOG was exclusively gas and liquefied natural gas (LNG). Last year, it made a decision to go 50/50 oil and gas. A lot of these companies are backing off development in some of their gas fields due to the low price and the glut.

Ironically, I think a new source of gas like shale—which means a dependability of supplies—also means people will be more willing to put the capital into gas-fueled fleets of buses and so on because they know we can get the gas.

TER: Do they expect the glut to go on forever?

AD: While there's no doubt that the shales have been remarkably and unexpectedly successful, there's still an open question as to how long many of them will last. The decline rates—going from the first to subsequent years of production—have been very, very fast. . .much faster than with conventional oil. We don't really know yet how long the tail will be. There's a lot of debate in the industry about that.

TER: How would an investor play the natural gas sector?

AD: Encana is good. Some of the trusts are good, such as ARC, which are both oil and gas. For the more aggressive investor, some of the smaller Canadian oil companies that are a bit capital-constrained are good plays.

TER: Any other companies you'd like to talk about?

AD: One of my favorites in the general resource area would be Sprott Resource Corp. (TSX:SCP). If you buy Sprott, which is quite a liquid company, you're getting it at a discount to net asset value (NAV). NAV is about $5.20; the stock's been trading at about $4.35. You're also getting great management—Kevin Bambrough and company—and a great balance sheet.

Sprott has direct and indirect investments in different resource areas, buying whole companies, sponsoring companies or growing them. The four main areas it's in now are: 1) gold, primarily gold bullion; 2) oil and gas; 3) agriculture; and 4) fertilizer. When the companies reach a certain level, ideally it will spin off a certain amount of the shareholding in a public company. Sprott is extremely disciplined and has done this a few times already—with Orion Oil & Gas Corp. (TSX:OIP), for example, which started trading on the Toronto Stock Exchange almost a year ago.

Sprott also has JVs, including one in phosphates with Altius, and owns shares in Lara Exploration Ltd. (TSX.V:LRA). The agriculture play is very interesting—One Earth Farms Corp.—a JV with First Nations, which owns more than a million acres of farmland. It's going to be a big business, one of the largest commercial farms in North America. It's really quite staggering. It's still a private company, but it's selling some shares in a secondary offering, raising $40M–$80M. If it brings in the maximum, it will take Sprott's stake down to 24%. In a year or two, it'll IPO. That's what it's trying to do—take a direct investment, build up the company and IPO it.

TER: Any other comments to wrap this up?

AD: We need energy for a modern industrial society and we need lots of energy for an agrarian economy to industrialize. We need all these sources—oil and gas, coal, uranium and geothermal. We're probably going to need a few solar panels and windmills, as well.

Adrian Day, a British-born writer and money manager who graduated with honors from the London School of Economics, has made a name for himself searching out unusual investment opportunities around the world. As president and CEO of Adrian Day Asset Management, he generously shares his thoughts, opinions, insights and analyses via Barron's, Forbes, Bloomberg Markets, Kitco, Casey, The Stock Advisors, Dick Davis Digest, MSN Money, Financial Times, The Daily Reckoning, The Herald Tribune, The New York Times and, of course, The Gold Report—among others. A frequent speaker at international seminars and a regular guest on CNBC and The Wall Street Journal Radio Network, he has been interviewed by Money, Straits Times, Good Morning America and others. He also writes the quarterly Portfolio Review newsletter for clients, serves as editor of Adrian Day's Global Analyst and has authored three books on global investing: International Investment Opportunities: How and Where to Invest Overseas Successfully, Investing Without Borders and the just-published Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks, which is now available in hardcover and e-book format.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

DISCLOSURE:

1) Brian Sylvester of The Gold Report conducted this interview. He personally and/or his family own the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Timmins.

3) Ian Gordon: I personally and/or my family own shares of the following companies mentioned in this interview:Timmins Gold, Golden Goliath, Millrock and Lincoln. My company, Long Wave Analytics is receiving payment from the following companies mentioned in this interview, for receiving mention on my website, Golden Goliath, Millrock and Lincoln Gold.

The GOLD Report is Copyright © 2010 by Streetwise Inc. All rights are reserved. Streetwise Inc. hereby grants an unrestricted license to use or disseminate this copyrighted material only in whole (and always including this disclaimer), but never in part. The GOLD Report does not render investment advice and does not endorse or recommend the business, products, services or securities of any company mentioned in this report. From time to time, Streetwise Inc. directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.