Dyseconomics: The New Macro Econ and The Greatest Economic Boom Ever

Economics / Economic Theory Apr 29, 2011 - 04:21 AM GMTBy: Submissions

Cetin Hakimoglu writes:

*warning the views of this summary may appear bunt, infuriating, and or egregious, but this is my analysis about why things are the way they (normative economic Natalie Bassingthwaighte s) versus a populist feel-good rant about the fed or shadow banking. *

Cetin Hakimoglu writes:

*warning the views of this summary may appear bunt, infuriating, and or egregious, but this is my analysis about why things are the way they (normative economic Natalie Bassingthwaighte s) versus a populist feel-good rant about the fed or shadow banking. *

The greatest economic and stock market boom in human history is unfolding because of a counter intuitive economic system called dyseconomics. Dyseconomics is a portmanteau of dysfunctional and dystopian with economics, but it’s actually the optimal economics system strong economic and stock market growth in today’s global economy. It’s dysfunctional or dystopian because it consists of things that people generally don’t like such as high government deficits, high unemployment, and a falling dollar. Dyseconomics is not only an economic practiced by policy makers but also describes the economic developments over the past decade (although most of these are not new, they have all coincided over the past 10 years). Dyseconomics:

1. Increased government intervention in financial markets (bank bailouts) and aggressive monetary policy (cutting rates in financial panic) to keep economic growth steady and recessions & bear markets brief.

2. Economic interdependency between the US and BRIC markets.

3. Increased government spending for things that create economic growth but are not necessarily socially popular such as war, national security, bailouts, stimulus, and tax cuts.

4. Disregard for US dollar and deficits by policy makers. A lower dollar combined with low rates makes the deficit less burdensome, while falling dollar helps multinationals. This spending is subsidized by foreign governments.

6. Two-track inflation characterized by low core CPI and low treasury yields, but steadily rising cost of living inflation due to relentless global economic growth, permanently low rates, and to a lesser degree price gouging & speculation.

7. An economic system that seems to exclusively benefit the ‘elite’ and multinationals though globalization and low borrowing rates.

8. Fed keeping the foot on the gas even during strong economic expansion and only releasing the gas pedal very slowly. It’s not like the 80’s and 90’s interest rates were high as the economy boomed.

9. Breakdown of Okun's law (decoupling of employment and GDP). What this means is economic output is unaffected much less today & in the future by high unemployment than in the past.

10. Dollar-denominated assets (oil, euro, gas prices, high-end real estate, metals, grains, stocks, web 2.0 company valuations) rising and falling in lockstep with the stock market. This is in contrast to the 80’and 90’s when commodities, the dollar, and stocks showed little correlation.

Alan Greenspan’s non-mistake and the 2002-present economic boom

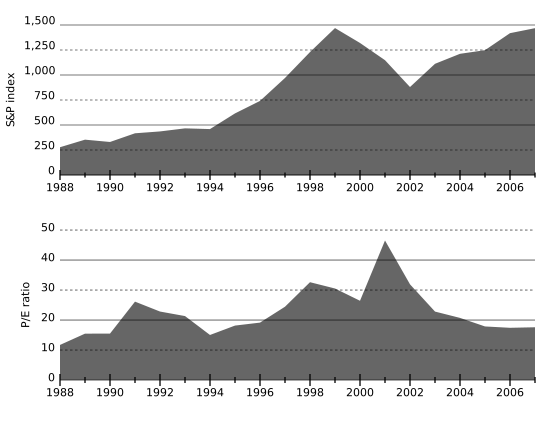

Contrary to popular belief Alan Greenspan didn’t hurt the economy by keeping ‘rates too low’ but was instead adhering to dyseconomics which gave him the luxury of leaving rates low for an extended period. The media would have you believe that had Bush and Greenspan been more fiscally conservative the economy would have been better off by preventing the 2008 recession. The media is wrong because when the stock market crashed, so did PE ratios falling from a high of 22 in 2007 to the low teens. If the fundaments were in trouble PE ratios would have risen or stayed the same as what happened in 2001 when the PE ratio of the S&P 500 actually hit a peak of 47 after the crash due to falling earnings. At the peak of the technology bubble the S&P 500 had a PE ratio of nearly 35 with the index at 1,500; now it’s at 1,300 but the PE is only 23 so you could extrapolate that if it were valued at the same level it was in 1999 it would be at over 2,600. That 1,100 point difference (even after the 2008 recession) is pure earnings that can be attributed to market friendly economic policies of the past decade.

As of March 2011 median US home prices are slightly lower than they were in early 2009, but GDP & profits have recovered markedly lending further doubt to the supposed correlation between the housing market and overall economic strength. Greenspan may have helped inflate a big bubble, but when it burst the S&P 500 felt it only modestly (in terms of profits & earnings). During Greenspan’s 18-year tenure the US economy was in recession for only 16 months, and even after the 2007-09 recession the total duration was just 34 months over the past two decades.

Remember the infamous Clinton surplus? The economy entered a recession on it, further dispelling the notion that high debt implies an unhealthy economy. High interest rates, relatively high personal savings rate, lack of spending contributed to it. Essentially, money began stagnating the late 90’s as the country became a giant piggybank.

Then came the dotcom crash, Iraq and Afghanistan wars, massive tax cuts, low rates, and the BRIC economic boom. These events prevented what could have been a repeat of Japan’s multi-decade economic malaise. Corporations were once again flush with cash and began reporting larger profits & earnings than ever.

As you can see from the chart below during the 90’s PE ratios gradually rose in tandem with the S&P 500, eventually peaking AFTER the market plunged! Since 2002 there has been a divergence meaning that earnings are so good that PE ratios fell despite stocks rallying. Therefore, you can surmise that the economic fundamentals in the past decade (under the least popular president and fed chairman) till the present are better than they were in the 80’s and 90’s, but you won’t hear that from the media.

S&P 500 earnings growth rivals that of the 90’s according to the chart http://static.seekingalpha.com/uploads/2010/6/11/283299-127626464876247-Joe-Eqcome.jpg earnings yields for the past decade matched or exceeded that of the 90’s and presently at the highest rate since 1994.

GDP calculations don’t fully reflect this growth due to the trade deficit deduction, which has become irrelevant as deficits haven’t been shown to be inflationary and economically detrimental. Fund managers know this and that is why the S&P has doubled even though GDP growth is only at 3%. Furthermore, projected United States GDP growth for 2011 exceeds that of any country in the Eurozone.

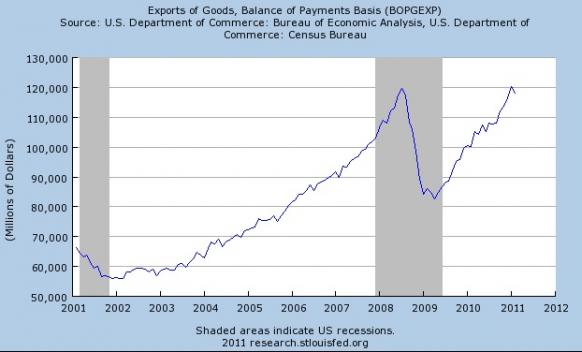

Exports, productivity, government spending, information technology, low rates, globalization, robust profits & earnings for multinationals, low taxes are the key driving factors for this economic expansion and huge bull market. None of these things shows signs of slowing. The chart below shows an obvious ‘v’ shaped recovery in exports:

Job creation, small business, and housing will have to sit on the sidelines in this boom. Small business is unable to take advantage of low cooperate bond rates, pricing power and globalization that multinationals enjoy and there’s nothing the government can do to spur more hiring or small business expansion that isn’t already being done.

Bank bailouts …a success and a necessity

We constantly read on the blogosphere and to a lesser extent in the main stream media in 2008 and 2009 about how the bank bailouts would lead to moral hazard and a Zimbabwe like hyperinflationary scenario. While risk taking is making a comeback, there was no hyperinflation. Short term yields are hypersensitive to financial shocks allowing bailouts and infusions to be made with impunity. The cost of TARP according to the bond markets was essentially free and it would have been reckless for policy makers to not take advantage of this opportunity.

Letting the banks ‘run wild’ can create volatility, but it’s easy to remedy by ‘printing it away’ as was shown in 1987 black friday, 1998 LTCM and 2008. The 2008 financial crisis, while deep, was brief thanks to the expediency of Bernanke, Geithner, Paulson, and G.W Bush. Risk tasking should be encouraged because it creates innovation and when things do, on occasion, go badly it’s pretty easy to fix the problem due to ‘free money’ in the form of perpetually low rates.

In retrospect the Bernanke TIME man of the year nomination was justified when you look at how well the stock market and economy has done in the past two years.

The debt binge is sustainable

Dyseconomics is not Reaganomics in that ‘reckless’ government spending is almost encouraged because it’s subsidized by an insatiable demand for US treasuries by BRIC and public & institutional holders, thus allowing deficit fueled growth without upsetting the bond vigilantes. This is evidenced by perpetually low 10, 30 year treasury yields. Until GWB came into office the BRIC was in its infancy and income taxes and interest rates were raised on numerous occasions out of necessity. The rise in BRIC economies, more specifically BRIC surpluses, correlates negatively with long term rates. The republican and libertarian fears about tax hikes because of the bailouts & stimulus were unfounded and still are. Despite the bailouts, two wars, and stimulus income taxes have not increased a single penny since Clinton’s tax hike and they will probably never increase again thanks to huge demand for treasuries.

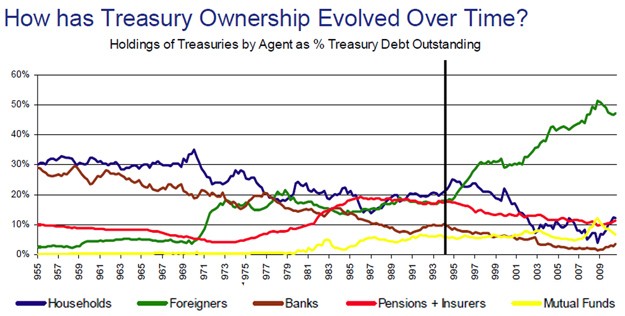

The chart shows below foreign ownership of treasuries has surged in the past decade, enabling the fed to keep rates low

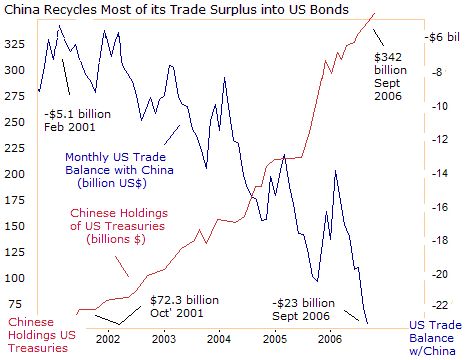

The next chart shows how China’s trade surplus depresses interest rates:

What about China dumping treasuries? Japan and China, whose economies depend on exports aren’t going to begin a trade war by dumping treasuries, so the politically unpopular trend of foreign government helping to subsidize ‘reckless’ spending will continue.

A huge bull market for stocks & web 2.0

The DJIA is poised to hit 17,000-20,000 within the next 2-3 years. By the time the interest rate cycle peaks at 4-6% the DJIA may be well above 50,000. The S&P 500 has already doubled from its March 2009 lows and interest rates still haven’t bunged. Bernanke may finally raise rates by a quarter or half point when the DJIA crosses 15,000.

Will there be a repeat of the 2008 commodities crash now that prices seem overheated again? Odds are no. It just so happened that the financial panic coincided as oil hit $150. The failure of several financial institutions, decline in confidence and the resulting stock market crash had nothing to do with oil. Unless there is a double dip commodities will continue their upward trajectory due to huge global demand, speculation, low rates. The unpopular truth is that surging commodity prices will not hurt growth, but may actually increase growth by forcing people to reduce their personal savings to purchase inelastic goods.

What if the fed begins to raise rates? Will this cause stocks and commodities to crash? No. Between 2004-2006 commodities, stocks, and interest rates rose together because rates were low relative to the expected/anticipated rates. When Bernanke does eventually get around to raising rates the rate hikes will be well-anticipated according to various prediction markets. Rate hikes cause deflation when they are unexpected and exceed the federal funds forecast rate.

The Facebook IPO will be a resounding success with the valuation rising to $200 billion within the first few months of trading. But it won’t be a bubble due to huge growth from facebook ads and its initially high PE ratio will rapidly contract as was the case with BIDU, GOOGLE, OPEN and other successful internet IPOs. The groupon and potentially a twitter IPO will be a similar success.

Usually what seems like a bubble isn’t. Remember the China economy ‘overheating’ talk of 2006? Or how Priceline, Netflix, and Baidu were overvalued last year? Those things still keep going strong and will continue to do so as long as the fundamentals of the economy remain strong.

Living expenses through the roof

Surging commodity and living expenses will result in even more populist angst (if that’s even possible), but have no negative impact on economy. The demand for food, energy, healthcare, education (the stuff rising the most) is considered to be inelastic. But the increased spending on these inelastic goods will translate into pure top line GDP growth without impacting elastic goods such as computers, appliances, and apparel. Thus, surging living expenses helps the economy and stock market by forcing consumers to spend more on these inelastic goods.

The personal savings rate will fall into negative territory like it did in 2008. We’ll see $5/gallon gas, $2000+/ounce gold, $150+ oil and parabolic charts for grains. Unlike in 2008 there will be no collapse; non-core components of the consumer & producer price index will keep rising, but treasury yields will rise only slightly confounding many of the experts like Peter Schiff who have been pounding the table about an impending ‘dollar crisis’ and hyperinflation. Technically there inflation, but it’s non-core inflation, which is the kind Bernanke and the bond market ignores.

Healthcare and college tuition costs will not relent. There will be no popping of the credit card or tuition bubble. The seismic shift in the labor market in the past decade to more technical, specialized jobs is contributing to the college boom.

Winner takes all economy

Companies that are market leaders today such as Facebook, IBM, Netflix, Apple, or Google will remain so long into the future. Large cap, globalist companies and high net worth individuals are the main beneficiaries of current economic policy. The system is one that seems to help those who have the most. if you’re out of college and have a lot of debt or out of a job don’t expect much help from the government. It’s a nation of huge personal debt but huge S&P 500 profits, too. The wealth gap will keep widening and wages continue will lag inflation. Healthcare, education, student loan debt, gas, energy, food will keep skyrocketing. It’s not fair and there’s nothing anyone can do about it. Buying and holding stocks, Euro, and commodities is one way to profit off dyseconomics. Or emigrate before the purchasing dollar becomes nonexistent and you’re stuck.

Job loss, unemployment not such a big deal

High unemployment has been shown to have a negligible to non-existent impact on consumer spending. Ref (http://www.savingpontiac.org/images/torturethenumbers.pdf ) According to msnbc Consumer spending was growing at the fastest pace in four years in the final three months of 2010 The S&P 500 consumer discretionary spider is well above its 2007 pre-recession highs. But the economic gains from high unemployment cannot be dismissed in the context of dyseconomics. High unemployment gives the fed a good excuse to never raise rates that the public will buy (the real reason is BRIC surpluses as explained earlier). High unemployment makes the remaining workers more productive which means higher profit margins. When consumers are less confident they are more productive, but still spending the same amount of money on essentials like gas and food as well as ipods, Netflix, Priceline etc. Spiking consumer confidence could be a bearish indicator for the markets. Finally, any weakness in American consumer & business spending from high unemployment is easily compensated by growing foreign business & consumer demand, and combined with a falling dollar you have a win-win situation for S&P 500 exporters. It’s not like the 80’s and 90’s when foreign markets were much smaller.

For the aforementioned reasons policy makers aren’t expressing much enthusiasm for getting people back to work. Also, No one can ‘force’ companies to hire more people. NO publics works, no shovel ready projects.

Wall st. and the fund managers don’t care about unemployment or housing because the economy in terms of earnings, exports and profits is doing great. That’s what matters from an investor’s standpoint. If you’re a trader a failsafe strategy is to buy the dip of any job news related selloff.

Unemployment will remain above eight percent for remainder of the decade, and may exceed ten percent if more people look for jobs. Their efforts will prove mostly futile as outsourcing, productivity, and technology means fewer workers needed. The baselines unemployment will settle at 7-8% and the total US labor force will continue to shrink. Structured labor tracked by the government will continue to be replaced by underground work.

Conclusion

Even with mainstreet is sitting on the sidelines the US economy now is stronger than it was at any other time in history thanks to dyseconomics. Permanently low interest rates combined with booming earnings and profits makes for a formidable bull market.

Cetin Hakimoglu is a stock market, macro economics, and mathematics enthusiast who operates a financial news aggregation website http://iamned.com/ and a personal math page http://iamned.com/math/

Copyright © 2011 Cetin Hakimoglu - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.