Forecasts, Commentary & Analysis on the Economy and Precious Metals

Commodities / Gold and Silver 2016 Jul 01, 2016 - 06:40 PM GMT

Shanghai settles 96% of gold trades in physical metal

Shanghai settles 96% of gold trades in physical metal

Absorbs 90% of global gold mine production

In the World Gold Council's Gold Investor magazine, Jiao Jinpu, Chairman of the Shanghai Gold Exchange, reports that "In its first month, the Shanghai Gold Benchmark Price’s trading volume was 105.91 metric tons of gold kilo bars, corresponding to a turnover of [renminbi] 27.94 billion and an average daily trading volume of 4.81 metric tons. 102.10 metric tons of gold were physically settled, addressing the market’s need for physical gold."

In The China Syndrome article series, I emphasize the physical nature of settlements on the Shanghai Gold Exchange as a requirement that will have significant impact on the gold market in the years to come. This quote from Jiao Jinpu verifies the strict application of physical settlement. Over 96% of the volume on the SGE is settled in physical metal. Speculation on the price sans delivery, which drives activity on New York's COMEX, is discouraged on the SGE.

Jiao goes on to describe how the Shanghai benchmark influences derivative contracts within China. Gold contracts, he says, including leases, derivative contracts of various kinds, and commercial banks savings and accumulation plans, are based on the benchmark price. The physical price arrived at on the SGE transfers, in turn, directly to derivative contracts. In other words, the dog (physical gold) wags the tail (derivative gold) in China's gold market, and by extension, can have a ripple effect on the rest of the global gold market.

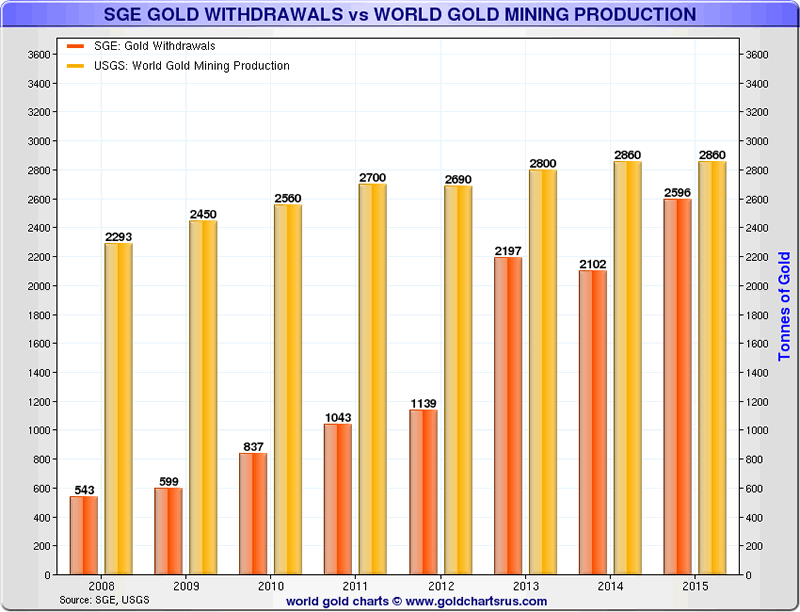

The chart at the top of this section (courtesy of Sharlynx.com) illustrates China's impact on the flow of physical metal in the global marketplace. In 2014, 73.4% of the gold mined globally ended up in the hands of Chinese investors, banks and its treasury reserves. In 2015, 90.8% of the gold mined went to China – up from 23.7% of production in 2008. In short, the rest of the world for the most part relies upon above-ground sources for its gold metal.

On several occasions since the SGE benchmark started, Chinese investors and traders drove the price to higher levels that carried over to London and New York as the day progressed. (I should note that Chinese traders can also drive the price lower.) As the first major market to open in any given 24-hour period, China is positioned strategically in the daily cross-global flow of gold business to influence trading for the rest of the day – including in the London and New York markets. Thus far, Shanghai has generally affirmed the trend in other markets or reversed down trends to the upside. We have yet to see a situation where Shanghai drove the price significantly lower.

Since all settlements are in physical metal, sellers will need to have a line on real metal in order to settle their side of the contract, not a paper promise. Already we have had reports of London bullion traders having to buy metal in Switzerland – the reverse of the prior relationship when London was the major seller to Swiss refiners. That might very well be due to the extended influence of the new Shanghai benchmark and "the need for physical gold in China," as Jiao pointedly reminds us. Four Chinese banks now hold seats on both the Shanghai and London benchmarks and are well-situated to bridge arbitrage opportunities between the two markets.

This newsletter has provided cutting-edge coverage of the gold and silver markets for over 25 years. Its content is widely quoted, re-circulated and sourced at websites all over the world. Its principal objectives have always been the same – to keep our clients informed on important developments in the gold market, condense the available gold-based news and opinion into a brief, readable digest, and, most importantly, to counter the traditional anti-gold bias in the mainstream media. That formula has won it a five-figure subscription base. If you would like to become a subscriber, we invite you to sign-up at our registration page. There is no charge for the service and your participation is welcome. This issue is published in the clear to provide as an introduction to prospective readers. Future issues will be available only through the subscription service.

Nascent Chinese silver demand

One of the conclusions one might draw from the SGE withdrawals/global gold production chart is that China could be running out of sources. That observation coincides with recent reports that Chinese mining companies are aggressively seeking to acquire gold mines outside its borders. China is already the top gold producing country in the world.

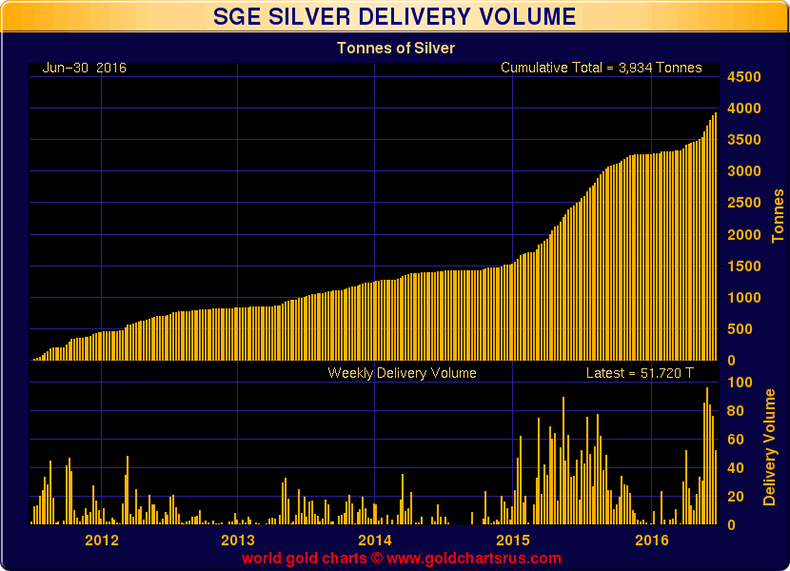

Another twist to the topping scenario is that China may have put its foot on the accelerator with respect to purchases of gold's sister metal, silver, as a way to augment its gold acquisition program. As you can see by the chart immediately below, silver deliveries have rocketed higher in China over the past two years – a development widely neglected by the financial media. Take a look at the ramp-up of physical demand in China over the past two years (bottom bar chart). China's quiet, nascent interest gives credence to silver's graduation from commodity status to monetary metal utilized by many investors as an asset of last resort, i.e., the other metal that functions as an asset that is not someone else's liability.

"You say: 'I did not think it would happen.' Do you think there is anything that will not happen, when you know that it is possible to happen, when you see that it has already happened?" - Seneca, 62 AD

The Brexit vote has come and gone, but the after-shocks remain. A good many will look upon the event as a black swan, but by definition it is not. For an occasion to gain black swan status, it must be at the minimum (a) unforeseen, and (b) bring extreme consequences. Those are the two criteria originally advanced by economist Nicholas Taleb who coined the term. Brexit misses on both counts. Though a surprise to much of the public, it was foreseen by many including a number of hedge fund operators who placed significant bets on the outcome. As for the consequences, they were troubling but fall short of being extreme. In fact much of the result is still pending.

All said, though, it would be a mistake to believe that the storm has passed without a major incident. Henry Kissinger warns that "The impact of the British vote is so profound because the emotions it reflects are not confined to Britain or even Europe." Alan Greenspan described the current financial environment as "the worst period I recall since I've been in public service." In other words, we are probably closer to the end of the beginning than the beginning of the end, to borrow Winston Churchill's famous admonition.

(One wonders which side the great wartime British prime minister might have taken on the Brexit question. I did see an interview of his grandson, Nicholas Soames, and in it he said there was no doubt in his mind that his grandfather would have come down on the side of Remain. I, for one, am not certain on that. If Winston Churchill was anything, he was an unwavering defender of British sovereignty. For many in the Conservative Party of which Churchill was a member, the whole Leave argument centered around the issue of self-determination.)

Though Brexit itself might not have been a black swan event, the public disaffection that drove it might be. That is where gold and silver once again enter the picture. Needless to say, precious metals demand went through the roof in the United Kingdom following the Brexit vote. Now, in the wake of severe credit rating downgrade and a collapse of pound sterling, that demand is likely to become entrenched for the long run. The Bank of England will do everything it can to smooth the way for Brexit, but we are in a time when central banks are not as capable of pulling rabbits out of the hat as they once were.

Outside the United Kingdom the flight to gold will likely gain pace simply because a good many investors around the world will conclude that the United Kingdom is not alone in either its politics or its economics. Black swans might someday paddle on both sides of the pond. The investor who is properly diversified might be surprised by an event like Brexit (or any further dislocations), but his or her portfolio won’t be.

Hedging Caesaropapism

“Brexit," writes the Telegraph's Ambrose Evans-Pritchard, "is not the cause and this is not contagion. The latest Pew survey shows that anger with Brussels is just as great in most of Northwest Europe as it is Britain, and in France it is higher at 61pc. This referendum was never a fight between Britain and Europe, as so widely depicted. It was the first episode of a pan-Europe uprising against the Caesaropapism* of the EU Project and its technocrat priesthood. It will not be the last.” I would add to Evans-Pritchard's assessment that the Trump and Sanders phenomena reflect the very same mind-set at work in the United States.

At the moment, the effects are largely political, but it will not be long until the markets begin to reflect the economic and financial backwash in a very real way. The immediate knee-jerk reactions in global stock and bond markets (negative), as well as the gold market (positive), might in future years be viewed as fractal events that foreshadowed the greater instability that followed.

If the "uprising" is going to generate an economic effect, it will likely be in bond ratings. Indeed one of the immediate casualties of the Brexit vote, along with a crash in pound sterling, was a downgrade in Britain's sovereign debt by the major rating services. "We take the view," says Standard & Poors, "that the deep divisions both within the ruling Conservative Party and society as a whole over the European question may not heal quickly and may hamper government stability and complicate policy making on economic and other matters."

|

|---|

Solidus, Byzantine Empire Constantine IV, 654-668 AD Courtesy of the British Museum |

If one reads between the lines in that statement, Standard & Poor's sees Britain as likely to proceed even deeper into the disinflationary tangle and the associated systemic risk that has become the new normal. The event that pushed gold to its all-time highs at over $1900 per ounce, we might recall, was Standard & Poor's downgrade of U.S. debt in August, 2011. Prior to that top-end spike, gold had already proven its wherewithal as a disinflation hedge in the wake of the 2008-2009 financial crisis – a performance that took a good many analysts and investors by surprise.

By the way, in the same interview quoted in the previous section, Alan Greenspan called for a return to the gold standard. In the past, he has publicly advocated private gold ownership saying "Gold is a good place to put money these days given its value as a currency outside of the policies conducted by governments." As reported in our last issue, Mervyn King, former governor of the Bank of England, has similarly recommended the safety of gold.

It has been said many times that in the absence of a gold standard, the judicious thing to do is to put one's self on the gold standard by purchasing physical gold coins and bullion. It is a matter of more than passing interest that two the most respected central bankers in the present era – two individuals with an intimate knowledge of the workings of the contemporary global economy – would resolve the complexities involved by suggesting gold as a workable option for private investors.

*Editor's note: Wikipedia explains Caesaropapism as "a political theory in which the head of state, notably the Emperor ('Caesar', by extension a 'superior' King), is also the supreme head of the church ('papa', pope or analogous religious leader)." To stretch Evans-Pritchard's analogy, the Brussels bureaucracy with its "technocratic priesthood" becomes the modern equivalent of the medieval Vatican. Britain's exit from the European Union, it follows, could be likened to Henry VIII's renunciation of the Roman Catholic Church – another chapter in history when Britain led the way in a much more inclusive and cross-border schism with long-lasting effects.

What others are saying. . . . .

The rush to gold

"George Soros is buying gold. Donald Trump is talking about reneging on a portion of U.S. debt, which some of his rationalizers interpret to mean unleashing inflation to drive down its value. Bill Gross talks about a bond-market supernova getting ready to blow. Peter Thiel speaks of an unsustainable government debt bubble. Today’s ultra-low, even negative, interest rates and apparently low inflation are taken for granted by the secular stagnation theorists, who believe the status quo will persist for years and years. It’s a view that seems implausible in light of the industrial world’s debts. The path may be crooked, but the way ahead seems clear: Governments will increasingly pay their bills and expand their spending not with the fruits of the productive labor of taxpayers but by printing money. Inflation is inevitable."

Editor's note: I'm not certain if Holman Jenkins has it right or wrong with respect to inflation's inevitability. In the end, it comes down to whether or not you as an investor/saver have taken the steps to protect yourself. If you have, the whole debate on where we might end up as a result of the current economic quandary becomes an academic matter – more something to occupy the mind like a challenging puzzle, than something required as matter of financial survival. Soros owns the ETF so he obviously believes the price is going to rise. What we do not know is whether or not he owns gold in the form of coins and bullion stored safely away in some depository somewhere – as a defensive holding. My guess is that he probably does given the litany of concerns he addressed in another Wall Street Journal article published earlier this month. (For an overview, go here.) Betting on the price simply is not enough when you come to this kind of world view.

Soros on Brexit – "EU. . .heading for a disorderly disintegration"

“The pound plunged to its lowest level in more than three decades immediately after the vote, and financial markets worldwide are likely to remain in turmoil as the long, complicated process of political and economic divorce from the EU is negotiated. The consequences for the real economy will be comparable only to the financial crisis of 2007-2008. . .That is where we are today. All of Europe, including Britain, would suffer from the loss of the common market and the loss of common values that the EU was designed to protect. Yet the EU truly has broken down and ceased to satisfy its citizens’ needs and aspirations. It is heading for a disorderly disintegration that will leave Europe worse off than where it would have been had the EU not been brought into existence.” – George Soros (Link)

Editor's note: The overall instability likely wrought from the fiery furnace Europe will have its most direct effect in bond ratings on the various European countries, and possibly beyond. That in turn will create margin calls and sell-offs to meet those calls. The net effect could be a repeat of 2007-2008 and once again, it could come without warning. Needless to say, there will be a good many trying to get ahead of the curve – a circumstance that brings the future present. The central banks, as promised immediately after the vote, will supply whatever cash is needed to stifle any emerging financial panic, but that will only further fuel the effects of the sell-off and, to some extent, the flight to the safety found in assets that are not someone else's liability.

Global economy not a theoretical petri dish

"There are laws that prevent the medical industry from adopting experimental procedures before they become, well, less experimental. To not have those laws in place would be dangerous. Experimental procedures can produce unintended consequences and their efficacy must be rigorously tested before wide release and adoption. So as a society, we do not let doctors perform experimental procedures on everyone who walks through the hospital doors.Yet for some reason, there are a lot of PhD holders from a different industry who are doing just that to entire nations and economic zones. This isn’t a theoretical petri dish. It’s the global economy." – Gregory Marks, Citi FX analyst, Let's Take Stock: The Efficacy and Merit of Negative Rates

Editor's note: The point of Marks' anti-central bank salvo is that even the best of minds with the best of intentions can occasionally lead the populace over a cliff. The standard advice to diversify against such malpractice with gold and silver is simplistic, and it does not require an advanced degree to understand. Yet, it is as effective now as it was in the time of the French assignat inflation in 1789, the nightmare German inflation in 1923, and Zimbabwe's 79.6 billion per cent inflation rate in 2008 – all examples of the unintended consequences resulting from monetary policies gone awry. Those times too were visited upon the population by a misguided intelligentsia with the best of intentions. The enlightened minority who diversified with gold and silver came out the other side a bit ruffled from the experience but pretty much financially intact.

By Michael J. Kosares

Michael J. Kosares , founder and president

USAGOLD - Centennial Precious Metals, Denver

Michael J. Kosares is the founder of USAGOLD and the author of "The ABCs of Gold Investing - How To Protect and Build Your Wealth With Gold." He has over forty years experience in the physical gold business. He is also the editor of Review & Outlook, the firm's newsletter which is offered free of charge and specializes in issues and opinion of importance to owners of gold coins and bullion. If you would like to register for an e-mail alert when the next issue is published, please visit this link.

Disclaimer: Opinions expressed in commentary e do not constitute an offer to buy or sell, or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. Centennial Precious Metals, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such USAGOLD - Centennial Precious Metals does not warrant or guarantee the accuracy, timeliness or completeness of the information found here.

Michael J. Kosares Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.