Trading The Global Future - Bad Consequences

Economics / Global Economy Sep 15, 2018 - 08:36 AM GMTBy: Dan_Steinbock

The Trump administration’s ‘America First’ policies come at a critical time in the global economy. These bad policies will have adverse consequences in international trade. In the absence of countervailing forces, they could unsettle the post-2008 global recovery and undermine postwar globalization.

The Trump administration’s ‘America First’ policies come at a critical time in the global economy. These bad policies will have adverse consequences in international trade. In the absence of countervailing forces, they could unsettle the post-2008 global recovery and undermine postwar globalization.

This summer, the Trump administration’s tariff war penalized $50 billion worth of goods traded between the US and China.

The next stage of White House escalation will impact up to $200 billion of Chinese imports, and result in proportionate Chinese retaliation.

If the White House opts to expand its tariff wars even further, collateral damage is likely to spread from goods to services and advanced technologies.

Damage Spreading from Goods to Services

Not so long ago, there was still serious talk about the US-China Bilateral Investment Treaty (BIT). Chinese foreign direct investment in the US soared to a record $46 billion in 2016, creating American jobs and injecting capital into the US economy.

Yet, last year Trump threats caused Chinese investment in the US to plunge to $29 billion, due to deleveraging in China and stringent US regulatory reviews of inbound acquisitions. After months of trade wars and asset divestitures, China’s net US direct investment was negative in the first half of the year.

Historically, advanced economies have tended to enjoy service surpluses and goods deficits in trade. US-Chinese trade is no exception. Since 2001, US services surplus with China has increased nine-fold. Last year, US goods exports to China totaled $130 billion, whereas imports from China equaled $506 billion. However, US services exports to China amount to $58 billion, while services imports from China are $17 billion. Consequently, while the US runs a goods deficit of $375 billion with China, it runs a service surplus of $38 billion.

As China exports far more goods to US than vice versa, Chinese retaliations already cover more US goods (85%) than US tariffs cover Chinese imports (50%). Consequently, the ongoing trade war is shifting from goods tariffs to non-tariff actions in services. While China has tried to avoid escalation, US battle over services trade has already begun, but with Brussels. As German Chancellor Angela Merkel has noted, it is misleading to focus on goods trade, in which the US has deficit with the EU, when the US excels in services trade, in which it has a surplus with the EU. Together with other EU leaders, Merkel is backing a “digital tax” against US multinationals including Amazon, Facebook and Google – companies that have come under fire for shifting earnings around Europe to pay lower taxes.

Trump’s tariffs have potential to undermine America’s most important competitive advantage in the postwar era: high-value, high-margin services, which range from advanced technology to pharmaceuticals. As collateral damage spreads, so will the costs. As US metropolitan centers take severe hits, the stakes will be much higher for US states, particularly California. And if trade wars continue to spread, neither Silicon Valley nor Hollywood will remain immune. Global economy does not thrive in insulated fortresses.

Chinese responses

For now, the full impact on Chinese banks and corporations is still likely to be limited. The US accounts for only 15% of China's goods exports, and China's domestic activity now fuels its economic growth, not its net exports as in the past. However, since there are no winners in trade wars, China, too, is beginning to feel the pain.

How is Beijing responding to the Trump tariff wars? The simple answer is that the White House has left Beijing few alternatives but to target those US export sectors that will suffer the most. In 2017, US exports to China soared to $130 billion. Only ten export groups accounted for more than half of the total, starting with civilian aircraft and engines ($16bn), soybeans ($12bn), passenger cars ($11bn), and semiconductors ($6 bn) (Figure 1).

Figure 1 US Exports to China, 2017 ($ Billions)

Source: US Census Bureau

To protect its interests, China has resorted to the WTO dispute settlement mechanism but has also taken measures of equal scale and strength against US products. Current tit-for-tat responses include targeting soybeans in farm states. US agricultural exporters supported Trump’s social policies, but their livelihood relies on free trade. Meanwhile, decades of trust have diminished in a matter of months. To China, the US is just one agricultural exporter among others; to US farmers, China is the key importer. In negative scenarios, they face a permanent loss of market share in China.

Moreover, China can raise the stakes by banning the import of genetically modified products from the US, which are already opposed by many countries. China can – and has – deferred trade and investment deals that were signed during Trump’s previous visit to China. As the Trump administration is obstructing Chinese investments in the US, China could resort to tougher measures as well, including by enacting restrictions on imports of US services.

Further measures would include Chinese currency valuation, although that could undermine the ongoing internationalization of the Chinese renminbi and revive the dated “currency manipulation” debates. Far more consequential would be a Chinese move to sell part of its US Treasury bond stockpile. Things could get even worse if the relatively rapid increases of gold reserves in Russia, China, and other economies herald new challenges against the US dollar hegemony at the time that concerns over US stability are mounting worldwide.

As stakes are upped, China is running out of US imports for penalties in response to Trump's tariff hikes. Consequently, Beijing is now putting off accepting license applications from US companies in financial services and other industries until Washington makes progress toward a settlement. That’s how the trade pain is now spreading from farmers in Iowa to US Chamber of Commerce and US business groups in China. If tariff wars prevail, the nightmares have only begun.

Despite retaliations, China continues to push for diplomatic negotiations, along with efforts to import more American cars, aircraft, and natural gas, while promoting reforms in its financial sector. Moreover, a bilateral compromise could also pave the way to new talks if Republicans lose their dominant Congressional position in this fall’s midterm elections.

Toward New Globalization?

Today, as US-led globalization by advanced economies is winding down, China-fueled globalization, which is driven by emerging and developing economies, has emerged as a complement. This is illustrated by Chinese longer-term efforts to achieve free trade in Asia Pacific, the creation of new multilateral development banks targeting the needs of emerging economies, and China-supported globalization.

While Trump favors bilateral trade talks to maximize US leverage, most nations today believe in multilateralism and regional trade negotiations. Ironically, the Trump trade war has intensified efforts at more inclusive trade in Asia Pacific. This has inspired even advanced economies in the region to take another look at trade agreements, such as the Regional Comprehensive Economic Partnership (RCEP), which were initially designed for emerging and developing economies.

In the long run, China is pushing for the Free Trade Agreement of Asia Pacific (FTAAP), which - ironically - was initially developed in Washington, until President Obama replaced it with a geopolitical pivot to Asia and the Trans-Pacific Partnership (TPP) that excluded China.

And as ‘America First’ policies surge in Washington, the attractiveness of the Asian Infrastructure Investment Bank (AIIB) and the BRICS New Development Bank (NDB) has significantly increased in emerging and developing economies. Yet, instead of participating in and benefiting from these initiatives, both the Obama and Trump administrations, in contrast to their trade partners and even NATO allies, have opted to remain uninvolved. Similarly, the China-led One Belt One Road (OBOR) initiative has been open for US participation, yet America has kept its distance.

The new initiatives of the Trump administration suggest that its goal may be to contain China’s economic rise, divide Asia, or both. On July 30, US Secretary of State Mike Pompeo gave a highly-anticipated speech on “America’s Indo-Pacific Economic Vision.” Pompeo announced $113 million in new US initiatives to “support foundational areas of the future" in the regional economy, energy, and infrastructure. This vision is a rehash of ideas that former Secretary of State John Kerry introduced in 2013 when the idea of the Indo-Pacific Economic Corridor was conceptualized few years ago.

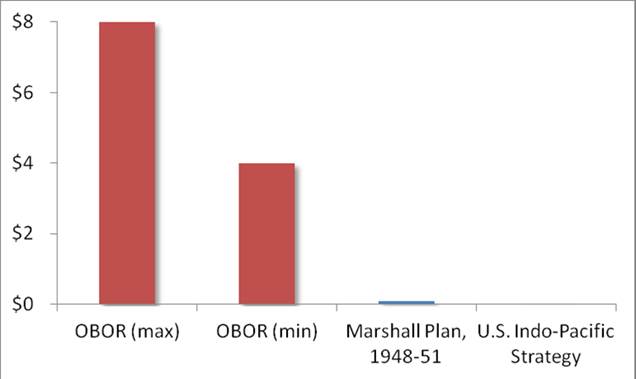

The scale of the US ‘Indo-Pacific Economic Vision’ and the Marshall Plan, which Pompeo alluded to, pale in comparison with the OBOR. While there is no consensus on exact historical amounts, the Marshall Plan’s cumulative aid may have totaled $12 billion (over $100 billion in today's dollar value.) Consequently, Trump’s much-touted Indo-Pacific Strategy represents less than 10% of the value of the Marshall Plan 70 years ago. The OBOR involves far greater cumulative investments estimated at $4 trillion to $8 trillion, depending on timelines and scenarios (Figure 2).

Figure 2 Indo-Pacific Vision, Marshall Plan, and China’s OBOR

* Estimates expressed in trillions of contemporary US dollars. China’s One Belt One Road (OBOR) initiative features both maximum (OBOR, max) and minimum (OBOR, min) estimates, based on relevant literature.

Three Scenarios

It is the hope for a better future in the emerging world associated with the OBOR that remains most underestimated in Washington. What Asia really needs is a sustainable, long-term plan for accelerated economic development - not new geopolitical divisions.

Where will the current tensions lead,? At the broadest level, the outcome of the Trump tariff war can be compressed into three generic scenarios, which are defined by their strategic objectives, de facto execution, and associated economic costs.

Scenario 1: Muddling Through

The first scenario is neither a win-lose nor a win-win strategy. It does not represent postwar multilateralism, but post-Cold War unilateralism, as reflected by the FTAs that were dictated by unipolar geopolitical primacies rather than multipolar economic opportunities. It is what the Obama, Bush, and Clinton administrations relied on. In the Trump era, this scenario was initially supported by those business constituencies and voters the White House is now alienating.

As for economic consequences, with $50 billion impacted, the tariff’s impact would probably have been limited to 0.1% of Chinese and American GDP. It is a scenario that most Americans would have supported - but it wasn’t enough for the Trump administration.

Scenario 2: “America First” Protectionism

This win-lose strategy it is not Trump’s invention. After US recovery from the 1929 market crash failed and the economy drifted into the Great Depression, Congress passed the Smoot-Hawley Tariff Act. Yet, the high tariffs only worsened the Great Depression, further contributing to the international turmoil.

Currently, the stakes of the Trump tariff war against China are about to rise to $200 billion. With such elevated stakes, the collateral damage would quadruple relative to the first scenario. In China, it would shave off 0.4% of the GDP; in the US, it would likely amount to 0.8% of GDP. If the stakes increase to $500 billion, the net impact would increase 10 times from the first scenario. While China would take a hit of 1.0%, the US would suffer a net impact of 2.0% of GDP. That could unsettle key stock indexes on Wall Street and unleash substantial volatility, while disrupting the Federal Reserve’s tightening and a strong US dollar.

In the long run, the worst impact of this scenario is that it is mitigating much of the bilateral trust between Beijing and Washington, and between ordinary Chinese and Americans. It took half a century to build that trust; quantitative GDP percentage points cannot capture it.

Scenario 3: Multipolar World Trade

This is the win-win strategy. There is no reason why the United States, along with U.S. multinationals, states, and municipalities, could not cooperate with large emerging economies, including China. When Great Britain lost its leading position in the world economy, it did not respond by rejecting US-led Bretton Woods, staying out of the World Bank and the IMF, taking distance from the UN and withdrawing from international agreements, or by seeking to undermine the US dollar and to contain the rise of the US economy while seeking to divide US alliances. London understood that its future was aligned with the US and the world economy.

It is by participating in the new initiatives put forward by China and other emerging economies that US economic interests can gain an appropriate voice in their realization. Instead of projecting economic penalties, the third scenario would entail positive outcomes and spillovers. US participation in the NDB and AIIB would open new markets in Asia and the emerging world at large, just as US participation in the OBOR initiative would ensure access to other markets that Washington has long hoped to access, but peacefully, without sanctions, destabilization, and regime changes. In Asia, the renewed talks over free trade in Asia Pacific (FTAAP) could create the greatest trading sphere the world has ever seen.

Today, the third scenario feels utopian because it contradicts much of what the Trump administration stands for. But it is the only viable way to the future.

In August, the “new export order” sub-index in China’s official purchasing manager index, which is used to gauge China’s export sector’s health, fell by 0.4 points to 49.4; the lowest since the escalation of bilateral tensions with the US However, its mirror indicator; the import sub-index also moderated by 0.5 percentage point to 49.1; the lowest since mid-2016.

Thanks to a new thaw in Chinese-Japanese relations, the trade negotiators from 16 likely signatories of the China-supported RCEP agreed on key elements of a deal, which could result in a broad agreement by November.

Dr Steinbock is the founder of the Difference Group and has served as the research director at the India, China, and America Institute (USA) and a visiting fellow at the Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more information, see http://www.differencegroup.net/

© 2018 Copyright Dan Steinbock - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Dan Steinbock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.