Credit Crisis Worse to Come as U.S. Mortgage Resets Continue

Housing-Market / Credit Crisis 2008 Oct 06, 2008 - 07:15 AM GMTBy: David_Haas

We are often told through the mainstream media that “the worst is behind us now” with respect to the credit crisis and that much of the blame for the crisis in the first place can be attributed to defaults on sub-prime mortgages, a meltdown in housing-related credit instruments, and plummeting housing values in many local markets across the USA.

We are often told through the mainstream media that “the worst is behind us now” with respect to the credit crisis and that much of the blame for the crisis in the first place can be attributed to defaults on sub-prime mortgages, a meltdown in housing-related credit instruments, and plummeting housing values in many local markets across the USA.

If we accept that our domestic housing markets are the primary driver for the global credit problems - problems that seem to have somehow morphed into a gigantic, global, credit-eating monster - then we need to be actively monitoring the overall health of the domestic U.S. housing markets to determine where we may be in this painful cycle.

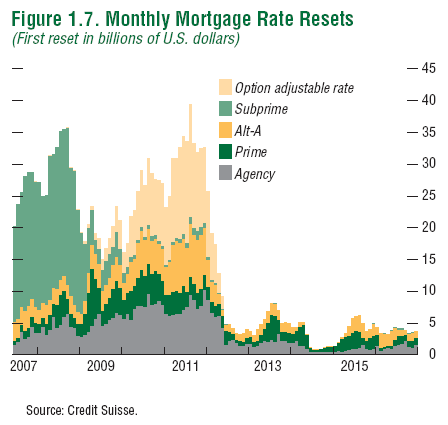

In case you haven't seen it, I'll first present a graph that is widely available on the web that depicts the approximate composition of the Adjustable Rate Mortgage (ARM) market along with when these mortgages might be subject to a rate reset:

I like to view this graph as a road map that we're forced to follow into the future. Our route has been prescribed for us by past market actions and it has been assured by valid contracts that are still in effect. So, there isn't likely to be much meaningful change in our course unless the contracts are modified or recast en masse to protect the remaining lenders in the financial system. We don't appear to be moving in that direction yet.

When looking at the above graph, we can see that a large portion of “wave 1″, the sub-prime problem, has now passed and it's obvious from reading about the sorry state of the global financial system that the sub-prime debacle was a serious miscalculation made by the “financial geniuses” that has already caused colossal problems for all of us.

The reality is more likely to be that there were plenty of other serious systemic weaknesses brewing for many years and sub-prime was just the straw that broke the camel's back. By headlining and blaming “sub-prime” debtors, the heat has been kept off of the bankers, brokers, and complacent regulators where the fault really lies. The real problems are/were systemic and the sub-prime problem was merely a symptom thereof.

Now, in order to put the RESET SCHEDULE to its best use we need to look at what is yet to come over the next few years and try to make some reasoned guesses about what seems most likely to happen as a result of it. The first thing I see is that 2009 appears to be a year that could present a modest reprieve in ARM reset activity. 2009 may serve (best case) as a year when the financial system is able to sort itself out, digest and consolidate its losses, formulate plans for recapitalization and rebuilding of confidence, and begin attracting the massive new investment needed to build a base for meaningful recovery.

Any successful plan will need to address how to effectively manage “wave 2″ of the ARM reset problem which is the wave that arrives in 2010 with Pay-Option ARM's and Alternate-A paper (liar loans) leading the way. You can see on the graph that waves 1 and 2 are approximately equal in scale. This might seem to imply that we are about two fifths of the way into this maelstrom at the end of 2008.

It is my best hope that our global leaders' current actions lead to a successful navigation of this crisis leading to only a moderate recession (we're already there) and a return to normalcy and prosperity within the next 3 to 5 years, with critically-important lessons learned. But this is only hope.

At the other extreme, I can imagine financial devastation on a scale that would resemble what the tsunami brought to Thailand or hurricane Katrina inflicted on the hardest hit parts of Louisiana. Picture little recognizable bits and pieces of the “old system” lying around in various states of ruin and disrepair - structures knocked off their foundations, many completely destroyed and scattered - with nothing readily brought back to full functionality for months or even years, masses of people totally dependent upon outside assistance and government aid, lives turned upside down perhaps forevermore.

Certainly, under this scenario, a full recovery would take a decade or more to achieve ASSUMING all the tools (social stability and order, stable national currency, stable and continuous government, ready access to investment cash and credit, supportive will of the people, responsible and capable leadership, peace, ability to feed, clothe, and house the masses of unemployed, etc.) were available for rebuilding. If ANY of these tools are missing, all bets are off. I pray this scenario is not one that unfolds.

Probably, the most likely scenario will emerge somewhere between the two extremes I've outlined. It may present bits and pieces and degrees of each scenario, depending on how severely a country or region is impacted by the financial meltdown. Some areas will fare much better than others. As we're seeing now, each country of the world is feeling the effects differently and I expect this will continue as the crisis evolves.

What I've shown so far (ARM resets) is just part of the story, however. There's one critical part of our analysis that can't be missed and that is the role that real estate prices will play in the above scenarios. One thing that is often mentioned is that many of the problems above can be resolved by borrowers simply refinancing out of an ARM that is resetting at a higher payment. For some lucky people, this is entirely true and, hopefully, many of them have preemptively secured a fixed rate mortgage already.

But there are many factors involved in refinancing. Here are a few obvious ones:

1. Adequate appraisal on current market value of home to support mortgage

2. Stable income and long-term employment

3. Moderate to strong credit score

4. Favorable income to debt-service ratio

5. Verifiable additional financial reserves and resources

Unfortunately for many holders of ARMs, one or several of these factors has seriously slipped over the course of the past year IN ADDITION TO THE FACT THAT mortgage lending standards have become extremely tight due to the crisis itself. Banks have little money to lend since they're busy trying to shore-up their capital base and they must make only the most secure loans.

During the 2003-2007 period, many people worked in jobs and industries that were related closely to housing, real estate, construction, and finance. Obviously, millions of these people have been hit hard with the slow-down and would no longer be in a position to qualify for a refinance. Their jobs may be gone for good. Millions more have exhausted their financial reserves and have begun falling behind on some monthly obligations that have impacted their credit scores - meaning they will not qualify for refinancing under the current strict lender requirements or, who may barely qualify but only at a much higher fixed interest rate due to their impaired credit.

But here's the biggest factor of all: If the property itself cannot appraise high enough to support the old indebtedness plus the refinance costs, the whole refinancing deal is dead UNLESS the borrower has the resources to bring the extra cash to the closing table. Huh? We're expecting these people who are already suffering from extreme financial duress in many cases to bring wads of cash to the refinance closing table? Errrgh, OK.

But how much might they need to bring? That, of course, depends on how much value their home may have lost. Here's the recent coast-to-coast authority on that subject, with compliments to Standard and Poors and Case-Schiller:

National Trend Of Home Price Declines

As noted in the report “Nevertheless, not one market is showing a positive return over the past 12 months and seven of the metro areas are reporting declines in excess of 20.0%. At the national level, the housing market peaked around June/July of 2006. As of June 2008, two years later, the 10-City Composite has fallen by 20.3% and the 20-City Composite is down 18.8%.”

This being the case, if the national median home price was $225,000, or so, in 2005-2006 when many of the ARMs were originated and home prices have dropped roughly 20% thus far, a “median” homeowner might be forced to bring an ADDITIONAL $36,000 IN CASH to close on his refinancing.

But what if there were home-equity loans taken or piggy-back 2nd mortgages used to “creatively” buy the house in the first place? Both of these were quite common if not typical. In these cases, say there was 100% financing in the aggregate, the homeowner would need to bring $81,000 IN CASH to close on his refinancing loan.

$225,000 - 20% Decline = $180,000 New Value

$180,000 X 80% Loan = $144,000 New Mortgage Offered

$225,000 - $144,000 = $81,000 Shortfall

And this is a relatively inexpensive home. The hyperactive markets, where most of these ARM loans were written, were in areas that had prices driven up much higher than the national median price. Prices of $500,000 to $2,000,000 were often more the rule than the exception in these areas.

Most of these people will not be bringing checks like these to closings on houses that no longer hold their original value. Adjust your expectations of the housing markets, the global financial markets, as well as your view of the above work-out scenarios accordingly. Hunker down and prepare for the full gamut of possibilities so you're able to weather the storm, regardless of its severity.

Think this is foreboding and ominous? Check back for my next post on financial derivatives and you'll begin, perhaps for the very first time, to understand the scale of what we're facing.

By David Haas

Consultant

In my consulting practice, I work with individuals, business owners, and professionals. I assist business owners and professionals in several critical areas ranging from business start-up, marketing, operational challenges, employee retention, and strategic planning to personal asset protection, financial, and retirement income planning. Often, these areas relate and need to be integrated to work most effectively. I also assist business owners in developing exit-strategies that enable them to maximize the value of their business interests and preserve their lifestyle in retirement. For individuals, I primarily focus on tax reduction, financial, and retirement income planning.

© 2008 David Haas, Consultant

David Haas Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.