U.S. Economy Heading for Japan of the 1990's or Argentina 2002?

Economics / Recession 2008 - 2010 Jul 02, 2009 - 05:29 PM GMTBy: John_Lee

Introduction: The inflation / deflation debate in the US is still alive and well. In deflation camp, there is the rising star du-jour Nouriel Roubini and old timer Robert Prechter. They argue the debt collapse would cause price deflation and depress world economies for years to come. The inflation camp includes Jim Rogers and Marc Faber, who said on May 27 2009 that "I am 100 percent sure that the U.S. will go into hyperinflation "

Introduction: The inflation / deflation debate in the US is still alive and well. In deflation camp, there is the rising star du-jour Nouriel Roubini and old timer Robert Prechter. They argue the debt collapse would cause price deflation and depress world economies for years to come. The inflation camp includes Jim Rogers and Marc Faber, who said on May 27 2009 that "I am 100 percent sure that the U.S. will go into hyperinflation "

The deflationists often talk about the two historic showcases - The 1930's US depression and Japan's lost decade of the 90's. In both of those cases, debt-fueled equity and real estate bubbles were gigantic and exceeded 100% of the GDP in size. The subsequent debt implosion caused 50%+ retrenchment in their respective equity and/or real estate markets.

While there are similarities in the cause of the bubble and immediate effect after the debt collapse, the long term economic outcome and survival can be very different. In this paper we will debunk the claim that US is facing an imminent 90's Japanese style deflation.

The Cause And Effect Of Deflation

Fractional-reserve monetary systems are inherently unstable. Money is created out of thin air by the banks and lent to government, consumers and businesses. In order to service and replay those debts, the borrowers take on more debts. Collateralized asset prices are inflated, and the vicious cycle continues until the debtors are unable to borrow or the banks are unwilling to lend. At that point the system snaps, everything is sold off, asset prices dive and we have a financial crisis at hand. The classical definition of deflation is the decrease in money supply. Although at times the rate of increase in money supply may slow, the actual money supply has never decreased in the fiat-money world we live in since 1913. Therefore, technically deflation is not a possibility. For the sake of discussion however, we will define deflation as "the decrease in the general prices of goods and services"

Japan of the 90's

Japan had an equity bubble and real estate bubble in the late 80's fueled by easy credit and excessive borrowing. The bursting of Japan's bubble economy in the early 1990s triggered an economic slump that has sometimes been called the "lost decade." The Nikkei stock index declined by more than 70%, and commercial land prices in large cities fell 82% from their peak, creating stockpiles of nonperforming loans. Altogether such loans were estimated to be in excess of US$2-$3 trillion, which is more than Japan's GDP.

Mortgage defaults and budget deficit in Japan

Throughout the crisis, the mortgage market was comparatively stable, as banks were willing to restructure the loans and defer payments. In Japan it is shameful to walk away from your home and mortgage, and fear of repossession kept default rates relatively low. In the 1990s, as interest rates fell default ratios did, too-from 2-3% to less than 1%. In 1990, Japan was running a balanced budget which created room for fiscal deficit spending. It wasn't till 1997 that budget deficit ran into double digit of GDP.

http://www5.cao.go.jp/zenbun/wp-e/wp-je01/wp-je01-00301.html

Current Account and External Debt in Japan

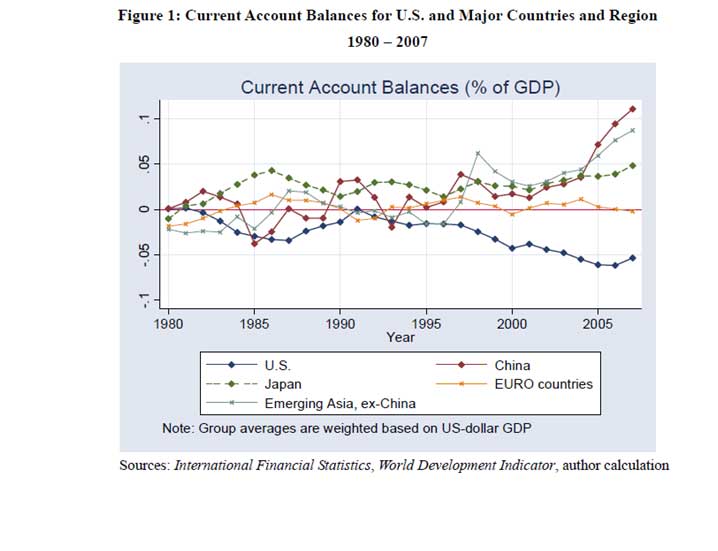

Japan long enjoyed current account surplus since 1982, and has little external debt owed to foreigners. The positive current account enables the government to expand spending without fear of inopportune foreign attacks on the yen through debt and stock redemption.

Japanese savings rate, the Yen,

Japan's national savings rate throughout the 90's exceeded 30% which created demand for the Yen.

During the same period, Japan was world's dominant creditor and the Yen was kept in high demand on the world stage. As shown in the chart below, the Yen appreciated 100% against the Dollar from 1990 to 1995. Purchasing power of the Yen was further enhanced through slow and painful deleveraging whereby world assets owned by indebted Japanese firms were sold to raise Yen to be repatriated.

Quantitative Easing in Japan

Quantitative Easing = Printing money to buy public and private assets (Treasury bonds, mortgage bonds, even stocks)

This is a direct attempt to prop up prices through money printing.

Faced with sluggish Japanese economy post-Nasdaq bubble, The Bank of Japan lowered the policy rate to zero in February 2001 and then went to quantitative easing the next month. It ended both quantitative easing and its zero interest rate policy only in 2006.

The size of the bond-buying operation became the policy tool to target the level of reserves rather than the policy rate, which was fixed at virtually zero. At its peak, reserves reached around Y35,000bn (US $300 billion) of which only around Y8,000bn were required.

Although a modest boost to GDP was observed through quantitative easing, the perceived growth came at the expense of the Yen. Indeed Yen lost nearly 20% against the dollar in just 12 months from the quantitative easing announcement. It doesn't take an academic to figure out that money printing resorts to depreciating currency and inflation, it not a matter of if but when.

It's interesting to note that Japanese understood the use of "quantitative easing" as last resort. Interfering prices so blatantly can cause irreparable damage to the currency, and the BOJ exercised this dubious demon power only some 11 years after initial debt bubble burst.

To summarize, Japanese lost a decade of progress in the 90's as it struggled to pay down domestic debts that's multiple times its GDP. The government began 1990 with budget surplus but expanded expenditures to eventually reach 10% budget deficit some 7 years later in 1997. 30% domestic savings rate coupled with positive current account balance provided support for the Yen, which enjoyed a formidable rise until 1995. The government didn't toy with unconventional monetary policies such as "Quantitative Easing" until 2001, a decade after the initial bubble burst.

USA Today

Avoiding this paper turning into Ph.D dissertation in length, let me summarize the USA section by saying that post bubble condition today in the US has almost nothing in common with that in Japan in the 90's.

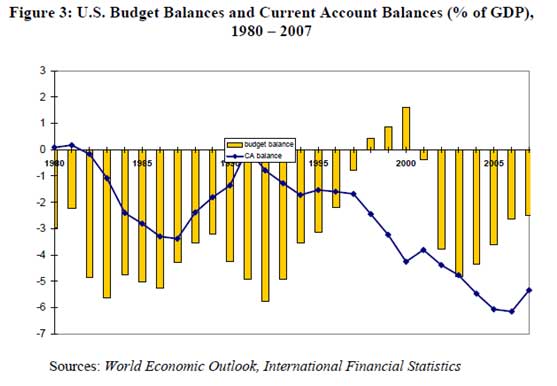

Japan entered into the crisis with a balanced budget, while US 2009 budget deficit is projected to be 12% of GDP. Such daunting budget gap is reserved mostly for 3 rd world countries. For example, during Argentina financial crisis in 2002, the country's budget deficit was only a "modest" 4.6% GDP.

What's most alarming - the US 12% budget deficit is only the beginning of a trend. Seeing all levels of government severely short on tax receipts, most analysts project the deficit to worsen further into future years.

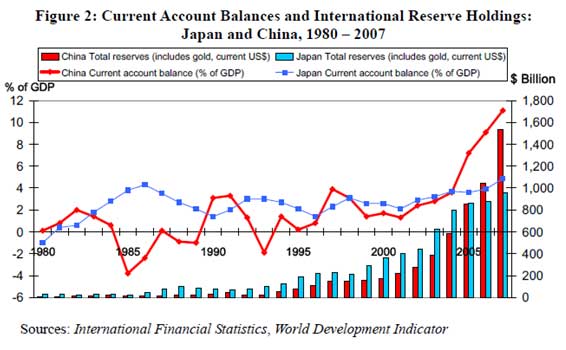

In the 90's Japan was world's top creditor nation whilst US today is the world's largest debtor nations with over $12 trillion owed to foreigners.

The following list from CIA shows US owing over $12 trillion to foreign residents as of June 2007.

1 United States $ 12,250,000,000,000 2 United Kingdom $ 10,450,000,000,000 3 France $ 5,370,000,000,000 4 Germany $ 4,489,000,000,000 5 Spain $ 2,478,000,000,000 6 Netherlands $ 2,277,000,000,000 7 Ireland $ 1,841,000,000,000 8 Japan $ 1,492,000,000,000

https://www.cia.gov/library/publications/the-world-factbook/rankorder/2079rank.html

In 2008, the US imported $670 billion more than it exported. The country requires foreign trading partners to re-invest all of that $670 billion to keep the dollar afloat. This means external debt would have to increase at least by similar amount just to keep the status quo.

China so far invested in $800 billion US treasury. What if they want to withdraw? Who can buy $800 billion worth of US treasury?

Quantitative Easing Revisited

"Who can buy $800 billion US Treasury notes from China?"

The Federal Reserve Bank is our savior and lender of last resort. The Fed is generous and has offered to buy US notes of all kinds.

To quote directly from Mr. Bernanke, chairman of the Fed

"U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation."

http://www.federalreserve.gov/BOARDDOCS/SPEECHES/2002/20021121/default.htm

I find it amusing that the deflation camp still exists after such statement. Since 2008 the Fed has bought over $2 trillion of soured notes issued by AIG's and the alike. To pick up the slack from wary demand of US assets by foreign creditors, the Fed recently affirmed the commitment to buy additional $1.7 trillion worth of MBS and US Treasuries.

It took 10 years after the bubble burst in Japan to take on quantitative easing. The US entered into financial crisis in 2008 and Mr. Bernanke is already prepared to print upwards of $4 trillion by the end of 2009.

How did the dollar react to the news? The dollar chart below shows a distinct bearish trend.

Often times, prediction arrives through the process of elimination.

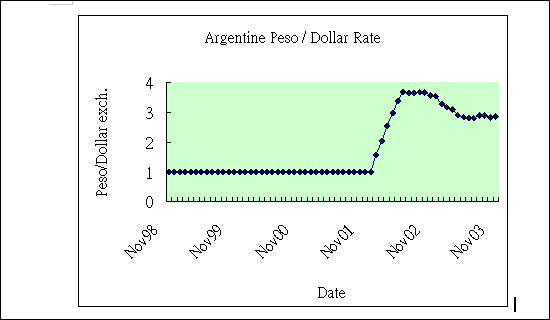

By now, it should be crystal clear that the immediate US path is NOT Japanese style deflation of the 90's. The path of concern is Argentine style hyperinflation of 2002. The chart below shows that the impaired peso was permanently devalued after the crisis.

The Savers Camp vs Borrowers Camp?

An average American family carries

- $9,000 in credit card debt, - $18,000 in debt and loans inclusive of credit cards, auto, and education - $70,000 in mortgage debt

Then there is borrowing by Uncle Sam. The $11 trillion national debt equates to over $31,000 per U.S. person.

If one sums up all recognized debt of federal, state & local governments, international, private households, business and domestic financial sectors, including federal debt to trust funds, the t otal Debt in America is over $57 Trillion, or $186,717 per U.S. person.

The foreigners own over $5 trillion of the national debt and over $12 trillion of all US debts. Even at 10% savings rate, it will take a full decade for US citizens to pay its foreign obligation.

With hundreds of $billions added to the external debt clock every quarter and a national savings rate of less than 7%, the fat lady may never sing and foreigners may never get the payback in full, in today's dollars anyway. With those stats in mind,

It's completely rational and clearly in the best interest of America to repudiate foreign debts and subject the dollar in harms way.

Foreigners don't have political representation in the US, so why would an average Joe work to pay foreigners? It's far easier to debase the currency.

Conclusion Buffet was quoted on May 2, 2009 --

Buffet warned that efforts such as the Treasury's $700 billion Troubled Asset Relief Program and the $787 billion fiscal stimulus plan passed this year by Congress will have to be paid for, one way or another. The biggest losers in a surge of inflation, Buffet added, would include holders of bonds and other fixed-income assets.

"I haven't had my taxes raised," said Buffett, who has run Berkshire for more than four decades. "My guess is the ultimate price will be paid by a shrinkage of the value of the dollar."

-- Greenspan was Quoted on June 26, 2009 --

Inflation is a special concern over the next decade given the pending avalanche of government debt about to be unloaded on world financial markets. The need to finance very large fiscal deficits during the coming years could lead to political pressure on central banks to print money to buy much of the newly issued debt.

The US is faced with the choice of either paring back its budget deficits and monetary base as soon as the current risks of deflation dissipate, or setting the stage for a potential upsurge in inflation.

http://www.ft.com/cms/s/0/786355f2-61ea-11de-9e03-00144feabdc0.html

--

The following gold chart speaks the same terms and seems ready for the next advance.

If you are in the savers camp, it's not too late to diversify out of dollars. Subscribe to our network and read letters from independent thinkers such as Aden Sisters, Lawrence Roulston, and Ron Struthers on how you can protect yourself from the imminent dollar crisis.

John Lee, CFA

johnlee@maucapital.com

John Lee is a portfolio manager at Mau Capital Management. He is a CFA charter holder and has degrees in Economics and Engineering from Rice University. He previously studied under Mr. James Turk, a renowned authority on the gold market, and is specialized in investing in junior gold and resource companies. Mr. Lee's articles are frequently cited at major resource websites and a esteemed speaker at several major resource conferences.

John Lee Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.