U.S. Economy Endgame, Muddle Through or Debt Crisis?

Economics / US Economy May 08, 2011 - 02:14 AM GMTBy: John_Mauldin

This week I finish the two-part letter on the Endgame and give you my thoughts on the economy and how it all plays out over the next five years. This is the second part of a speech I gave last week at the Strategic Investment Conference in La Jolla. It is a rather bold forecast, and fraught with peril and likely errors, but that is my job here. Damn the torpedoes, etc. I must offer one large caveat! If the facts change so will my forecast, but this is the view into my very cloudy crystal ball as I see it today. As always, remember that those of us in the forecasting world are often wrong but seldom in doubt. Read accordingly.

This week I finish the two-part letter on the Endgame and give you my thoughts on the economy and how it all plays out over the next five years. This is the second part of a speech I gave last week at the Strategic Investment Conference in La Jolla. It is a rather bold forecast, and fraught with peril and likely errors, but that is my job here. Damn the torpedoes, etc. I must offer one large caveat! If the facts change so will my forecast, but this is the view into my very cloudy crystal ball as I see it today. As always, remember that those of us in the forecasting world are often wrong but seldom in doubt. Read accordingly.

But before we get there, two quick things. I want to really show my strong appreciation for the work done by my co-hosts, Altegris Investments, at the 8th annual Strategic Investment Conference. We had a packed house with almost 500 people come to see what I think was the best line-up at an investment conference this year. Each year we say there is no way to get any better, and each year we somehow manage to do so. And that is due in no small part to the considerable effort of the team at Altegris. I am proud to be associated with them. This year we did video many of the speakers and panels, and over time we will figure out how to make some of this available. I will keep you posted.

Enemy of Spain

Second, Endgame continues to do well, so thanks to those who have purchased it, and if you haven't already got your copy you should go to www.amazon.com and do so! And quick kudos to my co-author, Jonathan Tepper, brilliant young Rhodes scholar and head analyst at Variant Perception. Apparently, he's on a small but prestigious list of enemies of Spain, according to El Mundo, one of the biggest Spanish newspapers, for the sin of pointing out that Spain is in a crisis (we have a whole chapter on Spain on the book). Their article appeared in print in the weekly finance edition, but is not online. Other papers have been called by government officials and asked not to quote him. Oddly, the people who helped inflate the enormous construction bubble and the incompetent government officials who denied for years there were any problems are not enemies of Spain. Go figure. I guess if you have to be on an enemies list, you could do worse than Spain (where, oddly enough, Jonathan spent most of his childhood growing up in a drug-rehab facility). Congratulations, young man! (Oh, and a publisher in Korea picked up the Endgame Korean-language rights, so we will soon be in bookstores in Seoul.)

And now to the second part of the Endgame. And for those who want to review the first part, you can read it here.

The Endgame, Part 2

There is an argument that the US should pursue a strong growth and jobs policy as its #1 goal and that growth, along with spending cuts and/or tax increases (depending on your views), will bring us out of the current doldrums and help us solve the budget deficit. I set the table in both the book and last week's letter that the US is going to be growth challenged for years to come. Let me review a few items in brief and add a few more, then we will get to my predictions of what the next five years will look like. Don't jump ahead. Without understanding the elements that are lining up to retard growth, the forecast will not make much sense.

First, job #1 MUST be to reduce the deficit below the nominal growth rate of GDP. Period. The level of debt threatens to overwhelm everything else, and at some point can produce a crisis like those evolving in Europe and Japan. I have outlined the reasons for this in depth, so here I merely make the assertion.

As I explained at length, if you increase government spending it will increase GDP IN THE SHORT TERM. The economic literature suggests this effect lasts about 4-5 quarters. Further, tax cuts will produce a growth in GDP of roughly 1 to 3 times the total amount of the cut over the next few years (depending on whose research you read, but the consensus is clearly that tax cuts make a difference). It sadly follows that increasing taxes will have a negative effect of roughly the same amount.

Now, basic economic accounting shows that if you reduce government spending you are going to reduce GDP over the short term by a rough equivalent (GDP = Consumption (C) + Investments (I) + Government Spending (G) + (Net exports)).

Therefore, the first headwind to economic growth over the next five years is the reduction of the deficit. While there is a longer-term difference between tax cuts and tax increases, in the short term (4-5 quarters) there is a simple drag effect. And we are going to need to cut government spending by about 1.5% of GDP per year every year for five years (allowing for some growth) to get the deficit to a manageable level.

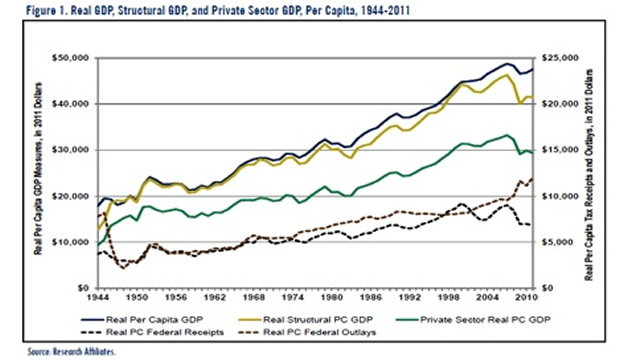

Below is a chart I used last week that is from my friend Rob Arnott at Research Affiliates (and to whose annual conference I am flying to as I write this letter), but it bears looking at again. The chart needs a little set-up. It shows the contribution of the private sector and the public sector to GDP. Remember, the C in the equation is private and business consumption. The G is government. And G makes up a rather large portion of overall GDP.

The top line (in dark blue) is real GDP per capita. The next line (yellow) shows what GDP would have been without borrowing. So a very real portion of GDP the last few years has come from government debt. Now, the green line below that is private sector GDP. This is sad, because it shows that the private sector, per capita, is roughly where it was in 1998. The growth of the "economy" has come from government spending. Private-sector spending is where it was almost 13 years ago, accompanied by no growth in median real income and no growth since 2000 in the actual number of jobs, even as population grew by 30 million.

As we bring government spending down, unless it is accompanied by private-sector growth, we will see overall real GDP shrink. That is just the how it works. Now, in the fullness of time (or a few years), the smaller government expenditures and deficit will mean more money for private-sector investment and productivity growth, but the process of simply getting the deficit under control is going to mean slower growth. Wrap your head around that. While Republicans (including me) want to control Congress and the presidency in 2012, the policy choices made in 2013 will not be met with a robust return to 4% growth and immediate jumps in employment levels. It is going to take a lot of education to convince voters that there is no magic in spending cuts (or even tax increases) and that we will need to stay the course, even while there is a general malaise in the economy. My advice to my fellow Republicans? Do not sell the concept that voting Republican will provide a quick fix. It will get you slaughtered in 2014. More on why below, in the conclusions.

Let's quickly list other headwinds.

• The next headwind we will face, in 2012, is a tax increase of about 2% for almost everyone, as we lose the reduction in Social Security taxes that was passed to 2011 as part of the Bush tax cut extension. This means less money in the pockets of everyone making below about $100,000, which is significant in terms of the drag on GDP.

• The stimulus package of 2009 is fading from view. There is little reason to think any of it will come back. Look at that graph again and see how much worse GDP would have been without it. But for all that, we are watching growth soften of late, with the economy now down to 1.8%. We didn't get the organic growth in the economy that the Keynesians promised. Where is that multiplier effect? It actually seemed to be a negative multiplier, which Austrian economics suggested it would be. Score one for von Mises and Hayek.

• QE2 is stopping in June. The hope at the Fed is that the economy can take over from there. But the last time QE was stopped, in 2010, the results were not impressive; and now we can look across the pond to England to see what is happening as they are about 6 months further along in their ending of QE. It is hard to get encouraged from the data, as it looks like growth in England has slowed. And the real effects of their new austerity pursuits have not really been felt. Can the Fed start up again? Or more apropos might be the question, "Will the Fed start another round of QE?" My answer is that, when they see the economy slip into recession, they will use the only real tool they have left, and that is to inject liquidity into the economy.

• A McKinsey study on the aftereffects of debt crises (in numerous countries) that require deleveraging in one form or another, is that for the first two years there is a significant slowing of GDP, and the slower growth does not dissipate for 4-6 years. We have not started deleveraging as a nation. The real work now looks like it will be done in 2013; and thus the real pain, the study suggests, is in our future.

• Unemployment is back at 9%, rising this morning another 0.2%. The real level is easily above 10% if you count people who were in the work force as recently as 2008. Five percent of the nation's workers are not paying income, Social Security or Medicare taxes. Many of them are on food stamps and unemployment, which are driving deficits at the federal and state levels higher. It is hard to imagine a robust economy that does not somehow figure out how to drive the unemployment level down, yet economic growth of 3% or more is required. We are simply not there.

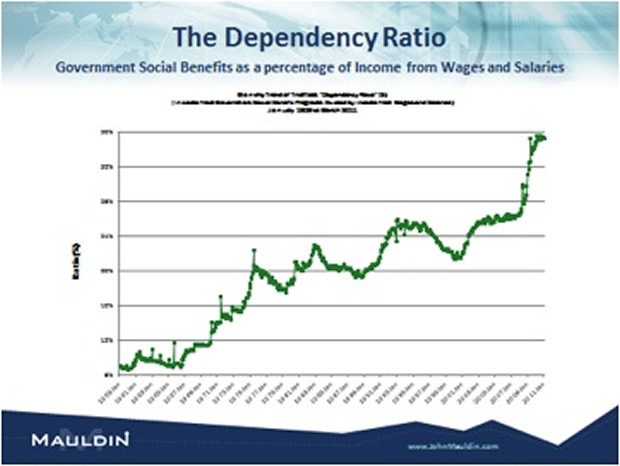

• I noted above that private-sector jobs have gone nowhere for 11 years. But transfer payments as a percentage of private-sector income and wages have risen inexorably for the past 50 years. Below is a chart from Madeline Schnapp, the chief economist of Trimtabs. Let me quote from the email she sent me along with the chart:

"Here is the graph which generated a HUGE amount of controversy when published awhile back. For lack of a better term, I called the ratio the "TrimTabs Dependency Ratio." What it is, using BEA data, is a ratio of 'BEA's government social benefits to persons' divided by 'BEA's wages and salaries.'

"While wages and salaries are about 50% of total personal income (other sources of personal income are benefits, interest, dividends, etc.), it is the largest bucket of income that produces revenue for the government via our tax structure. Therefore wages and salaries are currently the engine of support for the government's social programs.

"FYI, the BEA's definition of government 'Social Benefits to Persons' includes Social Security, Medicare, Medicaid (the biggies), unemployment insurance, supplemental nutrition (SNAP, formerly food stamps), veteran's benefits, etc.

"For the ratio to go back to something sustainable, e.g. 20%, either wages and salaries need to rise, benefits need to be trimmed, or taxes need to go up.

"Be careful not to confuse ratio with proportion. In this chart, I am comparing the size of one thing to the size of another (backpacker analogy); it is not a proportion, e.g. one thing as a part of another.

"Another useful analogy is:

"There is the engine (wages and salaries) pulling rail cars up a hill. In those cars are the Defense Department, the EPA, government social benefits to persons, etc. Since 1960, the size of the social benefits rail car has grown from 10% the size of the engine, to now 35%. The 'Little Engine that Could' is rapidly becoming the 'Little Engine that Couldn't.'"

• I showed two charts and research last week that clearly demonstrates that at some point the size of government becomes a drag on the economy. That may seem contradictory to my first point in this letter (reducing government spending will reduce GDP), but it is not. The first point was a short-term effect, and the size of government is a longer-term effect. We now have a government that is too large, and it acts as a headwind to growth.

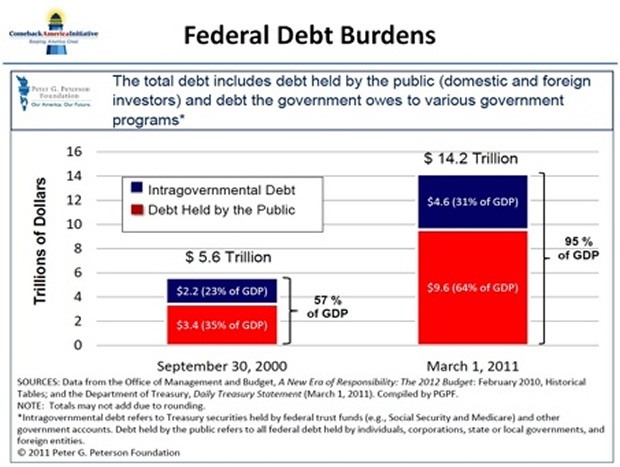

• The research of Rogoff and Reinhart clearly shows that, as the debt-to-GDP level of a country approaches 90%, there seems to be a slowing of potential GDP growth by about 1%. This is an observation of the data, not a theory. And this graph from David Walker suggests we are getting there. Notice it does not include state and local debt, which it should. We are very close to this level, if not there already.

Muddle Through, or Crisis?

Betting against the power of the free-market economy in the US is generally a bad idea. Yet when I suggested back in 2003 that we would see a slow-growth Muddle Through Economy for the remainder of the decade, it turns out I was right. We only grew at 1.9% last decade, which was the worst performance since the Depression. Ugh.

So where are we for the next five years?

I think we have two choices as a country. We can elect to deal with the deficit proactively, or wait until there is a crisis and react. And make no mistake, there is a an approaching Endgame, with regard to how much debt the market will let us have. We don't know that point now, but if it happens it will be quite a "surprise!"

What happens if we make the choice to get the deficit under control? What that really means is that we have to decide how much health care we want and how we want to pay for it. Let's forget for the moment how that happens. Let's just be optimistic and say we do make those decisions.

For me, that is the best-case scenario. But it means a slow-growth, Muddle Through Economy for quite some time, perhaps as long as 5-6 years, though getting better as time goes on. It also means it is highly likely we will have at least one recession during that period, as growth will be close to "stall speed" and any exogenous shock could tip us into recession. Recessions mean higher unemployment, lower tax revenues, and an even deeper hole that will require more fiscal discipline and work. It will make maintaining corporate earnings growth at today's expected levels more difficult, which puts a headwind to the US-based equity markets. Of course, a recession will mean (on average) a 40% retrenchment of US equities. It will also mean another deflation scare and a likely QE3. Bernanke can bring back and polish his "helicopter" speech, but this time he will be able to tell us what happened.

Then there is the crisis scenario. Let's assume we do not deal with the deficit in any meaningful way. Eventually the debt will rise to epic, Greek proportions. The bond vigilantes arise from the dead and start to push up interest rates. Interest as a percentage of government spending rises, crowding out other government expenses or increasing the debt still further.

Then we have a crisis. We are FORCED by the bond market to get the deficits under control, but now we are doing so in a crisis. Health care will have to be slashed by far more than it would in a more controlled scenario. Tax increases will be brutal. You think Social Security is untouchable? Not in this crisis world. Means testing and spending freezes will be the rule of the day. Military cuts will seem draconian. Our allies who depend on us for a defense shield will not be happy. Education? On the chopping block. The economy will not be Muddle Through, but Depression 2.0. Unemployment will go north of 15%.

What's my basis for this? History. This movie has played over and over again in various countries in modern history. While we may be the world's superpower, we are not immune from the laws of economic reality.

In such a scenario, I expect QE 3-4-5-6. Could the Fed literally monetize the debt and then "poof" it? When our backa are against the wall, don't assume that what has been seen as normal will be the reigning paradigm.

Let me jump out on a real limb. I was having dinner last Monday with Christian Menegatti, the #2 economist at friend Nouriel Roubini's economic analysis shop. We were comparing notes (imagine that), and he said their opinion is that the US has until 2015 before the bond market really calls the deficit hand. Knowing that Nouriel is seen as the ultimate bear, it makes me nervous to put out my own even more bearish analysis.

I think the crucial point will be reached in late 2013. If the bond market sees a serious move to control the deficit, I think they let us "skate." Then we Muddle Through. But if not, I think we begin to see some real push-back on rates then.

Why so early? Because bond investors are going to be watching the slow-motion train wreck that is happening in Europe and especially Japan. It is one thing for Greece to default (which they will in one form or another, with lots of rumors flying this morning), yet another for Japan to do so. Japan is big and makes a difference. Japan could start to go as early as the middle of 2013. As I have said, Japan is a bug in search of a windshield. Whenever this happens, 2013 or a year or so later, it is going to spook the bond market. The normal indulgence that a superpower and reserve-currency country would be accorded will become much more strained. It will seemingly happen overnight. Think Lehman Brothers on steroids.

I think the chances we will deal with this potential crisis are about 75%. Not doing so is such a horrific outcome that I think politicians will do the right thing. See, I am an optimist. (What was it Winston Churchill said? "You can always depend on the Americans to do the right thing, after they have exhausted all the other possibilities.")

And let me note that I have had some rather at-length, high-level (but very off-the-record) discussions with politicians on the right in recent weeks. More and more of them are really getting it. But as one said to me, "John, I can't run on that platform." And that is the reason that I give it a 25% chance that we'll wait until a crisis hits us. If the "good guys" (my view, not yours, gentle reader - I know many of you are of the more liberal persuasion) need a real push to act correctly, we are not in good shape.

I totally recognize it will not be easy to fix it. It will probably mean tax increases, which will not be good for the economy. And spending cuts that will be painful. I get all the consequences. I have written about them. But the goal is to get rid of the cancer of the deficit. It could truly destroy our economic body. Sometimes, if you have cancer, you take very ugly chemicals into your body, which have very serious side effects. The prospect does not make me happy at all, but we have made bad choices as a country for decades, and now we have to pay the price.

Just a few more thoughts. Republicans should demand a total restructuring of the tax code in return for any tax increase. I would opt for lower corporate rates to help make us competitive (say 10-15%) and include all foreign corporate income, and get rid of the mass of exemptions. Lower personal rates and a consumption tax would suit me just fine, as both an economist and a businessman; but I know that's not some people's cup of tea. Just saying. I like David's Walker's thoughts about $3 of spending cuts for every $1 of tax increases. And can we get rid of some of the "tax expenditures," like mortgage interest deductions? We all pay 4% in income tax so that a minority can have interest-rate deductions. (I have written about efforts we need to undertake that would more than offset any hit to real estate.) At least reduce it for mortgages over $1 million. If you can afford a mortgage that big, you don't need the deduction.

Every one of those tax expenditures is someone's else tax break that is vital to the future of the Republic, but if we got rid of all tax expenditures in one massive move (or over time) we could simplify the tax code and come within a few hundred billion of balancing the budget. Walker says the breaks total $1.2 billion. Basically, these are goodies that Congress hands out to get votes. Get rid of them all, I say. It will be politically difficult, but we need drastic action.

And I might suggest that Democrats should come to the table this year rather than waiting until 2013. If unemployment is north of 8% next election, as I think likely, you will lose more seats and (probably) the White House, given today's polls. Why not negotiate now when you have the Senate and can get what you can? Maybe "my guys" are being obstinate, but the sooner we do this the sooner we get through it.

And that is my point. We do get through it, either as adults or forced to do so by the bond market. One way or another, by the latter part of this decade, in the fullness of time, this too shall pass.

The eternal optimist in me wants to quickly point out that neither scenario is the end of the world. Yes, we may have to tighten our belts, some more than others, but life goes on. We all figure out our own paths. While investing has been more difficult the last five years, we are all still alive, celebrating birthdays and grandchildren. New businesses that will dramatically change our lives are being formed every day. There are lots of opportunities for business and investment, perhaps just not the traditional ones we are used to. Maybe gold goes to $5,000, but I hope it goes to $500. Either way I will still buy some physical gold every month as insurance, with the dream that I'll give it to my great-great grandchildren as a novelty from the days when we thought gold had value. But I will still buy, just in case. I simply don't completely or naively trust the &*%@^&'s who are running the place.

Seriously, I expect that, beginning later this decade we will see the secular bear crawl back into hibernation and a roaring secular bull market cycle come charging out. We will all get to once again be geniuses.

The book I am starting to write this month (finally!) will be called The Millennium Wave, in which we'll look at what our world may be in 2032. The journey there will be bumpy, but what a world it will be! So, over the next few months and quarters, we will keep our eye on the politicians and see what happens. I will be looking for good hedges and places to invest that don't depend on Washington DC or the other capitals of the world. And I will keep on writing to you, gentle reader, every week.

Last thought: I encourage you to get involved in the process in whatever way you deem correct. This is going to be the most important national conversation we have had in a long time, and you should be a part of it. Make your voice and vote count!

Philadelphia, Boston, Trequanda, Kiev, Geneva, and London

I am in Laguna Beach at the Montage this afternoon for Rob Arnott's annual client conference. He has an outstanding lineup of speakers: Lacy Hunt, Jim Bianco, Professors Burton Malkiel of Princeton and Nobel laureate Harry Markowitz, along with Rob and his associate Jason Hsu. They are known for the creation of Fundamental Indexes. This has become a (deservedly) amazing story of growth over the last few years. I remember writing about it and saying something like "This would be the fastest idea to grow to $100 billion in assets in history." They are over halfway there, taking assets from what the research and results say is the inferior performance of cap-weighted indexes.

I fly back on Sunday and am home for two whole weeks in my own bed, then I fly to Philadelphia for a conference with the Global Interdependence Center. To find out more you can go to http://www.interdependence.org/Event-05-24-11.php. Then it's to Boston for some business and a little relaxation, before flying on Sunday to Italy to stay for three weeks in a small village in Tuscany called Trequanda, where most of my kids will be for the first week or so, and then it will be a working vacation with Tiffani, while friends come to see us. Vacation for me is being in the same place for a few weeks. Then I'm off to Kiev for the weekend for a reunion of my classmates at Singularity University, then to Geneva for a few days and London for one day, where I will guest-host CNBC Squawk Box, which is always a few hours of fun. Then back home, and I'll get to be in Texas for most of the summer - at least that's how it looks now.

I feel somewhat awkward of late, going through airports and meetings wearing a large cast on my right foot, trying to keep it immobile to let the inflammation go down from doing too many lunges and straining the tendon. I can feel it helping, but it there is a long way to go.

This next week should be fun, as I will be taking a girls championship softball team to see the Texas Rangers. Most of them have never been to a professional game. Then good friend Cliff Draughn is in town, then (maybe) game six of the Mavericks-Lakers series, more family, and no alarm clocks. I need the rest. This last week, with cancelled flights and early mornings, has frankly been tiring. I really must get the schedule under better control.

Speaking of "brutal," it is time to hit the send button. Rob's conference starts with a soiree on the lawn and always features some mighty fine wine. I must go and indulge, while promising to get to bed early! Have a great week!

Your quite sure we get through all this analyst,

John F. Mauldin

johnmauldin@investorsinsight.com

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/learnmore

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2011 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.