REITS signaling a bottom in the US Housing / Real Estate Market

Housing-Market / UK Housing Feb 09, 2007 - 12:07 AM GMTBy: Clif_Droke

One of the inescapable conclusions one comes to after a long-term study of history is that current events and financial markets is very little happens without a pre-ordained reason. This statement is especially true when applied to the financial markets. With literally trillions of dollars in money and credit floating around the world, there is simply too much at stake to allow the natural forces of chance and coincidence to interfere with the plans and dealings of the world's financial controllers.

To Franklin Delano Roosevelt is commonly attributed the following statement: “In politics, if it happens, you can bet it was planned that way.” Viewed from this perspective, it becomes difficult to reconcile the financial panics, manias and crashes of the past with mere chance. Every major event in financial history can ultimately be tied to some plan (or reticular series of plans) of the “wheeler-dealers.” Another famous statesman once said that if you're looking for the reasons why anything happens in the realm of politics and economics look at the results and see who the winners were and then you'll have your answer.

So if we proceed under the assumption that nearly every major financial event has been pre-ordained and carefully thought in advance for the purpose of benefiting the elite few, it's only natural to ask, “What was the purpose of the real estate softness of 2005-2006?” The beginnings of the answer to this question can be found in a recent report on the U.S. real estate market.

Editor Robert Campbell in the January issue of his Campbell Real Estate Timing Letter (www.SanDiegoRealEstateReport.com) writes, “In the last two months, at least eight sub-prime mortgage lenders – lenders who make loans to ‘challenged' borrowers with credit problems and income issues – have shut their doors and/or gone bankrupt. Why? Because hundreds and hundreds of thousands of these sub-prime borrowers can't pay their mortgages, and they are inflicting severe losses on the lenders who made these types of loans.”

Could it be that one reason for the real estate slowdown was to push the smaller mortgage lenders out of business and foster consolidation among the survivors?

Another point worth mentioning is that whenever “thousands of sub-prime borrowers can't pay their mortgages” then it's time for the Federal Reserve to start priming the pump and upping the money supply…which is exactly what they've been doing since these statistics were first released. The mortgage market simply cannot be allowed to collapse at this point in time and it won't.

We keep hearing of excess inventory with “too many houses for sale and not enough buyers.” One analyst from a prominent brokerage firm remarked that this excess supply “may require a long time before it's absorbed.” Another analyst says it will probably take years to clear out the inventory of unsold houses on the market.

Others point to the rise in interest rates as being a factor that is expected to discourage buyers from coming forward. But in a healthy demand for housing, interest rates of no object unless they climb well into the double digits. Current interest rates are low by long-term standards and aren't even a factor worth considering in today's housing equation.

The real law of supply and demand in real estate says that the demand for real estate is latent and therefore theoretically insatiable. It further states that there can be no such thing as too much supply. Every house built will eventually be “absorbed” by a buyer and the current “oversupply” of houses in the U.S. could have even more units added to it and it still would find buyers eventually. The only thing to prevent the buyers from coming forward is a lack of availability of money and credit.

This leads to the fundamental principle governing the real estate market: demand is driven ultimately by money supply. When money supply and credit is loose and liquid, real estate and housing sales will be brisk. This isn't to say that bubbles can't exist and that prices don't sometimes exceed the boundaries of rationality. Indeed, sometimes housing prices and speculation exceeds the outer limits of what the market can bear and a reversal becomes inevitable. But this is not the same as a housing crash. Housing crashes can only be created by one thing: a severe diminution of liquidity. Only when bank credit and money supply dry up is there ever any real danger of real estate prices collapsing and remaining at depressed levels.

John Schoen, an economic commentator for MSNBC, wrote an article last Friday emphasizing the weaker-than-expected job growth in the U.S. despite the latest upbeat numbers in other areas of the economy. He noted that the latest figures show just 111,000 new jobs added for the month of January, which he and other economists interpret as a sign that the economy may be slowing. The renewed emphasis on lagging middle class incomes was one focus of the President's most recent speech.

The article also emphasized the housing market doldrums and Schoen quoted a report by outplacement firm Gray & Christmas, which stated: “…many experts feel that the housing market has not hit bottom, so manufacturers of home-building materials, and the real estate and construction sectors could see more job cutting this year.”

Schoen ended his article by quoting a statement by Richard Iley, a senior economist at BNP Paribas which, who said : “You take those two factors out, underlying the fundamentals, the economy is pretty poor,” he said. “The housing correction has a long way to run and there will be increasing spillovers.”

As you know, it's been my view repeated over and over to you since late last summer that the housing downturn would find bottom probably sometime in the first or second quarter of 2007 and I still hold to that view. The leading indicators, which almost no one looks at these days, are screaming “improvement is coming!” for the physical real estate sector, not only in the way the REITs are consistently making all-time highs but also in the steady improvement among the homebuilders.

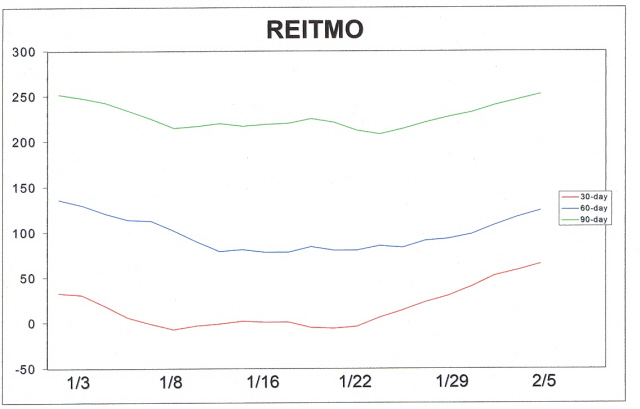

The REITs continue their bullish performance as we begin a new month with the Dow Jones REIT Index (DJR) closing on Feb. 7, at an all-time high. This has been expected as our REITMO series of internal indicators have been the most bullish of all our internal momentum indicators recently. Just take a look at the upward turn the 30-day, 60-day and 90-day internal momentum of the real estate equities have taken recently as shown in the chart below.

An even more important stock market sector for gauging the strength of the housing market, however, is the homebuilders. The Philly Housing Sector Index (HGX) has shown remarkable improvement since hitting bottom last summer. HGX topped out in August 2005 at about the 290 level and dove sharply to the 230 level by November of that year. After a brief recovery rally back up to 290 in January 2006 the HGX fell again even more sharply from April through July of last year and finally hit bottom at about 190. Since then the HGX has recovered steadily and has climbed all the way back up to a 6-month high of 255 last week. This represents a greater than 50% recovery from the housing sector bear market of 2005-2006.

|

$11 (29% discount) |

The message of the homebuilder stocks is that the physical housing sector will most likely continue to show improvement from last year's weakness as we've been preaching the past few months. That anticipated recovery has appeared already in the recent housing starts as well as in new home sales. Donald Rowe of the Wall Street Digest noted on Feb. 2, “Yesterday, pending home sales were up 4.9 percent, indicating that future existing home sales will be positive for all four regions of the country.”

Leading indicator stocks like Home Depot (HD), which is also a Dow 30 component, has also performed well and looks to have higher to go in its 6-month-old recovery. Also, the Dow Jones U.S. Building Materials and Fixtures Index is in a remarkable bull market since bottoming last July and has now completely retraced its bear market from last year, recently making a 52-week high. The turnaround in the Building Materials index has been among the most impressive turnarounds among industry groups in the past year.

So with the extraordinarily impressive charts in so many stock market groups related to real estate (residential as well as commercial) why are the experts still crying “bear!” on real estate? Why did Gray & Christmas predict more job cutting in firms related to construction? We know from history that big increases in job cutting and layoffs almost always occur as the bottom is being put in following a bear market. We also know from experience that the stock indices for major industry groups tend to give leading signals about 6-9 months for a bottom and turnaround in the physical sectors. Could the 6-month turnaround in the REITs, homebuilders and building materials groups be warning of an imminent bottom and eventual turnaround in the related physical real estate sectors? If history is any guide then the answer should be “yes.”

An even more immediate indication of the strength in the REITs and homebuilders is that the overall stock market is in an exceptionally bullish condition and should continue its strong performance in the weeks and months ahead. The REITs are leading indicators and strength in this sector nearly always precedes strength in the broad market. With the Fed pumping liquidity back into the system after the dry spell of 2004-2006, the stock market should continue to respond in positive fashion in 2007.

By Clif Droke

www.clifdroke.com

Clif Droke is editor of the 3-times weekly Momentum Strategies Report which covers U.S. equities and forecasts individual stocks, short- and intermediate-term, using unique proprietary analytical methods and securities lending analysis. He is also the author of numerous books, including most recently "Turnaround Trading & Investing." For more information visit www.clifdroke.com

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.