Stock and Commodity Market Forecasts 2008 - Enormous Investment Opportunities - Part I

Stock-Markets / Financial Markets Jan 18, 2008 - 10:13 AM GMTBy: Ty_Andros

2008 is going to be one for the record books. Like a roller coaster or thrill ride at an amusement park, the economic and financial ups and downs will thrill you and chill you! The opportunities in this year, and the next ten years, are ENORMOUS and as big as ever witnessed in history as the globe evolves and globalization unfolds. As a billion people in the G7 pay the price for their FAILURE to learn history's lessons, ask questions of their elected officials and demand accountability. Three billion people in the emerging world stand poised to ascend to thriving economies and new middle classes on the recipe of that little known economic school of thought called AUSTRIAN economics.

2008 is going to be one for the record books. Like a roller coaster or thrill ride at an amusement park, the economic and financial ups and downs will thrill you and chill you! The opportunities in this year, and the next ten years, are ENORMOUS and as big as ever witnessed in history as the globe evolves and globalization unfolds. As a billion people in the G7 pay the price for their FAILURE to learn history's lessons, ask questions of their elected officials and demand accountability. Three billion people in the emerging world stand poised to ascend to thriving economies and new middle classes on the recipe of that little known economic school of thought called AUSTRIAN economics.

The transfer of wealth to the emerging world is set to accelerate as the broad G7 character flaw known as the “something for nothing” personality drives more and more nails into the futures of its residents. IT IS IMPOSSIBLE to figure out what is going to unfold economically and financially without considering the politics and broad social trends afoot around the globe. These considerations are going to drive enormous investment trends for the next decade, and further, as globalization plays the role of Mother Nature, the evolution of the earth and Darwinian Theory in action. See what's unfolding, set your investment sails properly and get immensely wealthy; invest looking in the rearview mirror and be impoverished. In order to understand what we believe is about to transpire we need a little setting of the current economic table to understand the coming 2008 prognostications.

We will be covering all the major sectors such as stocks, interest rates, currencies and commodities, as well as the master thread that must be woven into the analysis - and that is FIAT CURRENCY and CREDIT CREATION. We will show real returns versus nominal ones. Due to “word count” constraints placed upon me by the websites which post my work, this 2008 outlook will be spread out over the next 3 to 4 weeks.

Now we come to the dominant pattern for 2008 courtesy of John Mauldin!

Everything will be a response to the unfolding collapse in income; the subsequent sequence of events will be like a game of dominoes as a consequence of this one REALITY spreading throughout the G7 economies!

Below, I have updated the chart from when it was originally published in March of 2007 and included my commentary at the time (in italics), as it is now CRUNCH TIME for this 50 year chart:

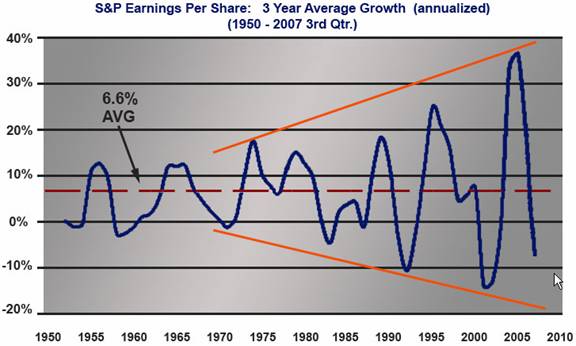

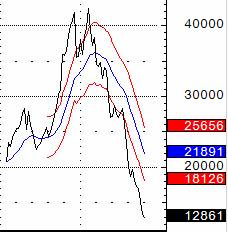

We are in a wolf wave, and the amplification of each wave up or down are expanding. A chart of a wolf wave looks like a mega phone, small on one end amplifying out. Wolves attack and eat things and it is no different with economies and asset markets, they are eaten when a wolf appears. A good example of a wolf wave is from John Maudlin latest letter and by extension Crestmont Research ( www.cresmontreasearch.com ), here he shows corporate profits since 1950; John can be reached at john@frontlinethoughts.com

(This chart has been updated to reflect through the 3rd quarter)

See the mega phone formation? It is called a wolf wave. We are at a fairly good level of profits now. But it projects a nuclear winter in corporate profits dead ahead (see chart below). From Record highs never seen in fifty years, to record lows also not seen in the same period, below the lows of 2001-2002. This chart is a testament to how fiat money and credit creation has made steady growth and economic stewardship become more and more unmanageable over a long period of time, it is clear that monetary policy is also following this wolf wave pattern, either too hot or too cold. Politicians (and their “something for nothing” constituents) in the western world see these enormous profits and are set to attack the creators and holders of this wealth, they want the money and will put in place new taxes and entitlement mandates to claw back this gusher of wealth, thereby accelerating the downside of this wave. We all want business cycles that cleanse past excesses but the up and downs are now out of control, there is no consistency. No orderly form to the business and economic cycles, everything now is either booming or busting.

Those words were prophetic in March when they were written in the first “Fingers of Instability” series as was that chart of corporate profits (see Tedbits Archives , this was one of the best of 2007. Read its words then look around you today). Now we are far below the ZERO line and falling fast, so, the gusher the public servants are telling the electorate (that they are going to CLAW back from those greedy corporations and small businessmen, i.e. your employers and neighbors) is now GONE. The lows are scheduled/projected to arrive at election time, making for good decision-making doesn't it?

The reflation that will be required will be ENORMOUS, and to think every politician in the G7 is angling to punish those EVIL corporations and small businessmen for raising their prices to compensate for the lower value and purchasing power of the G7 currencies in which they are priced. G7 corporate profits are only at NOMINAL new highs; in REAL terms they are “cratering”, just as you will see in an example of stocks and bonds later in this letter.

The loss of wealth and purchasing power of the currency held by the G7 middle class in the last two years is astonishing and now approaches 40% in REAL terms! Thank you “Pinocchio” George Bush, “Helicopter” Ben Bernanke, “Sold the Gold” Gordon Brown, “Mandated wage increase” Angela Merkel, “Let's divide corporate profits 1/3 to stockholders, 1/3 to labor and 1/3 to government” Nicholas Sarkozy, et al. No wonder the electorates are up in arms in the G7! Another round of crushing income reduction is set to materialize throughout the G7 on every level: individual, municipal, state and federal.

An unfolding “Crack up Boom” is in its infancy and must be considered as you deploy your investment dollars. “Fingers of Instability” allow you to find value as certain sectors implode after episodes of IRRATIONAL EXUBERANCE. Discipline will be everything for the next year and decade. (I urge new readers to review the Tedbits archives and learn more about “Crack up Booms”, “Fingers of Instability” and the “something for nothing” personality in the Tedbits archives at www.TraderView.com )

The world will continue to grow, and grow quite nicely, only its forms and residency will change. Wealth will increase enormously in some places and contract in others.

The developed G7 economies have CEASED growing in REAL terms and now only grow in nominal ones. Rather than create wealth on the factory floor, wealth is now manufactured with “PAPER” and asset backed economies. This is what is driving the demise of their financial systems and the constant erosion of their living standards. The policies of wealth creation are now a memory, as socialism, central control of economic policies and nationalization (through higher corporate taxes, employee mandates and smothering micromanagement via regulations of what few wealth creating activities that still exist within the G7) continue to grow.

They call them capitalist-free economies but it is actually central government socialism masquerading as such, socialism is a wolf with sheep's clothing. Spreading an ever shrinking economic pie further and further, socialism is the definition of “Misery spread widely”. Due to the misnaming of this socialism as capitalism, the constituents of the G7 have misdirected their anger at capitalism rather then their public servants who have destroyed the system which created the wealth they have enjoyed for generations.

The original G7 and its “something for nothing” constituencies are the mob at work robbing the hardiest among them (wealth creating entrepreneurs and business) and feeding them to the weakest (desperate middle classes who don't understand what is transpiring and the victims of their political classes who lack knowledge of history and the financial/banking industries). These people consume, and they eat whether they produce or not. Their moral fibers are of made of balsa wood and are the living definition of consuming more than they produce. The policies of insolvency on a society-wide scale, individual, municipal, state and federal, are a black hole of capital sucking the life out of their economies and futures and directing it into capital destructive policies and sectors. Government is increasing in these economies where it destroys the most: central government planning, taxes, the factory floor and in finance and banking. They rely on anyone but themselves and increasingly hold their governments UNaccountable.

The G7 is consuming more than they produce and exporting approximately 2 Trillion dollars of wealth on an annual basis. They are in the fall of their empires.

The emerging world is now where wealth is created, fresh from the memories of long socialist winters and command economies. Austrian economics and capitalism are in the springtime of their ascendance. A huge fight is unfolding as former “emerging world” servants of the G7 ascend to become future masters of the world economies and wealth. They are destined to do so as they are the only place creating wealth. There is a broad social trend at work in the emerging world and it is: “I will work 60 hours a week for a better life for myself and my family”. This is the absolute antithesis of the “something for nothing” personality. These people produce or they don't eat, so their moral fibers are of hardy timber and they illustrate the definition of producing more than they consume. These peoples' close knowledge of “government as savior” know that to be the fallacy it is. Government is receding in these economies where it counts the most: central government planning, taxes, the factory floor and in finance and banking. They rely on no one but themselves but increasingly hold their governments accountable . They are producing more than they consume and accumulating capital and savings at a 2 trillion dollar a year pace . (See the “wealth of the world is rotating” in the Tedbits archives at www.TraderView.com ).

In addition to this mound of savings and income, capital from around the world is pouring into the areas which are actually growing and fleeing the G7, creating huge pressure in currency exchange rates.

In the G7 economies and developed world things are a little dicey at the moment as their constituents are insecure and fearful of the unfolding globalization of the world. Their public servants did not anticipate the consequences of their previous socialist policies and now they are unprepared to compete on a global basis. G7 Politicians and their elite banking masters have pushed the envelope of their confiscation scheme known as FIAT money and credit creation TOO FAR in substitution for the policies of wealth creation which their “formally” rich societies were built upon. The deindustrialization of the developed world began in the mid 1960's and accelerated when deficit spending upset the basis of the Global Financial System created after WW II, known as the Bretton woods agreements. Bretton Woods II was convened in the early 1970's when their currency's final underpinnings of Gold and Silver reserves where severed, FOREVER. It's been downhill ever since!

The populism running thru the streets of the G7 is a consequence of “MONEY PRINTING” and an absence of the policies of wealth creation pure and simple. Money is no longer backed by anything but a public servant's promise to pay. Can you think of any other promise they deliver on? I can't, and the money people are paid with always “melts in their hands” as their governments and financial industries take it at night with their printing presses and credit creation. Take a look at this chart of Money and credit creation courtesy of www.financialsense.com :

Wow, using the rule of 72 we can see what's transpiring in the G7/20 and that the emerging world is forced into huge money supply growth to “sterilize” the massive influx of G7/20 money exports:

• Russia, 72 divided by 43.7 equals money supply doubling every 1.64 years

• India, 72 divided by 20.15 equals money supply doubling every 3.57 years

• China, 72 divided by 17.06 equals money supply doubling every 4.22 years

• Australia, 72 divided by 16.64 equals money supply doubling every 4.32 years

• United States, 72 divided by 15.8 equals money supply doubling every 4.55 years

• Denmark, 72 divided by 14.53 equals money supply doubling every 4.95 years

• UK, 72 divided by 13.06 equals money supply doubling every 5.51 years

• Mexico, 72 divided by 12.69 equals money supply doubling every 5.67 years

• Euro zone, 72 divided by 12 equals money supply doubling every 6 years

• Brazil, 72 divided by 12.37 equals money supply doubling every 5.82 years

• Korea, 72 divided by 9.97 equals money supply doubling every 7.22 years

• OECD, 72 divided by 8.22 equals money supply doubling every 8.75 years

• Canada, 72 divided by 8.15 equals money supply doubling every 8.83 years

• Germany, 72 divided by 6.16 equals money supply doubling every 11.68 years

I could continue but the point has been made. These are economies that CONTEND that inflation is contained and running below 4% in the developed world and less than 6% in the emerging world. “Inflation is a policy of Government” and constitutes a Crack up boom in its infancy . Those headline numbers are used to fool the least informed among them and they keep the man on the street as their fool and pawn.

A ten-year bond, certificate of deposit, or currency from these countries are certificates of confiscation. You are GARANTEED to lose half the purchasing power of your money or more.

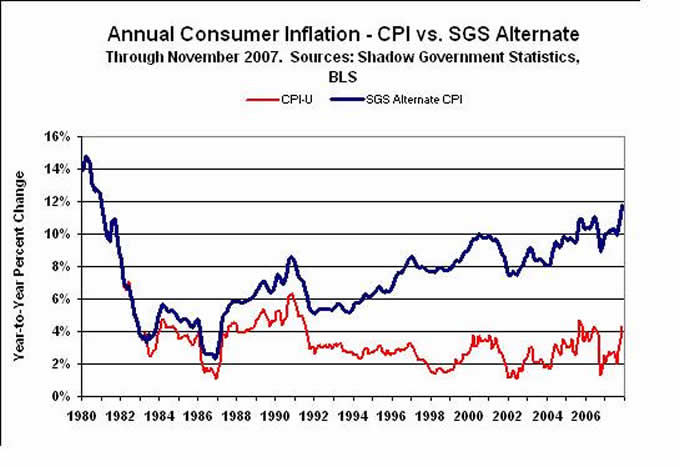

Investments which supposedly provide more yields still fail to retain the value of their initial deposit and fail to provide real returns. When long-term interest rates are 4-6 percent and money supply is growing at 13 percent, then the real yield on these INVESTMENTS is NEGATIVE! In the United States, a 10-year note yields approximate 4.00 %, and M3 is growing at approximately 15.8%, so you are getting a real return that is NEGATIVE, “compounded annually”. The last time it grew at this rate was the NIXON administration; do you remember the “cost controls” that he implemented? In the Euro zone and the UK, the numbers are equally UGLY! One needs look no further than the works of Milton Friedman to see the connection between money and credit creation and the ultimate inflationary consequences. Let's take a look at inflation (courtesy of John Williams and www.shadowstats.com , I urge you to subscribe to this site) as it was measured PRIOR to Clinton's presidency and all government numbers were POLITICIZED:

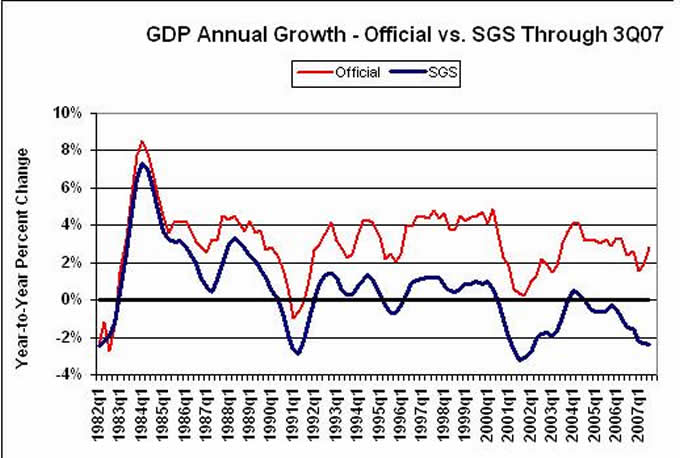

As you can see inflation is eating the middle class and G7 economies alive, economic growth and interest rates are massively negative if adjusted for this chart's message. Do you think this is limited to the US? The politicization of all economic data in the G7 has been expanding every year since 1990. Now lets take a look at another chart showing GDP (gross domestic product) of the US , adjusted for these realities(courtesy of John Williams at www.shadowstats.com ).

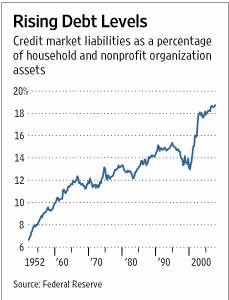

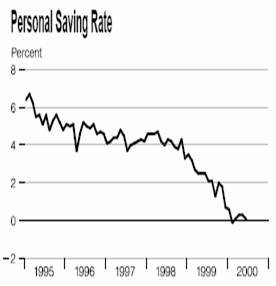

Now we can see that REAL growth has been almost nonexistent since 1990-1991. When you look at these two charts, you will see the middle classes' standard of living stagnant and drifting lower over a 17-year period. Shades of Japan . No wonder the national mood in the US and Europe is rotten, despondent and fearful. What Americans and Europeans realize and tell pollsters is that the government is on the wrong track. They are correct and when they vote for “change” (they want a return to wealth generation, a la Reagan) they are unwittingly voting for “more of the SAME”. They haven't progressed in their lives and incomes for over a decade and a half. No wonder they are frightened of immigrants to their countries and international trade. But these realities are a result of the Public servant's policies of de-industrialization, deficit spending, money printing, creeping socialism and runaway government expansion. Robbing the residents of the G7 of the ability to create and accumulate new wealth in their lives. As this has taken place, the public has gone into debt and reduced saving for over three decades:

The chart on the saving rates in the United States is a little dated - we are now approximately NEGATIVE 2% as of the 4 th quarter 2007. As their incomes have stagnated or declined, G7 residents have substituted debt and quit saving to maintain their lifestyles absent REAL income growth. Lowering interest rates is insanity, these people need rising incomes and policies that CREATE and REWARD wealth generation and hard work, not policies that encourage borrowing more and saving less . By not doing so and substituting money printing and inflation, public servants drive the middle class more and more into populous politician's hands in desperation. Hoping to regain the ability to save and increase wealth for retirement and their children, this is what the people mean when they say they want change. Commentators speak of a recession coming in 2008 that will last 1 or 2 quarters, how about the G7 in recession since 2004?

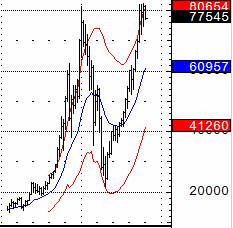

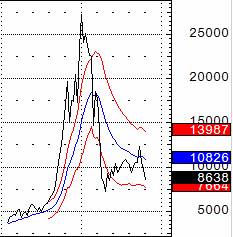

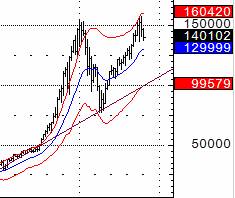

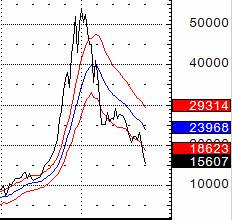

As a result of these government policies of deficit spending and fiat monetary and credit growth far in excess of prudent policies, investment returns are an illusion. Here are four charts to illustrate the illusion of growth: the German Dax stock index, the S&P 500, US ten year notes and German ten year bonds. Side by side as measured in dollars (fake money) and gold (real money):

1990 2000 I 1990 2000

DAX 30 in Euros I DAX 30 in GOLD

As you can see the rally in the DAX 30 DISSAPEARS when measured in real purchasing power of the paper currency (FIAT IOU's) versus gold (real currency which holds its value). Now the S&P 500:

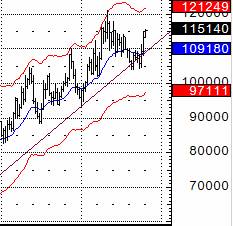

1990 2000 | 1990 2000

S&P 500 in dollars | S&P 500 in GOLD

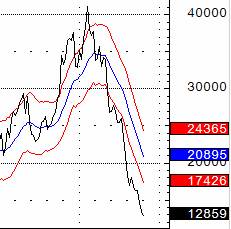

Where are the 80% gains CNBC has been crowing about since the 2002-2003 lows? In nominal terms stocks are rising, but in real terms they are falling in a blistering bear market. Notice the recent resumption of the bear market as gold moved up approximately 30% in 2007 . The things you invest and store your wealth in are VAPORIZING in value and purchasing power. That is your wealth being eaten and confiscated by the G7 governments/central banks, and the FINANCIAL and BANKING industry!!! Now let's look at the “RISK-FREE” rate of return on US and German Government 10 year bonds:

1990 2000 | 1990 2000

10-year bonds in dollars | US 10-year bonds in Gold

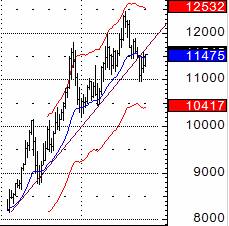

Doesn't seem so safe and “RISK FREE” anymore does it? US 10-year notes have lost half their value in purchasing power since mid 2000. That is also the measurement of loss in purchasing power for US DOLLARS. For all you savers out there, this is exactly where the government and G7 banking systems wish you to be and it does not matter whether you are talking the political LEFT OR RIGHT. Last but not least, let's look at German 10-year Bunds:

1990 2000 | 1990 2000

10 year Bunds in Euros I 10 year Bunds in Gold

WOW, over 50% loss in purchasing power in Euros as well - i n just 6 years . Would you call this RISK FREE? I speak with people all the time whose wives insist they keep their money safe in the bank. They know not of what they speak, they are destroying themselves and doing exactly the opposite of their intentions of being safe. Sitting ducks for the central banks and financial systems in which they reside. What a laugh, or should I say CRY!

The mass illusions of growth foisted on the public through misstatement of economic statistics are unbelievable. This period will be written about and studied for generations. When we go through the 2008 outlook you must keep this in mind. What we see here is only the warm up for what's about to transpire in 2008. Money and credit supply growth are about to accelerate from these levels in the ongoing reflation of the G7 Economies, financial and banking systems! PUBLIC SERVANTS, CENTRAL BANKERS and the G7 financial systems are perpetrating a fraud upon their constituents. Many commentators say fiat currencies are nothing to concern yourself with. I BEG TO DIFFER!!! GOT GOLD?

In conclusion, short circuiting the printing and credit creation machines is your first priority in 2008. You can't make money till you stop losing it. Many are saying this is the year of the collapse of the banking system in the G7! NO WAY! There is TOO much REAL wealth generation occurring in the emerging world for a collapse to occur at this time. There are trillions and trillions of Dollars, Pounds, Euros, Yen, etc. awash in the world and they are looking for a home while the Securitization Business and over-the-counter Derivative Market are “closed for renovation.”

In the developed world, the public servants and their constituents are voting for more money printing, socialism and government intervention (which is what has caused the mess they are in today), while in the emerging world and the BRIC's(Brazil, Russia, India and China) they are demanding more wealth creation and capitalism. Which policies do you think will PRODUCE more wealth for their respective areas?

The G7 bank's reserves and balance sheets are gone but there is plenty of paper to fill them at the right price and we will discover what that price is over the next year. Look no further than the takeover of Countrywide Mortgage. Many people thought Bank of America should have taken them out of Bankruptcy, NO WAY. The financial authorities didn't want to see the ghosts of Northern Rock's “run on the bank” on the cover of every newspaper in the United States: Countrywide Owns Thrifts. The financial authorities avoided the panic and quietly wrapped the maneuver in a private “Bernanke” put. Up next? Washington Mutual!

“Volatility is opportunity” and it is about to SOAR! (As you will see in the next installment of the 2008 Outlook) They will “Print the money” as the unfolding “Crack up Boom” powers generational moves in grains, commodities, currencies, and stocks are on the table . Nothing can go down NOMINALLY for long, in the face of the money creation that is about to unfold, on top of that which is already taking place! Bernanke promised this money creation in his speech just last week! His words could not have been clearer!

Do not be frightened, these are enormous opportunities. Recognize them and prosper. There is nothing you can do but understand them, figure out the methodologies to capture the opportunities within them and ride them for all they are worth. If you are not making money and a good deal of progress in your investments in the last 6 weeks and 6 months you know what to do. MORE HOMEWORK! Figure out why and make the adjustments. If your financial and investment advisor offers you no solutions except those that have failed you since the 2002 lows, then find one that will!!! If you enjoyed Tedbits send it to a friend, subscribe its free at www.TraderView.com P.S don't miss the next installment of the 2008 Outlook, it will be released Monday morning and will reveal a coming explosion!

Ty Andros & Tedbits LIVE on web TV. Don't miss Ty interviewed live by Michael Yorba from Commodity Classics every week discussing this week's commentary and unfolding news. Catch the show every Wednesday at www.MN1.com or www.CommodityClassics.com at 4:15pm Central Standard Time . Archived video casts are available there as well.

If you enjoyed this edition of Tedbits then subscribe – it's free , and we ask you to send it to a friend and visit our archives for additional insights from previous editions, lively thoughts, and our guest commentaries. Tedbits is a weekly publication.

By Ty Andros

TraderView

Copyright © 2008 Ty Andros

Hi, my name is Ty Andros and I would like the chance to show you how to capture the opportunities discussed in this commentary. Click here and I will prepare a complimentary, no-obligation, custom-tailored set of portfolio recommendations designed to specifically meet your investment needs . Thank you. Ty can be reached at: tyandros@TraderView.com or at +1.312.338.7800

Tedbits is authored by Theodore "Ty" Andros , and is registered with TraderView, a registered CTA (Commodity Trading Advisor) and Global Asset Advisors (Introducing Broker). TraderView is a managed futures and alternative investment boutique. Mr. Andros began his commodity career in the early 1980's and became a managed futures specialist beginning in 1985. Mr. Andros duties include marketing, sales, and portfolio selection and monitoring, customer relations and all aspects required in building a successful managed futures and alternative investment brokerage service. Mr. Andros attended the University of San Di ego , and the University of Miami , majoring in Marketing, Economics and Business Administration. He began his career as a broker in 1983, and has worked his way to the creation of TraderView. Mr. Andros is active in Economic analysis and brings this information and analysis to his clients on a regular basis, creating investment portfolios designed to capture these unfolding opportunities as the emerge. Ty prides himself on his personal preparation for the markets as they unfold and his ability to take this information and build professionally managed portfolios. Developing a loyal clientele.

Disclaimer - This report may include information obtained from sources believed to be reliable and accurate as of the date of this publication, but no independent verification has been made to ensure its accuracy or completeness. Opinions expressed are subject to change without notice. This report is not a request to engage in any transaction involving the purchase or sale of futures contracts or options on futures. There is a substantial risk of loss associated with trading futures, foreign exchange, and options on futures. This letter is not intended as investment advice, and its use in any respect is entirely the responsibility of the user. Past performance is never a guarantee of future results.

Ty Andros Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.