Turkish Economy, Is Turkey Golden?

Economics / Emerging Markets Nov 30, 2012 - 07:38 AM GMTBy: Steve_H_Hanke

Recently, Moody’s Investors Service took some wind from Turkey’s sails, when it declined to upgrade Turkey’s credit rating to investment grade. Moody’s cited external imbalances, along with slowing domestic growth, as factors in its decision. This move is in sharp contrast to the one Fitch made earlier this month, when it upgraded Turkey to investment grade. Moody’s decision not to upgrade Turkey, and its justification, left me somewhat underwhelmed – given how well the Turkish economy has done in recent years.

Recently, Moody’s Investors Service took some wind from Turkey’s sails, when it declined to upgrade Turkey’s credit rating to investment grade. Moody’s cited external imbalances, along with slowing domestic growth, as factors in its decision. This move is in sharp contrast to the one Fitch made earlier this month, when it upgraded Turkey to investment grade. Moody’s decision not to upgrade Turkey, and its justification, left me somewhat underwhelmed – given how well the Turkish economy has done in recent years.

Since the fall of Lehman Brothers, Turkey’s central bank has employed a so-called unorthodox monetary policy mix. For example, a little over a year ago, it began to allow commercial banks to purchase gold from Turkish citizens and allowed banks to count gold to fulfill their reserve requirements. Incidentally, this was a remarkable success – from 2010-2012, the Turkish banking sector’s precious metal account increased by over 7 billion USD.

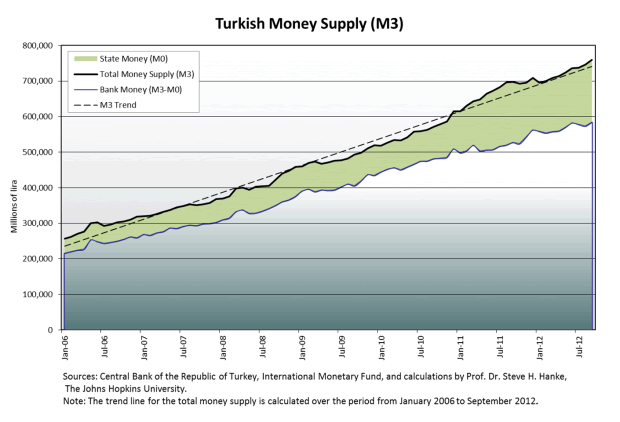

For all the criticism its unconventional monetary policies have garnered, the Central Bank of the Republic of Turkey has, in fact, produced orthodox, golden results. Indeed, as the accompanying chart shows, the central bank has delivered on the only thing that really matters – money.

Turkey’s economic performance has been quite strong (despite some concerns about inflation and its current account deficit) . Turkey’s money supply has been close to the trend level for some time, and it currently stands 2.41% above trend. This positive pattern is similar to that of many Asian countries, who continue to weather the current economic storm better than the West. And, it stands in sharp contrast to the unhealthy economic picture in the United States and Europe – both of which register significant money supply deficiencies.

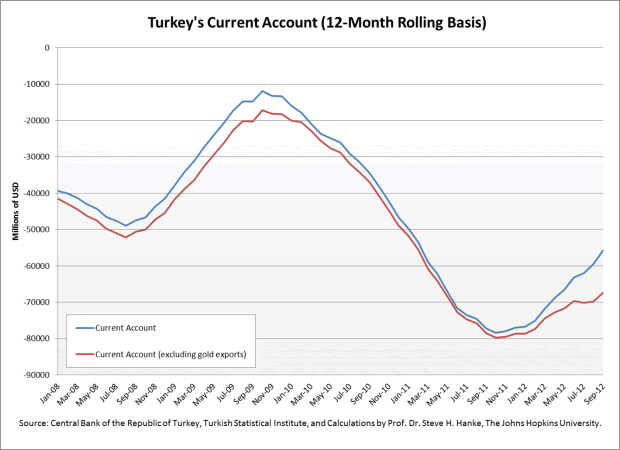

So, why would Moody’s not follow Fitch’s lead and upgrade Turkey to investment grade? To understand this divergence, one should examine Turkey’s recent current account activity. Since late 2011, Turkey’s current account has rebounded somewhat (see the accompanying chart).

But, if gold exports are excluded from the current account (on a 12-month rolling basis), a rather significant 47% of this improvement, from the end of 2011 to September 2012, magically disappears.

Where is this gold going? Well, a quick look at the accompanying chart shows just how drastically exports to Iran and the UAE have surged this year.

Taken together, the charts indicate that Turkey is exporting gold to Iran, both directly and via the UAE , propping up their current account in the process. This has put Turkey and the UAE in the crosshairs of proponents of anti-Iranian sanctions. Those who beat the sanctions drum are now seeking to impose another round of sanctions, aimed at disrupting programs such as Turkey’s gold-for-natural-gas exchange. This proposal clearly highlights some of the problems associated with sanctions, specifically the unintended costs imposed on the friends of the U.S. and EU in the region. Indeed, Dubai has already taken a hit, with its re-exports falling dramatically as a result of the sanctions.

What is the U.S. to do – go against Turkey, its NATO ally? Believe it or not, some in the Senate are allegedly considering such a wrong-headed move.

If these proposed sanctions are implemented, then Moody’s pessimistic outlook on Turkey may turn out to be not so far from the mark, after all – and Turkey will have no one but its “allies” to blame.

By Steve H. Hanke

www.cato.org/people/hanke.html

Steve H. Hanke is a Professor of Applied Economics and Co-Director of the Institute for Applied Economics, Global Health, and the Study of Business Enterprise at The Johns Hopkins University in Baltimore. Prof. Hanke is also a Senior Fellow at the Cato Institute in Washington, D.C.; a Distinguished Professor at the Universitas Pelita Harapan in Jakarta, Indonesia; a Senior Advisor at the Renmin University of China’s International Monetary Research Institute in Beijing; a Special Counselor to the Center for Financial Stability in New York; a member of the National Bank of Kuwait’s International Advisory Board (chaired by Sir John Major); a member of the Financial Advisory Council of the United Arab Emirates; and a contributing editor at Globe Asia Magazine.

Copyright © 2012 Steve H. Hanke - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Steve H. Hanke Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.