The Swiss Referendum On Gold: What’s Missing From The Debate

Commodities / Gold and Silver 2014 Nov 25, 2014 - 10:27 AM GMTBy: GoldSilverWorlds

This article is written by Eric Schreiber, independent asset manager, former head of commodities UBP, former head of precious metals Credit Suisse Zurich. All views expressed are his and may not reflect those of his former employers.

This article is written by Eric Schreiber, independent asset manager, former head of commodities UBP, former head of precious metals Credit Suisse Zurich. All views expressed are his and may not reflect those of his former employers.

The Swiss will vote on a referendum on November 30th that would ban the Swiss National Bank (SNB) from selling current and future gold reserves, repatriate foreign stored gold holdings to Switzerland, and mandate that gold must comprise a minimum of 20% of central bank assets. The SNB does not usually comment on political referendums. However, in this case it has done so quite vocally.

Why has the central bank decided to step into the political fray and oppose this initiative? What are its concerns? Are they valid or motivated by other factors?

The SNB’s primary objections to the gold initiative are three fold. 1) It claims that gold is “one of the most volatile and riskiest investments”, 2) that a 20% gold requirement will lower the “distributions to the confederation and the cantons” since gold does not pay interest like bonds and dividend paying stocks, and 3) that the 20% gold holding requirement will interfere with its ability to conduct monetary policy and complicate efforts to maintain “the minimum exchange rate”, the “temporary” policy of pegging the Swiss franc (CHF) to the Euro (EUR) it initiated in 2011 and continues to enforce to this day.

The first two concerns can quickly be addressed and discounted. Gold is indeed a volatile asset at times but so are bonds and equities. In recent years Greek, Spanish, Italian, Irish and other European bonds have been far more volatile than gold. The SMI, the Swiss stock index, lost over 50% of its value on two separate occasions between 2000 and 2009 while gold steadily rose at an annual rate of 8.50% over the same period.

Regarding the second concern, the distribution of proceeds derived from financial speculation and paid to the confederation and cantons, one has to question whether or not it is really appropriate for the SNB to re-brand itself as a hedge fund instead of remaining focused on its core responsibilities as a central bank.

To properly address the third SNB concern requires a historical context and a more detailed analysis. Prior to the change in the Swiss constitution, the CHF was backed by a minimum amount of 40% gold. Despite this constraint, Swiss monetary policy at the SNB was unhindered and functioned properly during the post World War II period. The SNB is correct in implying that today a partial gold backing, as required by the referendum, would make its policy of weakening the CHF against the EUR more difficult. Although the SNB has raised the currency peg as a reason for voting against the referendum the issue has not been directly addressed by the “YES” camp. Is the peg necessary? Does the population in Switzerland benefit as a whole from a weak EURCHF exchange rate? Why does the SNB feel compelled to continue a policy that it characterized over 3 years ago as “temporary”? How did “the minimum exchange rate” policy come to be? Why hasn’t there been a public debate about it?

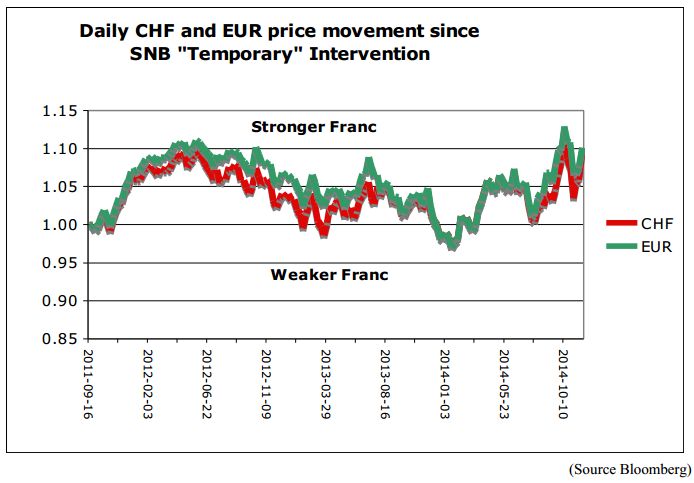

The answer to these questions begins with a look back into regional history a little over two decades ago. The Swiss population voted down two separate initiatives, one in 1992 and the other in 2001, to join the European Union (EU). Despite the popular votes, Switzerland was integrated into the EU for all practical purposes although officially it still remains outside the group of member nations. Entry into the EU was initially achieved by political means through a series of bilateral treaties, 10 in total, and then later in 2005 by popular vote in favor of the Schengen agreement. Laws between the EU and Switzerland were harmonized and Swiss border controls with EU member countries were abolished to permit the free flow of people, goods, and services. Unfortunately, Switzerland’s stealth ascension to the EU made a public vote on whether or not to replace the nation’s sovereign currency the CHF with the EUR politically impossible. To circumvent the issue, the SNB decreed on September 6th 2011 that it would enforce a “temporary” peg of 1.20 CHF to the EUR, a policy it refers to as “the minimum exchange rate”, to fend off EUR flows entering the country due to the financial crisis that was engulfing Spain and Greece at the time. The CHF would henceforth be permitted to loose value against the EUR but never to strengthen beyond 1.20. In this manner, monetary policy for Swiss affairs was quietly handed over to the European Central Bank (ECB) while maintaining the mirage of a Swiss sovereign currency before the public. The CHF was transformed overnight into a derivative instrument of the EUR without the ratification or knowledge of the population. The chart below shows the link between the EUR and the CHF derivative instrument since the “temporary” “minimum exchange rate” measure was put in place over 3 years ago. Note how the red line, the CHF, closely tracks the green line the EUR, but always remains a little bit below it (weaker) but never above it (stronger). Why is this policy still in place given the fact that the crisis in Spain and Greece has ended according to the EU?

The conversion of the sovereign Swiss currency into a EUR derivative tracking unit was achieved by the SNB in a four step process:

- the SNB publicly announced in 2011 that it stood ready to print “unlimited quantities of CHF “ and proceeded to print CHF out of thin air

- the SNB sold the newly minted CHF to buy EUR when the EURCHF exchange rate traded below 1.20

- the SNB used the EUR it acquired in step 2 to buy EUR denominated bonds

- the SNB promised Federal and Cantonal politicians the future interest “revenue” from the vast bond stockpile.

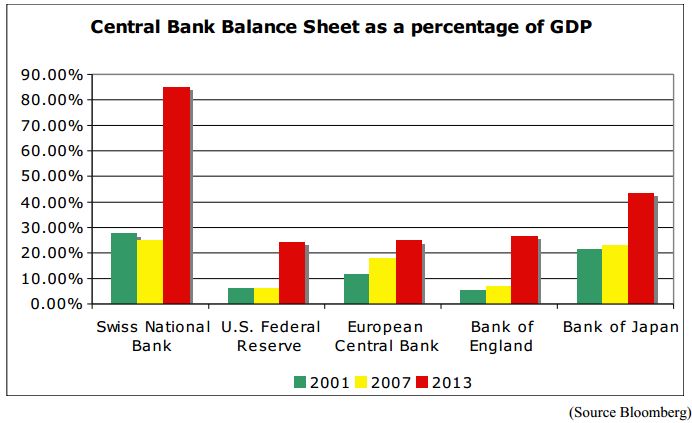

Evidence of this process can be seen in the figure below demonstating the dramatic expansion of the SNB balance sheet since the “minimum exchange rate policy” was put into effect. At over 83% of GDP, the Swiss National Bank’s EUR bond purchasing program is in a league of its own when compared to other activist central banks around the world. SNB “assets” have

surpassed 520B CHF and keep growing.

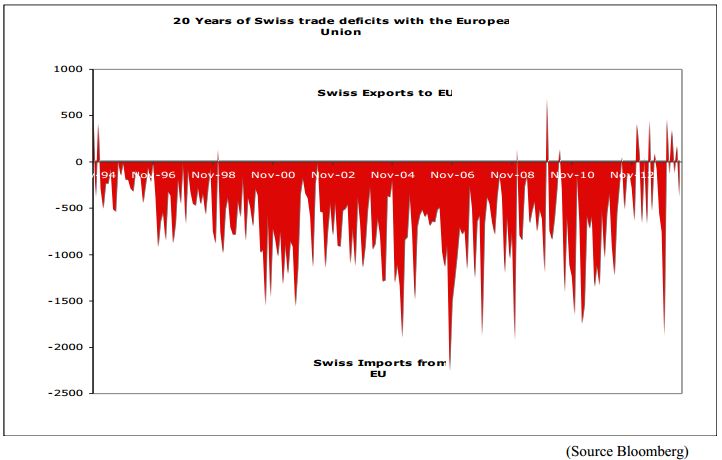

By gorging itself on EUR denominated bonds and bloating its balance sheet the SNB has created a significant foreign exchange risk exposure for itself. The SNB cannot meaningfully reduce its holdings and extricate itself from the currency risk it has created without incurring significant losses selling its inventory of EUR bonds at a rate below the 1.20 level. China, a country that has pegged its currency to the USD for decades, finds itself in a similar predicament. It is unable to sell its massive inventory of USD holdings without putting pressure on its own peg as well. However the Chinese and the Swiss situation differs in one very important manner. China is a net exporter of goods and services to the US. Chinese losses on the import side of the trade balance are more than offset by gains on the export side of the trade balance. This has been one of the key elements of China’s growth strategy since the 1990s. Chinese policy makers systematically undervalue their currency to provide an artificial boost for their exports. Switzerland on the other hand is a chronic net importer of goods and services from the EU and thus does not have the offsetting EU exports in sufficient quantity to compensate for the damage the peg inflicts on its domestic purchasing power.

Thus, the SNB “minimum exchange rate” policy impoverishes the domestic Swiss population by increasing the price of all EU imports purchased in Switzerland. This is perhaps the most egregious and certainly least publicized effect of the SNB action. Each time a Swiss resident purchases a good or service in Switzerland made in the EU, he or she is rendered poorer by the actions of his or her own national bank.

The problem of central bank overreach is certainly not isolated to Switzerland. Since the financial crisis 6 years ago, central banks around the world have interfered in and manipulated bond, foreign exchange, and equity markets on an unprecedented scale. These unelected institutions have actively redistributed wealth from one group to another and compete against one another to adjust the purchasing power of their national currency downwards relative to other nations without the knowledge of their populations. For over 3 years the SNB has been operating opaquely behind the scenes substituting another currency for its own, converted its citizen’s savings into EUR, and imposing a stealth tax on European imports without public consent.

A “YES” vote for the gold referendum is a first step towards redressing the imbalance that exists between the SNB and the people of Switzerland. A “YES” vote will begin a process to restore restraint, accountability, and transparency on an institution that took advantage of the removal of its previous gold holding constraint already once before to explode its balance sheet, reinvent itself as a hedge fund, and significantly expand into areas of policy far beyond its original remit. Central banks should be lenders of last resort and systemic regulators. In a direct democracy, decisions regarding taxation, membership in trade / political unions, and the autonomy of the national currency should be determined by popular vote not decreed or circumvented by central bank edict.

© 2014 Copyright goldsilverworlds - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.