Bond Yields vs Stocks and The Fed

Stock-Markets / Financial Markets 2015 Sep 07, 2015 - 12:54 PM GMTBy: Ashraf_Laidi

The widely anticipated US August jobs report headlined with a disappointing 173k increase in nonfarm payrolls (lowest since March). The silver lining was in the 44k upward revision of the previous two months and the decline in the unemployment rate to fresh seven-year lows of 5.1% from 5.3%. The decline 41K decrease in the labour force was too small to reduce the participation rate, which remained unchanged at 62.6%.

The widely anticipated US August jobs report headlined with a disappointing 173k increase in nonfarm payrolls (lowest since March). The silver lining was in the 44k upward revision of the previous two months and the decline in the unemployment rate to fresh seven-year lows of 5.1% from 5.3%. The decline 41K decrease in the labour force was too small to reduce the participation rate, which remained unchanged at 62.6%.

Average hourly earnings rose by a 5-month high of 0.3% m/m and 2.2% y/y in August. Both series are above their 3-month average, but they remain far below their 2007 highs of 0.6% m/m and 4.0% y/y. Some economists deem the rates as disappointing given the notable increases in minimum wages.

Are both the establishment and household surveys strong enough? Fed hawks require continued evidence of tightening labour markets at a time when the inflation mandate remains undershot. The evidence was obtained in the unemployment rate but not in non-farm payrolls. Renewed decline in energy prices will further drive inflation below the Fed's goal while jobs continue to offer low-paying employment.

Don't forget the Fed's other goal

Aside from the Fed's goal price stability and maximum employment, its3rd goal is to preserve financial system stability. A 10% decline in most US indices off their highs is no tragedy, neither is a 16% decline in Germany's Dax-30 or a 26% plunge in the Hang Seng Index. But tightening of financial market conditions becomes an issue when the borrowing environment becomes treacherous. We're not only talking about energy debtors, but all-sector high yield debt, which is at its worst measure since 2011 when using 10-year junk spread.

Asian corporate spread is also on the rise. After reaching 8-month highs back in January, Asian spreads are back up near 7-month highs. USD-based debt gone turned highly expensive is part of the problem. Relying on demand from a slowing China is another.

Fed's 1998 Backtrack

For those who claim the Fed is and should be focused on domestic issues and ignore China, think again. In spring 1998, the Fed was mulling a rate hike as US GDP growth was at 14-year high s and CPI was stabilizing. But as the 1997 emerging market route spiralled into a crisis from Brazil to Russia and Hong Kong in 1998, the Fed was forced to cut rates in Sep, Oct and Nov of that year. The collapse of LTCM also helped. Today, US growth remains subpar and the exogenous risks are considerable.

Back in the US, financial market stability is not exactly an ocean of calmness. But the rise in high-yield spreads and escalation in the VIX will grow more notable.

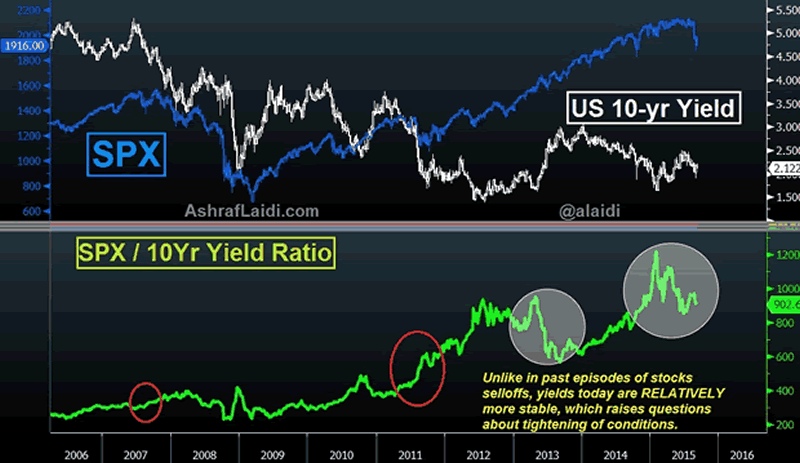

Finally, the uncharacteristically high level of US 10-year yields relative to the recent declines in US equity indices raises the following question: "If China were not selling treasuries to prevent CNY declines, then how low could yields be?" And if stocks continue to plummet (expect another 7% from today's close in US indices), then the relative relationship between indices and yields should reveal less tightening.

The above chart highlights the declining SPX/Yields ratio, suggesting that it's a matter of time before yields catch-down with stocks, regardless of whether the Fed raises rates or not. Earlier in the year, stocks were seen as too high relative to yields. Things have changed, but this too, will be temporary.

For more frequent FX & Commodity calls & analysis, follow me on Twitter Twitter.com/alaidi

By Ashraf Laidi

AshrafLaidi.com

Ashraf Laidi CEO of Intermarket Strategy and is the author of "Currency Trading and Intermarket Analysis: How to Profit from the Shifting Currents in Global Markets" Wiley Trading.

This publication is intended to be used for information purposes only and does not constitute investment advice.

Copyright © 2015 Ashraf Laidi

Ashraf Laidi Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.