Can the Fed Really Print Money? What Would Negative Interest Rates Do?

Interest-Rates / US Interest Rates Oct 16, 2015 - 03:58 PM GMTBy: Mike_Shedlock

Most people believe the Fed can print money. Caught on tape, former Fed chair Ben Bernanke once admitted the Fed prints money.

Most people believe the Fed can print money. Caught on tape, former Fed chair Ben Bernanke once admitted the Fed prints money.

However, in Hoisington's Third Quarter 2015 Review, economist Lacy Hunt makes the claim the Fed cannot print money. Let's take a look, emphasis mine.

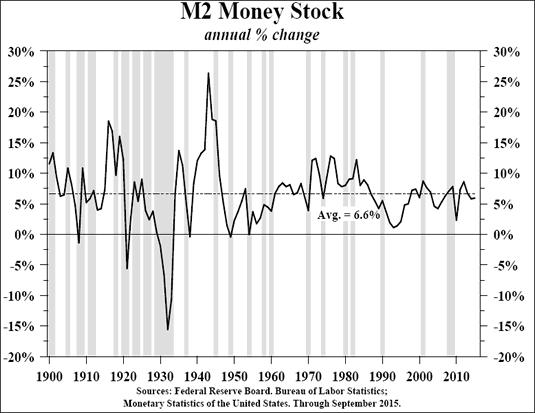

Despite the unprecedented increase in the Federal Reserve's balance sheet, growth in M2 over the first nine months of this year fell below its average rate of growth over the past 115 years, a time when the growth in the monetary base was stable and quite modest.

In addition, velocity of money, which is an equal partner to money in determining nominal GDP, has moved even further outside the Fed's control. The drop in velocity to a six decade low is consistent with a misallocation of capital and an increase in debt used for either unproductive or counterproductive purposes.

The evidence speaks for itself: the Fed cannot print money. The Fed does not have the authority or the mechanism to print money. They have not, they are not and they will not print money under present laws.

The Fed, of course, has the authority to buy certain assets, including government bonds, in the open market, but that is where their authority starts and stops. They create excess reserves by buying securities in the open market, which are then owned by the depository institutions. However, the Fed does not have the direct capability to move these funds and therefore place them in the hands of households, businesses, and other nonbank sectors. It is this transaction that creates money. Keeping short-term interest rates low for an extended period of time will not change the trajectory of the economic growth path as long as the massive debt overhang persists.

Ben Bernanke Says the Fed Prints Money

In Ben Bernanke's first infomercial on 60 Minutes in March of 2009, interviewer Pelley asked Bernanke point blank: "You've been printing money?"

Bernanke replied "Well, effectively. And we need to do that, because our economy is very weak and inflation is very low. when the economy begins to recover, that will be the time that we need to unwind those programs, raise interest rates, reduce the money supply, and make sure that we have a recovery that does not involve inflation."

Ben Bernanke Denies the Fed Prints Money

In a second 60 Minutes Fed infomercial in December of 2010 Bernanke made this claim: "One myth that's out there is that what we're doing is printing money. We're not printing money. The amount of currency in circulation is not changing."

This admission, and denial, is one of the funniest things the Daily Show covered. Please play the following video for a big laugh.

I covered the Daily Show video in my post Caught in a Massive Lie: Daily Show Comments on Bernanke's Lies Regarding "Printing Money".

So which is it? Is the Fed printing money?

The answer depends on the definition. In the first 60 Minutes interview Bernanke stated the Fed is "effectively" printing money.

In the second interview Bernanke stated "We're not printing money. The amount of currency in circulation is not changing."

Lacy Hunt has argued along the lines of Bernanke's second viewpoint.

I once gave this analogy in a presentation: Imagine you have a machine that prints perfect $100 counterfeit bills. The bills are so perfect, not even the treasury department can tell the real bill from the fraudulent bill. Next, imagine that you print $10 trillion of them and bury them in your back yard.

What happens? The obvious answer is nothing at all happens.

In one sense, that is what the Fed did. The Fed printed money and it sits as excess reserves. However, unlike printing money and burying it in your back yard, the Fed did ignite speculative asset bubbles.

I have phrased the Fed's role this way on numerous occasions: "The Fed can print money but it cannot dictate where the money goes, or if the money goes anywhere at all. Moreover, the Fed cannot give money away, and would not do so even it could."

To borrow Bernanke's word, I believe Lacy and I are "effectively" saying the same thing or at least similar things. The difference between Bernanke's counterfeiting and me printing $1 trillion and burying it in my backyard is the latter is totally benign. Boosting asset prices and creating bubbles as Bernanke has done, is not benign.

Here is the key idea: The Fed can provide liquidity support, but not capital. It cannot and will not give money away. The notion of a "helicopter drop" is fallacious.

Negative Interest Rates

Many economic illiterates have come out in favor of negative interest rates. I don't believe that would stimulate the real economy at all. Nor does Lacy Hunt. He offers this line of thought:

The Fed could achieve negative rates quickly. Currently the Fed is paying the depository institutions 25 basis points for the $2.5 trillion in excess reserves they are holding. The Fed could quit paying this interest and instead charge the banks a safekeeping fee of 25 basis points or some other amount. This would force yields on other short-term rates downward as the banks, businesses and households try to avoid paying for the privilege of holding short-term assets.

Many negatives would outweigh any initially positive psychological response. Currency in circulation would rise sharply in this situation, which would depress money growth. The Fed may try to offset such currency drains, but this would only be achievable by further expanding the Fed's already massive balance sheet. If financial markets considered such a policy inflationary over the short-term, the more critically sensitive long-term yields could rise and therefore dampen economic growth.

An extended period of negative interest rates would lead to many adverse unintended consequences just as with QE and ZIRP. The initial and knockoff effects of negative interest rates would impair bank earnings. Income to households and small businesses that hold the vast majority of their assets with these institutions would also be reduced. As time passed a substantial disintermediation of funds from the depository institutions and the money market mutual funds into currency would arise. The insurance companies would also be severely challenged, although not as quickly. Liabilities of pension funds would soar, causing them to be vastly underfunded. The implications on corporate capital expenditures and employment can simply not be calculated. The negative interest might also boost speculation and reallocation of funds into risk assets, resulting in a further misallocation of capital during a time of greatly increased corporate balance sheet and income statement deterioration.

Key Points

It's important to not get hung up over the word "printing". The key point is what the Fed can and cannot do.

- The Fed can stimulate bubbles by holding rates low

- The Fed can provide liquidity

- The Fed cannot simultaneously set interest rates and the supply of money

- The Fed cannot give money away

- The Fed cannot dictate where money goes

- The Fed can encourage but cannot force businesses or households to borrow

Debt is the problem. Yet, the Fed hopes to boost the economy by stimulating demand for more debt.

That strategy cannot possibly work as Japan has proven for decades.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2015 Mike Shedlock, All Rights Reserved.

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

Mike Shedlock Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.