FOMC Statement - Backing Off On the Rate Increases, Lowering Forecasts

Interest-Rates / US Interest Rates Mar 16, 2016 - 05:13 PM GMTBy: Jesse

The Fed recognized that growth is slow, and that inflation remains subdued.

The Fed recognized that growth is slow, and that inflation remains subdued.

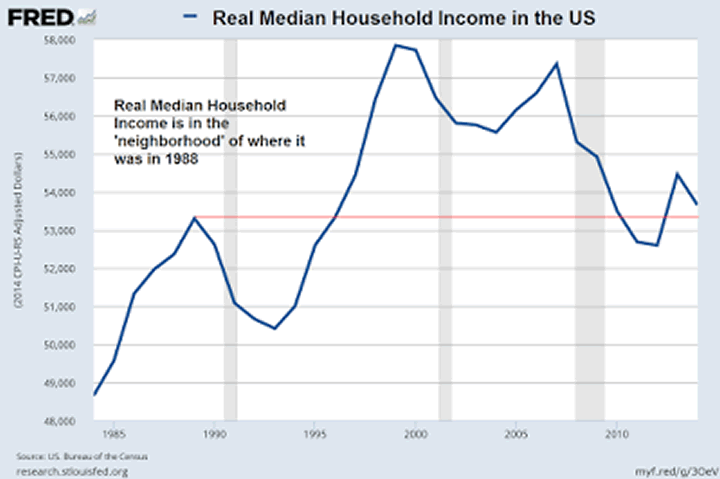

I include a chart of the real median household income to demonstrate why the recovery is so wobbly. Demand and investment are weak because people have less money to spend. Wow, what a surprise.

The pampered princes of the establishment keep point to the 'great jobs growth' while ignoring the low pay, part time nature of those jobs, and the slumping Labor Participation Rate.

And I believe that this is purposeful, because they are caught in a credibility trap. They cannot address the root problems because it risks their place in the 'system' that they have crafted that rewards the wealthy and powerful few excessively at the expense of most others.

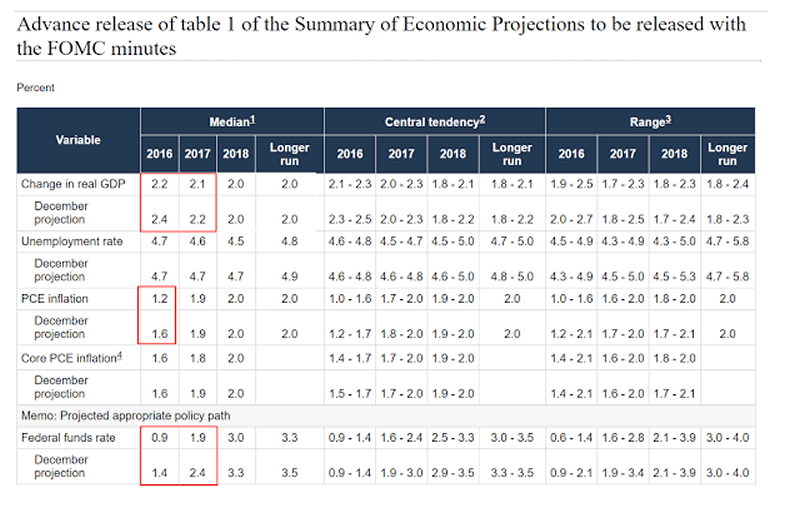

The Fed attributes this uncertainty to 'global economic and financial developments continue to pose risks.' And they have not only scaled back their inflation expectations, they have also scaled back forecasted GDP growth, which I think is still a bit optimistic.

If one looks at their 'dot plot' they are indicating a less frequent raising of rates this year, perhaps only two occasions rather than three.

I have included the Fed's data sheet below the text that shows the difference between what they had forecasted in December and what they have changed that to now.

The US dollar dropped and gold took off higher like a scalded cat. Stocks remain mixed.

Janet Yellen will be giving a press conference shortly.

Release Date: March 16, 2016

For release at 2:00 p.m. EDT

Information received since the Federal Open Market Committee met in January suggests that economic activity has been expanding at a moderate pace despite the global economic and financial developments of recent months. Household spending has been increasing at a moderate rate, and the housing sector has improved further; however, business fixed investment and net exports have been soft. A range of recent indicators, including strong job gains, points to additional strengthening of the labor market. Inflation picked up in recent months; however, it continued to run below the Committee's 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen. However, global economic and financial developments continue to pose risks. Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee continues to monitor inflation developments closely.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee's holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Loretta J. Mester; Jerome H. Powell; Eric Rosengren; and Daniel K. Tarullo.

By Jesse

http://jessescrossroadscafe.blogspot.com

Welcome to Jesse's Café Américain - These are personal observations about the economy and the markets. In providing information, we hope this allows you to make your own decisions in an informed manner, even if it is from learning by our mistakes, which are many.

© 2016 Copyright Jesse's Café Américain - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.