SPX Throws Over Two Trendlines, NDX Reverses From New High

Stock-Markets / Stock Market 2017 Dec 03, 2017 - 02:13 PM GMT

VIX challenged its mid-Cycle resistance at 14.54 this week, breaking out above its November 15 high at 14.51. It has since made a 62% retracement. A further breakout above the Ending Diagonal trendlne suggests a complete retracement of the decline from January 2016, and possibly to August 2015.

VIX challenged its mid-Cycle resistance at 14.54 this week, breaking out above its November 15 high at 14.51. It has since made a 62% retracement. A further breakout above the Ending Diagonal trendlne suggests a complete retracement of the decline from January 2016, and possibly to August 2015.

(Bloomberg) The “VIX Elephant” has awakened. And “50 Cent” is back.

At a moment when political tumult is roiling markets, volatility trading patterns closely associated with two high-rolling, but unknown, investors have re-emerged.

First, the trader who’s known as the Elephant for making big moves in the VIX -- but who’s been surprisingly quiet in recent weeks -- returned with a vengeance to start December, buying and selling more than 2 million contracts Friday to continue betting on a modest rise in the Cboe Volatility Index. That’s three times the average daily volume for all VIX options.

SPX throws over two trendlines.

SPX ramped to a new all-time high on Thursday, but gave some of its gains back in a high volume throw-over formation. It appears to have closed beneath the shorter trendline near 2650.00 while still above the long-term trendlin at 2630.00. A decline beneath both trendlines and the Cycle Top support at 2625.68 may break the uptrend.

(Bloomberg) Financial markets turned defensive, with U.S. stocks sliding and Treasuries advancing with gold after Michael Flynn pleaded guilty to lying to federal agents. Equities rebounded from the worst of the losses as Senate Republicans edged closer to passing tax cuts.

The S&P 500 Index fell as much as 1.5 percent on news that Special Counsel Robert Mueller’s investigation had pierced the White House inner circle. Equities clawed back more than half the plunge after the Senate said it had the votes to slash corporate taxes, finishing the day lower by 0.2 percent and notching the best weekly advance since early September. The 10-year Treasury yield fell five basis points Friday and Bloomberg’s dollar index slid as investors flocked to the yen.

NDX reverses from a new high.

NDX made a new high on Wednesday, but it was downhill from there with a weekly close beneath its Cycle Top and Short-term support/resistance, suggesting the rally may be finished. A decline beneath the lower Diagonal trendline at 6180.00 and Short-term support are at 6238.40 may produce a sell signal.

(Forbes) With the rash of stories about sexual harassment by male media personalities such as Harvey Weinstein, Charlie Rose, and Matt Lauer this month, testosterone-driven events have been making the headlines. While not as well reported in the media, testosterone has also been impacting financial market movements.

Some people think that overconfidence is related to testosterone levels. Certainly, surprise is the hallmark of overconfidence, and the sharp decline in technology stocks this past Wednesday caught many investors off guard. The Wall Street Journal’s coverage of the event emphasized that analysts could find no fundamental explanation for the drop. Trouble is, the magnitude of the tech stock rise over the last two years has also lacked a fundamental explanation.

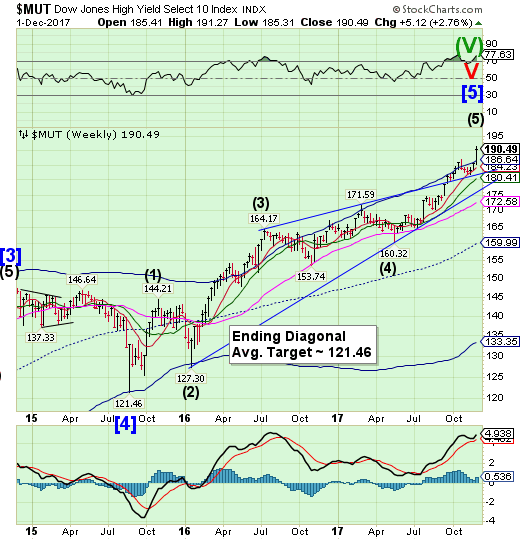

High Yield Bond Index throws over Cycle Top resistance.

The High Yield Bond Index threw over its Cycle Top at 186.64 making a new all-time high. A break of the Cycle Top and upper Diagonal trendline may tell us the rally is over. A sell signal may be generated with a decline beneath the lower Diagonal trendline at 178.00.

(SeekingAlpha) One of my favorite market anomalies is well underway, and it likely has meaningful implications for Seeking Alpha's fixed income investors. Since the advent of the modern high-yield debt market in the early 1980s, there has been a bankable calendar trade that has persisted. In the table below, readers can see that the highest excess returns over Treasuries in the high-yield market have historically been experienced in January (1.74%). December is not far behind at 1.26% and is the month that most frequently has produced positive excess returns at 85% of observations.

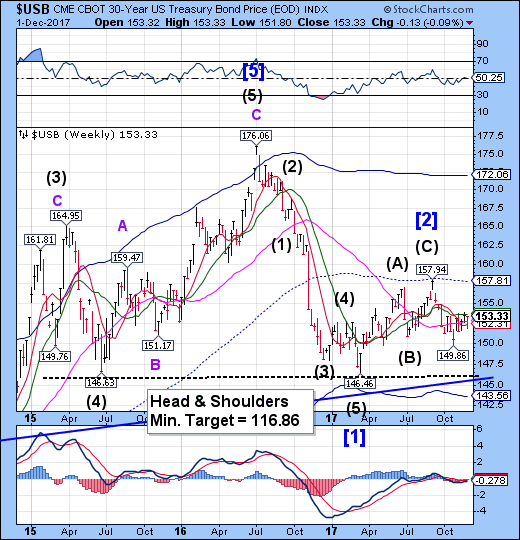

USB continues its consolidation.

The Long Bond continued to consolidate this week, closing beneath Intermediate-term resistance at 153.63. The Cycles Model suggests the period of strength may have passed, leaving USB in a potential decline that may last through mid-December.

(Reuters) - U.S. Treasury yields plunged on Friday after ABC News reported that Michael Flynn, a former adviser to U.S. President Donald Trump, said he was prepared to testify that Trump directed him to make contact with the Russians when he was a presidential candidate.

Reuters could not immediately verify the report. ABC News cited a confidant as saying Flynn was ready to testify that Trump directed him to make contact with Russians before he became president, initially as a way to work together to fight the Islamic State group in Syria.

This developed as Flynn on Friday pleaded guilty to lying to the Federal Bureau of Investigation about contacts with Russia's ambassador, and prosecutors said he consulted with a senior official in Donald Trump's presidential transition team before speaking to the envoy.

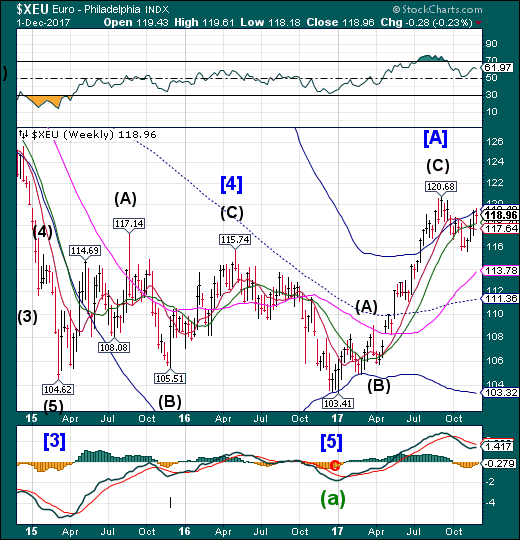

The Euro consolidates beneath its Cycle Top.

The Euro rallied through Intermediate-term support at 118.20, to consolidate beneath its Cycle Top resistance at 119.40. The rally may extend through mid-December should the rally exceed the Cycle Top.

(SeekingAlpha) The euro has shown some movement on Friday but remains close to the 1.19 line. Currently, EUR/USD is trading at 1.1906, up 0.01% on the day. On the release front, the focus is on manufacturing data, with the release of PMIs in Europe and the US. The Eurozone Final Manufacturing PMI improved to 60.1, above the estimate of 60.0. German Final Manufacturing PMI climbed to 62.5, matching the forecast. Later in the day, the US releases ISM Manufacturing PMI, which is expected to dip to 58.4 points. We'll also hear from FOMC members Robert Kaplan and Patrick Harker.

EuroStoxx declines beneath Intermediate-term support.

The EuroStoxx 50 Index fell below Intermediate-term support at3543.50 to challenge Long-term support at 3508.52. A stumble here has the potential to set off a cascading decline into motion through the end of the year.

(Reuters) - European stocks, which were recovering from early losses and set to finish the first trading day of December in positive territory, fell suddenly after ex-U.S. national security adviser Michael Flynn pleaded guilty to lying to the FBI.

U.S. stocks and the dollar fell as ABC News reported that Flynn was prepared to testify that President Donald Trump directed him to make contact with the Russians.

The news triggered a rise in the euro and in the pound, which hurt stocks as investors questioned the ability of the U.S. president to implement his tax cuts or simply to survive the political storm.

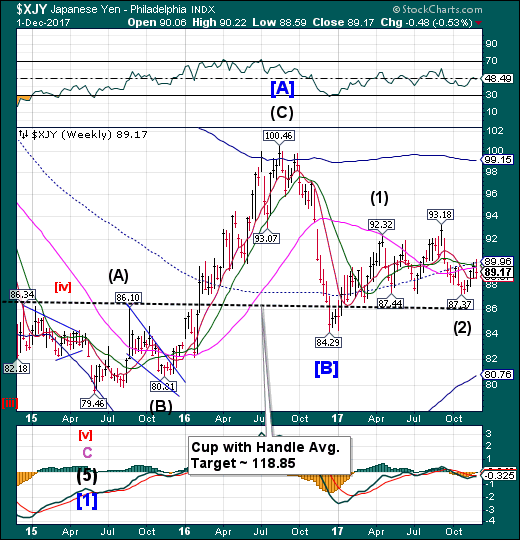

The Yen consolidates beneath mid-Cycle resistance.

The Yen pulled back from mid-Cycle resistance at 89.96 to consolidate its gains. The breakout and pullback may signal a major change in trend.

(Bloomberg) Japan’s economy is on track to close out the year expanding faster than the rate which typically sparks inflation, even after recent soft readings for consumption and prices.

Global demand remains strong, driving double-digit gains in Japanese exports in recent months and helping to fuel business investment. Capital expenditure stood out in a slew of important data released on Friday, beating expectations with a 4.2 percent gain in the third quarter.

“Overall, the pace of growth remains good," said Masamichi Adachi, senior economist at JPMorgan Securities Japan Co. "An increase in capital investment is playing a big part in this.”

Nikkei makes a partial retracement.

The Nikkei retraced 71% of its loss from the high. It has made a 72.5% retracement in about two weeks. A break beneath the Cycle Top and Short-term support at 22077.29 suggests the rally is over and may produce an aggressive sell signal. Confirmation comes at the crossing of the lower Diagonal trendline at 20500.00.

(EconomicTimes) Japan's Nikkei share average rose for a third straight day on Friday, led by oil, steel and machinery stocks, while SharpBSE 4.92 % Corp soared after it announced a return to the bourse's main board.

The Nikkei ended 0.4 per cent higher at 22,819.03 points, rising for three straight days. For the week, the index gained 1.2 per cent.

The benchmark index dipped briefly earlier when sentiment was hit by news that the US Senate had delayed voting on a Republican tax overha ..

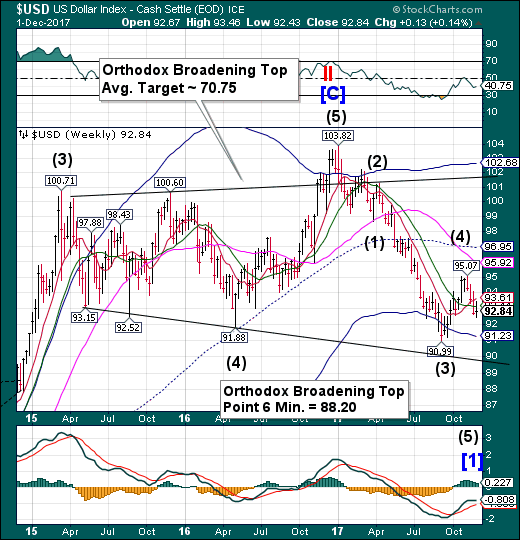

U.S. Dollar continues its decline.

USD back-tested Intermediate-term support/resistance at 93.14, then resumed what may lead to a panic decline. The lower trendline of the Orthodox Broadening Top at 89.70 may be the next attractor, but the Orthodox Broadening Top formation calls for a breakout beneath the trendline, as indicated by “point 6.” .

(Bloomberg) Whether the flattening U.S. yield curve should be a concern to traders is perhaps the biggest question in the bond market.

In the $5.1 trillion-a-day currency market, on the other hand, the trend is sending a clear signal: Sell the dollar.

After staging a two-month rally to rebound from its longest stretch of losses in a decade, the greenback is again in a slump. It’s down 1.4 percent this month, even though two-year Treasury yields have increased in 15 of 20 trading days in November. Usually, climbing short-end rates bolster the dollar.

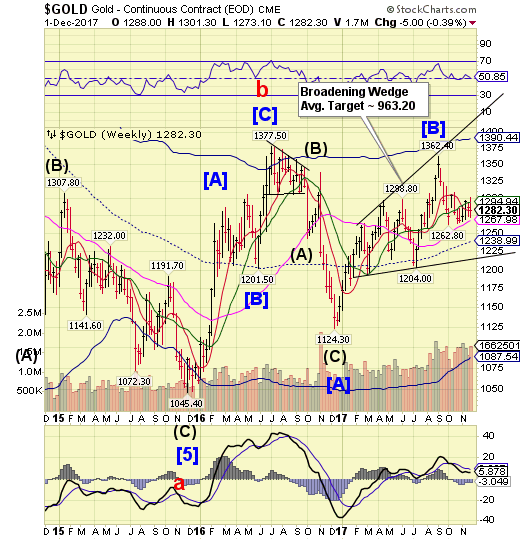

.Gold continues to consolidate.

Gold continued its consolidation between Long-term support at 1267.98 and Intermediate-term resistance at 1294.94 with no resolution of its trend. However, a further break of Long-term support at 1267.96 indicates that the decline may proceed to the lower trendline of the Broadening Wedge and possibly trigger that formation.

(SeekingAlpha) The price of gold dropped nearly 1 percent on Thursday to end the month of November essentially unchanged. The underperformance comes against a backdrop of rising sentiment as investors increasingly focus on the rally in U.S. equities and the continued positive economic news, thus eroding gold’s safe-haven appeal. In this commentary we’ll look at what investors can likely expect from gold in December, as well as a possible scenario which could lift it out of its current malaise.

Crude consolidates beneath the Cycle Top.

Crude consolidated beneath its Cycle Top resistance at 59.17. Oil’s period of strength may be over but a new trend has yet to be established. The odds are strong that we may see the price of oil decline through the end of the year.

(Forbes) Predictably OPEC and Russia have kicked the proverbial crude oil can down the road at their latest ministerial summit on Thursday (30 November). In case you haven’t heard, the oil cartel led by Saudi Arabia, and 10 non-OPEC oil producers led by Russia, agreed to extend their collective crude production cut of 1.8 million barrels per day (bpd) beyond March next year to December.

While initial doubts were expressed over extending the ongoing deal by the Russians, most believed the cuts would be extended. That’s because, in opting to intervene in an oversupplied market 12 months ago and taking on a linear market supply and demand dynamic, OPEC took a leap into the unknown without an exit strategy.

Shanghai Index loses Intermediate-term support.

The Shanghai Index declined beneath Intermediate-term support at 3347.24. This action may have invoked a sell signal. The potential for a sharp sell-off rises as the next levels of support are breached. The Cycles Model suggests that the decline may continue through mid-December

(ZeroHedge) Until a modest dip in Chinese bond yields in the past two days, 10y CGB and 10y policy bank bond yields soared by 40bps and 70bps, respectively, over the last 2 months. In fact, Chinese government notes are headed for the worst selloff since 2013, with the 10-year yield surging 86bps this year to 3.92%, and the yield of 10y CDB bonds rose above 5%. This bond rout and sharp spike in rates, caught the market by surprise, as the economic growth actually slowed in October and inflation is still below 2%.

What happened to drive up interest rates so sharply?

The most likely answer is also the simplest one: after years of aggressive debt expansion, leading up to October's Party Congress, China finally unleashed a sharp, aggressive deleveraging, which has finally been appreciated by the market in recent weeks, resulting in the biggest plunge in many local stocks in the past year, as well as a flurry of recent crashes in both Hong Kong and the mainland.

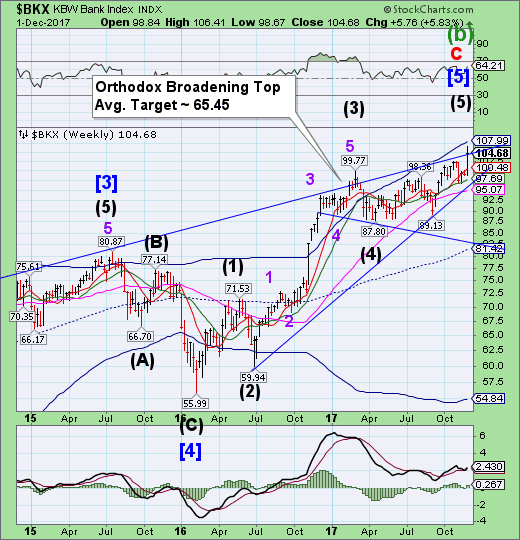

The Banking Index probes above its Diagonal formation.

-- BKX made a new high as it probed above the Ending Diagonal formation. A decline beneath Intermediate-term support at 97.69 and the lower boundary of the Diagonal formation may invoke a sell signal. The Cyclical period of strength may run out this weekend. If the Orthodox Broadening Top formation is correctly identified the next move may be beneath mid-Cycle support at 81.42.

(ZeroHedge) While mainstream media eyes have been focused on wrecked tech stocks and towering trannies, professionals in the world's largest liquidity markets have been shocked at the sudden explosion in one chart... that most everyone is hoping is not 'real'.

With central banks puking money at low or negative rates to anyone who can fog a mirror, the sudden spike in EONIA, or overnight money rates in Europe, which we first highlighted yesterday, is quite a shock in a normally stable market.

EONIA has spiked from -36bps to -24bps in the last 2 days and the authority that 'manages' this index has verified this is not a 'fat finger'.

(ZeroHedge) 'Mystery' solved... maybe.

Bloomberg is reporting that excess liquidity within Greek banks - who leant it to their credit-risky peers at notably high rates - are responsible for the sudden, scary spike in EONIA over the last two days, according to two bankers with knowledge of the matter.

Salaries that were deposited by Greek civil servants and higher receipts from repurchase agreements provided National Bank of Greece with more liquidity,the person said, asking not to be named because the matter is not public.

National Bank of Greece SA had excess liquidity of around 450 million euros ($536 million) this week, which it loaned to its peers in the country, the people said.

Other Greek banks found the rate offered by National Bank of Greece appealing, thus drawing on the cash, the people said.

(ZeroHedge) We always shudder slightly when we discuss ABN Amro, since nothing ever seems straightforward in the ongoing saga of the Dutch bank. However, this time at least nobody has died. In 2015, we noted that Chris Van Eeghen, head of the bank’s corporate finance and capital markets “startled” friends and colleagues after the “always cheerful” banker reportedly committed suicide. Van Eeghen was the fourth ABN banker suicide since the financial crisis.

(Bloomberg) With Congress getting closer to passing a tax overhaul package and the Federal Reserve talking about easing regulation, a regional banking exchange-traded fund is getting a lot of love from investors.

The SPDR S&P Regional Banking ETF, ticker KRE, took in $290 million on Nov. 29, its largest daily inflow since 2008. That added to the almost $270 million the fund received the day before, as investors line up bets that regional banks will benefit from tax reform and deregulation. The ETF has gained about 7 percent this week.

Regards,

Tony

Our Investment Advisor Registration is on the Web.

We are in the process of updating our website at www.thepracticalinvestor.com to have more information on our services. Log on and click on Advisor Registration to get more details.

If you are a client or wish to become one, please make an appointment to discuss our investment strategies by calling Connie or Tony at (517) 699-1554, ext 10 or 11. Or e-mail us at tpi@thepracticalinve4stor.com .

Anthony M. Cherniawski, President and CIO http://www.thepracticalinvestor.com

As a State Registered Investment Advisor, The Practical Investor (TPI) manages private client investment portfolios using a proprietary investment strategy created by Chief Investment Officer Tony Cherniawski. Throughout 2000-01, when many investors felt the pain of double digit market losses, TPI successfully navigated the choppy investment waters, creating a profit for our private investment clients. With a focus on preserving assets and capitalizing on opportunities, TPI clients benefited greatly from the TPI strategies, allowing them to stay on track with their life goals.

Disclaimer: The content in this article is written for educational and informational purposes only. There is no offer or recommendation to buy or sell any security and no information contained here should be interpreted or construed as investment advice. Do you own due diligence as the information in this article is the opinion of Anthony M. Cherniawski and subject to change without notice.

Anthony M. Cherniawski Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.