The Federal Reserve is Immoral

Interest-Rates / Central Banks Aug 13, 2009 - 05:26 PM GMTBy: Tim_Iacono

During the first few days of each month comes a task that is increasingly approached with dread around here and, unfortunately, that condition is likely to persist for some time.

During the first few days of each month comes a task that is increasingly approached with dread around here and, unfortunately, that condition is likely to persist for some time.

Shortly after banks make their month-end update to various short-term savings accounts that we hold, these balances are queried, only to find that, almost without exception, interest credited is less than it was in prior months and far less than it was eight or ten months ago.

Why?

Why?

Largely as a result of the Federal Reserve keeping short-term interest rates pegged to zero.

You see, aside from some Certificates of Deposit that were locked up late last year which, today, provide the strangest of feelings during a very strange period in history (i.e., feeling lucky to get about 2.5 percent interest for a one-year CD), it's nearly impossible to get more than a two percent return these days on any kind of an FDIC-insured account and, more likely than not, you'll get less than one percent.

Speaking as one who knows from experience, there's a big difference between one or two percent and five or six percent, what used to be the "minimum" rate of return for a super-safe savings account backed by the government.

More importantly, if this is causing us angst every month, I can only imagine what it's doing to the budgets of other savers whose finances are far less comfortable than ours.

Put simply, the freakishly low short-term interest rates that the Federal Reserve is jamming down everyone's throat are immoral and, maybe, just maybe, a lot more people are beginning to see this, along with other practices of our central bank that are just not right.

Maybe, just maybe, something will finally be done about reforming (or, as suggested by Rep. Ron Paul, abolishing) this banking cartel - hopefully before the Fed celebrates its 100-year anniversary in a few years.

Just to be clear on the terminology here, Merriam-Webster offers the following:

immoral

adjective

not moral; broadly : conflicting with generally or traditionally held moral principles

moral

adjective

1a: of or relating to principles of right and wrong in behavior

Setting aside questions about the dark veil of secrecy surrounding who and how much the central bank has been helping with their problem loans, problem assets, and problems staying solvent, there are at least three ways that the organization David Wessel calls "the fourth branch of government" is acting badly these days - by punishing savers, by enriching the banks, and by fleecing the poor.

Of course, none of this is really new - it all just seems a whole lot more relevant today than ever before given the current state of affairs in this country and around the world.

Punish the Savers

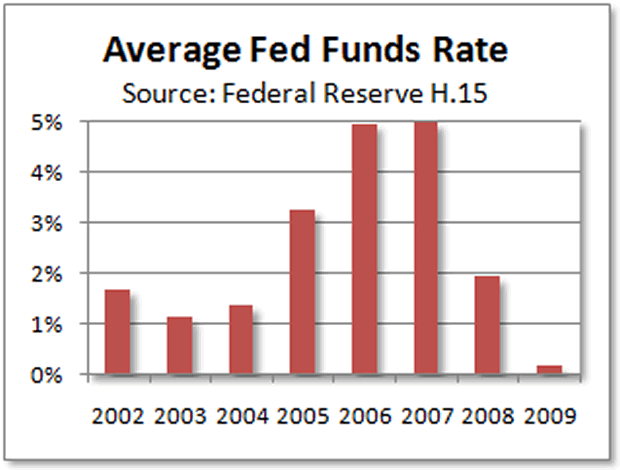

As noted above, it used to be that you could always count on getting five or six percent interest in a "no-risk" savings account backed by the FDIC. In fact, going all the way back to 1955 (when the interest rate data at the Fed's website stops), the average short-term lending rate is right between those two marks - 5.66 percent.

Ever since I was a teenager, I can remember thinking, "If I could somehow amass a million dollars, that would surely generate enough money to live on for the rest of my life".

Well, welcome to the 21st century, where the asset bubbles keep a-poppin' and the interest rates keep a-droppin'.

Over most of the last hundred years, aside from the dollar losing more than 90 percent of its purchasing power (versus a loss of zero during the prior ten decades), there hasn't been too much to complain about in the Fed's management of money and interest rates but, since asset bubbles and the attendant "mopping up" process have become a way of life, the rate of return on savings has been abysmal.

With the exception of the "baby-steps" rate raising campaign a few years ago, the Fed funds rate has been below two percent since 2002 - after the decade's first asset bubble met its pin.

Now, if there was a good reason for keeping rates so low, this might all make some sense to senior citizens who have looked disappointingly at their bank statements for years, but given the fact that the low-rates in 2002-2004 led to the housing and credit bubbles forming and then bursting a few years later, and here we are with even lower rates today, all of this should make anyone with half a brain realize that there is something seriously wrong with the system as it currently operates.

In a nation in dire need of internal savings, the fact that savers are being punished as never before is just plain wrong - immoral - and the idea that we live in an era of "low inflation" is just salt rubbed in the wounds of senior citizens who, year after year, watch prices for health care and energy rise by some multiple of the one or two percent they can earn on their savings.

Twenty years from now (perhaps sooner), they'll look back on today's monetary policy and say to themselves, "What were they thinking, punishing the savers like that when the U.S. desperately needed savings?"

Enrich the Banks

As if it weren't bad enough that savers are cheated every time the Federal Reserve lowers interest rates, the worst part is that banks are the beneficiaries.

You see, in addition to buying up many of the bad assets previously held on bank's books over the last year or so - the result of waves of imprudent bank lending - when the Fed lowers interest rates it helps to make the business of banking much more profitable and, conventional wisdom has it that our financed-based economy will then begin to recover.

And when the banks can borrow at these super-low rates, that means that savers can't earn much more in interest.

And when the banks can borrow at these super-low rates, that means that savers can't earn much more in interest.

Banks come first and savers are far down on the list.

Why does the system work this way?

Well, most people haven't got a clue what the Federal Reserve is or what it does (though, understandably, there is growing interest in this topic, ever since the wheels fell off of the global economy last fall), but the crucial bit of information that the now-slightly-more-curious public should learn quickly is that the central bank was not set up to help the people or the government, but, rather, to help the big banks.

In fact, according to G. Edward Griffin, who happened to write a whole book on the subject, the very reason that the Federal Reserve was formed back in 1913 was so that big banks could wrest back control of the banking system from the many small, fledgling, independent banks all around the country that were taking away their business.

Look around you today. You might see lots of little banks failing, but only a few large ones ever go under and none of the country's biggest banks ever fail.

The Fed was created by the big banks, for the big banks, and its unwritten "mission statement" is to do whatever it takes to ensure the survival and profitability of those big banks, getting the government to step in with public money when necessary for "the greater good", effectively socializing the losses while keeping the gains in private hands.

That's why what we have today - a wholly unsustainable system of ever-expanding credit and debt dominated by a handful of "too big to fail" banks - keeps getting propped up.

The masses are led to believe that credit is the "lifeblood of the economy" when, in fact, credit is the lifeblood of a banking system that has, over time, sucked the life out of the economy.

It's hard to imagine anything that is more immoral than the Federal Reserve's role in this process, now almost a hundred years in the making.

Fleece the Poor

In arriving at the third and final way that the Federal Reserve is immoral, clearly, that last thought in the previous section was premature.

In fact, there is one very good example of something being done today by the central bank that is even more immoral than a nearly century long wealth transfer from the public sector to the private banking system - the ongoing assistance being provided by the Fed in helping the banking system reach out and find new customers so that every possible dollar can be extracted from them.

You see, the country's big banks (along with the central bank that serves their interests) would much prefer that poor people all across the country not go to a place like you see to the right and, for a small fee, convert their paycheck into cash and forever live within their means.

Bankers would much rather see the nation's poor open up checking accounts and then venture further into the world of modern day banking, quickly learning to spend well beyond their means.

Left unsaid in the Fed's many efforts to reach out to the "unbanked" is that checking accounts are a sort of "gateway drug" for many people - a road to debt serfdom where, in addition to paying interest on money borrowed to buy stuff that they don't need, these "newly banked" poor will also be fleeced by a bewildering array of fees and charges in a system that is set up to systematically suck as much money out of as many people as possible.

Over the years, the Federal Reserve has made great efforts to attract new customers for banks, in some cases providing cartoon characters to make the whole idea of debt serfdom seem like a friendly sort of condition, much in the same way that Joe Camel once attracted new smokers.

Under the guise of "education" and with "consumer protection" as its goal, the Federal Reserve might seem to be "looking out for the little guy", but they're not. They've had the power to do this for many years now but, for obvious reasons, have exercised their "power to protect" the consumer only sparingly, allowing millions of subprime borrowers to give the housing bubble one last giant hurrah before it finally burst.

Fortunately, it appears that the Obama administration would like to see the American consumers' interests watched over by some other group and for good reason. A report earlier in the week in the Financial Times detailed how big banks in the U.S. plan to extract almost $40 billion in overdraft fees from American consumers whose balance sheets haven't been bolstered by government bailouts.

It seems that, with the collapse of the mortgage finance bubble, big banks are now reverting to a profit model that is driven more by extracting fees from their customers wherever possible and overdraft fees from the cash-strapped are "the mother lode".

A full 90 percent of overdraft fees come from just 10 percent of all checking accounts and most of this 10 percent have low credit scores and/or are recent entrants to the world of mainstream banking.

Not surprisingly, the highest overdraft fees come from the biggest banks - Citigroup, Bank of America, JP Morgan Chase, Wells Fargo, SunTrust, and Citizens Bank.

For banks, overdraft fees are a low risk, high profit part of their business, not something that is usually mentioned as part of the Fed's outreach programs. It is a sophisticated, large scale sort of "payday loan" system that many Americans fall prey to and, as long as customers have their payroll checks automatically deposited, the bank will always have first crack at the money and people will continue to spend more than they make because, when you get down to the very basics here, most people aren't very good at math.

But, banks are.

Maybe Ron Paul is right - the Fed should be abolished.

Then markets could set interest rates, banks would have to fend for themselves, and there would be one less group helping to extract what little money the poor have left.

By Tim Iacono

Email : mailto:tim@iaconoresearch.com

http://www.iaconoresearch.com

http://themessthatgreenspanmade.blogspot.com/

Tim Iacano is an engineer by profession, with a keen understanding of human nature, his study of economics and financial markets began in earnest in the late 1990s - this is where it has led. he is self taught and self sufficient - analyst, writer, webmaster, marketer, bill-collector, and bill-payer. This is intended to be a long-term operation where the only items that will ever be offered for sale to the public are subscriptions to his service and books that he plans to write in the years ahead.

Copyright © 2009 Iacono Research, LLC - All Rights Reserved

Tim Iacono Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.