Why the Housing Market Has Failed You. Five Major Failures of the US Housing Market

Housing-Market / US Housing Jul 21, 2007 - 12:36 AM GMT

I'm sure many of you already read the article about The Real Estate Prayer Luncheon in Florida where a group of hopeful agents prayed that the housing slump will end. I actually think this is a great idea to resurrect the housing market. So in light of this, I am going to pray that my new book coming out called The Wealth via Failure Code will be a major success. I'm praying that all of you will buy it. Since we are living a surreal housing environment, I figure writing a book with Orwellian themes will tickle many of your fancies.

I'm sure many of you already read the article about The Real Estate Prayer Luncheon in Florida where a group of hopeful agents prayed that the housing slump will end. I actually think this is a great idea to resurrect the housing market. So in light of this, I am going to pray that my new book coming out called The Wealth via Failure Code will be a major success. I'm praying that all of you will buy it. Since we are living a surreal housing environment, I figure writing a book with Orwellian themes will tickle many of your fancies.

There are 5 major failures with the current housing market. There are more, but 5 large items that need to be addressed immediately since they will impact the market in the next few months. Anyone buying a home in this market is tempting fate; it is reminiscent of the woman who stuck her arm in a Siberian tiger's cage and had it ripped from the socket. Nature does what it will always do. And housing economics and bubble psychology will always do what it always does. All market indicators are blinking red. By reviewing MLS data, nearly every large metro market in the US is reaching record inventory even after adjusting for population growth (we love making babies). Foreclosures and REOs are hitting the market like Tsunami waves. Sub-prime outlets are systematically being eradicated from the market. And fear of risky debt infecting the general market is prevalent. No wonder why this group of agents in Florida went to church to find housing religion.

Major Foreclosures Will Hurt the Public

Losing your home royally sucks. I'm not sure if we can find anything positive about foreclosures. It hurts families. It also displaces families and forces new inventory on the market via REOs. Sometimes foreclosures happen because a person loses a job or a family emergency. In usual housing markets, this was the majority of cases. Now, the majority of foreclosures are due to buying more than you can afford. Are you going to feel sorry about the person that bought a $700,000 home on a $14,000 a year income only to realize that maybe $6,000 a month is too much when you net $1,000? Maybe the blame should fall a little bit on the agent hungry for their commission check wouldn't you think? Even a back of the napkin calculation will show you this wouldn't work.

The demise of many sub-prime outlets is justified. They created their undoing for instant gratification and fast money. Easy come, easy go. When I worked as an agent, I would constantly hit heads with brokers that laughed about creative financing they were able to pull on buyers. I would look at financial statements and shake my head as buyers fudged numbers encouraged by brokers to get into overpriced homes. “Don't worry, banks never check especially if we go stated income. All we need is your signature here stating you make $100,000.” I would hear statements like this constantly and this was a few years ago. God only knows what has been going on in the shady underbelly of housing since I left the industry. Oh yeah, we are already seeing what is going on. Ridiculous loans on massively overpriced homes with folks unable to afford the monthly payment.

Now foreclosures also hurt the market because it adds further inventory to a market that is reaching epic numbers. Prices are falling in many regions already. Many in Southern California look at the median price and with a look of dismay, see the median increasing! What is going on here? Well high priced homes are selling and lower priced homes are sitting on the market. A case of the Miss Universe contest; anyone that wins is beautiful. Yet they don't represent a sample of the population. That is why sales are dropping in amazing numbers. But the market strain is taking a toll on many areas. Let us take a look at some hard data for Southern California :

So we have plenty of data showing that many zip codes in Los Angeles County are going down. And you'll notice a general pattern here. Most of the homes listed above are in the $300 to $700 thousand dollar range; your typical Real Home of Genius . So why are median prices still going up? Well you'll also notice that the sales numbers are rather low. If we are to look at the high priced areas selling, you'll notice sales numbers and prices are much higher. Obviously looking at the current aggregate median of $550,000 does very little in highlighting the overall market conditions in Los Angeles County . The devil is in the details. Suddenly we have a spiritual overtone to housing. Maybe because certain price tags are actually sinful.

And notice of defaults are up a record 148% statewide. What this means is more foreclosures coming online in the next few months and growing inventory further pushing the median price down. And this isn't just for California . Nationwide according to RealtyTrac foreclosures are up a whopping 17% as of Q3 of 2006. Many areas such as Miami , Fort Lauderdale , Las Vegas , and Denver are seeing numbers in foreclosures jump by 50% year-over-year. With the implosion of the sub-prime market and the prospect of more inventory hitting the market, this summer will break the stalemate of sellers thinking their home is worth what it once was. Banks will sell properties quick and dirty even if it means cutting prices to the bone.

Mortgage Debt Largest Debt in the US

Consumer spending makes up 70% of the $13.7 trillion dollar US economy. Mortgage debt has increased at a radical pace due to underwriting standards and the lax monetary policy taken by the Federal Reserve. Take a look below at the growth of mortgage debt in the US :

You'll notice that in a matter of 5 years, we practically doubled the outstanding amount of mortgage debt. Mortgage debt outstanding rivals the amount of consumer spending that makes up 70% of our economy. Now you can understand why a spook in the mortgage market will send the market into a tailspin. The interesting thing to note is that as mortgage debt increases each year by double-digit figures, according to our government plutocrats we are facing very minor inflation. Too bad for most middle-class Americans, housing payments are the largest line-item payment each month. Oh yeah, and based on ridiculous hedonics used at the Bureau of Labor and Statistics, we are facing moderate 3 to 4 percent inflation according to the Ministry of Truth. Keep in mind they use owner's equivalent of rent, take out energy and food prices, and pretty much anything useful for a daily life. As a consolation they'll adjust for electronics since we buy computers and HDTVs on a weekly basis. Good job government.

We know how scared the market is right now. Remember long ago (in March 2007) with the sub-prime implosion and the stock market dropping 400+ points in one day? Fears of mortgage implosions sent the market down hard. The market recovered quickly because all the talking head pundits would have you believe that it was contained principally to the sub-prime market. They also discussed in great detail the legend of the summer housing easter bunny and how the market will come roaring back. Summer is here and no bouncing bunnies are to be found. We now have Bear Sterns issuing warnings about Merrill Lynch pulling assets out of a mortgage hedge fund that made idiotic bets. Bear Sterns and Merrill Lynch are not New Century Financial. This is as prime as it gets. Bear is throwing money to keep this afloat because it is a major embarrassment to their asset management. The market got hit once again and bad money is chasing more bad money to keep the party going a little bit longer.

Keep in mind that we are only entering the first stages of trillions of dollars in mortgage resets. Nothing is contained. The main question everyone should be asking is can the American public sustain monthly payment jumps while real estate prices fall? If the answer is no, how long can the market withstand jumping resets and foreclosures before a panic arises? Ronald Reagan had one thing right when he said a “ Recession is when a neighbor loses his job. Depression is when you lose yours.”

Public Infatuation with all Things Real Estate

Never has the industrial world been so infatuated with real estate. Turn on your television and you'll see shows such as Flip this House and Extreme Makeover . If you are up passed 1am or stay home on a weekday from 10-2pm, you'll see infomercials with tanned Hawaiian shirt wearing gurus showing you how no money down is the key to financial success. Robert Allen actually was a pioneer of the no money down technique. The funny thing is that his ideas were geared toward sophisticated investors that were able to get sellers to buy/create notes, assume mortgages, and find short-term carry over loans. Not easy at all for anyone that has tried it. Reading his books, I learned a lot but it was not simple like the title implied. Fast forward to now. No money down is institutionalized. Forget no money down, we have lenders giving you cash-back at closing! By the way, cash back at closing is illegal but so is lying on a mortgage application but apparently what is illegal in one area of justice, is perfectly okay in another.

Then we have the boom of Home Depot and Lowes. Stores that cater to the housing infatuation. Ceramic tiles, granite countertops, pseudo-rock pool fountains, stainless steel stovetops, and everything that would arouse a housing enthusiast. These things don't come cheap. They are expensive and for practical purposes, don't do anything else than visually make your home look better; a boob job for your house or a tummy tuck for your condo. But wages haven't increased in relation to other cost of living items. How can Americans afford this? Come in American Express and Visa to the rescue. Americans carry an amazing amount of credit card debt. Debt that usually has rates of 20%+ and has so many penalties, you'd think you were at a Detroit Red Wings hockey game. Yet home prices kept climbing and Americans needed more credit for their growing consumption appetite. Welcome home equity withdrawals.

*Source: The Economist

To keep up with the hunger of spending, folks decided to slap a virtual Diebold ATM to their house, and start pumping out equity at amazing rates. The sun was bright again and grass was greener on your Bermuda lawn. The problem however is that home equity lines of credit and home loans are other credit instruments. In other words, you need to pay the money back. All that was created was a low rate loan locking yourself into an overvalued asset. You became your own appraiser. Your house has $100,000 in equity? Okay, here's the money at 7 percent. But what if your house isn't worth more than $100,000? Ahhh, the pickle that we are currently in. Maybe housing isn't worth what the market is saying. Maybe $500,000 for a 500 foot box in an area where rents go for $900 isn't so economically priced. But now you have a 2nd mortgage on a house you can't unload. This love affair had to end and summer seems like a good time to end many flings.

Redefining Failure and Success

We've all heard about the 25 year old mortgage broker making $15,000 a month. Or the 22 year old agent with a high school diploma raking in six-figures a year simply for showing houses. We've also heard about a 24 year old investor that went $2.2 million in debt with an income of less than $40,000 a year. The theme? Getting rich quick isn't enough. Getting rich young became the new standard. Forget about education because school is for elites who care about issues surrounding the world. Street knowledge and the love for the almighty dollar became the new Mammon.

We obviously live in a capitalist society. Yet this ideal breaks down when you have a system flooding the market with easy credit and encourages frivolous and downright idiotic spending. The public subsidizes this spending on the back of false inflation numbers and a higher cost of living. Think this isn't the case? Go to Europe and see how far your dollar goes. You have a market telling you that saving is pointless. Why save when bank rates are giving you 1% and real estate is making you 20%? Interesting to note that historically real estate trends with inflation, which we already mentioned by the government's own data, is hovering around 3 to 4 percent. So if we are to use logical thinking, this would imply that either inflation is amazingly understated or housing is incredibly overpriced. I knew basic college logic and philosophy would come in handy at some point in life.

But I have a news flash for you. Failure is wealth . Amazingly, we have folks to be proven bad at what they do, claiming to be experts! They are passing on their real estate horror stories as a method of investing. Call it what it is. An idiot with a fascinating story garnering massive attention and creating a social epidemic; like Paris Hilton going to jail. But no way can you call these people gurus or investors. Last time I looked at a dictionary investing meant making money, not losing it. To go further with this, Paris has indicated that she will use her stature for improving the world. Well good for her. But what about all the people that are currently making an impact on the world; firefighters, police officers, volunteer workers at shelters, missionaries, soldiers, and those in the helping professions? Why don't we profile them? Because psychologically we love seeing losers turn into winners. This goes back to the Horatio Alger rags to riches story. It is part of the American psyche. However taking advice and guidance from these modern day gurus is like praying for real estate to go up. Oh yeah, we're already doing that.

You should be a guru too! Your voice has as much weight as others. Here is the recipe for success. Do everything possible to fail; gamble, cheat, commit fraud, and smoke weed because we all love a good joint. If you can, do these things all at once. I haven't had any luck combining all four but maybe you can succeed where I failed. Then, make it all public. Get the paparazzi to follow you or chronicle it online. Don't commit crimes that'll put you away for life, that'll defeat the purpose. Mortgage fraud seems to be okay so go for that one. Then, decide to write a book and ride the gravy train to Tuscany. See! And you wonder why I'm writing a book? It is the key to riches in this country baby!

Destroying the Middle Class Psychology

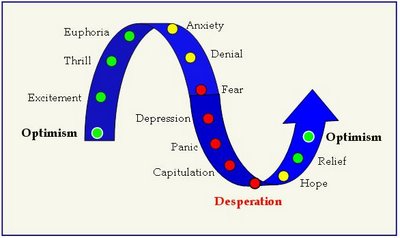

Hard to believe we are only entering the first stage of this bubble. Bubbles follow a systematic pattern . Below you can see the typical cycle of any bubble:

*Source: Real Estate Decline

Currently we are between denial and fear. You still have your delusional sellers pining for yesteryear prices but a market with growing inventory from builders and REOs is quickly changing the pace of things. As far as bubbles are documented, data going back to the 1600s, this pattern is typical and rarely fails to follow through. Timing is always an issue but the stages seem to hold true.

So what does this do to the middle-class? What is the middle-class after all? We always hear political pundits using this term. Well in terms of median income for the U.S. , it is approximately $47,000 per year. Net worth looks like this:

*Source: CNN Money

And 70% of all households own their home. Keep in mind that the net worth statistics include a large portion of equity in home. So even though the numbers may look high, it is because we are in a nationally distorted housing market. So you can see that a national decline in housing will impact a large portion of Americans. I'm fascinated with the 70% number. 70% of our economy is based on consumption and 70% of Americans own their home. Coincidence? I think not. What say you dear public?

By Dr. Housing Bubble

Author of Real Homes of Genius and How I Learned to Love Southern California and Forget the Housing Bubble

http://drhousingbubble.blogspot.com

Dr. Housing Bubble Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.