Fed’s Destructive Monetary Policies Expose Mainstream Economic Fallacies

Economics / Economic Theory Feb 10, 2013 - 12:12 PM GMTBy: Frank_Shostak

At the annual meeting of the American Economic Association in San Diego (January 4–6, 2013), Harvard professor of economics Benjamin Friedman said,

At the annual meeting of the American Economic Association in San Diego (January 4–6, 2013), Harvard professor of economics Benjamin Friedman said,

The standard models we teach … simply have no room in them for what most of the world’s central banks have done in response to the crisis.

Friedman also advises sweeping aside the importance of the role of monetary aggregates. On this he said,

If the model you are teaching has an “M” in it, it is a waste of students’ time. Delete it.

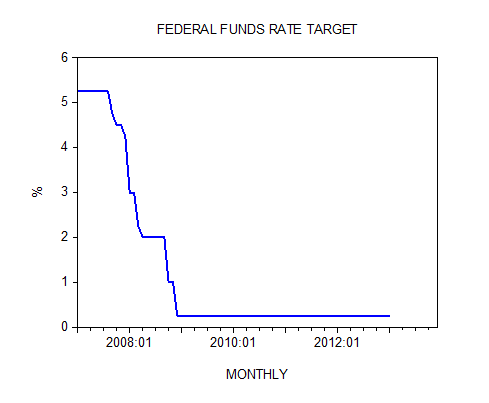

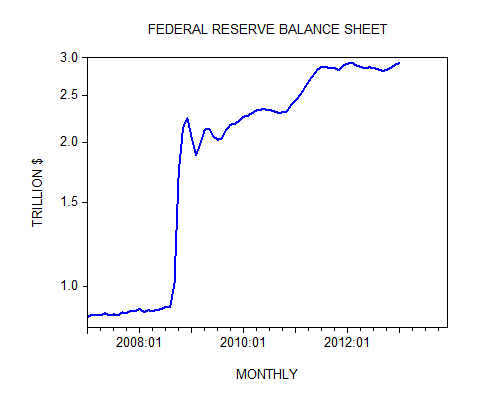

According to most economic experts, the Fed has re-written the central banking playbook, cutting interest rates to near zero and tripling its balance sheet by buying bonds. The federal funds rate target is currently at 0.25%. The Fed’s balance sheet jumped from $0.86 trillion in January 2007 to $2.9 trillion in January 2013.

Professors who say they agree with the Fed’s approach to the 2008–2009 economic crisis are nonetheless challenged to explain this new world of central banking to their students. They argue that the dramatic action by the central banks to counter a global financial crisis cannot be explained by traditional models of how monetary policy works.

So what seems to be the problem here?

According to traditional thinking, a lowering of interest rates stimulates the overall demand for goods and services, and this in turn, via the famous Keynesian multiplier, stimulates general economic activity. Furthermore, according to traditional thinking, massive monetary pumping should also lead to a higher rate of inflation.

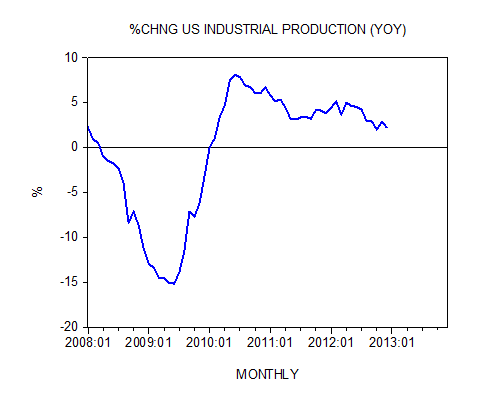

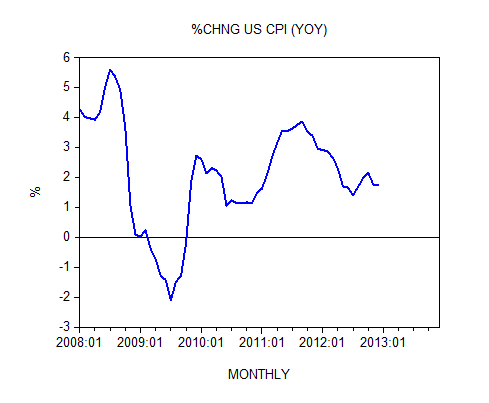

Yet despite the massive monetary pumping, both economic activity and the rate of inflation remain subdued. After closing at 8.1% in June 2010, the yearly rate of growth of industrial production fell to 2.2% in December 2012. The yearly rate of growth of the consumer price index (CPI) fell to 1.7% in December 2012 from 3.9% in September 2009. Additionally, the unemployment rate stood at a lofty 7.8% in December 2012 with 12.2 million people out of work.

So why has the massive monetary pumping by the Fed, and the near zero federal funds rate, failed to strongly revive economic activity and exert visible upward pressure on the prices of goods and services?

Is the comment by Benjamin Friedman, that money is not relevant, now valid?

No. The fact that the massive Fed pumping has failed to produce the expected results—along the lines of mainstream models—does not mean that the money supply is no longer important to understanding what is going on.

The fact that economic activity is currently not responding to massive monetary pumping, as in the past, indicates that prolonged reckless monetary policies have severely damaged the economy’s ability to generate real wealth. So contrary to Friedman, we maintain that money matters very much. However, contrary to mainstream thinking, an increase in money supply does not grow, but rather destroys the economy.

The ongoing monetary pumping, coupled with an ongoing falsification of the interest rate structure, has caused a severe misallocation of scarce real capital. As a result of reckless monetary policies, a non-wealth-generating structure of production was created. Obviously, with the diminishing ability to generate real wealth, it is not possible to support, i.e., fund, strong economic activity.

Monetary pumping is always bad news for the economy because it diverts real funding from wealth generating activities to wealth consuming activities. It sets in motion an exchange of something for nothing.

As long as the economy’s ability to generate wealth is functioning, the reckless monetary policies of the central bank can be absorbed. Under such conditions, market watchers get the false impression that "loose" monetary policies are the key drivers of economic growth.

When wealth-generating activity, as a percentage of the total economic activity, drops below a certain point, reality takes over and general economic activity has to fall. This decline in wealth-generating activity undermines the ability to lend. Real funds for lending have also declined and lending "out of thin air" results. Following suit is the growth of the money supply and price inflation.

As a result of the weakened wealth generating process, formerly subsidized non-wealth-generating activities come under pressure. Since they don't produce enough to sustain their own viability, they are forced to lower their prices of goods and services to stave off bankruptcy. According to Mises,

As soon as the afflux of additional fiduciary media comes to an end, the airy castle of the boom collapses. The entrepreneurs must restrict their activities because they lack the funds for their continuation on the exaggerated scale. Prices drop suddenly because these distressed firms try to obtain cash by throwing inventories on the market dirt cheap.[1]

It is not clear whether we have already reached this stage in the US. But despite massive pumping by the Fed, economic activity remains subdued and this raises the likelihood that the US economy is not far from sinking into a black hole.

The Fed's aggressive pumping policies highlight the destructive nature of loose money. Popular mainstream theories aside, the actions of the Fed have proven that monetary pumping cannot grow an economy. It can only set in motion a process of destruction.

Many mainstream policy thinkers are of the opinion that the Fed’s policies can be made more effective by making the central bank’s policies transparent and consistent. The following remarks, by the prominent economist Michael Woodford and reported by Reuters, are but an example:

"The recent events ... have given us a lot of reason to change what we teach when we talk about monetary policy," said Michael Woodford, a professor at Columbia University and one of the most influential current thinkers about monetary policy.

In future, Woodford said he would incorporate a lot more discussion about the importance of stability in the financial sector on the macro economy, and tell students why future expectations for central bank interest rates can be vital.

"Explain why expectations are important for aggregate demand," he told the panel. . . .

"Make it credible that the central bank will actually follow through with the policy it is indicating," Woodford said, referring to the importance of convincing businesses and households to invest and spend.

The belief that greater transparency and consistency in the Fed’s policies would lead to stable economic growth is fallacious. We have seen that it is the Fed’s actual policies that are the key factor behind the destruction of the wealth generating process. Hence, the damage inflicted by these policies cannot be avoided even if the Fed is consistent and transparent.

The key problem with the mainstream perspective is its notion that all that is needed for economic growth is to boost the demand for goods and services, i.e., demand creates supply. It is for this reason that mainstream thinkers held the view that increases in the money supply, and the subsequent increase in the overall demand for goods and services, is a catalyst for economic growth.

But we have seen that once money is pumped, it sets in motion an exchange of something for nothing, i.e., the diversion of real wealth from wealth generators to non-wealth generators, and subsequently to economic impoverishment.

Summary and conclusion

At the recent American Economic Association meeting, academic economists said that the latest monetary policies of the Fed made it difficult to employ accepted theories regarding the effect of central bank policies on the economy. Experts are of the opinion that in the “new world,” because of Fed policies, there is little room left for the money supply to explain why economic activity and the rate of inflation are subdued despite, the Fed’s aggressive policies since 2008. Contrary to mainstream thinking, the aggressive policies of the Fed have highlighted the destructive nature of loose monetary policy. Money supply matters more now than ever.

Frank Shostak is an adjunct scholar of the Mises Institute and a frequent contributor to Mises.org. He is chief economist of M.F. Global. Send him mail. See Frank Shostak's article archives. Comment on the blog.![]()

© 2013 Copyright Frank Shostak - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.