5 Reasons Why Commodities Are the Investment Place to be in 2018

Commodities / Investing 2018 Feb 18, 2018 - 12:03 PM GMTBy: Richard_Mills

The stock market pullback of the last couple of weeks has shown that markets are jittery, and will likely be volatile for awhile as investors keep a vigil on rising bond yields (inflation) and potential interest rate hikes. In these uncertain times, one sector that appears to be holding its own, and then some, is commodities. Let’s examine why this is the case, and why commodities are going to be THE place to put your money in 2018.

The stock market pullback of the last couple of weeks has shown that markets are jittery, and will likely be volatile for awhile as investors keep a vigil on rising bond yields (inflation) and potential interest rate hikes. In these uncertain times, one sector that appears to be holding its own, and then some, is commodities. Let’s examine why this is the case, and why commodities are going to be THE place to put your money in 2018.

The correction

The stock market correction (let’s not call it a crash) that suddenly saw everyone’s trading apps turn red on Monday Feb. 5 shocked investors. The S&P 500 was off 4.1% at 2,648 - the worst fall in 6.5 years. The rot spread to Asian stock markets the next day, with Japan’s Topix index falling 6.3%, South Korea’s Kospi losing 2.6%, and Australia’s S&P/ASX 200 down by 3.7%.

Predictably, equity investors swiftly moved their holdings into safe havens - bonds, the dollar and gold - with all flights to safety pointing up on the 5th. The yield on the 10-year US Treasury bill hit 2.88%, the US dollar rose against competing currencies, and gold defied its usual trend of moving in the opposite direction of the dollar by gaining six tenths of a percent to $1,345 an ounce.

The correction was generally blamed on inflation fears and worries about the world’s central banks raising interest rates, which would make stocks a less attractive investment than income-bearing instruments like bonds. Algorithmic trading is also said to have played a role.

Adam Hamilton of Zeal Intelligence offered a better dissection, noting that the S&P 500’s near 9-year stock bull represented an increase of 324%. The index at the end of January was sporting a price to earnings ratio of 31.8X, where historical fair value is 14X and bubble territory is 28X. The writing on the wall for a major selloff appeared on Friday the 2nd with the US jobs report.

“Average hourly earnings beat expectations by climbing 2.9% year-over-year, the hottest read on wage inflation since June 2009. That triggered inflation fears with the 10-year Treasury yield already at 2.78%,” Hamilton wrote.

Few think that the correction will echo something like the 1987 Black Monday 22.6% plunge which turned the then-bull market into a bear. There have been 11 under-20% corrections since 1976. US GDP is targeted to grow at 2.5% and unemployment is down to 4.1%, showing health in the US economy and likely, continued confidence in US stocks.

Already the markets seem to be tracking back upward, with stocks posting a three-day winning streak as of Tuesday.

Commodities strong

At the end of 2017 the Bloomberg Commodity Index, which measures returns on 22 raw materials, had the longest rally on record dating back 27 years to 1991. The index was propelled by major yearly gains in copper, which had its best month in 30 years in December, oil, which moved above $60 a barrel for the first time in over two years, and gold, up for the second year in a row, by 12.5% in 2017.

The roll continued into the New Year, with the index hitting a three-year high on Jan. 5 due to what the Financial Times described as the global economy’s best period of growth (measured in manufacturing activity) since the 2008 financial crisis. The FT named oil’s move above $68 and into backwardation (where spot prices are higher than oil futures contracts), zinc vaulting to a 10-year high, and thermal coal trading above $100 a tonne, as examples of commodities strength.

I think that we are entering a secular bull market in commodities - one that could last for several years if not the decade-plus commodities supercycle that lasted roughly from 2000 to 2014, and I’m offering five reasons why.

1.Inflation

The fear of inflation was a major determinant of the Feb. 5 stock market pullback and it’s easy to see why. With expectations of wage inflation from the Feb 2 jobs report, bond market participants saw a strong possibility of their investments being eroded by inflation when their Treasury bills reach maturity. This caused a selloff in T-bonds, which caused prices to fall and yields to rise. Inflation is a bond’s worst enemy because it erodes the purchasing power of a bond’s future payout. The higher the rate of inflation, or expectation of inflation, the more yields rise, because bond investors demand higher yields to be compensated for inflation risk.

Commodities can be the beneficiary of higher bond yields especially if long-term interest rates rise. Bloomberg columnist Shelley Goldberg points out that the US 10-year Treasury yield is one of the best metrics for determining the direction of commodity prices:

Should long-term rates rise enough that inflation becomes a concern, investors will turn to commodities like gold and crude oil as havens. In addition, governments of heavy commodity-importing nations may hoard inventory as they did in 2008, severely driving up prices of commodities such as wheat and copper. And portfolio managers will turn to commodities as a way to diversify as they sell equities, which tend to suffer in high-interest rate environments as borrowing costs for businesses rise.

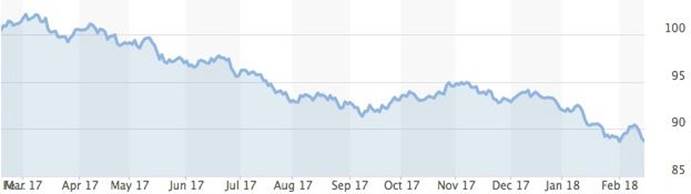

The chart below shows the correlation between the 10-year Treasury and the Bloomberg Commodity Index over the past year.

An even more interesting chart to look at is the historical 10-year yield. It shows that yields have been dropping for the last 36 years!

Not since 1988 have yields risen and that is exactly what is happening right now. With yields at under 3% for at least the last seven years, according to the chart, investors kept piling into bonds, thinking they could never lose out to inflation. Now that is starting to change, with the 10-year rate clicking up past 2.7%, reversing a 36-year trend.

“This is the largest technical change that many will probably see in their lifetime,” Financial Sense quoted Craig Johnson from investment bank Piper Jaffray. “Ultimately, we’re likely looking at the return of inflation and the need for inflation-related strategies coming out of this, which is where investors should be placing their attention.” Higher CPI numbers may force the Federal Reserve to pick up the pace of interest rate hikes this year - which are likely to affect the markets in a negative way.

The evidence shows that inflation is rising, faster than anyone expected. A Labor Department report on Wednesday revealed the consumer price index rose 0.5% from last month, higher than the anticipated 0.3%. The CPI increased 2.1% year on year in January, more than the 1.9% rise expected by economists, and the most since January 2014. One alarming statistic was a 1.7% monthly rise in apparel prices, which is the biggest jump since 1990.

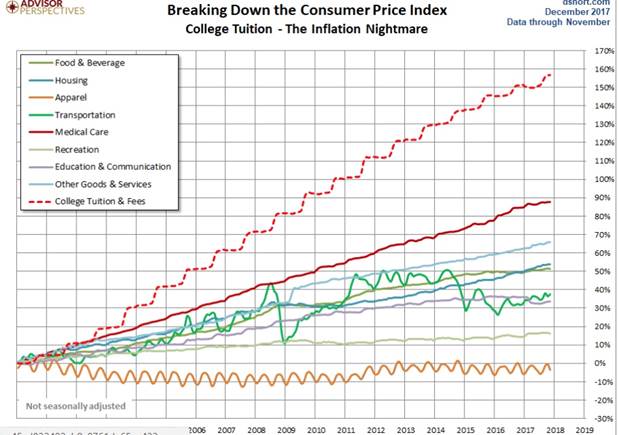

While CPI is up 43% since 2000, a seemingly modest annual increase over 18 years, a deeper dive shows that number is misleading. The biggest monthly expense for most Americans is their rent or mortgage payment, but the CPI doesn’t calculate housing expenses that way; rather it looks at a home via rental market value. If the CPI was broken down by real expenses, as in the chart below, it would show housing costs have risen by over 60% since 2000, medical care is up by more than 80%, and college tuition has increased by 160% over the past nearly two decades.

2.Weak US dollar

Commodities are priced in US dollars, so there is a strong correlation between the strength of the dollar and commodities. As the dollar barrelled along during the mining bear market 2012 to 2016, commodity prices slumped. Now the inverse is true, with the prices of copper, iron ore, gold and other metals rising partly due to USD weakness (supply and demand factors obviously play a huge role too).

That’s because countries that hold other, weaker currencies need to buy commodities using dollars, so when the dollar is strong, their ability to buy commodities goes down (it takes more units of their currency to buy one dollar), and therefore, commodity prices suffer.

Why has the dollar weakened? There are principally two reasons. The first is that the USD has dropped in relation to other competing currencies, such as the euro, the pound and the yen. For example better economic performance from the Eurozone, combined with the European Central Bank eyeing an end to its stimulus program, has pushed the euro from $1.06 a year ago to $1.24 on Thursday. The Bank of Japan recently trimmed its purchase of Japanese bonds by about $20B, with the yen also gaining against the dollar. One Japanese yen that a year ago was worth US$.0083, is now at $.00939.

The US dollar index, which tracks the dollar against six major global currencies, has dropped 13% over a year.

The second reason is inflation. Because, as proven above, we have rising inflation, the value of the dollar is diminished. For example if your wages rise 4%, but inflation is running at 6%, you actually lose 2% of your purchasing power, meaning it takes more dollars to pay your expenses.

There are other reasons too for a weaker US dollar. Last month I wrote about how the Chinese are threatening to stop buying US Treasuries, of which they hold $1.3 trillion, the most of any country. Just the suggestion this could happen spiked the 10-year Treasury yield, and sunk the value of the dollar. Uncertainty about US trade relationships - like pulling out of the Trans-Pacific Partnership and threats to quash NAFTA - have also weighed on the greenback.

This hasn’t been helped by recent comments from Treasury Secretary Steve Mnuchin, who said at the World Economic Forum in Davos that a weaker dollar helps the US economy. President Trump has gone back and forth on the issue, saying that he favors a strong dollar but also expressing concerns about the dollar being too strong. The inconsistency is understandable, because while a strong dollar reflects a robust US economy, a lower dollar is good for manufacturing and mining because it makes exports cheaper - both finished goods and raw materials - and imports more expensive.

3.Strong economic growth

The commodities complex is heavily dependent on economic growth to provide steady demand for everything from wheat and soybeans to copper and oil. During the commodities boom of the 2000s much of that demand came from China, the largest consumer of mined commodities, whose economy was growing at double digits. The fall in Chinese economic growth was a big factor in producing the bear market of 2012-16. But there are signs that growth is back, and with it, the mining supercycle that many thought was dead.

According to the World Bank global growth is expected to reach 3.1% this year, “after a much stronger-than-expected 2017, as the recovery in investment, manufacturing, and trade continues, and as commodity-exporting developing economies benefit from firming commodity prices.” The Bank added it’s the first year since the financial crisis that the global economy will operate at or near capacity. Emerging markets will see the lion’s share of growth, 4.5%, while advanced economies including the US, Japan and the EU will grow at 2.2%.

PwC is more bullish, predicting the global economy will add $5 trillion in output in 2018, with the US, emerging Asia and the Eurozone contributing almost 70% of economic growth this year. In the EU, the Netherlands will grow most at 2.5%. China is expected to grow between 6 and 7%. India, Ghana, Ethiopia and the Philippines will grow more than China, and eight of the 10 fastest-growing countries this year are likely to be in Africa, according to PwC.

What does this mean for commodities? PwC predicts 2018 to be the most energy-hungry year on record, double that of 1980, with China and India expected to consume a third of almost 600 quadrillion BTUs.

MINING.com recently reported that the LME index of base metals has climbed to the highest since 2014, with copper - a bellwether for economic growth - gaining two-thirds from its January lows.

In the same article two analysts from Goldman Sachs are quoted saying that “rising commodity prices will create a virtuous circle, improving the balance sheets of producers and lenders, and expanding credit in emerging markets that will, in turn, reinforce global economic growth.” “The environment for investing in commodities is the best since 2004-2008,” they wrote in a research note.

The New York-based investment bank is most bullish on copper, iron ore and metallurgical coal.

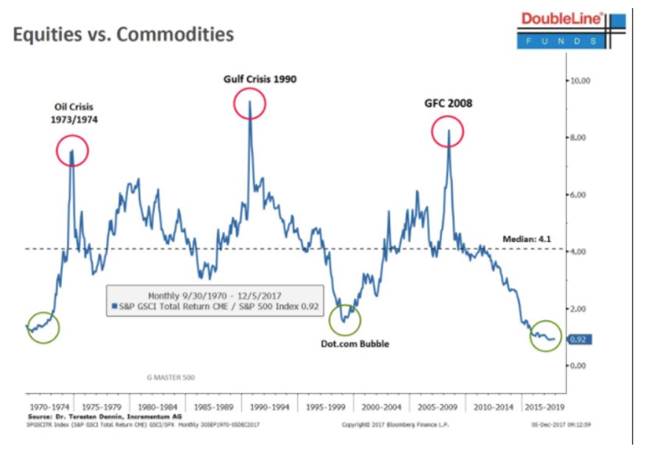

4.Commodities are undervalued

During the market bull of the last nine years, investors haven’t had to think too hard about where to plunk their money: everything has been going up, at least in US equities. Now that volatility has gripped the markets, it may be time to think about rebalancing the portfolio. According to funds manager Jeffrey Gundlach, now is as good a time as any, historically, to go into commodities - after many sold their metals and mining stocks during the bear market. Quotes CNBC:

“We’re right at that level where in the past you would have wanted commodities instead of stocks,” said Gundlach, noting that commodity prices stopped falling in 2016 and the global economy is “definitely hanging in there.”

Gundlach believes commodities are cheap relative to stocks - check out this chart which shows how undervalued commodities are right now compared to stocks.

And since commodities also act as a hedge against inflation (which could prove to be valuable over the coming years) investors should own a basket of different commodities.

5.Tight supply

When talking about commodity bull markets, it’s customary to talk about demand, but just as important this time around is supply. More specifically, how tight supply is in some of the key commodities markets. I can’t cover everything here, but two really demonstrate how tight supply over the next year or so is likely to boost the prices of these two key commodities: lithium and gold.

Lithium

Tesla’s Nevada Gigafactory will produce more lithium-ion batteries than were produced globally in all of 2013. CEO Elon Musk has already announced plans to build four more gigafactories. Lithium is the main ingredient in electric vehicle batteries.

By 2021, Chinese gigafactories will provide 3.5 times more gigawatt-hours of battery cells than Tesla’s current Gigafactory. Five new gigafactories will be built in Europe.

But there’s a problem: There isn’t enough lithium currently being mined to supply all those gigafactories.

In a previous article I calculated that between sales of electric cars in China, the UK and France, in 2016 there were 32.73 million electric vehicles all requiring lithium-ion battery packs, without counting electric buses which are going great guns in China and India. If each vehicle uses the same amount of lithium carbonate as Tesla’s Model S, that’s 3.273 billion pounds or 1.487 million tonnes of new lithium carbonate demand. Where will all the lithium be found? Clearly this is a market that is heading for a supply crunch.

Tesla recently suggested it doesn’t have enough lithium to supply batteries for its electric vehicles, grid storage and Powerwalls. So the luxury EV maker is looking to Chile, and is apparently in talks with the country’s biggest producer, SQM, about partnering in a processing plant. The irony was probably lost on Tesla that a lithium exploration boom is happening in the Clayton Valley in Nevada, not far from its Gigafactory, but that’s another story.

The price of lithium carbonate nearly tripled to over $20,000 a ton in10 months. Along with EVs, the storage market for intermittent wind and solar power is poised to become a major demand driver for lithium. Put demand and insecurity of supply together - there is only one operating lithium mine in the US, Albermarle’s Silver Peak, and its grade are falling - and the price of lithium can only go up further.

Gold

I’m sometimes reluctant to talk about gold as a commodity, since so much of the gold market is driven by investment, but there are some interesting things happening that makes this a very good time to consider an investment in gold or gold stocks.

Simply put, the world is running out of gold, especially the stuff that’s high grade and easy to find, and this makes me bullish on the precious metal - irrespective of all the familiar demand factors like safe haven, inflation hedge and store of value.

South African gold production has plummeted below 250 tonnes compared to 1,000 tonnes in the 1970s, and in China, the only country to increase production in recent years, it fell in 2017 by 9%.

This has many industry observers talking about “peak gold”. A Thomson Reuters report said 2016 was the first year since 2008 that gold mine output actually fell - by 22 tonnes or 3%. World Gold Council chair Randall Oliphant agreed that the world may already have produced the most gold in a year that it ever will. He predicted gold prices to move as high as $1,400 an ounce in 2018. “Production is likely to plateau at best, before slowly declining as demand rises…” Bloomberg quoted him saying in September.

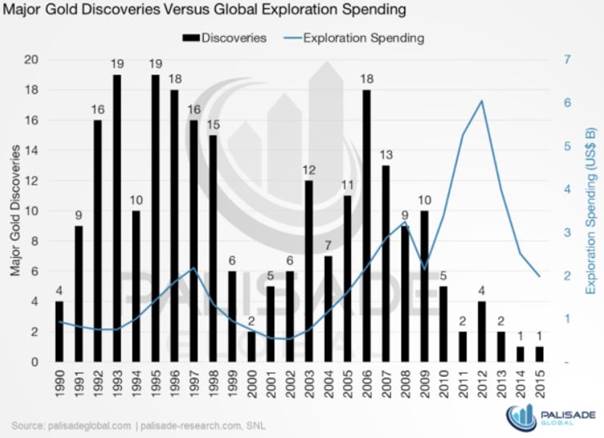

As for new gold mines, the bear market of 2012 to 2016 meant most large gold companies slashed exploration budgets and small explorers had an extremely tough time raising cash.

The experts agree the industry is seeing a significant slowdown in the number of large deposits being discovered. Funds manager Frank Holmes quotes Franco-Nevada cofounder Pierre Lassonde saying that he doesn’t know how we’ll replace the massive deposits found over the last 130 years.

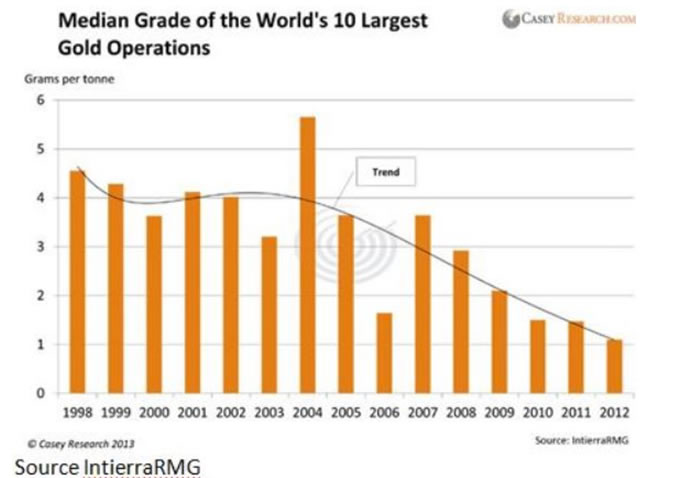

Grades have been declining for a while.

This all bodes well for junior miners, who will become acquisition targets of the majors who have slashed operating costs throughout the mining bear market, fired CEOs and sold key assets, trying to make up for disastrous deals made at the height of the mining supercycle.

Those same miners are now looking for good projects to buy, in order to avoid a drop in production. Bloomberg quotes Newmont Chief Economist Tom Brady saying that drop will be about 1 percent annually in coming years.

On Wednesday Barrick predicted an eighth straight decline in annual production, equating to 300,000 fewer ounces in 2018 than previously forecast. Barrick’s forecasted costs are also up.

“Higher cost guidance for 2018 primarily reflects lower anticipated gold production from Barrick Nevada, Pueblo Viejo and Veladero, increased processing of higher-cost inventory, and higher costs at Acacia,” the company said in a statement.

Thus with gold production falling everywhere, combined with a lack of large gold deposits that could move the market, you have the setup for a continued rise in the gold price - irrespective of what happens on the demand side.

Conclusion

The commodities complex tends to move in cycles with global expansions and recessions, and we have seen a contraction in commodities correspond with the bear market that occurred when global growth fell across the board. Over the past few years we have seen commodities suffer for another reason - the stock market bull that has investors plowing their money into other sectors like banking, tech and pharmaceuticals. Commodities seemed like a good sector to stay away from, with steep declines in metals prices and since 2014, crude oil.

However commodities are showing to be hot again, thanks to the factors I’ve outlined: the rise of inflation, the slump in the US dollar, the resurgence of global growth, undervalue, and tightening supply.

I’m very excited to be riding another commodities wave as it continues to gather momentum in 2018, and I’ll be watching closely for investment opportunities.

Commodities are the place to be in 2018. Are you in?

If not, maybe it should be.

By Richard (Rick) Mills

If you're interested in learning more about the junior resource and bio-med sectors please come and visit us at www.aheadoftheherd.com

Site membership is free. No credit card or personal information is asked for.

Richard is host of Aheadoftheherd.com and invests in the junior resource sector.

His articles have been published on over 400 websites, including: Wall Street Journal, Market Oracle, USAToday, National Post, Stockhouse, Lewrockwell, Pinnacledigest, Uranium Miner, Beforeitsnews, SeekingAlpha, MontrealGazette, Casey Research, 24hgold, Vancouver Sun, CBSnews, SilverBearCafe, Infomine, Huffington Post, Mineweb, 321Gold, Kitco, Gold-Eagle, The Gold/Energy Reports, Calgary Herald, Resource Investor, Mining.com, Forbes, FNArena, Uraniumseek, Financial Sense, Goldseek, Dallasnews, Vantagewire, Resourceclips and the Association of Mining Analysts.

Copyright © 2018 Richard (Rick) Mills - All Rights Reserved

Legal Notice / Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified; Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.