Romney Election Win Would End Quantitative Easing

ElectionOracle / US Presidential Election 2012 Oct 16, 2012 - 01:07 PM GMTBy: Gary_Dorsch

It’s been nearly eight years, since Fed chief Ben Bernanke told the Senate Banking Committee at his confirmation hearing, that “with respect to monetary policy, I will make continuity with the policies and policy strategies of the Greenspan Fed a top priority.” The former Princeton University professor who served as a Fed governor from August 2002 to June 2005 before accepting the post as President George W. Bush’s top economic adviser, also pledged, “I will be strictly independent of all political influences,” Bernanke said.

It’s been nearly eight years, since Fed chief Ben Bernanke told the Senate Banking Committee at his confirmation hearing, that “with respect to monetary policy, I will make continuity with the policies and policy strategies of the Greenspan Fed a top priority.” The former Princeton University professor who served as a Fed governor from August 2002 to June 2005 before accepting the post as President George W. Bush’s top economic adviser, also pledged, “I will be strictly independent of all political influences,” Bernanke said.

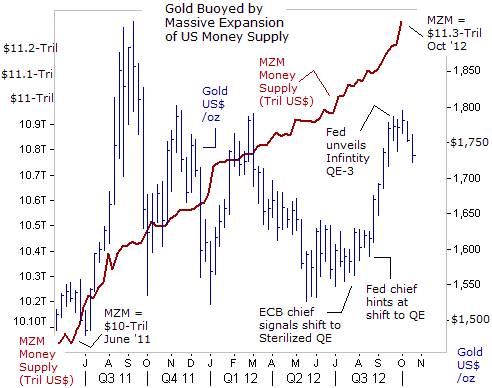

History will show that Bernanke did follow in the footsteps of his mentor for the first 3-½ years of his tenure. The infamous “Greenspan Put,” or the knee-jerk reaction by the Fed to rescue the stock market whenever risky bets went sour, - through massive injections of liquidity and reductions in interest rates, - was seamlessly replaced by the “Bernanke Put.” Since Bernanke gained control over the money spigots, the Fed continued to expand the MZM money supply by +65% to a record $11.3-trillion today. That’s an increase of about +9.4% per year, on average. The yellow metal never traded a nickel lower since Mr Bush tapped Bernanke to become the next Fed chief in Nov 2005, when the price of Gold was $468 /oz. Today, Gold is hovering around $1,735 /oz, up +370% for an annualized gain of +57%, - highlighting the most devastating blow to the purchasing power of the US-dollar of all-time.

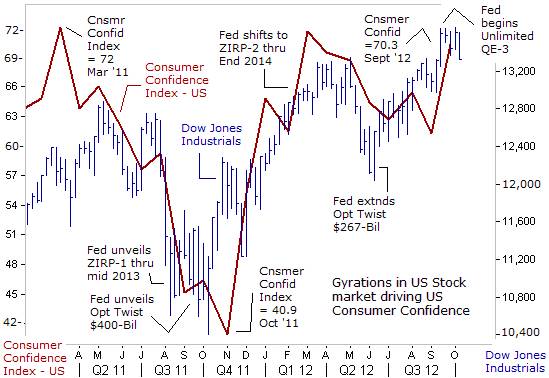

Following the stock market crash of 2008, Bernanke decided to take US-monetary policy down a very dangerous path that his predecessor had never explored. Bernanke experimented with the nuclear options of central banking, - unleashing powerful weapons for the first time in the US, such as “Quantitative Easing,” (QE), the Zero Interest Rate Policy (ZIRP), and “Operation Twist.” These weapons were forcefully deployed in order to artificially re-inflate the value of the US-stock market, and in turn, help to boost President Barack Obama’s chances at winning re-election. Bernanke borrowed the blueprints of the Bank of Japan, - the original pioneer in QE and ZIRP, dating back to March of 2001. The Fed was able to engineer a doubling of the S&P-500’s market value in just three-years, for a gain of $7-trillion, from the bottom of the brutal Bear market that came to a merciful end in March of 2009.

However, the Fed chief broke his promise to stay above the political fray, when on Sept 13th, Bernanke and his band of super doves, decided to unleash “Infinity QE-3” or the unlimited printing of money, at an initial rate of $40-billion per month, with less than eight weeks left in the race for the White House. The Fed crossed the line by brazenly supporting the President in his bid for re-election. By jolting the stock market higher, Fed aimed to conjure-up the illusion among the general public of an economic recovery looming on the horizon that would in the short-term, boost consumer confidence, and the opinion polls for Barack Obama.

One-year ago, the Conference Board’s consumer confidence index, had sunk to as low as 40.9, following a sudden crash in the Dow Jones Industrials. Shortly afterwards, Mr Obama’s approval rating plunged to the lowest of his presidency, at 42%. However, the Fed engineered a quick recovery of the market’s losses, by utilizing ZIRP and Operation Twist, combined with covert intervention in the stock index futures markets. As the Fed guided the Dow Industrials higher, above the 13,250-level, Obama’s approval rating also rebounded to 49%.

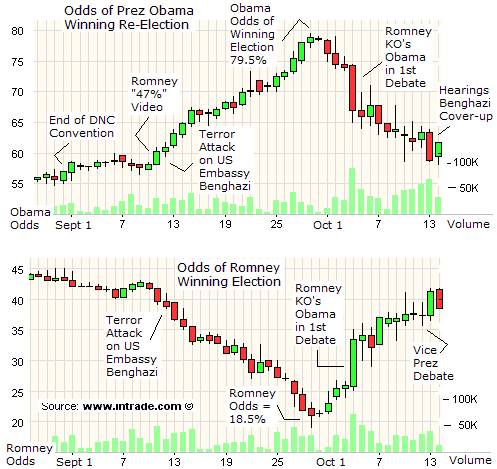

Hedge fund trader Jim Rogers cried foul in an interview with CNBC on Sept 12th, “The +30% gains since last October have been largely driven by one catalyst, - the Fed. It’s pumping huge amounts of money into the market. This is a Fed rally. The money has to go somewhere and it’s going into the stock market and the commodity market. Those who timed the market right will do well, but most won’t. It’s going to end terribly,” Rogers said. However, with the Dow climbing to a five-year high, - traders at Intrade.com also lifted the odds of Obama winning a second term to as high as 78% on Sept 29th.

“Strip out monetary support and the Dow Jones Industrials would likely fall more than 4,000 points, if corporate and economic fundamentals truly reflected share prices, said billionaire real-estate magnate Sam Zell on October 2nd. Monetizing government debt and pegging interest rates at near zero-percent for several years are experiments in market socialism, and not “free market” capitalism. The longer the Fed fails to let market forces determine interest rates, the more the Fed creates inflationary pressures. Oil prices go up, food prices go up and the average American doesn’t see wage increases. That means there is less disposable income for consumers and will eventually it would lead to another economic recession.

The Fed’s QE policy revolves around the “trickle down” theory, - or the idea that “higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. In turn, increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.” However, it hasn’t quite workout that way. US-listed companies are sitting on $2-trillion in cash and would rather spend most of the hoard on stock buybacks, higher dividend payouts, mergers and acquisitions of competitors, and the like, all of which creates no jobs whatsoever and, in many cases, will leads to fewer jobs. Furthermore, there isn’t an equitable distribution of wealth in the stock market, where 82% of the outstanding shares are owned by just 10% of the richest Americans.

Bernanke has publicly committed the Fed to a zero-interest rate policy through the end of 2015. Traders in the US-markets have been under the spell of the Fed’s radical monetary schemes for so long, that they believe the “Bernanke Put” can endlessly keep equity prices afloat, even if the US-economy that’s sliding into a recession. Banks can borrow from the Fed at less than 0.25% - essentially free money, and lend the funds to speculators like hedge funds, private equity firms, and others. The speculators then channel the money into the US-equity markets, but also into crude oil futures and precious metals.

The hallucinogenic world of QE, and ZIRP, and Operation Twist has become the new normal in the markets. Nobody knows how long the Fed’s latest scheme – “Infinity QE-3” will last, but already some analysts are predicting the Fed might end-up increasing the MZM money supply by at least $1-trillion in the next few years. This premise is built upon the assumption that President Obama would win a second term, and therefore, allow the addicted money printers at the Bernanke Fed to continue with their radical schemes. Under this scenario, - many investors have turned to the precious metals, Gold and Silver as a hedge that can protect their purchasing power, while the Fed is whittling away at the US-dollar.

Most analysts agree that the long-term trend for Gold is Bullish, and that it’s only a matter of time until the yellow metal will eclipse its record high of $1,925 /oz, reached in August of 2011. The price of Gold is ultimately buoyed by the expansion of the money supply. Since the Fed began its efforts to pump-up the stock market from its lows of July and August 2011, the size of the MZM money supply has increased by $1.3-trillion. Meanwhile, the price of Gold has been gyrating sideways, between support at $1,500 and resistance at $1,800 /oz.

Currency War, Fed versus the Bank of Japan – friendly fire

Flooding the world’s money markets with an endless stream of greenbacks is also designed to weaken the value of the US-dollar against other major foreign currencies. However, other central banks are fighting back, especially the Bank of Japan (BoJ), which does not want to see the US-dollar fall below ¥75 in the currency markets. Japan’s “Lost Decade” of economic growth has stretched into a “Lost Generation,” amid tougher competition for Japan Inc in foreign markets from the likes of Apple and Samsung Electronics, an aging and spend-thrift population at home, and most of all, exporters are suffering from a super strong yen with the rest of the world. Growth in Japan throughout the 1990’s averaged +1.5% that was slower than growth in other major developed economies, giving rise to the term “Lost Decade.” During the 20-years thru 2011, Japan's average quarterly GDP Growth was even slower, expanding at an anemic +0.50% clip, giving rise to the term “Lost Generation.”

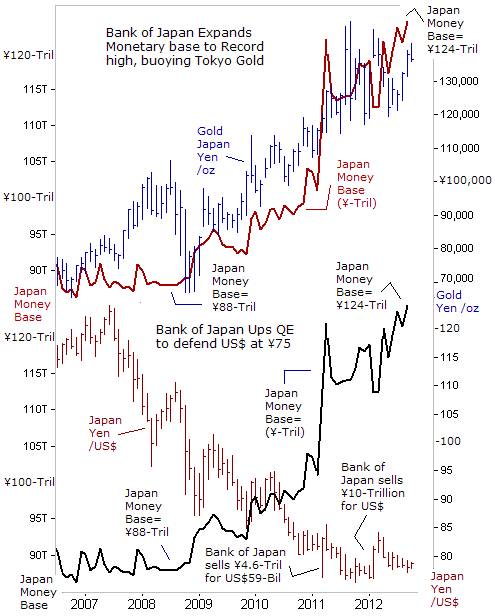

Starting in November 2011, Tokyo secretly began to manage a “dirty float” for the dollar /yen exchange rate. The BoJ dumped ¥10-trillion yen into the currency market, and bought $133-billion, as it tried desperately to stem the US-dollar’s slide at ¥75. The US Treasury was happy to give the green light for Japan’s massive intervention in the currency markets, since the US-dollars that are acquired in the operation are usually recycled into US Treasury notes, helping to keep US-bond yields low. Japan is now the third largest holder of US T-notes, with $1.1-trillion, up from $983-billion a year ago.

However, intervention alone in the currency markets is not sufficient enough for the BoJ to defend the US-dollar at ¥75, when the Fed churning out dollars with Infinity QE-3. As such, the BoJ boosted its own QE-scheme, by adding an extra ¥10-trillion ($127-billion) to its bazooka, with the increase earmarked for purchases of government bonds and treasury discount bills. Equipped with ¥80-trillion yen, ($1-trillion), the total amount allotted for QE is now equivalent to nearly a fifth of Japan’s economic output.

In other words, the Fed and the Bank of Japan are involved in a currency war, with each side printing local currency, and purchasing domestic bonds. Otherwise known as “financial repression,” the central banks exert totalitarian control over credit and can finance the Treasury at ultra-low rates in spite of a mushrooming national debt. To counter the increase in the Fed’s MZM money supply, the BoJ has increased Japan’s monetary base, which hit a record high of ¥124-trillion last month. Benefitting from the friendly fire between the world’s two most powerful central banks is the Tokyo Gold market, which is priced at just under ¥140,000 /oz, and double its market value versus six years ago. For Japanese investors, - Tokyo Gold has been one of the few stellar areas in a dismal local market.

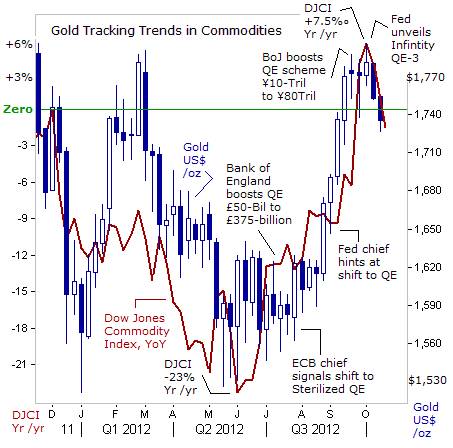

The BoJ and the Fed have also been joined by the Bank of England in printing vast quantities of money and in turn, fueling the fire in the Gold market. Other G-20 central banks in Brazil, China, and Korea are either injecting huge volumes of liquidity or cutting interest rates, thus improving the landscape for the Gold market. Yet despite these bullish drivers, it hasn’t been a straight line upward for the yellow metal. There are always zig-zags along the way. After soaring more than $200 /oz since late July, Gold is found stiff resistance at the psychological $1,800 level, befoee slumping to $1,735 /oz today. The reason for the drop is is a pullback in the broader commodity indexes, led by a slumping agricultural sector, and weaker US light crude oil and industrial metals. The year-over year change in the Dow Jones Commodity index (DJCI) turned slightly negative, at -2% compared with a year ago, after peaking at +7.5% on October 4th. That’s a real-time signal that global inflationary pressures are abating, even as many of the G-20 central banks are engaging in QE or lowering interest rates.

Commodity prices could be held in check if the global economy continues to weaken substantially. On October 9th, the IMF warned that the global economy is slowing down and if European and US-policymakers that failure to fix their economic ills it would prolong the slump. The IMF predicting the global economy would grow at a +3.3% rate in 2012, as Europe and Japan’s economies sink into outright recession and China’s factory output growth slows to its weakest in 3-years, underlining stiff global headwinds. As a general rule of thumb, for every -1% drop in China’s growth rate it leads to a -1.5% decline in industrial commodity prices over a few quarters, threatening exporters in Australia, Brazil, Canada, Chile, and Russia. China alone buys 65% of the global demand for seaborne iron ore, 40% of the copper supply, and 1/3 of exports of natural rubber, sold by Malaysia, Indonesia and Thailand.

Yet the biggest wildcard that could rock the Gold market, and by extension, the world’s stock markets, is the outcome of the upcoming Nov 6th elections. The odds of Romney winning have been resurrected from the dead, since the October 3rd debate, rebounding from as low as 18.5% on Sept 29th, to 38.5% today. The likelihood of an upset victory by Mitt Romney still seems far fetched by on-line bettors. However, Gold’s recent $60 /oz slide to the $1,735 /oz area might be partly explained by the rising possibility of a Romney victory on Nov 6th.

An upset victory by Romney could be Bearish for the price of Gold, because it could spell the earlier than expected end of QE-3 in the US-money markets. In an August 23rd interview with FOX Business Network, Romney said he would not reappoint Fed chief Bernanke when his term expires in 2014. “I would select a new person to that chairman position, someone who shares my economic views, and is sympathetic to the needs of our nation. I want to make sure that the Federal Reserve focuses on maintaining the monetary stability that leads to a strong dollar, and confidence that America is not going to go down the road that other nations have gone down to their peril. I don’t think QE-2 was terribly effective. I think a QE-3 and other Fed stimulus is not going to help this economy. I think that is the wrong way to go. I think it also seeds the potential for inflation down the road that would be harmful to the value of the dollar and harmful to the stability of our nation’s needs.”

The Federal Reserve has become the “fourth branch of government,” because of how much power it wields in the marketplace. The Fed sets interest rates and depresses bond yields, it determines the size of the money supply, regulates and secretly bails out Oligarchic banks, and determines “target rates” for unemployment and inflation. Every small move the Fed makes causes global financial markets to swing wildly. However, if Ryan become VP, he’s expected to push for forensic audits of the Fed’s secret monetary policy operations and its covert intervention in stock index futures. Equally important, a Romney-Ryan victory could lead to the early departure of Bernanke from the Fed, as early as February of 2013.

In a detailed speech on monetary policy in December 2010, Ryan hardly minced words in his criticism of the Bernanke Fed. “There is nothing more insidious that a government can do to its countrymen than to debase its currency, yet this is in fact what is occurring,” Ryan said at Freedom Works, a right-wing think tank. Such strongly worded criticism is viewed as an effort to stop the Fed’s radical QE schemes in its tracks. Ryan wants the Fed to adopt sound money policies - in keeping with the free-market, limited-government stance that has marked his signature budget plan and made him a favorite of Tea Party conservatives.

The idea that “Infinity QE-3,” could be aborted as soon as February of next year, should Romney win the race for the White House, is currently viewed as a long shot. It’s a contrarian call, with most Wall Street banks betting on further QE gains in the stock market. So a Romney win would catch the majority of traders off guard, and deal a tremendous jolt to the world’s financial markets. It would knock the precious metals lower and badly rattle the US-stock market indexes, while boosting the value of the US-dollar in the foreign exchange markets. The chance of a Republican led White House is increasing.

According to a USA TODAY/Gallup Poll posted on October 15th, “Mitt Romney leads President Obama by 4-points among likely voters in the nation’s top battlegrounds. As the presidential campaign heads into its final weeks, the survey of voters in 12 crucial swing states finds female voters are increasingly concerned about the deficit and debt issues that favor Romney. The Republican nominee now ties the president among women who are likely voters, 48%-48%, while he leads by 12-points among men. The White House also finds itself at the center of a mounting storm over a possible cover-up of the terrorist assault on the US embassy in Libya, with potentially disastrous consequences for Mr Obama’s re-election prospects. If correct, Romney could be on his way to winning the presidency, - and as a result, traders should brace for the premature death of Infinity QE-3.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2012 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.