Stock Market Boosted by Better than Expected Corporate Earnings

Stock-Markets / Financial Markets 2009 Oct 18, 2009 - 03:41 PM GMT

Risky assets remained in favor during the past week, generally helped along by fairly robust economic data and better-than-expected corporate earnings reports. A number of bourses, crude oil, inflation-linked bonds and high-yielding corporate bonds and currencies recorded fresh highs for the year, whereas gold hit an all-time high of $1,070.20 per ounce.

Risky assets remained in favor during the past week, generally helped along by fairly robust economic data and better-than-expected corporate earnings reports. A number of bourses, crude oil, inflation-linked bonds and high-yielding corporate bonds and currencies recorded fresh highs for the year, whereas gold hit an all-time high of $1,070.20 per ounce.

Assets such as government bonds and the US dollar saw fading demand as safe havens, now that the global economy is on the mend. Similarly, credit default spreads tightened markedly and the CBOE Volatility Index (VIX) declined to its lowest level since early September 2008.

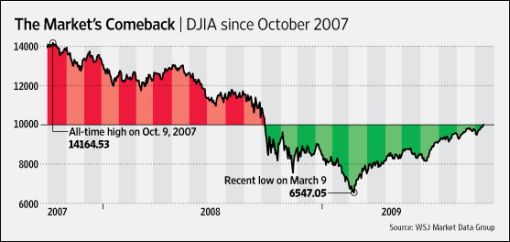

The Dow Jones Industrial Index passed a psychological milestone this week as the Index broke above the 10,000 level for the first time in a year, although it then declined again to fall shy of the roundophobia number by four basis points by the closing bell. The Dow first broke above 10,000 more than ten years ago in 1999 and has since done so on 26 occasions. Yes, a ten-year buy-and-hold index investor has had no capital gain over the period!

Source: The Wall Street Journal, October 16, 2009.

Meanwhile, according to the Financial Times, a survey of 44 leading economists by the National Association of Business Economics (NABE) showed the jobs that were lost during the Great Recession are not expected to return before 2012, while anemic wage growth of only 1% this year and 2.2% next year is forecast - the slowest two-year period on record. “But the way that investors are almost relying on unemployment to stay high [and central banks not to start exiting from the exceptionally low interest rates any time soon] demonstrates that the recovery, in markets and the economy, remains on shaky foundations,” warned FT’s investment editor, John Authers.

Source: Walt Handelsman, October 14, 2009.

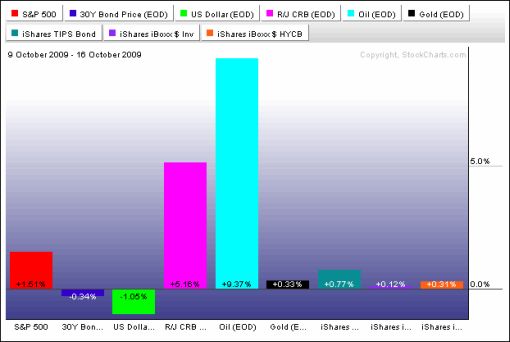

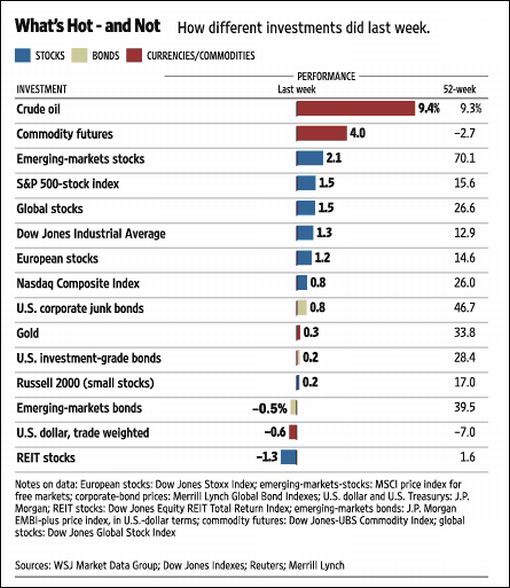

The past week’s performance of the major asset classes is summarized by the chart below - a set of numbers that indicates an increase in risk appetite.

Source: StockCharts.com

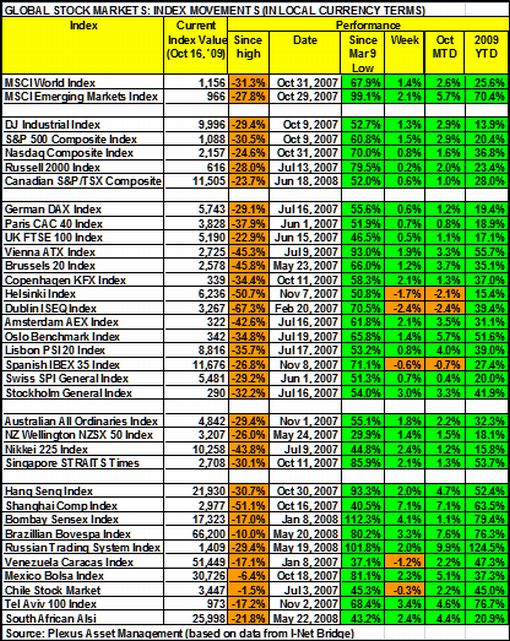

A summary of the movements of major global stock markets for the past week, as well as various other measurement periods, is given in the table below.

The MSCI World Index (+1.4%) and MSCI Emerging Markets Index (+2.1%) both made headway last week to take the year-to-date gains to +25.6% and an impressive +70.4% respectively. Interestingly, Chile is now only 1.5% down from its July 2007 highs and could be one of the first markets to wipe out all the financial crisis losses.

Notwithstanding a down-day on Friday, US indices closed higher for the week. The year-to-date gains remain firmly in positive territory and are as follows: Dow Jones Industrial Index +13.9%, S&P 500 Index +20.4%, Nasdaq Composite Index +36.8% and Russell 2000 Index +23.4%.

Click here or on the table below for a larger image.

Top performers among stock markets this week were Sudan (+22.6%), Kazakhstan (+8.9%), Cyprus (+7.6%), Egypt (+6.0%) and Hungary (+5.5%). At the bottom end of the performance rankings countries included Nigeria (‑4.2%), Thailand (-4.0%), Qatar (-3.2%), Bahrain (-2.8%) and Ireland (‑2.4%).

Of the 99 stock markets I keep on my radar screen, 76% recorded gains, 21% showed losses and 2% remained unchanged. (Click here to access a complete list of global stock market movements, as supplied by Emerginvest.)

John Nyaradi (Wall Street Sector Selector) reports that, as far as exchange-traded funds (ETFs) are concerned, the winners for the week included United States Gasoline (UGA) (+11.1%), United States Oil (USO) (+8.9%), PowerShares DB Energy (DBE) (+8.8%) and iShares S&P GSCI Commodity (GSG) (+7.4%).

On the losing side of the slate, ETFs included iShares MSCI Thailand (THD) (-6.0%), Market Vectors Solar Energy (KWT) (-2.8%), Claymore/MAC Global Solar Energy (TAN) (-2.6%) and ProShares Short MSCI Emerging Markets (EUM) (-2.5%).

Referring to the declining US dollar, the quote du jour this week comes from 85-year-old Richard Russell, author of the Dow Theory Letters. He said: “Now I’ll let you in on an awful secret. The US, despite all its BS talk, really wants a lower dollar. The fact is that the US is doing absolutely nothing to defend the dollar. Of course, if the Fed wanted to defend the dollar they could halt their mass printing of dollars, and they could raise interest rates. And Bernanke could win the 800 meter race at the next Olympics at Rio.

“But let’s be rational - how in God’s name is the US going to pay off trillions in debt? By raising taxes? Impossible. They could renege on the debt like Argentina - unthinkable. But there is a way - they’ll try to minimize the importance of the debt with a cheaper, devalued dollar. That’s the time-honored US way, but loyal Americans don’t believe it. If they did, gold would be selling at $4,000 an ounce.”

Russell added: “It’s all so smarmy, but c’mon, what do you think the Fed has been doing since World War II? It’s been systematically inflating. They can’t fool me, I was around after the War, and I remember prices in 1945. Maybe the chief culprit was Alan Greenspan, but Bernanke is carrying on. There’s a lot of inflating coming up. ‘Strong dollar policy.’ Bite your tongue, and give me a break.”

Other news is that the Federal Deposit Insurance Corporation (FDIC) closed another bank on Friday, bringing the tally of US bank failures in 2009 to 99 (124 since the beginning of the recession). Meanwhile, CreditSights, which tracks the dismal data, predicts (via MarketWatch) that we could be no more than 10% of the way through this cycle of bank collapses, which is sure to be the worst run of closures since the Great Depression.

Next, a quick textual analysis of my week’s reading. Although “bank” still features prominently, the key words have started taking on a more normal pattern compared with the crisis-related words that have dominated the tag cloud for many months. “Recovery” is also gaining in prominence.

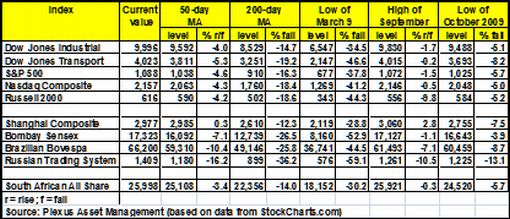

The major moving-average levels for the benchmark US indices, the BRIC countries and South Africa (where I am based) are given in the table below. With the exception of the Shanghai Composite Index, which is trading marginally below its 50-day moving average, all the indices are above their respective 50- and 200-day moving averages. The 50-day lines are also above the 200-day lines in all instances.

The US indices are creeping closer to the so-called 50% retracement levels (i.e. regaining half the loss suffered between the October 2007 highs and March 2009 lows). The levels are: 10,346 for the Dow Jones Industrial Index and 1,121 for the S&P 500 Index.

The September highs and October lows are also given in the table as these levels could define a support area for a number of the indices.

Click here or on the table below for a larger image.

“We regularly note that the earnings reporting season often marks the end of the market trend into earnings announcements. The reversal tends to occur during the second week [last week] of reporting. Given this is expiration week, which often creates a short-term peak on the usual manipulation, the odds favor a short-term stock market peak late this week or next week. Of course any unexpected ugly news, like negative revenue, earnings or guidance from several key companies could commence a stock downdraft,” said Bill King (The King Report).

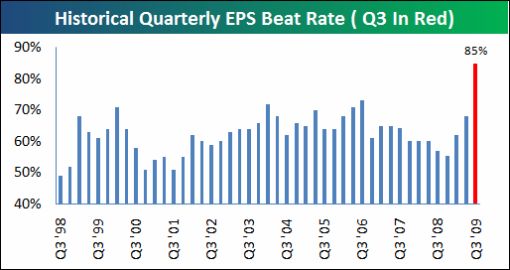

Talking of earnings, the third-quarter earnings season has progressed on an upbeat note since Alcoa’s results announcement on October 7 marked the onset of the reporting cycle. It is still early days in this period, but 85% of US companies have so far beaten earnings estimates. According to Bespoke, the current beat rate is well above any other quarter since at least 1998. ”Even with analysts raising estimates significantly leading up to the earnings season, companies have still managed to come in better than expected so far,” they said.

Source: Bespoke, October 16, 2009.

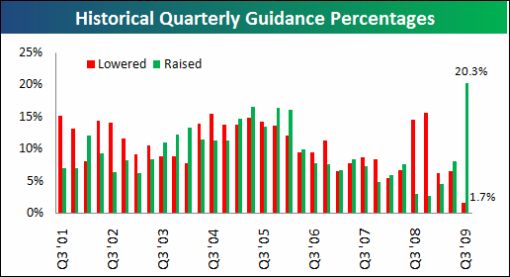

Additionally, Bespoke also highlighted that while the earnings per share numbers grab the headlines, it is what companies say about future quarters that impacts equity prices most on their reporting days. As shown in the graph below, 20.3% of US companies have raised guidance so far this earnings season. Bespoke’s report said: “The highest reading for this number has barely broken 15% in any prior quarter this decade. And if we compare the percentage of companies raising guidance versus the percentage of companies lowering guidance, no other quarters come even close to this one. It will be hard to keep this up as the earnings season progresses, but it’s also shaping up to be a record-breaking quarter on the positive side.”

Source: Bespoke, October 16, 2009.

Importantly, one needs to assess what is priced in by the stock market. Useful research comes from David Rosenberg, chief economist and strategist of Gluskin Sheff & Associates, who said: “We re-ran our regressions with the latest tightening in spreads and breakout in equity valuation and found that US investment grade credit is now priced for 2.5% GDP growth in the coming year (was 2.0% two months ago) and the S&P 500 is now de facto pricing in 4.8%, which, by the way, is now basis points shy of what it was discounting in the summer/fall of 2007. And, backing out the fair-value P/E from the corporate bond market, and yields have been backing up sizably in recent weeks, we can see that the S&P 500 is now pricing in $85 of operating earnings, which we think will be, at best, a 2013 story. In other words, the rally continues to move further away from the fundamentals.”

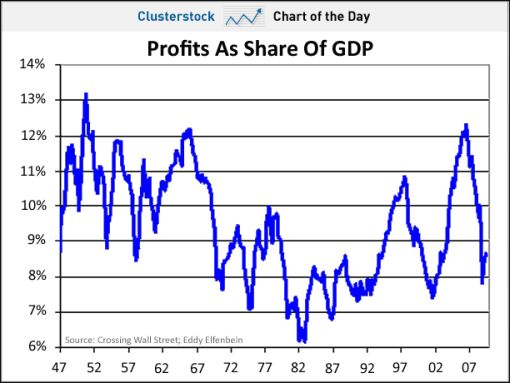

However, Rosenberg’s bearish prognostications are not universally accepted. In a rebuttal (via Clusterstock), Eddy Elfenbein created the chart below of profits as a share of GDP. “They’re clearly compressed, and if they revert to a historical standard, it means earnings have some spring in them,” said the report.

Source: Clusterstock - Business Insider, October 9, 2009.

Jeremy Grantham, who has just announced his retirement as chairman of GMO, put matters into perspective in a Kiplinger article, saying: “The recent rally has been very speculative, favoring risky assets over the past few months. I’m sorry if you missed investing at the market’s March lows, but don’t compound the damage to your portfolio by chasing gains in risky assets. We’re at the beginning of a seven-year period of lean returns. You should only be buying the highest-quality blue-chip companies, where valuations are most attractive.”

As stated before, share prices have moved too far ahead of economic reality. This calls for a cautious approach in anticipation of the market working off its overbought condition and fundamentals reasserting themselves. I will bide my time while the fundamentals play catch-up.

Economy

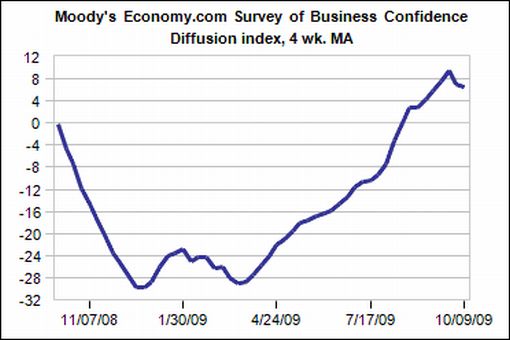

“After improving steadily this past summer, global business sentiment has remained largely unchanged so far this fall, consistent with a global economy that is experiencing a tentative economic recovery. The recession is over but the nascent recovery is not quickly gaining traction,” according to the results of the latest Survey of Business Confidence of the World by Moody’s Economy.com. “Businesses remain more upbeat about the outlook into next year and broader economic conditions, and dourer when considering the strength of their sales and intentions to hire. South Americans are the most positive and North Americans generally the most negative.”

Source: Moody’s Economy.com

As far as hard data are concerned, China’s economy gained new impetus, according to US Global Investors. “Passenger car sales in September rose 84% year on year to 1.02 million units. Housing starts jumped 56% in September from a year earlier, the fastest pace of growth in at least five years.

“China’s exports declined 15.2% year on year in September, the smallest contraction in nine months, while imports dropped only 3.5% year on year as the domestic economy continued to recover. Exports rose 7.7% on a month-on-month basis, adjusted for seasonality.” The stronger export performance follows a similar trend in South Korea, Taiwan and Vietnam.

“Singapore, which led Asia into recession, on Monday pointed the way to further regional recovery with strong third-quarter economic growth … The Monetary Authority of Singapore (MAS) said GDP expanded 14.9% on a seasonally adjusted quarter-on-quarter annualized basis in the June to September period, after a comparable revised increase of 22% the previous quarter,” reported the Financial Times.

Further good news on the global economic front came from Eurozone industrial production that expanded for the fourth month in a row in August. Output rose by 0.9% from July, when it increased by a revised 0.2%.

A snapshot of the week’s US economic reports is provided below. (Click on the dates to see Northern Trust’s assessment of the various data releases.)

Friday, October 16

• Widespread strength in factory report

Thursday, October 15

• Inflation remains a non-issue, for now

• The quandary between initial claims and total continuing claims

Wednesday, October 14

• Minutes of September 22-23 FOMC meeting - more of the same

• Q3 consumer spending expected jump likely, but muted growth in Q4

• Import prices are turning around

• Restocking - one of the conduits of economic growth in the months ahead

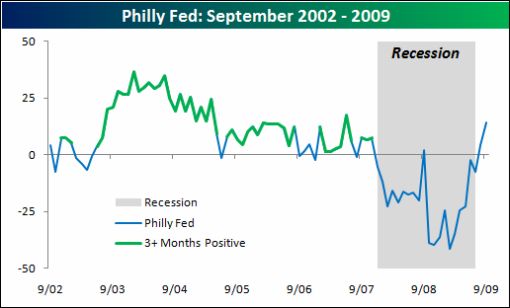

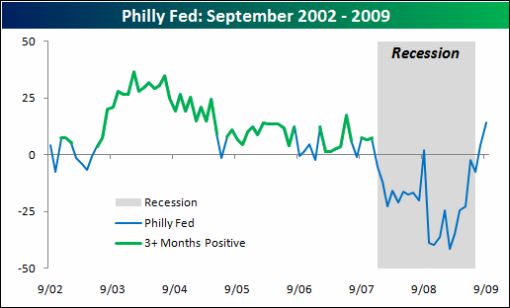

Further evidence that the recession that began in December 2007 has ended, came from the Philly Fed report that was positive for the third straight month. According to Bespoke, “the last time this indicator was positive for three straight months was from September through November 2007, which was the last three months leading up to the start of the recession”.

Source: Bespoke, October 15, 2009.

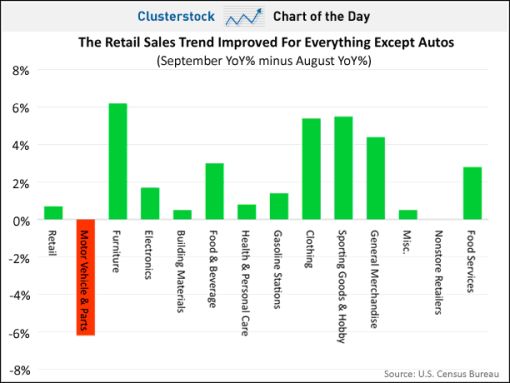

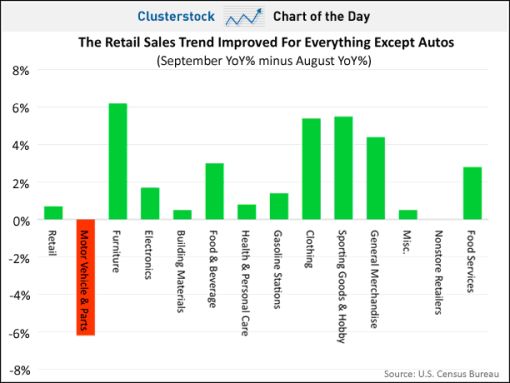

Dissecting the retail sales data shows that trends improved all over, with the exception of auto-related sales due to “Cash for Clunkers”. The chart below, courtesy of Clusterstock takes September’s year-on-year sales change (Sep 09 versus Sep 08) and subtracts August’s year-on-year sales change (Aug 09 versus Aug 08). It thus shows the change in the retail sales trend. “Yes, this matters: American retail trends have to become less negative before they go positive,” said the report.

Source: Clusterstock - Business Insider, October 14, 2009.

The minutes of the Federal Open Market Committee’s (FOMC) September meeting indicated that most participants thought the recession was over. Although they expected the recovery to be weak initially, most members also upgraded their expectation for near-term growth.

Participants generally expected inflation to remain low in the near term. “The Fed is in the most favorable spot in the near term with regard to inflation because the excess capacity in the economy allows the Fed to maintain a focus on economic growth and leave inflation on the back burner, for now,” said Asha Bangalore (Northern Trust).

Cautioning against bullish expectations, David Rosenberg said (via MoneyNews) that the economy was being held together by very strong tape and glue provided by the Fed, Treasury, and Congress, and that the recovery would be weak.

He predicted the economy would stagnate this quarter and then grow no more than 2% in 2010. The economy won’t take on the “V” shape of previous rebounds, Rosenberg said. “It’s going to look like this whole string of lowercase Ws for the next five years.”

US economic data reports for the week include the following:

Tuesday, October 20

• Building permits

• Housing starts

• PPI

Wednesday, October 21

• Fed’s Beige Book

Thursday, October 22

• Initial jobless claims

• Leading economic indicators

• FHFA Housing Price index

Friday, October 23

• Existing home sales

Markets

The performance chart obtained from the Wall Street Journal Online shows how different global financial markets performed during the past week.

Source: Wall Street Journal Online, October 16, 2009.

“The emotional brain responds to an event more quickly than the thinking brain,” said Daniel Goleman, author of Emotional Intelligence and Primal Leadership. Let’s hope the news items and quotes from market commentators included in the “Words from the Wise” review will assist the thinking brains of readers of Investment Postcards and take the emotion out of their investment decisions.

Click here for more thought-provoking items and quotes.

That’s the way it looks from Cape Town (where we are blessed with balmy spring weather at the moment).

Did you enjoy this post? If so, click here to subscribe to updates to Investment Postcards from Cape Town by e-mail. (For short comments - maximum 140 characters - on topical economic and market issues, web links and graphs, you can also follow me on Twitter by clicking here.)

Source: Tom Toles, October 16, 2009.

Financial Times: Nobel economics prize for governance duo

“Elinor Ostrom and Oliver Williamson shared the 2009 Nobel Prize for economics of Monday for their work on how economic transactions operate outside markets in common spaces and within companies. Martin Wolf, chief economics commentator, explains the value of the surprise winners’ research.”

Click here for the full article.

Source: Financial Times, October 12, 2009.

Asha Bangalore (Northern Trust): Minutes of September FOMC meeting - more of the same

“The minutes of the September 22-23 FOMC meeting contain the typical pros and cons of Fed policy, with nothing standing out. The willingness of some members to enlarge the size of the mortgage-backed securities purchase plan could be raised to ‘reduce economic slack more quickly than in the baseline outlook’. At the same time, another member held the opinion that improvements underway implied a reduction of these purchases. The importance of ‘flexibility’ to expand purchases of assets in the event of a deterioration of economic conditions was noted.

“The FOMC’s views about inflation are noteworthy. The majority of the FOMC views the inflation outlook during the next few quarters as roughly balanced. There were those belonging to the significant disinflation camp, but they had lowered the probability of this occurrence in the intermeeting period. In the longer term, a few were reported to see ‘risks tilted to the upside’. Inflation expectations have been stable and allow the Fed to watch and wait and focus on economic growth.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 14, 2009.

CNN Money: Foreclosures - worst three months of all time

“Despite concerted government-led and lender-supported efforts to prevent foreclosures, the number of filings hit a record high in the third quarter, according to a report issued Thursday.

“‘They were the worst three months of all time,’ said Rick Sharga, spokesman for RealtyTrac, an online marketer of foreclosed homes.

“During that time, 937,840 homes received a foreclosure letter - whether a default notice, auction notice or bank repossession, the RealtyTrac report said. That means one in every 136 US homes were in foreclosure, which is a 5% increase from the second quarter and a 23% jump over the third quarter of 2008.

“Nevada continued to be the worst-hit state with one filing for every 23 households. But even tranquil Vermont, where the foreclosure crisis has barely brushed the housing market, saw foreclosure filings jump nearly 170% compared with the third quarter of 2008. Still, that resulted in just one filing for every 5,023 households in the state - the best record in the country.

“The RealtyTrac report also unveiled the results for September, and it found that there was slight relief from foreclosure filings. Last month, notices totaled 343,638, down 4% compared with August. Unfortunately, that total accounts for 87,821 homes that were repossessed by lenders.

“That deluge contributed significantly to the quarter’s record 237,052 repossessions, a 21% jump from the previous three months. So far this year lenders have taken back 623,852 homes.’

“The foreclosure crisis may not diminish anytime soon. ‘The fastest growing area is in the 180 days late-plus category, the most seriously delinquent borrowers,’ Sharga said. ‘It’s going to be a lingering problem.’”

Source: Les Christie, CNN Money, October 15, 2009.

Financial Times: Slow US recovery blamed on low demand

“Weak demand from battered consumers will be a ‘major constraint’ on the US economy for the foreseeable future, a key White House adviser said on Monday, as the administration mulls over further ways to spur demand and create jobs.

“Lawrence Summers, the director of the National Economic Council, has been banging the drum for the $787 billion stimulus package in the face of Republican criticism that it is not creating the jobs it promised.

“With political pressure building as unemployment nears 10%, the administration is looking for additional ways to mitigate the problem, though it insists there will be no ’second stimulus’.

“‘It is not for me … to preview policies that President Obama will announce in coming weeks,’ said Mr Summers in a speech to an economics conference on Monday. But he said that while the economy had improved substantially, people had to recognise that demand was hobbled and US consumers and exports should be supported.

“‘We need to recognise that lack of demand will be a major constraint on output and employment in the American economy for the foreseeable future,’ he said at the National Association for Business Economics conference. ‘Direct public investment has a crucial role at a time like this.’

“His speech was made as a survey of 44 leading economists by the NABE showed many were worried about the effects of unemployment and the budget deficit on the US economy.

“Four in every five said that the worst recession since the 1930s was over. But while they expected the stock market and corporate profits to rise next year, they saw unemployment hitting double digits and did not expect all the jobs that have been lost to return until 2012.

“Wage growth will be only 1% this year and 2.2% next year: the slowest two-year period on record. That leaves the outlook for consumer spending, which typically accounts for two-thirds of gross domestic product, fairly bleak. Next year it will grow at an anaemic 1.6%, the economists predict, while car sales will not bounce much from this year’s 40-year low.

“‘From a technical standpoint [the recession] is probably over, but that doesn’t mean in any way shape or form that it’s over from the point of view of an awful lot of people,’ said Dr Tony Cherin, finance professor at San Diego State University.

“But they upgraded their expectations for real gross domestic product growth, forecasting it to rise at a pace of 2.9% in the second half of this year and 3% next year. They think the housing market will recover enough in 2010 to contribute to overall growth for the first time in five years.

“Business investment will also pick up next year, they reckon, while corporate profits will rise 11% and the S&P 500 will add 7.5%.”

Source: Sarah O’Connor, Financial Times, October 13, 2009.

MoneyNews: Soros - bankrupt banks hamper recovery

“Economic recovery in the United States will be sluggish thanks to ‘bankrupt’ financial institutions and debt-laden consumers, says billionaire investor George Soros.

“US financial institutions in the Americas have written down or lost $1.1 trillion in the last two years, while savings rates have risen to the highest levels in 24 years as wary consumers tighten their purse strings, according to Bloomberg.

“‘The United States has a long way to go,’ Soros said at an International Monetary Fund and World Bank meeting in Istanbul, Turkey.

“Soros urged leaders to stick with plans to beef up regulation, which could become difficult once recovery moves ahead.

“‘It will be very difficult to accomplish,’ Soros says.”

“‘The crash of 2008 now seems like a bad dream and people like to treat it like a bad dream and forget about it and get back to business as usual.’

“Economic indicators suggest recovery is taking place and the recession is thawing or even ending.

“‘I see the risk of a stock market correction, especially when the markets now realize that the recovery is not rapid and V-shaped, but more like U-shaped,’ says Nouriel Roubini, a New York University economic professor who is said to have accurately predicted the extent of the current financial crisis.

“‘That might be in the fourth quarter or the first quarter of next year,’ says Roubini, according to Marketwatch.”

Source: Forrest Jones, MoneyNews, October 12, 2009.

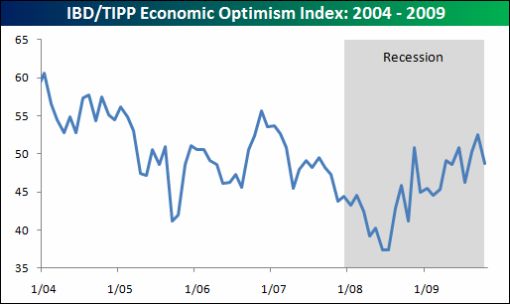

Bespoke: Long-term downtrend in confidence continues

“It’s increasingly becoming a glass half empty mood in the US. This month’s index of Consumer Confidence by IBD/TIPP showed that sentiment declined 7.2% from 52.5 to 48.7. For this index, readings above 50 indicate net optimism and readings below indicate pessimism. While the index is still near its recent highs, from a longer-term perspective, the five-year downtrend is somewhat concerning. As shown in the chart below, the index peaked above 60 in 2004, then made a lower high back in late 2006, and now is showing signs of another lower high in 2009. Is it a faulty index, or to borrow a line from former President Carter, are American consumers stuck in a crisis of confidence?”

Source: Bespoke, October 13, 2009.

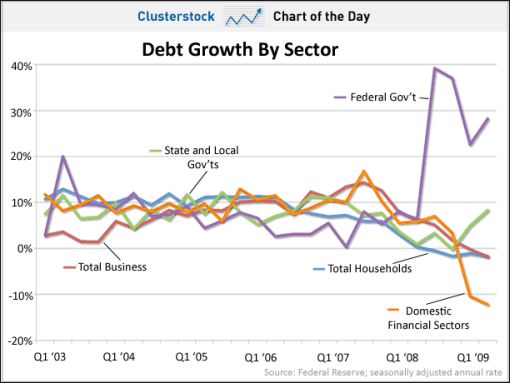

Clusterstock: The government debt explosion

“The growth of government debt has ‘decoupled’ from the rest of the economy.

“While households, businesses and the financial sector reduce leverage, public sector debt growth has simply exploded. As you can see from the chart, every non-governmental sector of the economy is now in debt reduction mode while governmental debt is growing a breakneck speeds.”

Source: John Carney and Kamelia Angelova, Clusterstock - Business Insider, October 13, 2009.

Asha Bangalore (Northern Trust): Q3 consumer spending expected jump likely, but muted growth in Q4

“Retail sales in September fell 1.5% after a 2.2% gain in August. These headline numbers reflect the swings in auto sales brought about by the lift from the temporary ‘Cash for Clunkers’ program. Excluding autos, retail sales increased 0.5% in September following a 1.0% increase in August.

“Furthermore, the sharp increase in gasoline prices in August translated into corresponding gains of gasoline purchases in the retail sales report. Excluding autos and gasoline, retail sales increased 0.4% in September after a 0.6% advance in August.

“The main message is that retail sales in September have been impressive with purchases of furniture (+0.9%), apparel (+0.5%) and general merchandise (+0.5%) posting significant increases which will add up to a strong increase in consumer spending in the third quarter (+3.0%) compared with a 0.9% drop in the second quarter. The absence of the ‘Cash for Clunkers’ program implies that consumer spending will be positive but show only muted growth in the fourth quarter.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 14, 2009.

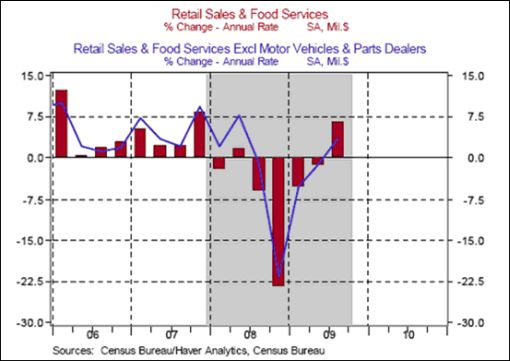

Clusterstock: The retail sales second derivative is on fire

“Dissecting today’s [Wednesday] advance retail sales data shows that trends improved for everything, except auto-related sales due to cash for clunkers. This is strong.

“The data beat expectations, with overall retail sales down 1.5% vs. an expected negative 2.1%. While 1.5% is the largest drop since December of last year, it was due to the end of cash for clunkers.

“The chart below takes September’s year over year (YoY) sales change (Sep 09 vs. Sep 08) and subtracts August’s year over year sales change (Aug 09 vs. Aug 08). It thus shows the change in change. Yes, this matters: American retail trends have to become less negative before they go positive.

“And that’s exactly what is happening. While sales continued to fall for many categories, the rate of decline slowed down substantially, improving by the amount in green shown below for each.”

Source: Vincent Fernando, Clusterstock - Business Insider, October 14, 2009.

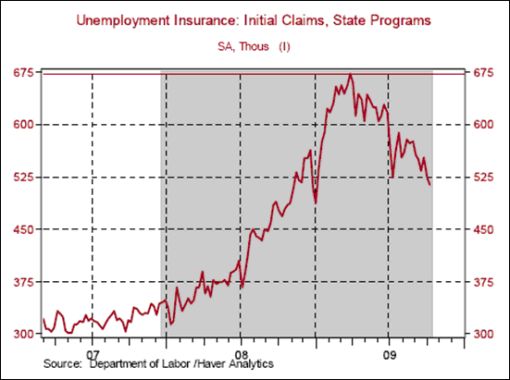

Asha Bangalore (Northern Trust): The quandary between initial claims and total continuing claims

“Initial jobless claims fell 10,000 to 514,000 during the week ended October 10. This reading is the lowest since March 2009 when initial jobless claims peaked at 674,000. This is good news, firms are not hiring but the pace of firing has slowed. Continuing claims, which lag initial claims by one week, declined 75,000 to 5.992 million and the insured unemployment rate moved down one notch to 4.5%. Continuing claims have held above the 6-million mark for six straight months.

“However, total claims including continuing claims and claims under the Extended Benefits Program and Emergency Unemployment Compensation Program have advanced to nearly 10 million. The good news here is that total continuing claims appear to have peaked; they have held between 9.86 million and 9.89 million for the four weeks ended September 26, with the latest weekly reading at the lower end of this range. We will be tracking these numbers closely for signs of improvement in the labor market.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 15, 2009.

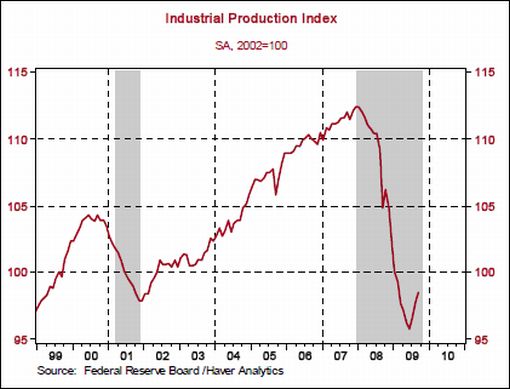

Asha Bangalore (Northern Trust): Widespread strength in factory report

“Industrial production increased 0.7% in September, following an upwardly revised 1.2% gain in the prior month. The industrial production index hit the cycle low in June and has since risen every month.

“In the third quarter, industrial production rose at an annual rate of 5.2%, the first increase since the first quarter of 2008. Production at the nation’s mines (0.7%) advanced while that of utilities (-0.7%) fell in September.

“Factory activity, which excludes mining and utilities and makes up roughly 85% of industrial production, moved up 0.9% after revised gains of 1.2% in each of the prior two months. In the third quarter, factory production advanced at an annual rate of 8.9%, the largest gain since the fourth quarter of 1987!

“The operating rate of the factory sector has increased to 67.5% in September from a record low of 65.1% in June 2009. The overall tone of the industrial production report is positive and confirms that an economic recovery is underway.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 16, 2009.

Bespoke: Philly Fed positive three months in a row

“If you needed more evidence that the recession that began in December 2007 has ended, this morning’s [Thursday] Philly Fed report should provide it. While the actual number came in below forecasts (11.5 vs 12.0), it was still positive for the third straight month. The last time this indicator was positive for three straight months was from September through November 2007, which was the last three months leading up to the start of the recession.”

Source: Bespoke, October 15, 2009.

Asha Bangalore (Northern Trust): Restocking - one of the conduits of economic growth in the months ahead

“Business inventories dropped 1.5% in August, marking the twelfth consecutive monthly drop. In the meanwhile, business sales have risen for three straight months, inclusive of a 1.0% increase in August.

“As a result of the drop in inventories and gain in sales, the inventories-sales ratio plummeted to 1.33 in August from 1.36 in July and it is a sharp reduction from the cycle high of 1.46 in January 2009. Starting from the end of the third quarter of 2008 businesses have been liquidating stocks in response to the weakness in demand conditions. As the economy recovers, inventories will add to real GDP growth, some of which is already apparent, particularly in the auto sector.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 14, 2009.

Asha Bangalore (Northern Trust): Inflation expectations non-threatening

“The Fed is in the most favorable spot in the near term with regard to inflation because the excess capacity in the economy allows the Fed to maintain a focus on economic growth and leave inflation on the back burner, for now. Moreover, inflation expectations are also non-threatening at the present time. Inflation will emerge as a major concern after there is self-sustaining economic growth.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 15, 2009.

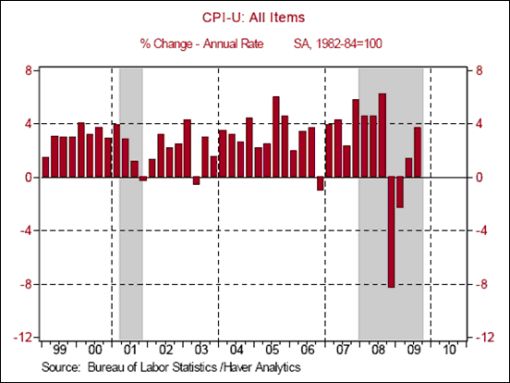

Asha Bangalore (Northern Trust): Inflation remains a non-issue, for now

“The Consumer Price Index (CPI) increased 0.2% in September after a 0.4% increase in the prior month. In the third quarter, the CPI has increased 3.6% after a 1.3% gain in the second quarter. On a year-to-year basis, the CPI fell 1.3% in September. The food price index dropped 0.1% during September vs. a 0.1% increase in August. The energy price index moved up 0.6% in September compared with a 4.6% jump in the previous month.

“The core CPI, which excludes food and energy, increased 0.2% in September after two consecutive monthly gains of 0.1%. The core CPI has risen 1.5% from a year ago in September, following a cycle low gain of 1.44% in August.”

Source: Asha Bangalore, Northern Trust - Daily Global Commentary, October 15, 2009.

MarketWatch: Banks cutting back on loans to businesses

“US banks are reducing their lending at the fastest rate on record, tightening the credit squeeze and threatening to leave many otherwise viable businesses unable to borrow money to expand their businesses, meet their payroll or refinance their maturing debts.

“According to weekly figures provided by the Federal Reserve, total loans at commercial banks have fallen at a 19% annual rate over the past three months, while loans to businesses have dropped at a 28% annualized pace.

“Last autumn, bank lending temporarily expanded when other sources of funding from the shadow banking system dried up after the collapse of Lehman Bros. Since then, however, total outstanding bank loans have dropped at an accelerating pace.

“The decline in bank lending mostly affects smaller businesses. Larger corporations have alternative sources of funding, including retained earnings, corporate bonds, securitized loans and new equity. Those other sources of capital have increased in recent months, but not enough to offset the decline in bank lending.

“In the first and second quarters, the US private sector consumed more capital than it raised for the first time in more than 60 years. Negative net investment is ‘the hallmark of depression and difficult to reverse’, said economist Leigh Skene of Lombard Street Research.

“The big drop in credit also shows up as slower money growth. In the past 13 weeks, the money supply has fallen 0.3%. Most new money is created by borrowing, as banks credit the borrower’s account with the proceeds of a loan. Conversely, the money supply is reduced when debts are paid off or written off. Deflation is not a threat - it’s already here.

“The question is whether the decline in lending will be reversed soon.

“If the drop-off in lending is mainly due to weak demand by businesses, then there’s some hope that the recent upward momentum in industrial output and sales could lead to more optimistic business sentiment, greater demand for capital, and more lending by banks.

“But if the decline is mainly due to weak banks unable or unwilling to lend, then a turnaround in credit creation may have to wait until banks’ balance sheets are repaired, a process that could be delayed by further expected defaults in consumer loans, mortgages and commercial real-estate loans.”

Source: Rex Nutting, MarketWatch, October 9, 2009.

Financial Times: US bank results highlight recovery gap

“Bumper third quarter profits at Goldman Sachs and another loss for Citigroup on Thursday highlighted the gap between the financial resilience of Wall Street and the woes of Main Street, fresh evidence that two Americas are emerging from the crisis.

“The diverging performance of investment banks such as Goldman and the retail banking operations of the banks such as Citi is problematic for an Obama administration that wants a strong Wall Street but is also under pressure to tackle the plight of ordinary people.

“‘When you have unemployment creeping towards 10% and a sluggish economy, stories of huge profits and huge bonuses … could create difficulties if [the president] needs any more stimulus,’ said Norman Ornstein, a political analyst at the American Enterprise Institute.

“Goldman announced near-record earnings of $3.2 billion, boosted by surging profits in bond and currency trading - two activities that have become more profitable after the crisis reduced competition in financial markets and governments injected emergency funds into the banking system.

“Goldman’s profit, which was nearly four times higher than in the third quarter of 2008, underscores its status as one of the winners from a crisis that eliminated two rivals - Lehman Brothers and Bear Stearns - and hobbled others such as Citi, Merrill Lynch and UBS.

“Citi, by contrast, suffered its seventh loss in eight quarters as US consumers continued to fall behind on credit card bills and mortgage payments.

“‘US consumer credit remains the number one issue affecting our near-term results,’ said Vikram Pandit, Citi’s chief executive, after announcing the bank had suffered credit losses of $8 billion in the three months to September, largely in its consumer business.

“Citi, which has been bailed out with $45 billion of US taxpayers’ money, has suffered a total of more than $42 billion in credit losses since the beginning of 2008.

“The contrasting fortunes of Goldman and Citi suggest that Wall Street, which played a major part in the crisis and was one of its first victims, is recovering much faster than the rest of the US economy.”

Source: Francesco Guerrera, Greg Farrell and Anna Fifield, Financial Times, October 15, 2009.

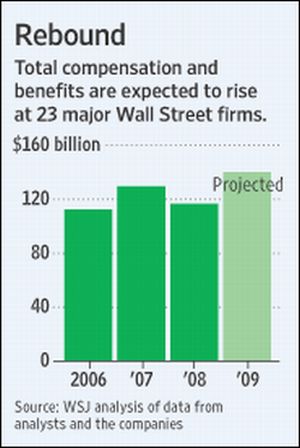

The Wall Street Journal: Wall Street on track to award record pay

“Major US banks and securities firms are on pace to pay their employees about $140 billion this year - a record high that shows compensation is rebounding despite regulatory scrutiny of Wall Street’s pay culture.

“Workers at 23 top investment banks, hedge funds, asset managers and stock and commodities exchanges can expect to earn even more than they did the peak year of 2007, according to an analysis of securities filings for the first half of 2009 and revenue estimates through year-end by The Wall Street Journal.

“Total compensation and benefits at the publicly traded firms analyzed by the Journal are on track to increase 20% from last year’s $117 billion - and to top 2007’s $130 billion payout. This year, employees at the companies will earn an estimated $143,400 on average, up almost $2,000 from 2007 levels.

“The growth in compensation reflects Wall Street firms’ rapid return to precrisis revenue levels. Even as the economy is sluggish and unemployment approaches 10%, these firms have been boosted by a stronger stock market, thawing credit market, a resurgence in deal making and the continuing effects of various government aid programs.”

Source: Aaron Lucchetti and Stephen Grocer, The Wall Street Journal, October 14, 2009.

Bespoke: 30-year fixed mortgage rate back below 5%

“For those worried that they missed the bottom in mortgage rates a few months ago, you’ve now got a second chance to refinance or lock in that home loan at less than 5%. As shown below, after spiking nearly 100 basis points off its low in late April, Bankrate.com’s national average for 30-year fixed mortgage rates hit 4.97% on Friday.”

Source: Bespoke, October 13, 2009.

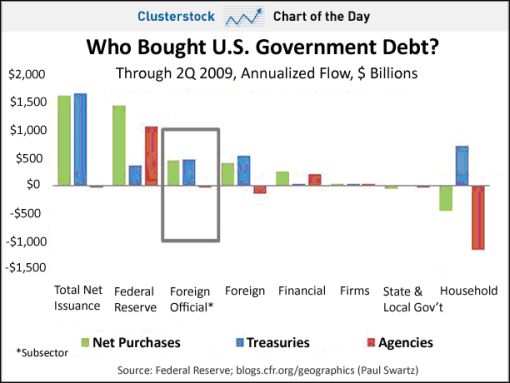

Clusterstock: Besides the Fed, nobody is buying agency debt

“Where would we be without the Fed and its printing press? There’s been a lot of debate about the appetite of foreign investors of our debt - Treasury auctions continue to be strong, even as noises emanate from overseas about wanting to dump the dollar.

“But here’s a stark fact, via the Council on Foreign Relations: Only the Fed is buying agency debt. Foreign buyers, who once consumed it voraciously, have been net sellers so far this year.”

Source: Joe Weisenthal and Kamelia Angelova, Clusterstock - Business Insider, October 8, 2009.

Bloomberg: Pimco’s Gross boosts government debt, cuts mortgages

“Bill Gross, who runs the world’s biggest bond fund at Pacific Investment Management Co. (Pimco), bought government debt last month and cut mortgage bond holdings to the lowest level since 2005 after he said this year that the US recession will lead to a period of less-than-average growth.

“Gross boosted the $185.7 billion Total Return Fund’s investment in Treasuries, so-called agency debt and other government-linked bonds to 48% of assets in September from 44% in August, according to Pimco’s website. The holdings are the most since August 2004.

“‘We’ve exchanged our mortgages for the government’s check,’ Gross, who is based in Newport Beach, California, said in an interview last month. He said he was buying longer-maturity Treasuries because of deflation concern.

“Treasuries rose in July, August and September, offering their first three-month gain in a year, Merrill Lynch & Co. indexes show, as optimism waned about the pace of economic recovery. Federal Reserve Vice Chairman Donald Kohn said this week inflation and growth will probably stay below the central bank’s objectives for some time, warranting very low interest rates for an ‘extended period’.

“The Total Return fund cut mortgage debt to 22%, the lowest level since February 2005, from 38%, according to the website.”

Source: Wes Goodman and Susanne Walker, Bloomberg, October 15, 2009.

Bespoke: Investment-grade corporate bond ETF breaks down

“Investment-grade corporate bonds have generally moved alongside the stock market throughout the bull market. In recent days, however, investment grade corporates have moved lower even as stocks have risen. Below is a chart of the iShares iBoxx Investment Grade Corporate Bond Fund ETF (LQD) since the March lows. As shown, the ETF had been in a tight uptrend for months until just last week when it broke below its 50-day moving average. With the uptrend now broken, it will be interesting to see what, if any, impact this has on equity markets.”

Source: Bespoke, October 12, 2009.

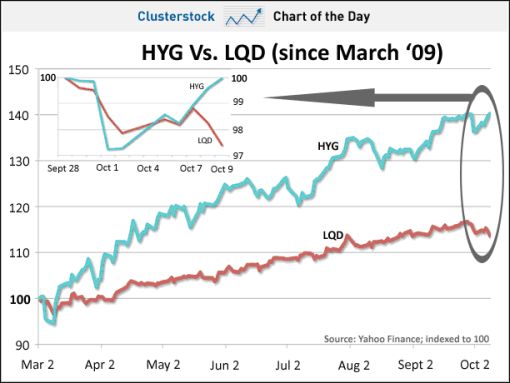

Clusterstock: Investors are only interested in high-yield junk

“Today’s chart shows not only that high-yield junk debt (HYG) has decimated safe debt (LQD) since the market lows, but that in recent days the situation has gotten really extreme.

“Investment-grade debt has started to break down over the past couple of weeks, clearly breaking an uptrend, while the risky stuff keeps on powering higher.”

Source: Joe Weisenthal and Kamelia Angelova, Clusterstock - Business Insider, October 12, 2009.

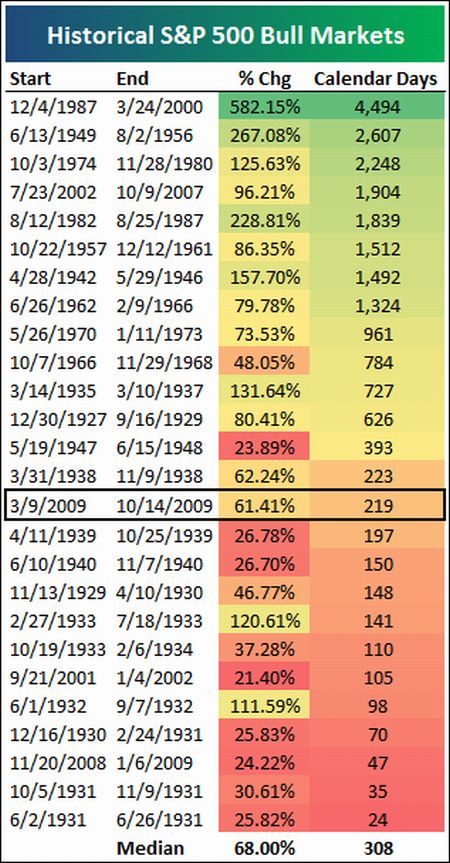

Bespoke: Bull market check-up

“Below we have updated our table of historical S&P 500 bull markets (at least a 20% gain that was preceded by at least a 20% decline) since index data begins in 1927. The table is sorted by bull market length. The current bull market that started on March 9 is now 219 calendar days with a gain of 61.41%. As shown, the median gain for all bull markets has been 68%, and the median length has been 308 days. The current bull is still below the median in terms of both gains and days. However, there aren’t a lot of bulls bunched up around the median, and there is a pretty big deviation between all of them. Bottom line though is that this is definitely a bull market.”

Source: Bespoke, October 15, 2009.

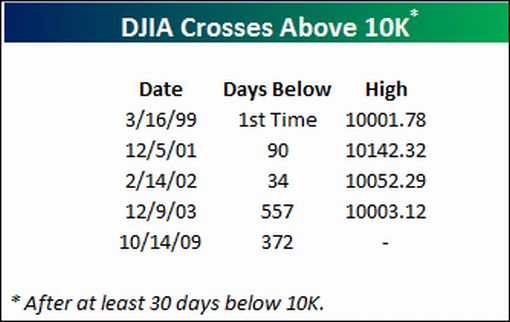

Bespoke: Break out the Dow 10,000

“For the fourth time in the index’s history, the Dow has broken above 10,000 after trading below that level for at least a month. While the media would have you believe otherwise, the more this occurs the less exciting it becomes. Call us at Dow 100K.”

Source: Bespoke, October 14, 2009.

By Dr Prieur du Plessis

Dr Prieur du Plessis is an investment professional with 25 years' experience in investment research and portfolio management.

More than 1200 of his articles on investment-related topics have been published in various regular newspaper, journal and Internet columns (including his blog, Investment Postcards from Cape Town : www.investmentpostcards.com ). He has also published a book, Financial Basics: Investment.

Prieur is chairman and principal shareholder of South African-based Plexus Asset Management , which he founded in 1995. The group conducts investment management, investment consulting, private equity and real estate activities in South Africa and other African countries.

Plexus is the South African partner of John Mauldin , Dallas-based author of the popular Thoughts from the Frontline newsletter, and also has an exclusive licensing agreement with California-based Research Affiliates for managing and distributing its enhanced Fundamental Index™ methodology in the Pan-African area.

Prieur is 53 years old and live with his wife, television producer and presenter Isabel Verwey, and two children in Cape Town , South Africa . His leisure activities include long-distance running, traveling, reading and motor-cycling.

Copyright © 2009 by Prieur du Plessis - All rights reserved.

Disclaimer: The above is a matter of opinion and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Do your own due diligence.

Prieur du Plessis Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.