Euro-zone Credit Crisis and China Shanghai Commodites Market Shakeout

Interest-Rates / Credit Crisis 2010 Jun 03, 2010 - 09:28 AM GMTBy: Gary_Dorsch

Until mid-April, few traders knew much about the credit default swap (CDS) markets. They’re traded on an unregulated, over-the-counter market, and far from the public’s view. Yet nowadays, the CDS market has become a major battleground between high-stakes speculators and Euro-zone politicians, with the fate of the Euro currency hanging in the balance. In turn, the violent swings in the CDS markets are having a profound impact on the global bond, commodity, currency, and stock markets.

Until mid-April, few traders knew much about the credit default swap (CDS) markets. They’re traded on an unregulated, over-the-counter market, and far from the public’s view. Yet nowadays, the CDS market has become a major battleground between high-stakes speculators and Euro-zone politicians, with the fate of the Euro currency hanging in the balance. In turn, the violent swings in the CDS markets are having a profound impact on the global bond, commodity, currency, and stock markets.

Credit default swaps have existed since the early 1990’s, but the volume of trading began to increase dramatically in 2003. By December 2007, the CDS markets had grown in size to $62-trillion of contracts outstanding, before shrinking to $38-trillion by the end of 2008. Huge throngs of “naked” short sellers were wiped-out in the CDS market following after Lehman Brothers defaulted on $365-billion of liabilities, which were settled at just 8-cents on the dollar.

Fourteen months later, the obscure CDS markets were again at the center of another major financial crisis, this time, raising the specter of a sovereign debt default. CDS traders were among the first to recognize that the government of Greece was technically insolvent, and unable to repay its €300-billion of outstanding debt. The size of Greece’s debt rivals the size of Lehman’s, when it defaulted, and is almost four times of the size of Argentina’s debt, when it defaulted in 2001.

Typically, a bond-holder can hedge against the risk of default by purchasing a CDS contract, and making quarterly insurance payments to the CDS seller. If a company or a national government defaults on its debt obligations, seeks a restructuring, or declares bankruptcy, the CDS seller is obligated to pay the CDS buyer the par value of the bond, in exchange for physical delivery of the bond. Most CDS contracts are in the $10-to-$20-million range with maturities of 1-to-10-years.

However, speculators can buy “naked” CDS contracts without actually owning the underlying bond. Likewise, sellers of CDS contracts might not have sufficient funds to cover their obligations, in the event of a default. These “naked” credit default swaps constitute the majority of trading volume, and permit banks and hedge funds to place bets on whether or not a company, or even a country, will default on it debts.

However, speculators can buy “naked” CDS contracts without actually owning the underlying bond. Likewise, sellers of CDS contracts might not have sufficient funds to cover their obligations, in the event of a default. These “naked” credit default swaps constitute the majority of trading volume, and permit banks and hedge funds to place bets on whether or not a company, or even a country, will default on it debts.

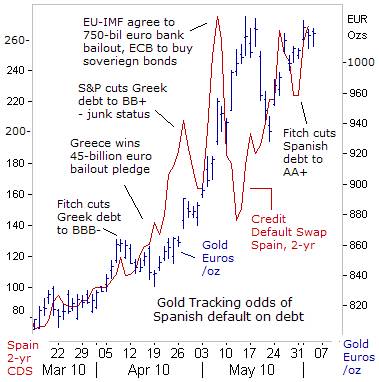

The nature of CDS trading, - which doesn’t require reporting of transactions to a government agency, - is such, that CDS speculators have an incentive to push companies or countries toward bankruptcy. CDS traders nearly toppled the Greek finance ministry, and are now betting on defaults in Euro-zone junk bonds. Attracted to the highly indebted Greek bond market like vultures to a decaying corpse, the CDS traders at major banks and hedge funds moved in for the kill in April.

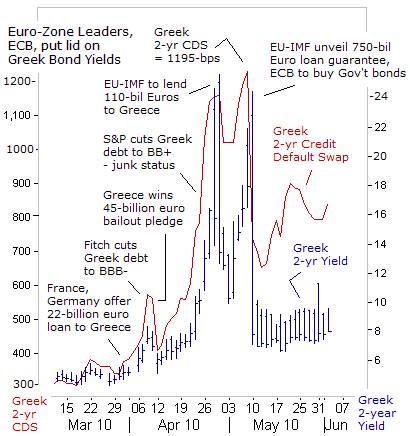

Trading in credit default swaps linked to Greek debt surged over the past year, prior to the upward explosion in CDS rates in late April and early May. The overall amount of insurance on Greek debt hit $85-billion in February, compared with $38-billion a year earlier. CDS speculators nearly hit the jackpot on May 7th, when the cost of insuring $10-million of Greek bonds soared to $1.2-million, worsening the budgetary plight of Greece and bringing it closer the specter of default.

Prior to the climactic surge in late April and early May, each time CDS traders bid-up the cost of insuring Greek bonds against default, Euro-zone politicians and the IMF were quickly forced to ante-up more bailout money. Initially, Euro-zone politicians pledged a paltry €22-Euros to prevent Athens from defaulting on its debts. When that gambit failed, the ante was raised to €45-billion.

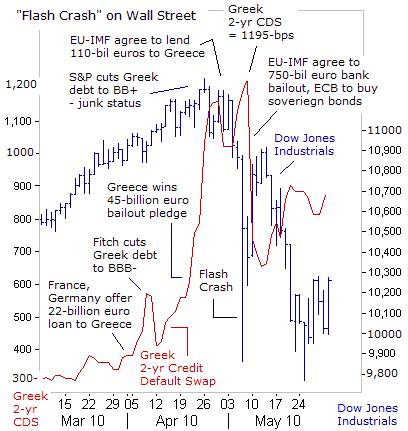

However, on April 26th, the S&P credit rating agency, - which usually lingers far behind the credit default curve, lit a fire in the CDS tinderbox, roiled Euro-zone politicians and shocked the global markets, by downgrading Greece’s €300-billion of debt three notches to junk status, at BB+. Greek CDS rates soared to 1,200-bps, and yields on Greece’s two-year notes jumped to 25.8-percent. Euro-zone politicians and the IMF quickly raised the ante for the Greek bailout to €110-billion.

German finance minister Wolfgang Schauble had warned on April 20th, of another global financial meltdown. “We cannot allow the bankruptcy of a Euro member state like Greece to turn into a second Lehman Brothers,” he told Der Spiegel. “Greece’s debts are all in Euros, and it isn’t clear who holds how much of those debts. The consequences of a national bankruptcy would be incalculable. Greece is just as systemically important as a major bank,” Schauble warned.

German finance minister Wolfgang Schauble had warned on April 20th, of another global financial meltdown. “We cannot allow the bankruptcy of a Euro member state like Greece to turn into a second Lehman Brothers,” he told Der Spiegel. “Greece’s debts are all in Euros, and it isn’t clear who holds how much of those debts. The consequences of a national bankruptcy would be incalculable. Greece is just as systemically important as a major bank,” Schauble warned.

On May 6th, Greece’s 2-year CDS rate surged to a record 1,195-basis points, and triggered the historic “flash crash” on Wall Street, - an intra-day, 1,000-point meltdown in the Dow Jones Industrials, climaxed by a shocking 700-point drop, in less than 20-minutes, to below the psychological 10,000-level. Since the mainstream media was unfamiliar with the movements of the Greek CDS market, it peddled a story, that a computer glitch caused the “flash crash.”

The rebellious CDS speculators in Greek bonds, refused to fold their cards, knowing that Athens would need to raise €50-billion for each of the next five years, in order to roll-over debts and pay interest. That adds up to €250-billion, easily topping the EU’s €110-billion bailout offer. On May 8-9th, European politicians, finance chiefs, central bankers, and officials from the IMF were taken aback, by the brazen CDS traders, and huddled behind closed doors for an emergency summit, trying to devise a decisive plan of action, that could stamp out the speculative attack against the Euro and to bring some calm into the Greek bond market.

“We now see wolf-pack behavior, and if we will not stop these packs, they will tear the weaker countries apart,” Swedish Finance chief Anders Borg told reporters before the meeting. “We need resources to stop the market turmoil. If this goes on for more than a couple of days it will be very, very problematic for the recovery,” Borg warned on May 8th. French Prime Minister Francois Fillon added, “The joint action taken to save Greece will defeat and put an end to speculation which has been unleashed against this country and which represents an attack on the entire Euro zone.”

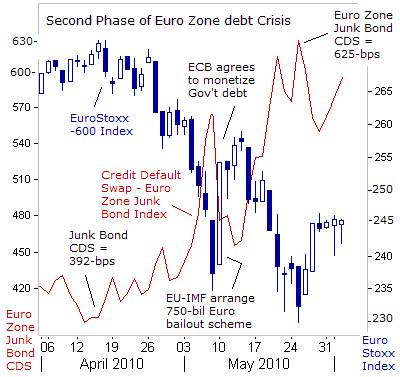

On May 10th, after two-days of deliberations, the EU-leaders unveiled the financial equivalent of “shock-and-awe,” – a €750-billion package of standby funds and loan guarantees that could be tapped by Euro-zone governments shut-out of credit markets, plus central bank purchases of bonds, to steady markets, - all designed to crush CDS speculators by its sheer scale. The European Central Bank (ECB) immediately began implementing its part of a deal, - unleashing the “nuclear option,” - buying Greek and Portuguese government bonds in the open market.

On May 10th, after two-days of deliberations, the EU-leaders unveiled the financial equivalent of “shock-and-awe,” – a €750-billion package of standby funds and loan guarantees that could be tapped by Euro-zone governments shut-out of credit markets, plus central bank purchases of bonds, to steady markets, - all designed to crush CDS speculators by its sheer scale. The European Central Bank (ECB) immediately began implementing its part of a deal, - unleashing the “nuclear option,” - buying Greek and Portuguese government bonds in the open market.

With the ECB pledging to buy Greek bonds, yields on its two-year note plunged in the blink of an eye, from an intra-day high of 24%, to 7.5-percent. Since May 10th, the ECB has effectively locked Greece’s two-year yield between 7% and 9.5-percent. However, the cost of insuring Greek debt is still hovering around 850-bps today, very high by historical standards. CDS traders reckon that at some point, Athens might grow tired of trying to pay-off an insurmountable mountain of debt, and will demand a restructuring, - a haircut of 50% or more for its creditors.

Since May 10th, the EU’s “shock and awe” effect has worn-off. The EuroStoxx-600 Index briefly fell to new lows on May 25th, and the Athens stock index fell to within 5% of its March 2009 lows. The Euro failed to gain any traction, and is still sliding lower along a slippery slope towards $1.20 versus US-dollar. While the “Big-Bang” bailout has subdued the threat of a Greek debt default, the next lethal phase of the European debt crisis is starting to materialize, - a frightful situation where European banks become unwilling to lend money to the private sector.

Specter of Euro-zone Credit Crunch

There are latent fears that a Euro-zone “credit crunch,” is looming on the horizon which could put the $14-trillion Euro-zone economy, into a deep freeze. On May 31st, the ECB warned that Euro zone banks could face a new wave of loan losses - up to €195-billion of losses over the next 18-months. Euro-zone banks would need to raise additional capital in order to cover expected losses of €90-billion this year and €105-billion in 2011, on top of €238-billion in bad debts already written off. Banks have already begun hoarding a record amount of cash at the ECB, opting for the safety of the central bank, rather than risk more profitable lending in the private sector.

Euro-zone banks are finding it very difficult to find buyers for their debt in the capital markets. Bond issuance has slumped to $2.6-billion in May, down from $82-billion in January. Also, indicative of a potential credit crunch in the offing, the credit default swap rate for the Euro-zone’s top-50 junk bond index, measuring lesser credit worthy companies, jumped as high as $625,000 on May 25th, from around $460,000 four weeks ago. Each upward surge in Euro-zone junk bond CDS rates has ignited a sell-off in the EuroStoxx-600 Index. Conversely, each decline in CDS junk bond rates has lifted the fortunes of the Euro-zone stock market.

Euro-zone banks are finding it very difficult to find buyers for their debt in the capital markets. Bond issuance has slumped to $2.6-billion in May, down from $82-billion in January. Also, indicative of a potential credit crunch in the offing, the credit default swap rate for the Euro-zone’s top-50 junk bond index, measuring lesser credit worthy companies, jumped as high as $625,000 on May 25th, from around $460,000 four weeks ago. Each upward surge in Euro-zone junk bond CDS rates has ignited a sell-off in the EuroStoxx-600 Index. Conversely, each decline in CDS junk bond rates has lifted the fortunes of the Euro-zone stock market.

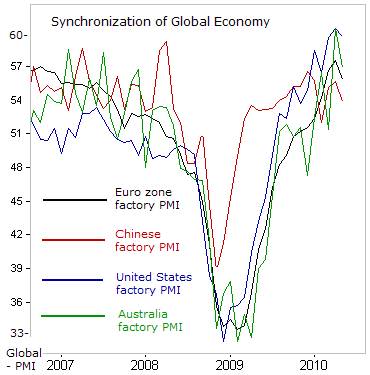

The Euro-zone is a major player on the world economic stage, accounting for roughly 22% of the world’s economic output. The Euro-zone buys 20% of China’s exports, and 15% of Latin America’s, and nearly a quarter of S&P-500 multinational income is earned by US-affiliates located in Europe. Given the increasing synchronization of the world’s economy, any sharp downturn in the Euro-zone economy, precipitated by a lending freeze, could undermine global commodity and stock markets.

Traders got their first look at what a European credit crunch might do to the global economy on June 2nd. The Euro-zone’s factory Purchasing Managers’ Index (PMI) for May sank to 55.8 from a reading of 57.6 in April. The factory sector is still where global recessions tend to begin and end. For this reason, the factory PMI’s in the top industrialized nations are watched very closely, setting the tone for the upcoming month and other key economic indicators.

The Euro-zone’s factory PMI figures might have already peaked in April, since Euro-zone governments are starting to remove large dosages of fiscal stimulus. EU leaders have rescued the Euro-zone banks from enormous losses, but also vowed to cut their budget deficits to 3% of GDP, to meet a 2013 deadline for compliance with EU stability criteria. In order to do so, the Euro-zone countries and Britain will have to slash their budget deficits by a total of €400-billion ($492-billion).

Greece is aiming to reduce its budget deficit by €30-billion over the next three years through wage and pension cuts, slashing social programs and a 2% increase in VAT (sales tax) to 23-percent. Spain voted to cut spending by €80-billion, with a one vote majority in parliament. To this end, 13,000 jobs in the public service will be cut, the salaries of state employees will be reduced by 5%, and pensions frozen. Britain’s budget deficit will be cut over the next four years by more than $120-billion. This will include slashing 300,000-jobs in the public service and a freeze on public sector pay. Italy agreed to spending cuts of €25-billion by 2012.

Greece is aiming to reduce its budget deficit by €30-billion over the next three years through wage and pension cuts, slashing social programs and a 2% increase in VAT (sales tax) to 23-percent. Spain voted to cut spending by €80-billion, with a one vote majority in parliament. To this end, 13,000 jobs in the public service will be cut, the salaries of state employees will be reduced by 5%, and pensions frozen. Britain’s budget deficit will be cut over the next four years by more than $120-billion. This will include slashing 300,000-jobs in the public service and a freeze on public sector pay. Italy agreed to spending cuts of €25-billion by 2012.

China Tightens Liquidity, Clobbers Industrial Commodities

Whereas the ECB has just crossed the Rubicon, by embracing “Quantitative Easing, (QE), - or printing vast quantities of Euros in the year ahead, in order to monetize the debts of the Euro’s most reckless delinquent borrowers, - the People’s Bank of China (PBoC), is moving in the opposite direction, - removing a large chunk of the stimulus that it injected into the Shanghai money markets last year.

PBoC chief Zhou Xiaochuan said on May 24th, that domestic issues are by far the most important factors in determining Chinese monetary policy, and the European liquidity crunch wouldn’t necessarily affect the central bank’s calculations on when to hike interest rates. Zhou thinks the global economy will likely maintain the pace of its recovery despite the Euro-zone’s woes. Therefore, there’s a risk that the PBoC might continue to tighten its monetary policy in the months ahead, despite signs of rough patch in global factory activity developing in May.

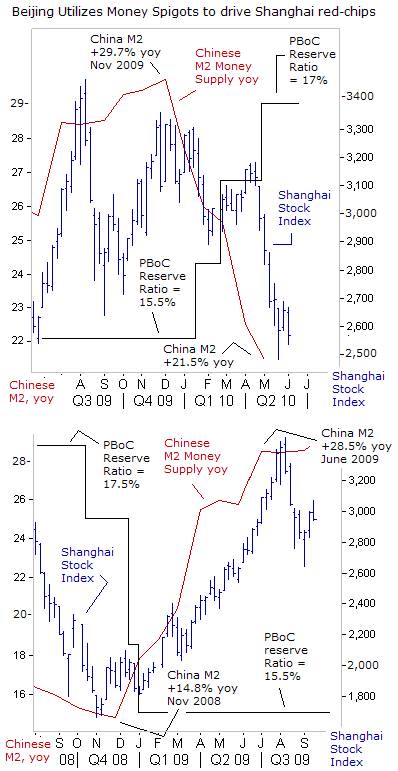

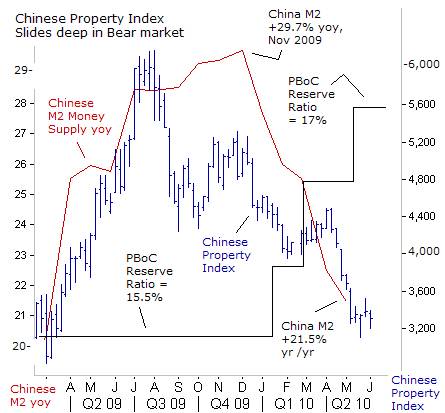

Even in the midst of the turmoil in Europe, on May 2nd, the PBoC lifted the reserve requirement ratio for its largest banks by 50-basis points, to 17%, its third increase this year, thus draining about 900-billion yuan ($132-billion) out of the Chinese banking system. The PBoC is trying to contain an accelerating inflation rate, while deflating a housing price bubble. April’s 12.8% jump in property prices in China’s top-70 cities, defied the government’s crackdown on speculation. Meanwhile, producer prices jumped +6.8%, and consumer prices climbed +2.9%, up from +2.4% in March. New lending of 774 billion yuan ($113 billion) was far above target, and retail sales were +18.5% higher in April from a year earlier.

In order to deflate asset bubbles, the PBoC aims to reduce bank lending 22% this year, from a record $1.4-trillion of yuan loans extended in 2009. The PBoC has also stepped up its drainage of yuan via open market operations. By tightening the money spigots, the PBoC has slowed the growth of the Chinese M2 money supply, from a +29.7% clip in November, to +21.5% in April. In turn, by draining excess liquidity, the PBoC has sucked some helium out of the Shanghai stock market.

While the benchmark Shanghai Composite Index has tumbled 22% this year, to as low as 2,568-points, - the worst performing sector in the marketplace is the property index, tracking 34 real estate firms, which briefly fell below the 3200-level, or 48% below its high of 6,137 seen in July 2009. China’s property market is vulnerable to a crash, warned Li Daokui, a top advisor to the PBoC. “China’s housing market problems combine a possible bubble with the risk of social discontent,” he said.

While the benchmark Shanghai Composite Index has tumbled 22% this year, to as low as 2,568-points, - the worst performing sector in the marketplace is the property index, tracking 34 real estate firms, which briefly fell below the 3200-level, or 48% below its high of 6,137 seen in July 2009. China’s property market is vulnerable to a crash, warned Li Daokui, a top advisor to the PBoC. “China’s housing market problems combine a possible bubble with the risk of social discontent,” he said.

Beijing’s efforts to deflate the real estate bubble, include measures that restrict pre-sales by developers, curbs loans for third-home purchases, doubled mortgage rates, and lifted down-payments to 50% for second-home purchases. Property sales in Beijing, Shanghai and Shenzhen fell as much as 70% in May as developers delayed sales following government tightening measures. A tax on residential real estate has been submitted to the Chinese central government for review.

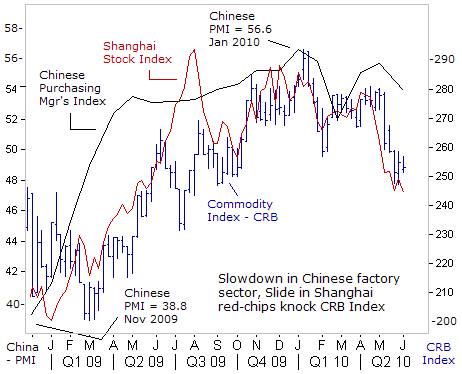

The sharp slide in Shanghai red-chips, led by a slumping property sector, combined with a decline in China’s Purchasing Managers’ Index to a reading of 53.9 in May, from 55.7 in April, and mixed with the headwinds from the Euro zone credit crunch, conspired to knock the Reuters CRB Index of 19 commodity futures -8.2% lower in May, the biggest monthly plunge since the collapse of Lehman Brothers.

Traders are betting that the slide in the CRB commodity index is signaling a peak in global factory activity. According to the CFTC, speculative net-long positions, or bets on rising prices, for 16 commodity futures have plunged 33% in the past three weeks. Industrial commodity kingpins, such as copper and crude oil, have tumbled by roughly 16% from their highest levels in April. The shakeout in the  CRB Index, might also reflect fears of smaller position limits in the US-commodity markets, under a financial reform bill, that is under debate in Congress.

CRB Index, might also reflect fears of smaller position limits in the US-commodity markets, under a financial reform bill, that is under debate in Congress.

The outlook for the Chinese economy, is of utmost importance to speculators in key industrial commodities, since Chinese consumption as a percentage of global demand last year, was 68% for nickel, 44% for aluminum, 36% for iron ore, and 10% for crude oil. In addition to a potential credit crunch in the Euro-zone, a big risk for industrial commodities is a miscalculation by Beijing, - in tightening its monetary policy too aggressively. A bursting of the Chinese real-estate market may put China’s 8% annual growth target in jeopardy.

Gold Knows what no One Knows!

Despite the 15% slide in key industrial commodities, the Gold market remains resilient, fighting off nagging worries about deflation, or a downturn in the global economy. Instead, Gold knows what know one knows! At the end of the day, the nations of Greece, Portugal, and Spain are technically insolvent, and living on artificial life support, courtesy of their wealthier neighbors.

As much as French and German taxpayers resent the idea of guaranteeing the debts of their delinquent neighbors, Greek and Spanish workers abhor the idea of working slavishly for decades to pay-off the debt, accumulated by corrupt politicians. The only easy way out of dealing with the Euro-zone debt crisis is the ECB’s monetization of the debts, by printing vast quantities of Euros, to buy sovereign bonds. Thus, gold has soared to above the psychological 1,000-euros /oz level in recent weeks.

So far, the ECB has bought about €35-billion of sovereign debt, mainly Greek. It probably needs to buy debt on a far larger scale, in order to prevent yields on Club-Med bonds from rising again. Spanish 10-year bond spreads have already widened to 180-basis points over German Bunds, a record since before the credit crisis began. Italy’s odds of default have followed Spain’s in sympathy. Italian CDS rates are trading at 240-basis points, a record high, and 10-basis points higher than before the ECB’s bond-buying scheme was launched on May 10th. Spanish CDS rates are trading at 270-basis points, also near a record.

So far, the ECB has bought about €35-billion of sovereign debt, mainly Greek. It probably needs to buy debt on a far larger scale, in order to prevent yields on Club-Med bonds from rising again. Spanish 10-year bond spreads have already widened to 180-basis points over German Bunds, a record since before the credit crisis began. Italy’s odds of default have followed Spain’s in sympathy. Italian CDS rates are trading at 240-basis points, a record high, and 10-basis points higher than before the ECB’s bond-buying scheme was launched on May 10th. Spanish CDS rates are trading at 270-basis points, also near a record.

In addition to the bond buying spree, the ECB quietly injected €118-billion into the banking system last week the highest amount since the ECB flooded money markets with half-a-trillion Euros of ultra-cheap 1-year money in June 2009. At some point, depositors may fear that European banks are too exposed to Club-Med debt, and combined with the ECB’s money printing operations, could spark a flight into the king of currencies, a truest safe-haven in times of financial distress - Gold.

This article is just the Tip of the Iceberg of what’s available in the Global Money Trends newsletter. Subscribe to the Global Money Trends newsletter, for insightful analysis and predictions of (1) top stock markets around the world, (2) Commodities such as crude oil, copper, gold, silver, and grains, (3) Foreign currencies (4) Libor interest rates and global bond markets (5) Central banker "Jawboning" and Intervention techniques that move markets.

By Gary Dorsch,

Editor, Global Money Trends newsletter

http://www.sirchartsalot.com

GMT filters important news and information into (1) bullet-point, easy to understand analysis, (2) featuring "Inter-Market Technical Analysis" that visually displays the dynamic inter-relationships between foreign currencies, commodities, interest rates and the stock markets from a dozen key countries around the world. Also included are (3) charts of key economic statistics of foreign countries that move markets.

Subscribers can also listen to bi-weekly Audio Broadcasts, with the latest news on global markets, and view our updated model portfolio 2008. To order a subscription to Global Money Trends, click on the hyperlink below, http://www.sirchartsalot.com/newsletters.php or call toll free to order, Sunday thru Thursday, 8 am to 9 pm EST, and on Friday 8 am to 5 pm, at 866-553-1007. Outside the call 561-367-1007.

Mr Dorsch worked on the trading floor of the Chicago Mercantile Exchange for nine years as the chief Financial Futures Analyst for three clearing firms, Oppenheimer Rouse Futures Inc, GH Miller and Company, and a commodity fund at the LNS Financial Group.

As a transactional broker for Charles Schwab's Global Investment Services department, Mr Dorsch handled thousands of customer trades in 45 stock exchanges around the world, including Australia, Canada, Japan, Hong Kong, the Euro zone, London, Toronto, South Africa, Mexico, and New Zealand, and Canadian oil trusts, ADR's and Exchange Traded Funds.

He wrote a weekly newsletter from 2000 thru September 2005 called, "Foreign Currency Trends" for Charles Schwab's Global Investment department, featuring inter-market technical analysis, to understand the dynamic inter-relationships between the foreign exchange, global bond and stock markets, and key industrial commodities.

Copyright © 2005-2010 SirChartsAlot, Inc. All rights reserved.

Disclaimer: SirChartsAlot.com's analysis and insights are based upon data gathered by it from various sources believed to be reliable, complete and accurate. However, no guarantee is made by SirChartsAlot.com as to the reliability, completeness and accuracy of the data so analyzed. SirChartsAlot.com is in the business of gathering information, analyzing it and disseminating the analysis for informational and educational purposes only. SirChartsAlot.com attempts to analyze trends, not make recommendations. All statements and expressions are the opinion of SirChartsAlot.com and are not meant to be investment advice or solicitation or recommendation to establish market positions. Our opinions are subject to change without notice. SirChartsAlot.com strongly advises readers to conduct thorough research relevant to decisions and verify facts from various independent sources.

Gary Dorsch Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

|

Simon

03 Jun 10, 16:18 |

Good Work

Superb article! Many thanks |